Tax Relief Company Comparisons

Optima Tax Relief Alternative: Your Best Options in 2026

The short answer: the best Optima Tax Relief alternative depends on your situation. Most balances under $10,000 can be resolved directly with the IRS for free, Low Income Taxpayer Clinics represent qualifying taxpayers at no cost, and larger or contested debts do best with a flat-fee firm where credentialed professionals — not salespeople — evaluate your case first.

You saw the commercials, maybe sat through the phone consultation, and something told you to keep looking — the pressure to sign today, the pricing that unfolds in stages, or a pitch that felt built around the company's script rather than your actual IRS file. That instinct is worth trusting. Comparing before you commit is exactly what this page is for.

Below is every real path for your tax debt — including the free ones no company will advertise, because there's nothing to sell. By the end you'll know which path fits your balance, your income, and your notice status, and whether you need to hire anyone at all.

⏱ The real clock: there's no deadline to hire anyone — but your balance grows while you compare. The failure-to-pay penalty adds 0.5% per month and interest compounds daily, and if you're behind on IRS notices, the automated collection sequence keeps moving whether or not you've picked a company.

Why people look for an Optima Tax Relief alternative

Optima Tax Relief is one of the largest and most heavily advertised tax relief companies in the United States. Scale is not a flaw by itself — but it shapes the experience, and the reasons people end up searching for alternatives tend to cluster around a few patterns common to big national firms:

- Sales-first intake. Heavy ad spend has to be recouped, so the first person you talk to at a high-volume firm is often a commissioned salesperson, not the tax professional who would work your case. The diagnosis you get on that call is a pitch, not a plan.

- Phased pricing. Many large firms charge for an "investigation" phase before quoting the "resolution" phase. You can end up paying to learn things about your own account — balance, years owed, notice status — that your free IRS online account already shows.

- Minimum-debt thresholds. National firms typically focus on debts large enough to support their fee. If you owe a modest amount, you may be better served by a path that costs nothing.

- Wanting to know who's actually working the file. Some people simply want a named enrolled agent, CPA, or attorney they can call — not a case number in a queue.

None of this means every big-firm case goes badly. It means the brand name is the wrong thing to shop on. What matters is the fee structure, the credentials of the person representing you, and whether your case even needs a company — which is where the rest of this guide goes.

What happens to your IRS balance while you shop around

The IRS collection sequence runs automatically from first bill to levy, regardless of whether you've hired anyone. If you're comparing companies because you owe back taxes, know where you sit in that sequence — because your options shrink at each stage:

- CP14 — the first bill. You typically have about 21 days before the system queues the next notice. Cheapest moment to act; every option is still open.

- CP501 / CP503 — reminder notices. Still just bills, but the balance grows monthly and the clock keeps running.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a realistic next step.

- LT11 / Letter 1058 — Final Notice of Intent to Levy. A 30-day clock starts on your Collection Due Process rights (requested on Form 12153). After it runs, the IRS can levy bank accounts and garnish income.

- Active levies. A bank levy freezes funds for 21 days before they're sent to the IRS; a wage levy is continuous until released. If you're retired, the Federal Payment Levy Program can take up to 15% of your Social Security benefit, month after month — see our guide to the IRS taking 15 percent of Social Security.

- Passport certification. Once a debt passes $66,000 (the 2026 threshold), the IRS can certify it to the State Department, which can deny or revoke your passport.

In 2026 this matters more than the sales calls suggest: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder — but the notices and levies come from automated systems that never stopped. Spending three months choosing a company while an LT11 clock runs is the most expensive way to comparison-shop.

Comparing tax relief companies right now?

Before you sign anything anywhere, get a second opinion for free. An experienced tax professional will pull your actual IRS status, tell you which program your finances fit, and tell you honestly if you don't need to hire anyone — while interest and penalties keep accruing, the review costs nothing.

Alternatives to Optima Tax Relief: every real path compared

Every result a tax relief company can deliver comes from a standard IRS program you can also access directly. There is no back door and no negotiation trick — a firm's value is knowing which program your finances fit, documenting your case correctly, and defending it. Here is the full menu (our how to settle tax debt yourself guide walks through each in DIY detail):

| Path | Who it fits | Cost & key facts |

|---|---|---|

| Short-term IRS payment plan | Can pay in full within 180 days | $0 setup; interest and penalties accrue until paid |

| Guaranteed installment agreement | Balance of $10,000 or less | Set up online in minutes; no financial disclosure |

| Streamlined installment agreement | Balance of $50,000 or less; up to 72 months | Modest setup fee (lower with direct debit); no detailed financials |

| Currently Not Collectible (CNC) | Income covers only allowable living expenses | Free to request; collection pauses, debt remains, 10-year statute keeps running |

| Offer in Compromise (Form 656) | Assets + future income genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers — both waived with low-income certification; roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance for the prior 3 years | Free to request; the new Automatic Exemption from Penalty applies automatically starting summer 2026 |

| Low Income Taxpayer Clinic | Income below program limits | Free representation in disputes and collection cases |

| Flat-fee professional firm | Levies in motion, unfiled years, OIC math, larger balances | One quoted fee; a credentialed professional works the case |

Which path is realistic depends heavily on how much you owe. This table is the honest version of the sales call you may have already sat through:

| Balance | Realistic options | Do you need a company? |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement or 180-day plan, set up online | No — most people finish this in under an hour |

| $10,000 – $25,000 | Streamlined installment agreement; penalty abatement if compliant | Usually no, unless a levy is active or years are unfiled |

| $25,000 – $50,000 | Streamlined agreement (direct debit at the upper end); CNC or OIC if income is fixed | Helpful when hardship or OIC math is involved |

| $50,000 – $100,000 | Financial disclosure on Form 433-F; non-streamlined agreement; watch the $66,000 passport threshold | Professional help usually pays for itself here |

| Over $100,000 | Likely a revenue officer; full financials; lien and levy defense | Yes — get representation before the first RO contact |

Worked example: $27,500 in IRS debt on Social Security income

A $27,500 balance on fixed retirement income has three realistic outcomes — and only one of them is a monthly payment. Say you're 71, you owe $27,500 from a retirement-account withdrawal a few years back, and your income is $2,150 a month in Social Security plus a $400 pension. This is hypothetical, but the math is how the IRS actually runs it:

- Streamlined installment agreement: $27,500 ÷ 72 months ≈ $382 a month at minimum — somewhat more in practice, because interest and the failure-to-pay penalty keep accruing until the balance is gone. On $2,550 of monthly income, that payment may simply not be there.

- Currently Not Collectible: if housing, utilities, food, and out-of-pocket medical costs consume your income under the IRS's allowable-expense standards, collection pauses entirely. The debt remains on the books, but nothing is levied — and the 10-year collection statute keeps running. Our guide to IRS hardship while on Social Security covers the documentation.

- Offer in Compromise: the IRS decides offers on Reasonable Collection Potential (RCP) — your asset equity plus your monthly disposable income projected forward (12 months of it for a lump-sum offer). Say you have $2,000 in savings above the allowance, no home equity, and $75 a month left after allowable expenses: RCP ≈ $2,000 + ($75 × 12) = $2,900 — a defensible offer against a $27,500 debt. With AGI at or below 250% of the poverty line, low-income certification waives the $205 fee, the 20% down payment, and payments during review. You can estimate your own numbers with our Offer in Compromise Calculator.

Now the comparison-shopping point: a fixed-income, low-asset profile is exactly what the OIC program was built for — but the IRS accepted roughly 1 in 5 offers in FY2024, and acceptance turns entirely on whether the RCP math holds up, not on which company's name is on the letterhead. Any firm quoting you a settlement figure before running that math is guessing. And if you do nothing at all, the Federal Payment Levy Program can take 15% of that $2,150 benefit — about $322 a month — indefinitely.

How to choose an Optima Tax Relief alternative, step by step

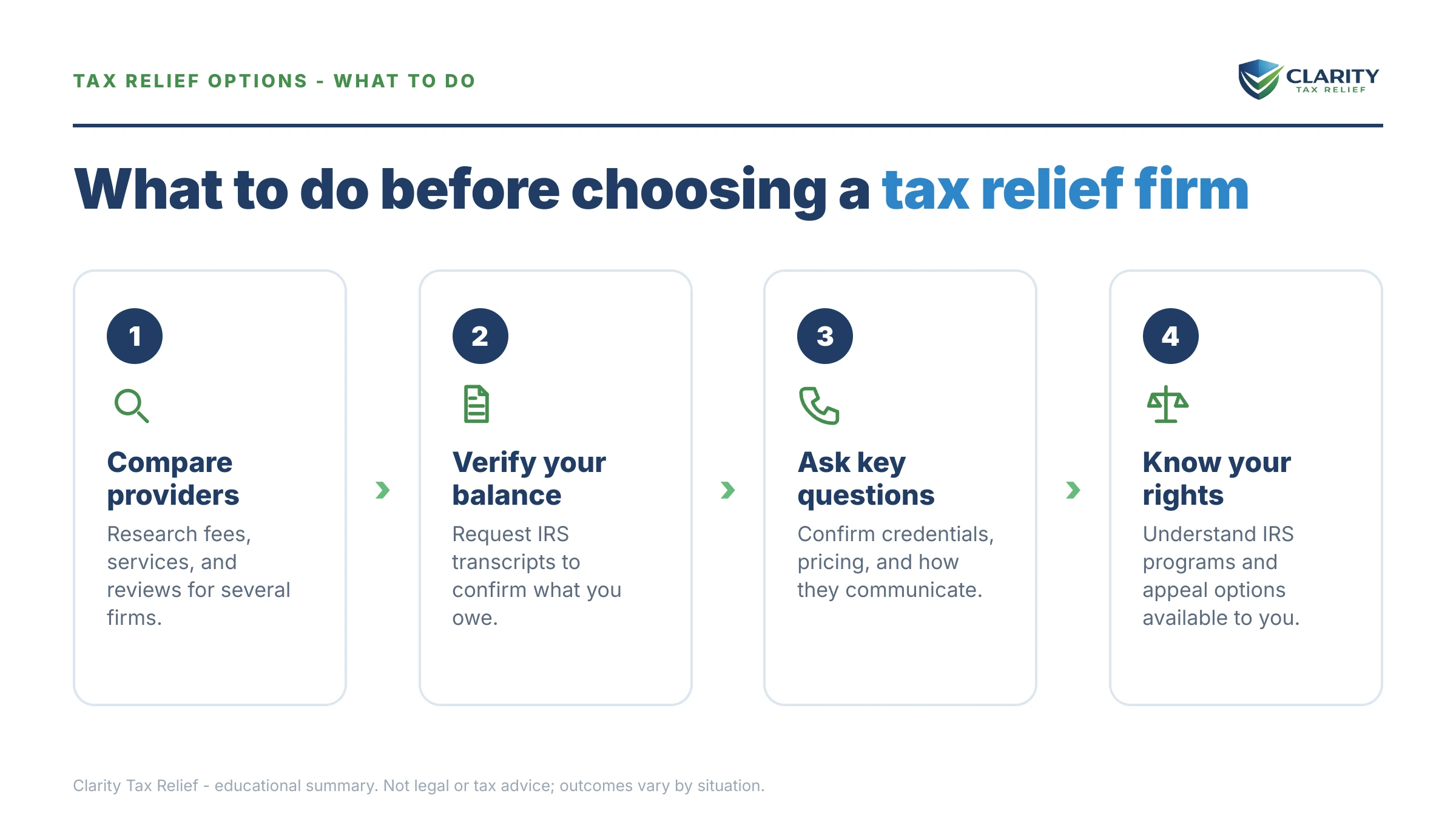

- Pull your own IRS records first. Create an IRS online account and download your account transcripts before any consultation. Knowing your exact balance, the years you owe, and where you sit in the notice sequence means no salesperson anywhere can inflate the problem.

- Decide what kind of help you actually need. Match your situation to the options table above. A simple payment plan needs no company at all; an active levy, multiple unfiled years, or Offer in Compromise math justifies professional help.

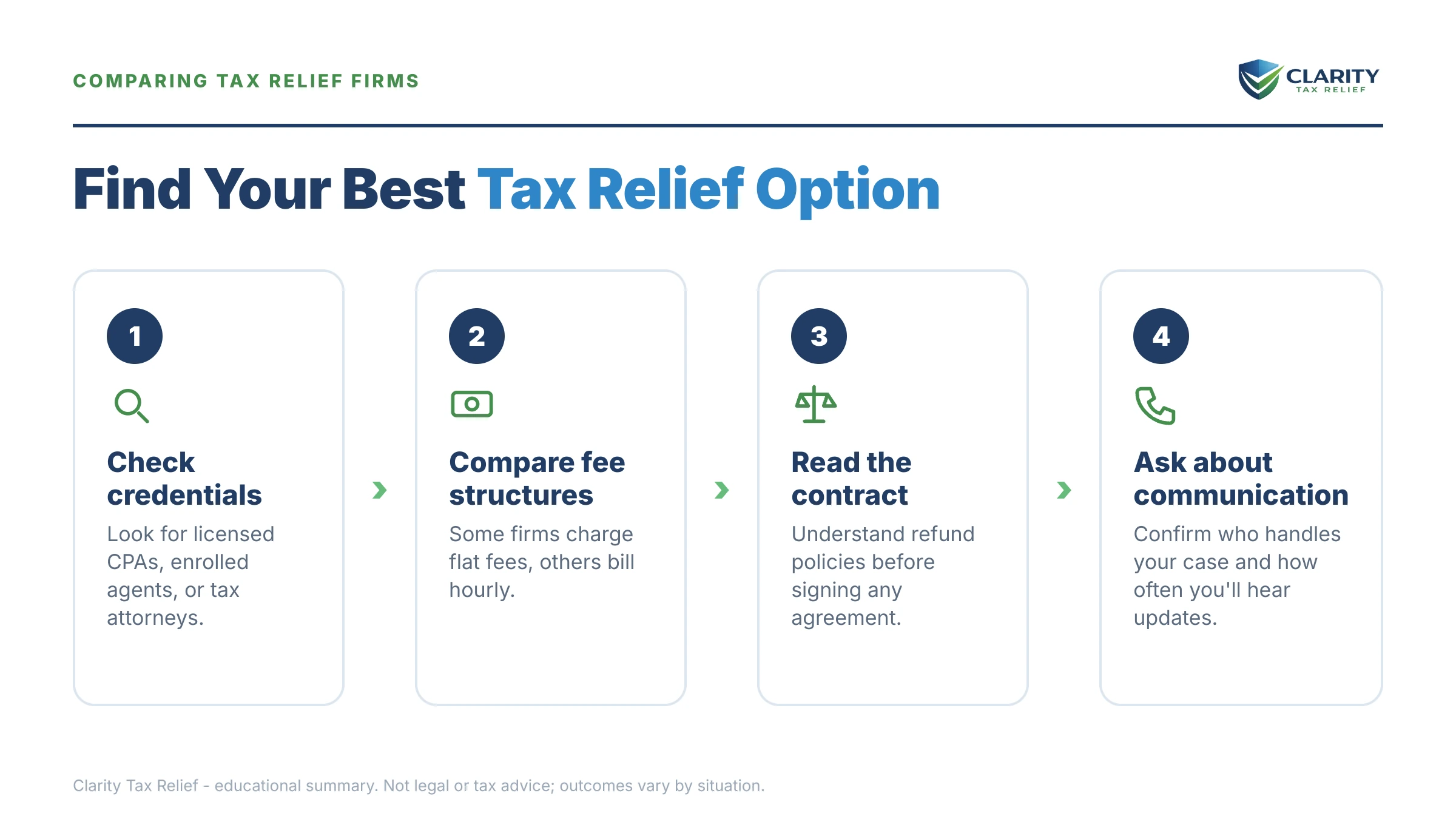

- Get quotes from two or three providers. Ask each the same questions: the total flat fee in writing, who personally works the case and what credentials they hold, and what happens if the IRS rejects the first proposed strategy.

- Verify credentials and read the contract. Confirm the person representing you is an enrolled agent, CPA, or attorney, and check the agreement for phase pricing, refund terms, and cancellation rights before paying anything.

- Pick a path within one week and act. Whichever route you choose — DIY, a free clinic, or a firm — start it. Interest compounds daily and the failure-to-pay penalty adds 0.5% every month you deliberate.

For a fuller vetting checklist, see how to choose a tax relief company, the specific questions to ask a tax relief company before signing, and the tax relief company red flags that should end a sales call on the spot. If pricing is your sticking point, our breakdown of how much tax relief costs explains what drives a legitimate fee.

When you don't need Optima — or any tax relief company

Most tax debts under $10,000 can be resolved online without hiring anyone. Be honest with yourself here, because the cheapest alternative to any firm is often the IRS's own website:

- You agree with the balance and can pay within 180 days. A short-term plan costs $0 to set up. Done.

- You owe $10,000 or less. A guaranteed installment agreement is yours for the asking — no financial disclosure, no negotiation.

- Your only problem is a penalty. First-time abatement (and, starting summer 2026, the Automatic Exemption from Penalty) removes penalties for taxpayers with a clean prior three years — no company required.

- Your income is low. A Low Income Taxpayer Clinic provides free representation, and our roundup of free help with IRS tax debt lists every no-cost door.

Where experienced help genuinely changes outcomes: a levy already in motion (release requests are time-sensitive and documentation-heavy), multiple unfiled years (the order you fix things changes what you owe), Offer in Compromise cases (RCP math done wrong wastes months and the filing fee), hardship cases on fixed income (allowable-expense documentation makes or breaks CNC), and anything involving a revenue officer. In those situations, the fee buys expertise and time you don't have — not access to a secret program.

Tax-relief sales terms, decoded

These are the phrases you'll hear on sales calls while comparing firms — here's what each actually means:

- Investigation phase: the paid first stage where a firm pulls your IRS records — largely the same transcripts you can download free from your IRS online account.

- Fresh Start Program: an umbrella marketing name for standard IRS options (payment plans, OIC, lien thresholds) — not a special program you must be "enrolled" in.

- Power of attorney (Form 2848): the form that lets a representative deal with the IRS on your behalf. Signing it does not, by itself, stop collection.

- Reasonable Collection Potential (RCP): the IRS's formula for the most it could ever collect from you — the number that decides an Offer in Compromise. Math, not negotiation skill.

- "Pennies on the dollar": a marketing phrase the FTC has taken enforcement action over. Real settlements exist, but only when the RCP math supports them — never because a company promised one.

Optima Tax Relief alternative FAQs

What is the best alternative to Optima Tax Relief?

It depends on your balance and income. Under $10,000, the best alternative is usually the IRS itself — a guaranteed installment agreement takes minutes to set up online. If your income is low, a Low Income Taxpayer Clinic can represent you at no cost. For larger or contested debts, look for a flat-fee firm where an enrolled agent, CPA, or attorney — not a salesperson — evaluates your case before you pay anything.

Can I do what a tax relief company does myself?

Often, yes. Setting up a payment plan, requesting first-time penalty abatement, and responding to a first balance-due notice are all things you can do directly with the IRS at little or no cost. Where self-help gets risky is hardship documentation, Offer in Compromise math, active levies, and multiple unfiled years — mistakes there cost real money and can lock you into worse terms.

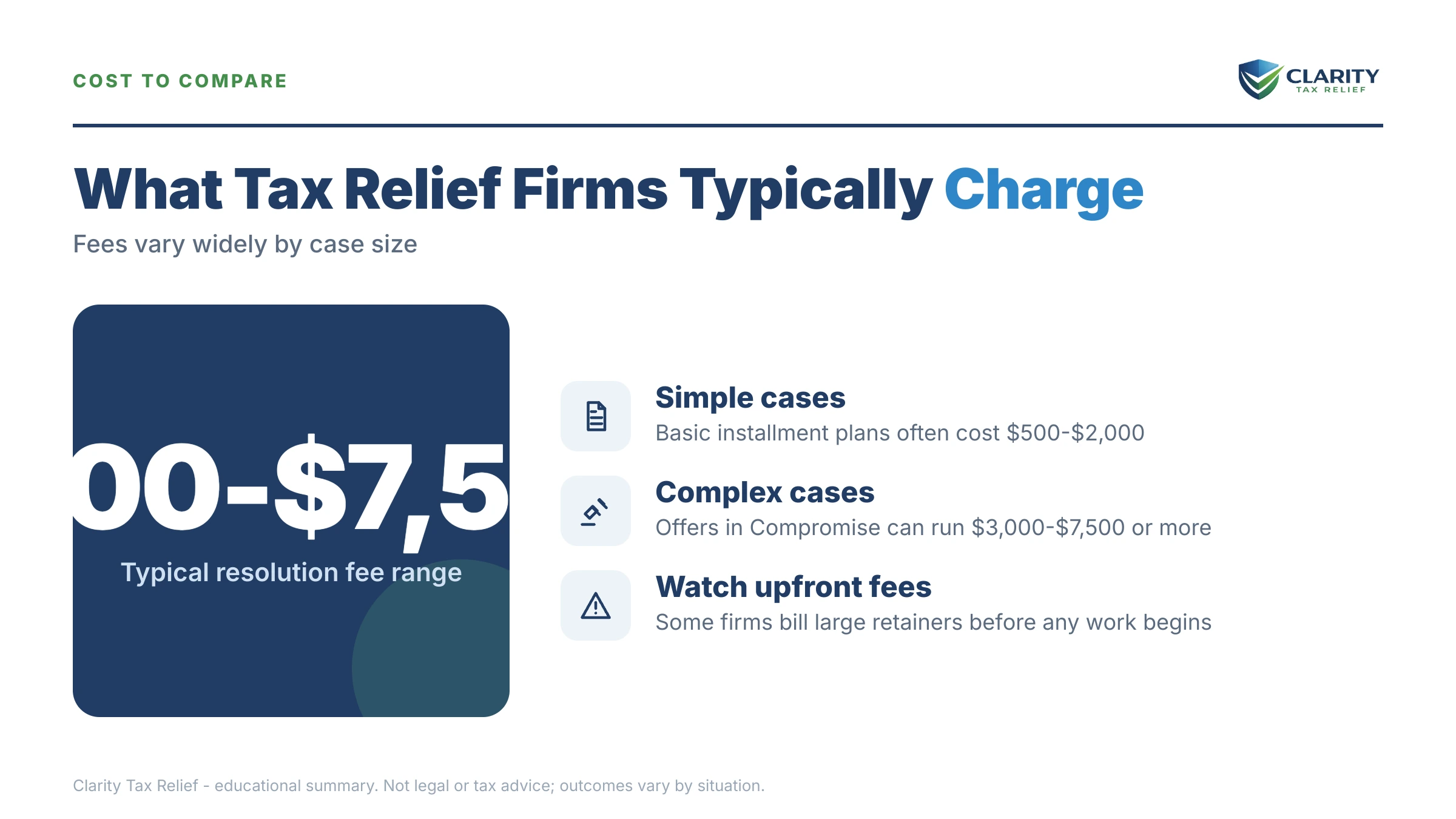

How much should tax relief services cost?

Fees vary widely by case complexity, but structure matters more than the sticker. A simple installment-agreement case should cost far less than a full Offer in Compromise with financial disclosure. Before signing anywhere, get the total flat fee in writing, ask what happens if the IRS rejects the first proposed resolution, and be wary of open-ended phase pricing where the second phase isn't quoted until you've already paid for the first.

Is there free help for IRS tax debt?

Yes — three real sources. The IRS itself lets you set up payment plans online, Low Income Taxpayer Clinics represent taxpayers whose income falls below program limits in disputes and collection cases, and the Taxpayer Advocate Service steps in when IRS delays or actions cause hardship. None of these will do the strategic work a complex case needs, but for straightforward situations they cost nothing.

Will hiring a tax relief company stop IRS collections immediately?

No — and any company that promises instant protection is overselling. Filing a power of attorney lets a representative speak for you, and certain filings, like a timely Collection Due Process request or a processable Offer in Compromise, pause specific enforcement actions. But interest and penalties keep accruing through all of it, and every form of relief comes with conditions the IRS enforces.

Can the IRS take my Social Security while I decide what to do?

Yes. Through the Federal Payment Levy Program, the IRS can take up to 15% of your Social Security benefit — continuously, until the debt is resolved or you're placed in hardship status. On a $2,150 monthly benefit, that's about $322 a month. If your benefits are already being reduced or you've received a CP91 notice, act now rather than continuing to compare companies.

Are tax relief companies a scam?

The industry contains both legitimate firms and bad actors, which is why the FTC has taken enforcement action against companies making "pennies on the dollar" settlement promises. Legitimate tax relief is real: IRS payment plans, penalty abatement, hardship status, and Offers in Compromise all exist. The scam is promising a specific outcome before anyone has reviewed your finances — eligibility for every IRS program is means-tested.

Your next 24 hours

- Pull your real numbers. Log in (or sign up) at IRS.gov and note your exact balance, the tax years involved, and the most recent notice on your account — that's the fact set every quote should be built on.

- Gather three things: your last filed return, any IRS letters you've received, and a rough monthly picture of your income and essential expenses. That's everything needed to match you to a program.

- Get a free, no-pressure comparison point. Call (888) 825-7779 or use the 2-minute form. An experienced tax professional will tell you which option your finances actually fit — including "handle it yourself" when that's the honest answer — before another month of penalties and interest posts to your account.

Primary sources worth bookmarking as you compare: the IRS's own payment plans and installment agreements page, the official Offer in Compromise page, and the independent Taxpayer Advocate Service.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Clarity Tax Relief is not affiliated with Optima Tax Relief; references to other companies describe industry patterns generally and are not statements about any specific firm's practices in your case.