IRS Forms

Power of Attorney for a Parent with the IRS: How Form 2848 Works in 2026

The short answer: to get power of attorney for a parent with the IRS, file Form 2848 — the IRS's own power-of-attorney form. A regular durable POA is not enough by itself. Form 2848 lets you speak to the IRS, receive your parent's notices, and negotiate on their behalf; Form 8821 grants view-only access.

You found the drawer — or the shoebox — full of unopened IRS envelopes at your parent's house, and every call to straighten it out ends the same way: the IRS won't tell you anything because the account isn't yours. That wall is real, but it comes down with one two-page form, and everything after it is a solvable money problem.

Form 2848 looks bureaucratic the first time you see it, and one wrong box gets it bounced back weeks later. The image below shows you exactly what the form looks like and where the sections that trip up families sit, so keep reading before you fill anything in.

⏱ The real clock: Form 2848 itself has no deadline — but your parent's balance is not waiting for it. The failure-to-pay penalty adds 0.5% every month, interest compounds on top, and if any unfiled year would have produced a refund, the 3-year window to claim that money closes for good.

Why a regular power of attorney doesn't work with the IRS

A durable financial power of attorney — even one a lawyer drafted — does not by itself let you represent your parent before the IRS. The IRS runs on its own document: Form 2848, Power of Attorney and Declaration of Representative, recorded in the agency's Centralized Authorization File (CAF).

Once a valid Form 2848 is on file, you can call the IRS about the years it covers, get transcripts, respond to notices, and set up payment arrangements. Check the box in Part I and the IRS mails you a copy of every notice — so nothing else dies unread in the shoebox. Our Form 2848 power of attorney walkthrough covers the form line by line.

You do not need to be a tax professional. Form 2848 has a family-member designation (designation f) that lets a spouse, parent, child, or sibling represent immediate family. The IRS treats this as limited practice — routine calls, transcripts, and basic arrangements — while appeals, offers, and levy fights typically go further with a credentialed representative.

If your parent can still sign, this is the whole process: fill out the form together, both sign, submit. Capacity here means they understand what they're authorizing on the day they sign — a diagnosis alone doesn't disqualify them.

If your parent is incapacitated, the durable POA becomes the bridge. When it grants authority over tax matters, you can sign Form 2848 as their agent and attach a copy of the POA. The IRS scrutinizes these packages, so the POA's language matters — vague documents get rejected.

If there is no POA and no capacity, the path runs through the courts: a guardianship or conservatorship. The court-appointed fiduciary then files Form 56 with the IRS and legally stands in your parent's shoes — no Form 2848 needed unless they hire a representative.

If you only want to watch the account, Form 8821 is the lighter tool: it authorizes the IRS to show you your parent's information and copy you on notices, but you can't advocate with it. See our Form 8821 tax information authorization guide.

| Document | Who signs it | What it lets you do | When it fits |

|---|---|---|---|

| Form 2848 | Your parent + you | Speak, negotiate, respond, receive notices | Parent has capacity and wants you handling it |

| Form 8821 | Your parent | View account info and receive notice copies only | Monitoring an account before problems escalate |

| Durable POA + Form 2848 | You, as agent (POA attached) | Full representation despite incapacity | Parent lost capacity but signed a POA covering tax matters |

| Form 56 (fiduciary) | Court-appointed guardian/conservator | Stand fully in the taxpayer's shoes | No POA exists and parent lacks capacity |

What happens if your parent's IRS debt goes unhandled

An unfiled, unpaid balance moves through the IRS's automated pipeline on its own — and for retirees, it ends at income you'd assume was safe: the IRS can take up to 15% of Social Security through the Federal Payment Levy Program. For a parent with unfiled self-employment or gig years, the sequence usually runs like this:

- Non-filer notices (CP59 and successors) — the IRS knows returns are missing because employers, banks, and gig platforms reported income under your parent's SSN.

- Substitute for Return — the IRS files the return itself using only the reported income, with no business expenses and no favorable filing status, producing the worst-case tax. Our guide to when the IRS filed a substitute return for me explains why these numbers are almost always inflated.

- Statutory notice of deficiency — the proposed tax becomes a legal assessment if nobody responds within the notice's window.

- The billing sequence — CP14, then reminder notices, each adding penalties and interest.

- CP504 — the IRS declares intent to seize state tax refunds, and a federal tax lien becomes likely.

- LT11 / Letter 1058 — the final notice. After 30 days the IRS can levy bank accounts (funds are held 21 days before they leave) and garnish income — including the Social Security levy above. See can the IRS garnish Social Security for how that works on a fixed income.

Two more stakes worth knowing. A balance above $66,000 (the 2026 threshold) can be certified to the State Department, blocking passport renewal. And if you're worried the unfiled years are criminal territory: for nearly all non-filers this is a civil money problem — our guide to whether you can go to jail for owing the IRS draws the line honestly.

In 2026, don't mistake IRS silence for a stalled case. Staffing is down sharply, so humans are hard to reach — but the notices, liens, and levies come from automated systems that never stopped running.

Stepping in for a parent who owes the IRS?

Bring us the stack — even photos of the notices. An experienced tax professional will map exactly where your parent's account stands and the fastest way to get you authorized and the debt handled. Every month of waiting adds penalties and interest; the review is free and confidential.

Your parent's options once you're authorized

Once Form 2848 is on file, every IRS resolution program becomes available to you on your parent's behalf — and for a parent with substitute-return years, the first move is almost never "pay." The general DIY playbook for these programs lives in our guide to how to settle tax debt yourself; here's how each one applies to a parent's account:

| Option | Who qualifies | Cost & timeline |

|---|---|---|

| File the real returns (SFR reconsideration) | Anyone with substitute-return years; almost always the first move for gig income | $0 to file; IRS reprocessing takes months, but it can shrink the balance itself |

| Short-term payment plan | Balance payable in full within 180 days | $0 setup; interest and penalties continue until paid |

| Streamlined installment agreement | Total balance ≤ $50,000, all returns filed | Setup fee (lower online/direct debit, reduced for low income); up to 72 months |

| Non-streamlined installment agreement | Balance over $50,000 | Requires full financial disclosure (Form 433 series); setup takes longer |

| Currently Not Collectible | Allowable living expenses meet or exceed income — common for parents on Social Security alone | $0; collection pauses while hardship lasts, though the debt and interest remain |

| Offer in Compromise | Means-tested — assets and future income genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers (both waived with low-income certification, AGI ≤ 250% of poverty); the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance in the prior 3 years; note the new Automatic Exemption from Penalty rolling out from summer 2026 | $0; can remove failure-to-file and failure-to-pay penalties on a qualifying year |

Two notes on that table. First, penalty relief only reaches penalties — interest generally stays unless the penalty it rode in on is removed, as our guide to whether IRS interest can be waived explains. Second, once you've picked a path, how you actually send money matters less than people think — the best way to pay the IRS compares the mechanics.

A worked example: your parent owes $83,100 from three unfiled gig years

Say your father drove for delivery apps for years and hasn't filed since 2021. The IRS built substitute returns from his 1099s for three years and assessed $83,100 — because the SFRs treated roughly $58,000 of gross platform income per year as pure profit: no mileage, no phone, no supplies, no favorable filing status. This is exactly the pattern covered in haven't filed in 3 years.

Now run the math with real returns. If his reconstructed mileage logs support about $20,000 of vehicle and business expenses per year, his actual net profit is closer to $38,000 annually — and the recomputed tax, self-employment tax, penalties, and interest might land near $39,500 total instead of $83,100. That's hypothetical arithmetic, but the mechanism is real: SFR reconsideration through original returns is often worth more than any settlement program.

The knock-on effects are just as concrete. At $83,100, he's over the $50,000 streamlined ceiling (full financial disclosure required) and over the $66,000 passport-certification threshold. At roughly $39,500, he qualifies for an online 72-month plan — about $39,500 ÷ 72 ≈ $549 a month, with interest still accruing, so paying faster costs less. And if he lives on Social Security alone, Currently Not Collectible may fit better than any payment at all — see Currently Not Collectible status. To see how much of a balance like this is penalties and interest rather than tax, run the numbers through our Penalty & Interest Calculator.

How to set up IRS power of attorney for your parent, step by step

Setting up IRS power of attorney for a parent takes one form, two signatures, and an upload or fax to the IRS CAF unit.

- Confirm your parent can sign. If they understand what they're authorizing, Form 2848 works directly. If capacity is doubtful, locate the durable power of attorney now — or talk to an elder-law attorney about a conservatorship before the balance grows further.

- Choose the right form. File Form 2848 if you need to act — call, negotiate, respond. File Form 8821 if you only need to see their records and receive copies of notices.

- Fill out Form 2848 completely. List each tax type (for most parents, "Income" and Form 1040), each specific year — "all years" gets rejected — and your designation. Most adult children use designation f, Family Member.

- Sign and date — both of you. Your parent signs as taxpayer; you sign the Declaration of Representative. Missing dates and year ranges that don't match Part I are the most common rejection reasons.

- Submit it to the IRS CAF unit. Upload it online, or fax or mail it per the current instructions for Form 2848. If a specific IRS employee already has the case, fax them a copy directly so you can talk the same day.

- Pull transcripts and map the debt. Before calling collections, get account and wage-and-income transcripts for every year so you know what was assessed, which years are substitute returns, and where each collection clock stands.

The official form, current instructions, and submission options are on the IRS pages for Form 2848 and Form 8821; payment options once you have a plan are at IRS.gov/payments.

When you can handle this yourself — and when help changes the outcome

You don't need professional help for a single phone call or a small balance your parent agrees with. If your parent is lucid, the debt is one recent year, and it's under the streamlined thresholds, a family-member Form 2848 plus an online payment plan is genuinely a do-it-yourself job — the steps above are the whole project.

Experienced help changes outcomes in specific situations: a levy already in motion against a bank account or Social Security; multiple substitute-return years where the reconsideration math determines whether the balance is $80,000 or $40,000; incapacity questions where a rejected POA package costs months; and Offer in Compromise analysis, which is means-tested arithmetic, not negotiation. Family representation is also formally limited — appeals and complex collection work sit more comfortably with a credentialed representative. One more caution while things are unresolved: if you share a bank account with your parent, understand the exposure in joint bank accounts with family and IRS levies.

Terms on the forms, decoded

CAF number — the ID the IRS assigns you the first time you're listed as a representative; you'll reuse it on every future authorization.

Declaration of Representative — Part II of Form 2848, where you state your standing (attorney, CPA, enrolled agent — or family member) and sign under penalty of perjury.

Durable power of attorney — a state-law document that survives incapacity; with the right language, it lets you sign Form 2848 for a parent who no longer can.

Fiduciary (Form 56) — someone who legally stands in the taxpayer's shoes, like a court-appointed conservator or an executor, rather than merely representing them.

Substitute for Return (SFR) — the return the IRS files for a non-filer using reported income only, with no deductions — which is why SFR balances are usually overstated.

CSED — the Collection Statute Expiration Date: generally 10 years from each assessment, though appeals, offers, and bankruptcy can pause the clock.

Power of attorney for a parent: your questions answered

Can I talk to the IRS about my parent's taxes without a power of attorney?

Yes — for a single conversation. If your parent is on the call, verifies their identity, and gives the IRS employee verbal permission, the agent can discuss that matter with you. But oral consent ends when the call does. For anything ongoing — pulling transcripts, setting up a payment plan, receiving copies of notices — you need Form 2848 or Form 8821 on file, or you'll repeat the same identity dance every time.

Does a durable power of attorney from a lawyer work with the IRS?

Not by itself. The IRS records representation on its own form, Form 2848, in the Centralized Authorization File. Where a durable POA matters is incapacity: if it grants you authority over tax matters, you can sign Form 2848 as your parent's agent and attach a copy of the POA. If there's no POA and your parent has lost capacity, a court-appointed conservatorship is usually the remaining path.

Can I be my parent's IRS representative if I'm not a CPA or attorney?

Yes. Form 2848 includes a family-member designation (designation f) that lets an immediate family member — including an adult child — represent a parent without any professional credential. The IRS treats family representation as limited practice, though: it covers routine calls, transcripts, and basic arrangements, while appeals conferences, offers, and levy fights typically go further with a credentialed representative such as an enrolled agent, CPA, or attorney.

What is the difference between Form 2848 and Form 8821?

Form 2848 lets you act; Form 8821 only lets you see. With Form 2848 you can speak for your parent, respond to notices, and negotiate arrangements. Form 8821 authorizes the IRS to share their account information and send you copies of notices, but you cannot advocate or make agreements with it. Many families start with Form 8821 to monitor a parent's account, then file Form 2848 when there's a problem to fix.

Am I personally responsible for my parent's tax debt?

No — signing Form 2848 never makes you liable for a parent's IRS balance, and children do not inherit tax debt. The exceptions are indirect: money in a joint bank account can be levied for their debt, and assets a parent transfers to you for less than value can be pursued. Keep your finances separate from theirs while the debt is unresolved.

My parent has dementia and never signed a power of attorney — what now?

Once capacity is gone, your parent can no longer validly sign Form 2848 or a durable POA, so the path runs through the courts: a guardianship or conservatorship. The court-appointed fiduciary then files Form 56 with the IRS, which lets them stand in your parent's shoes for tax matters — and they can file Form 2848 to bring in a representative. An elder-law attorney handles the court side; the IRS side is paperwork.

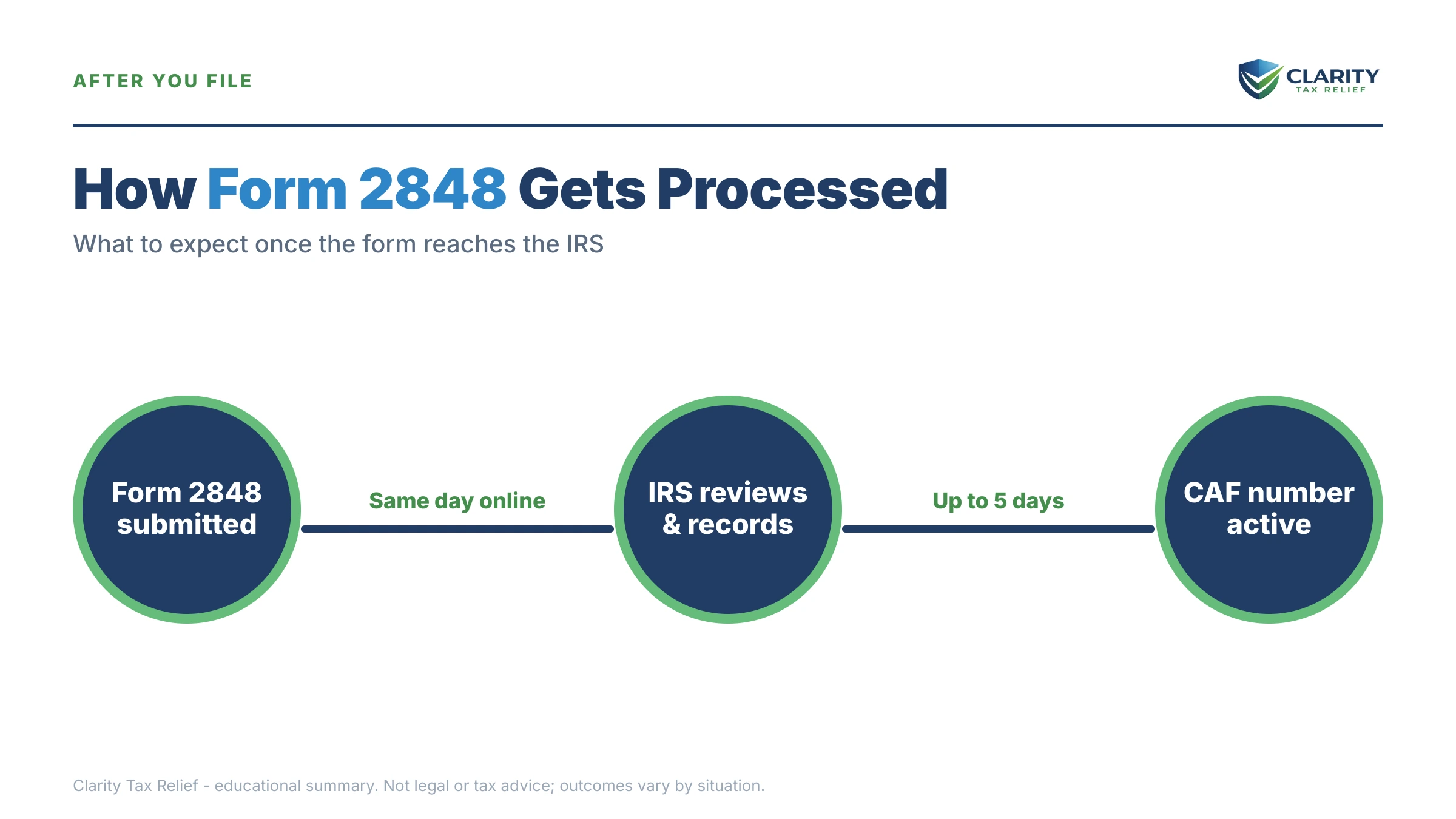

How long does the IRS take to process Form 2848?

It varies — online submission is typically the fastest route into the Centralized Authorization File, while faxed and mailed forms can take weeks, and 2026 staffing cuts have stretched processing further. There's a workaround for urgent matters: if a specific IRS employee is handling the case, you can fax the signed Form 2848 directly to them and be recognized on that matter the same day.

Will filing Form 2848 make the IRS look harder at my parent's account?

No. A power of attorney changes who the IRS talks to — it does not trigger an audit, restart collection, or flag the account. The automated notice stream continues on its own schedule whether or not a representative is on file. What Form 2848 changes is visibility: with the notice-copy box checked, you see every letter your parent might otherwise leave unopened.

Your next 24 hours

- Open the newest IRS envelope in the stack. Note the notice number in the top corner and the total balance — that tells you exactly where your parent sits in the collection sequence.

- Gather the paperwork you'll need. Your parent's last filed return, all the IRS notices, their 1099s or income records for the unfiled years, and any durable power of attorney that exists.

- Get a free case review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will confirm the fastest authorization path for your family and which resolution actually fits, before another month of penalties and interest lands on the balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.