Choosing Help

Is Tax Relief Legit? What's Real, What's a Scam, and How to Tell (2026)

The short answer: yes, tax relief is legit. The IRS programs behind it — payment plans, Offer in Compromise, penalty abatement, and hardship status — are real options written into federal law. What is often not legit is how some companies sell them, with "pennies on the dollar" promises no firm can guarantee. The programs are real; verify the company.

You saw the late-night ad promising to erase your IRS debt, then read a review calling the whole industry a rip-off, and now you can't tell which is true. That confusion is fair — because both things are happening at once. The relief itself is genuine government policy; the marketing around it is where the danger lives.

In June 2026, the FTC and the State of Nevada permanently banned the operators of American Tax Service from the debt-relief and tax-preparation business — for the exact claims that make people distrust the whole field, guaranteed settlements and big upfront fees. So the honest question isn't "is tax relief legit," it's "which parts are legit, and how do I tell them apart."

The image below shows what real IRS resolution paperwork looks like, so you can see the genuine programs behind the sales pitch and recognize when a company is selling you something the IRS doesn't actually have.

⏱ The clock that's actually running: there's no deadline on deciding whom to trust — but the failure-to-pay penalty of 0.5% per month plus interest never pauses while you research. Every month you spend unsure, your balance grows, which is exactly the anxiety scam marketing exploits. Verify fast, then act.

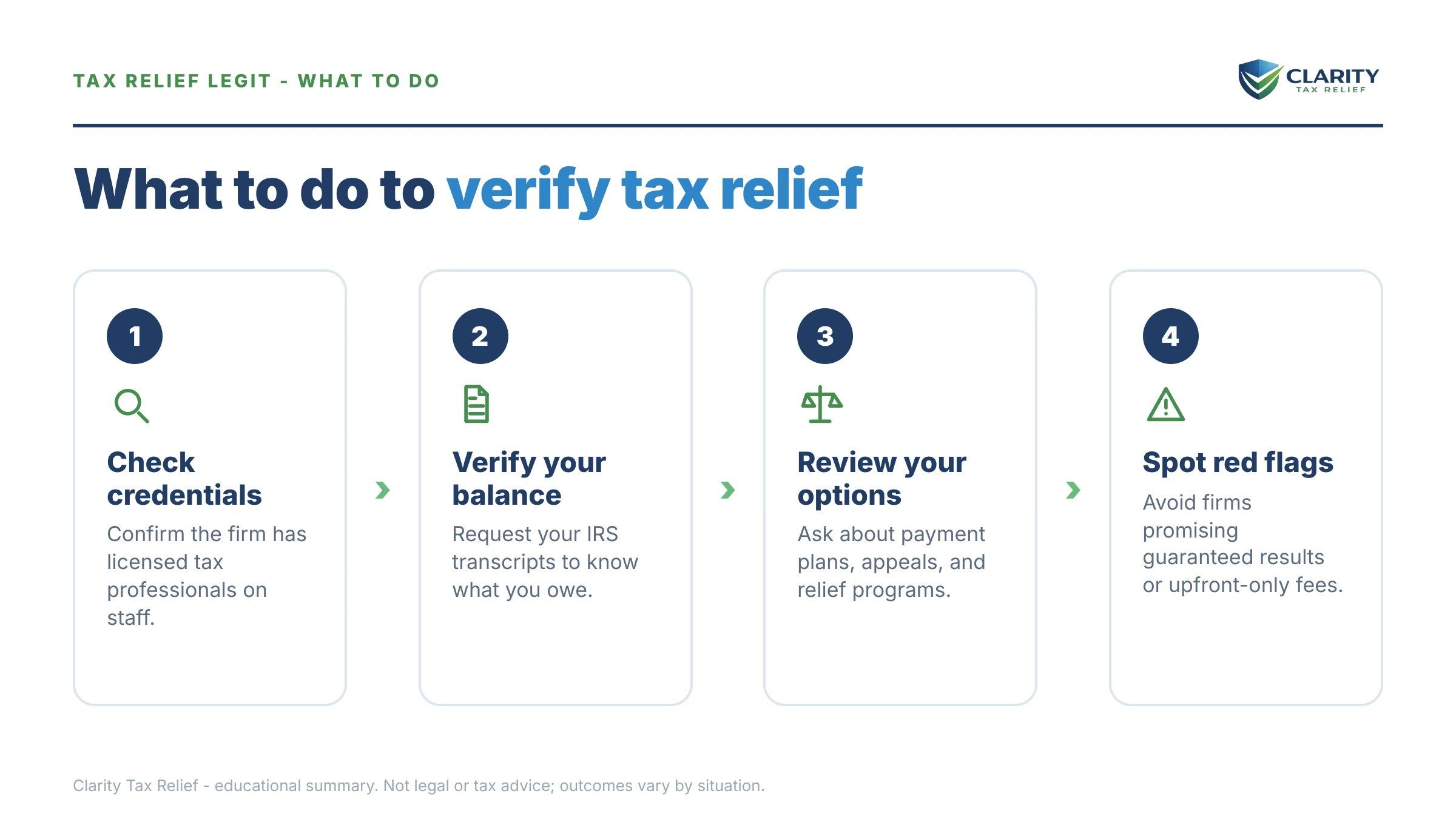

Why you're asking "is tax relief legit"

You're asking because the industry earned its bad reputation. For years, a handful of large firms ran the same playbook: a scary radio ad, a "free consultation" that turned into a $4,000 retainer, and a settlement that never came. When those companies collapsed, they took clients' money with them — and the headlines stuck to everyone.

Want to test these checks on us? See Is Clarity Tax Relief legit? How to verify us yourself — every claim on that page comes with an independent way to check it.

The confusion runs deeper than bad actors, though. The words are misleading. "Tax relief" is a marketing phrase, not a legal one. Behind it sit ordinary IRS programs with unglamorous names, and any firm can claim to offer "relief" whether they're a credentialed enrolled-agent practice or a boiler room reselling leads.

So the real skill isn't deciding whether tax relief works — it demonstrably does, for the right situations. It's learning to separate the legitimate program from the company selling it. Our hub on how to settle tax debt yourself walks through every program in depth; this page is about trust — how to tell real help from a con.

What happens if you do nothing — or hand money to the wrong firm

Doing nothing is the one choice with a guaranteed downside: the IRS collection sequence is automated, and in 2026 the machine keeps escalating even though IRS staffing was cut roughly 27% in 2025. The notices below arrive on their own schedule whether or not a human ever touches your file:

- CP14 — your first bill. Roughly 21 days to pay or arrange before it escalates (only 10 business days if the balance is $100,000 or more). No enforcement yet.

- CP501 / CP503 — reminder notices. Still bills, but the balance grows monthly with penalties and interest.

- CP504 — Notice of Intent to Levy your state tax refund or other property. A federal tax lien becomes a real possibility.

- LT11 / Letter 1058 — Final Notice of Intent to Levy. After a 30-day window, the IRS can garnish wages and levy bank accounts — and you gain formal Collection Due Process appeal rights.

Handing money to the wrong firm creates a second, quieter harm. A scam operation cashes your retainer, files nothing, and lets that clock keep running. By the time you realize it, you've lost the fee and months of the window where cheaper options were still open. If that already happened to you, read "a tax relief company took my money" for how to claw some of it back.

The lesson isn't "trust no one." It's that inaction and misplaced trust cost the same thing — time — and time is the one resource that makes every IRS option more expensive as it passes.

Not sure who to trust with your tax debt?

Before you pay any company a dime, get an honest read on where you actually stand. A Clarity tax professional will pull your transcripts, tell you which real IRS program fits, and quote a flat fee in writing — free review, no pressure, no guarantees we can't keep.

The legitimate tax relief options that actually exist

Every real "tax relief" outcome comes from one of a small set of IRS programs — there is no secret one. Here is what genuinely exists, who each option fits, and what it costs, so you can recognize when a company is steering you toward the wrong one.

| Program | Who it fits / eligibility | Real cost |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup; interest & penalties continue |

| Streamlined installment agreement | Owe $50,000 or less; up to 72 months | $0–$130 setup; no detailed financials |

| Offer in Compromise | Assets + future income genuinely can't cover the debt before the statute expires | $205 fee (waived if low-income); 20% down; ~1 in 5 accepted |

| Currently Not Collectible | Paying anything would create real hardship | Free; debt remains, collection paused |

| Penalty abatement (FTA / AEP) | Clean compliance the prior 3 years, or reasonable cause | Free; removes penalties, not the tax |

Two things on that table debunk most scam pitches. First, an Offer in Compromise is accepted only about 1 in 5 times — so any "settle for pennies, guaranteed" claim is mathematically impossible to promise. Second, penalty relief is real but only touches penalties; it can't erase the underlying tax. Note too that first-time abatement is being replaced by Automatic Exemption from Penalty (AEP) starting summer 2026 — automatic, with no request needed for eligible accounts.

Wonder whether you'd even clear the Offer in Compromise bar? You can estimate your own offer with our Offer in Compromise Calculator before any company tells you what you "qualify" for. And if a firm pushes an OIC without running that math on your finances, that's your cue — see how the OIC mill scam works.

How to tell a legit tax relief company from a scam

A legitimate tax relief company reviews your IRS transcripts before quoting an outcome — a scam quotes the outcome first to close the sale. That single difference sorts most of the field. The table below turns it into a checklist you can run on any firm, including us.

| Green flag (legitimate) | Red flag (walk away) |

|---|---|

| Uses enrolled agents, CPAs, or tax attorneys who can represent you before the IRS | Vague "tax consultants" and no named credentials |

| Pulls your transcripts before quoting a plan or price | Promises a settlement amount on the first call |

| Flat fee and exact scope in writing | Large upfront retainer, unclear what it buys |

| Says outcomes depend on your finances | "Pennies on the dollar," "guaranteed," "you qualify" |

| Listed and reviewable at the BBB and state AG | Pressure to sign today "before the offer expires" |

The banned phrases in that right column aren't just tacky — after the FTC's June 2026 action, they're a legal liability for any firm that uses them. If you hear "pennies on the dollar," you're hearing a phrase the government has specifically targeted as deceptive. For a deeper vetting routine, use how to choose a tax relief company and the questions to ask a tax relief company before you sign anything.

It also helps to know who you're comparing. If a specific big-name firm cold-called you, our head-to-head breakdowns — like the Optima Tax Relief alternative comparison — show what to check for in fees, credentials, and process, not just marketing.

A worked example: $27,500 and a refinance on the line

Say you owe the IRS $27,500 and you're a homeowner hoping to refinance this year. A scam firm's pitch: "We'll settle it for a fraction — sign here." Here's what a legitimate review of the same facts actually finds.

Your home has, say, $60,000 in equity. Because an Offer in Compromise counts the equity the IRS could collect, that equity alone likely puts a real settlement out of reach — the IRS's math says it could collect far more than a token offer. A firm that promised you a "pennies" settlement was never going to deliver it, because the numbers were never there.

The legitimate path is less dramatic and far more useful. Your $27,500 is under the $50,000 line, so a streamlined installment agreement over 72 months runs about $27,500 ÷ 72 = roughly $382 a month before interest — call it the mid-$400s once interest is layered on. That stops the escalation and keeps you current.

The refinance problem is the real work. If the IRS has filed a lien, it can block your closing — but you can request a tax lien subordination so the new mortgage takes priority, which is often exactly how a refinance closes with a balance still owed. That's a specific, honest fix a credentialed firm handles; it's not something a "settle it all" pitch even mentions. See refinancing with an IRS lien for how the timing works.

How to respond, step by step

- Verify your own balance first — log into your IRS online account and pull your transcripts so you know the real number, the tax years, and the penalties before anyone quotes you a price.

- Learn which programs actually fit you — match your situation to the real IRS options (payment plan, penalty abatement, hardship status, or Offer in Compromise) so you can spot a company selling you the wrong one.

- Vet the company in writing — confirm credentialed representatives, get the flat fee and exact scope in writing, and check the firm at the BBB and your state attorney general before paying.

- Reject the guarantees — walk away from any "pennies on the dollar," guaranteed-settlement, or "you qualify" promise made before your finances and transcripts are reviewed.

- Get a free review, then decide — have a professional read your transcripts and tell you honestly which program you qualify for and what it costs, then choose whether to do it yourself or hire help.

When you can handle this yourself — and when help changes the outcome

You do not need to hire anyone for a simple, clear-cut situation. If you owe a modest balance you can clear within 180 days, or you agree with a first notice and want a standard payment plan, you can set that up yourself at IRS.gov in minutes — no fee to a company. Penalty abatement for a clean-history year is often a single phone call or letter. Free options like free help with IRS tax debt and Low Income Taxpayer Clinics exist for exactly these cases.

Experienced help earns its fee when a mistake gets expensive. That means a levy or garnishment already in motion, several unfiled years to reconstruct, a business or payroll (trust-fund) debt, an Offer in Compromise where the equity and income math decides everything, or a balance over roughly $50,000 where the IRS wants full financial disclosure. In those cases the order you fix things in — returns, then penalties, then the balance — changes the final number, and a wrong move forfeits rights you can't get back.

The honest test: if the downside of doing it wrong is small, do it yourself. If a single misstep could cost you thousands or a levy, get a credentialed set of eyes on it first.

Terms on the pitch, decoded

Tax relief: a marketing umbrella term, not a legal one — it refers to any of the real IRS resolution programs, not a single product.

Offer in Compromise (OIC): the IRS program that settles a debt for less than the full amount, but only when your finances genuinely can't cover it; roughly 1 in 5 are accepted.

"Pennies on the dollar": the classic scam phrase — a promise no firm can legally guarantee, since the IRS, not the company, decides every offer.

Enrolled agent (EA): a federally credentialed tax professional authorized to represent you before the IRS — a real credential you can and should ask for.

Fresh Start: the IRS's collection of easier-qualification rules, not a secret forgiveness program — read is the IRS Fresh Start program real and why "IRS one-time forgiveness" is a myth.

Is tax relief legit? Your questions, answered

Is tax relief a scam?

Tax relief itself is not a scam — the IRS programs behind it are written into federal law and used by millions of taxpayers every year. What can be a scam is how certain companies market those programs, with "pennies on the dollar" guarantees and large upfront fees before they've reviewed a single document. The relief is real; some sellers are not.

Do tax relief companies really work?

A reputable tax relief company works by qualifying you for programs the IRS already offers — an installment agreement, penalty abatement, hardship status, or an Offer in Compromise — and handling the paperwork and negotiation for you. They cannot invent a program the IRS doesn't have or force approval. The value is expertise and representation, not magic; results depend entirely on your finances and compliance.

Can tax relief really settle my debt for less than I owe?

Sometimes, through an Offer in Compromise — but only when the IRS's own math shows your assets and future income genuinely can't cover the balance before the collection statute expires. The IRS accepted roughly 1 in 5 offers in FY2024, so this is far from automatic. Anyone who promises a settlement amount before reviewing your finances is selling a fantasy, not a program.

How much does tax relief cost?

Professional tax relief fees typically run from a few hundred dollars for a simple payment plan to several thousand for a full Offer in Compromise or multi-year unfiled-return case. The IRS's own fees are separate and modest — $205 for an OIC application (waived for low-income filers) and $0 to $130 to set up a payment plan. Be wary of any firm quoting thousands before knowing what your case needs.

Is the IRS Fresh Start program real?

Yes, Fresh Start is real — but it's an umbrella term for changes the IRS made to existing programs (easier installment agreements, expanded Offer in Compromise rules, and streamlined lien relief), not a single application you file. There is no "one-time forgiveness" button. Companies that advertise Fresh Start as a secret settlement program are dressing up ordinary options in urgent marketing.

Can I get tax relief myself for free?

Yes — you can request a payment plan, penalty abatement, or hardship status directly at IRS.gov at no cost beyond the IRS's own fees. Low Income Taxpayer Clinics and VITA offer free help for those who qualify. Hiring a professional makes sense when the debt is large, multiple years are unfiled, a levy is in motion, or an Offer in Compromise requires careful math — the cases where a mistake is expensive.

Will a tax relief company stop the IRS immediately?

No company can freeze the IRS instantly or stop all collections with a phone call. What a professional can do is file a power of attorney, request a collection hold, and pursue a levy release once financial information is submitted — steps that take days, not seconds. Interest and penalties keep accruing throughout, so any claim of an instant freeze is false.

How do I check if a tax relief company is legitimate?

Confirm the firm uses credentialed representatives — enrolled agents, CPAs, or tax attorneys who can appear before the IRS — and get the fee and scope in writing before paying. Check that they review your transcripts before quoting an outcome, and search the company at the Better Business Bureau and your state attorney general. A firm that guarantees a result or demands full payment upfront is a red flag.

Your next 24 hours

- Find your real number. Log into your IRS online account and note the total balance and the tax years — this is the figure any legitimate firm must start from.

- Gather three things: your most recent tax return, any IRS notices you've received, and a rough picture of your monthly income and expenses.

- Get a free, honest review. Call (888) 825-7779 or use the 2-minute form — we'll tell you which real program fits and what it costs, before you pay anyone anything. Meanwhile, remember the penalty and interest clock never stops, so the sooner you verify, the less it grows.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.

Authoritative sources: the IRS's own Offer in Compromise page, payment plans and installment agreements, and the independent Taxpayer Advocate Service.