Tax Relief Consumer Protection

Tax Relief Company Took My Money: How to Get It Back and Still Fix Your IRS Debt (2026)

The short answer: if a tax relief company took your money and delivered nothing, work two tracks at once. Recover the fee — written refund demand, credit card chargeback (generally within 60 days of the statement), state attorney general and FTC complaints, small claims court — and fix the tax debt yourself, because the IRS never stopped collecting.

You paid thousands up front. Then your "case manager" changed twice, the calls started going to voicemail, and this week another IRS notice landed in your mailbox as if nothing was ever filed. If you're searching "tax relief company took my money," you already suspect the truth — and being burned by the people you hired to protect you stings twice. Both problems in front of you are fixable, though, and the playbook below is concrete: get the fee back through the channels that actually work, then close out the tax debt the company left growing.

⏱ The clock that matters most right now: under the Fair Credit Billing Act, you generally have 60 days from the date of the card statement showing the charge to dispute it in writing. And whatever the company told you, IRS penalties and interest keep posting to your balance every month.

Why the tax relief company took your money and went quiet

Most complaints about tax relief companies follow one script: a large upfront fee, a salesperson's settlement promise, then months of silence while the IRS keeps collecting. The person who signed you up was almost certainly a commissioned closer, not a tax professional. Their job ended when your payment cleared. Your file then went to an overloaded back office — or nowhere at all.

The bait is usually a version of "settle for pennies on the dollar." That pitch is the scam, not the program. The Offer in Compromise is real, but it's a strict means test — the IRS accepted roughly 1 in 5 offers in FY2024 — and no honest professional can promise you a settlement before analyzing your income and assets. The FTC has permanently banned tax relief operators over exactly these deceptive claims, including an action in 2026. We break down the full playbook in our guide to the offer in compromise mill.

Many of these firms also structure contracts to keep your money even when they do nothing: a non-refundable "investigation phase" fee, then a separate "resolution phase" fee, with the money-back guarantee quietly limited to only one of them. If you're rereading your contract and recognizing the pattern, our tax relief company red flags checklist will confirm what you're looking at.

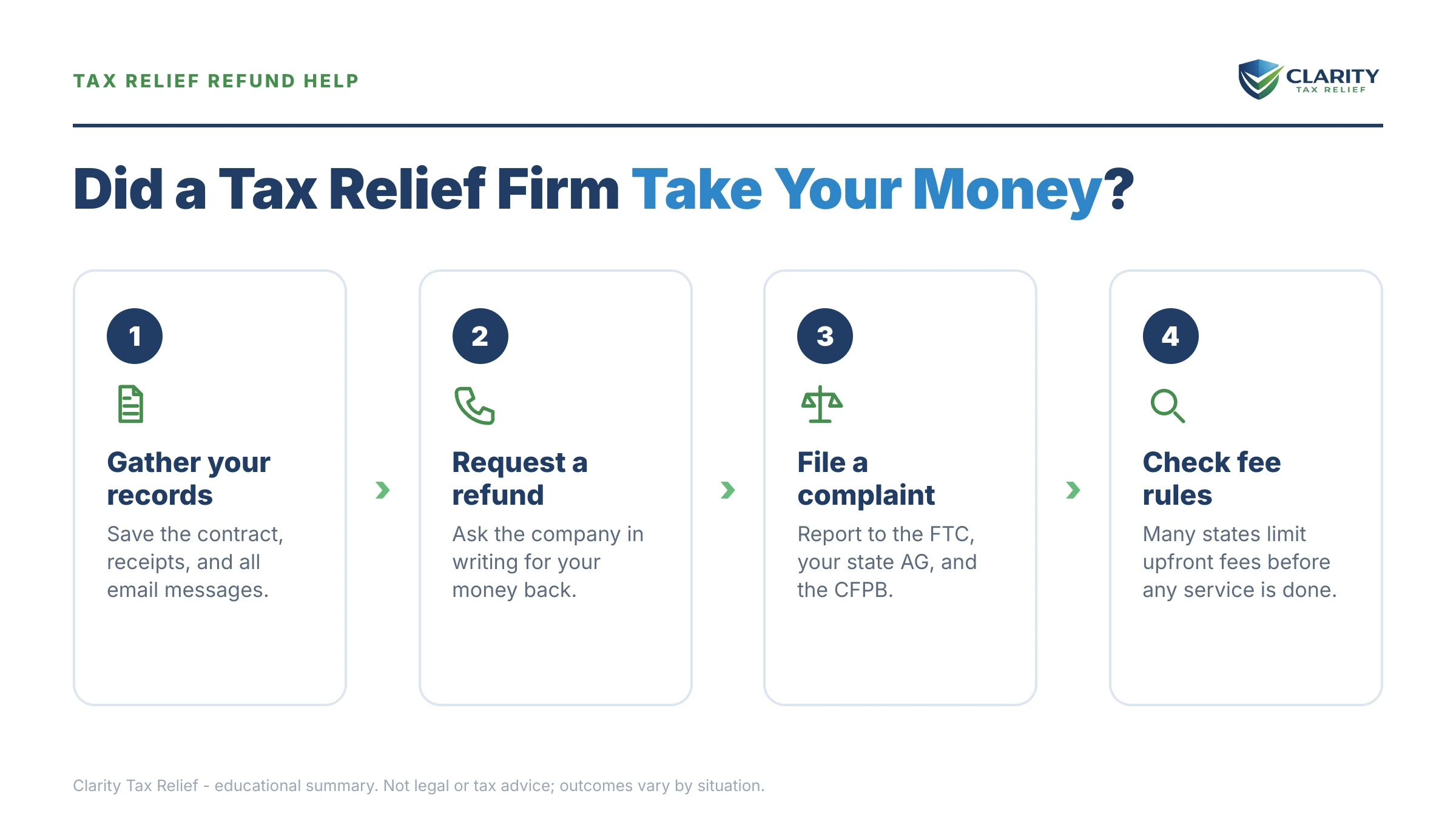

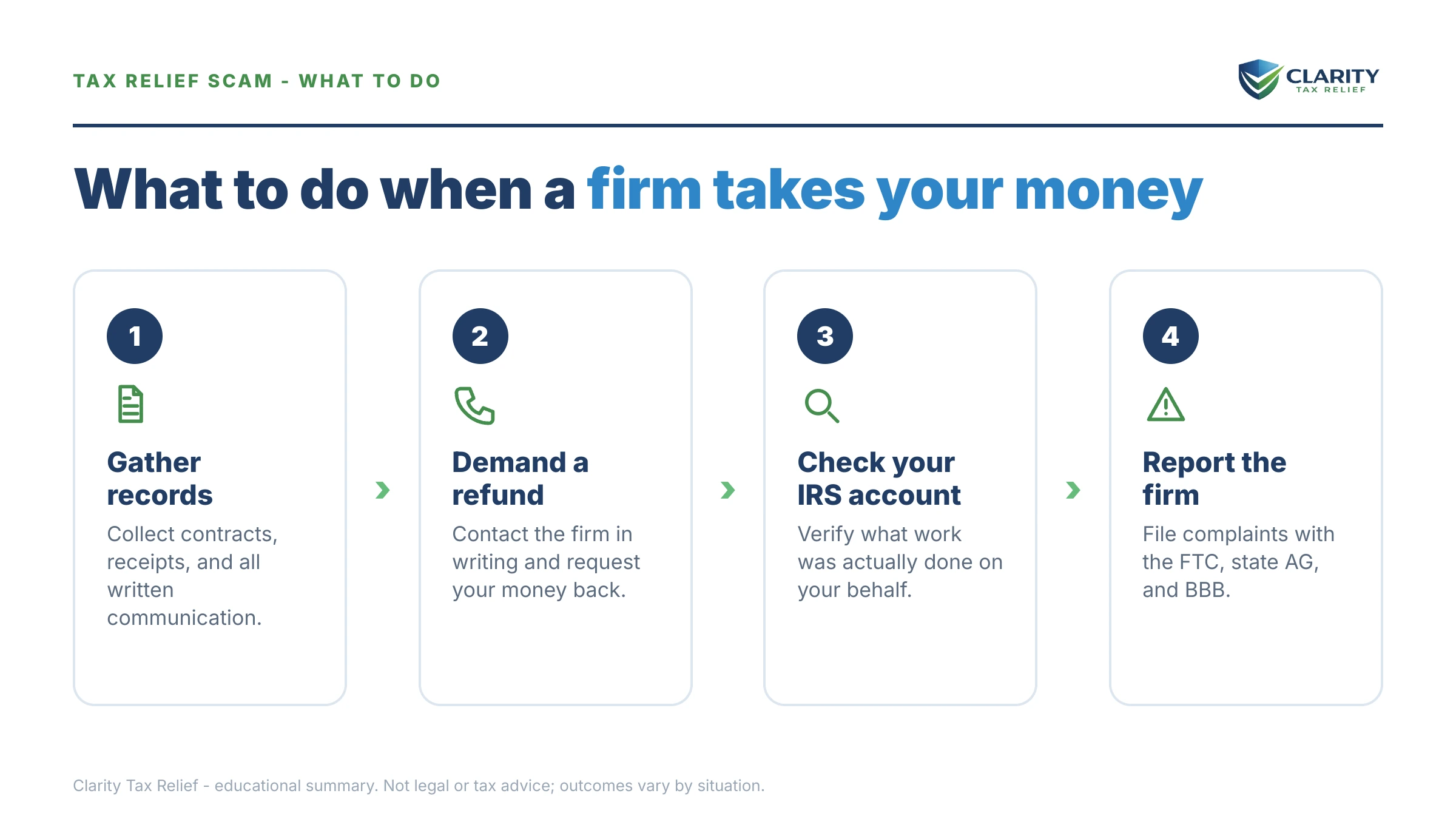

First, find out what the company actually did (it's often nothing)

You can verify every action a tax relief company took on your IRS account in about 20 minutes, without asking them. Log into your IRS online account and pull your account transcripts — here's how to get IRS transcript online if you've never done it.

Three things to look for. First, whether a Form 2848 power of attorney is even on file — some firms never file one, which means they never had authority to speak to the IRS about you at all. Second, whether anything was actually submitted: a pending Offer in Compromise shows as code 480 on your transcript, and an installment agreement shows as an active payment plan on your account. Third, what your balance is today versus the day you hired them.

If the transcripts show nothing but monthly penalty and interest postings since you signed the contract, that transcript is your evidence of non-performance — for the chargeback, the attorney general, and small claims court. Also ask the company, in writing, for a complete copy of your case file. Silence or stalling is itself useful documentation.

What happens if you keep waiting

Every month you spend chasing the company, your IRS balance grows and your recovery windows shrink. The damage compounds on a predictable sequence:

- Penalties and interest keep posting. The failure-to-pay penalty adds 0.5% of the unpaid tax every month, and interest compounds on top of the whole balance.

- The IRS notice sequence keeps advancing. The automated collection stream doesn't pause because you "hired someone" — see the table below for what may already have arrived.

- Your chargeback window closes. The Fair Credit Billing Act's 60-day clock runs from your statement date, whether or not you've realized the service was never performed.

- A filed-and-abandoned Offer in Compromise quietly extends collection. If the firm did lob in an OIC and let it die, the review period paused your 10-year collection statute — meaning your debt now lives longer than if they'd done nothing.

- Enforcement eventually lands — state refund seizure, then levy rights after a final notice. The further this runs, the fewer good options remain.

| Notice | What it means | The clock it starts |

|---|---|---|

| CP14 | First bill for the balance due | About 21 days before the sequence escalates (10 business days if the balance is $100,000 or more) |

| CP501 / CP503 | Reminder notices — still just bills | No enforcement yet, but the balance grows monthly |

| CP504 | Intent to levy your state tax refund (IRC §6331(d)) | State refund can be seized; a lien becomes realistic |

| LT11 / Letter 1058 | Final notice of intent to levy | 30 days to request a Collection Due Process hearing (Form 12153) before wage and bank levies |

Dig any recent envelopes out of the drawer and check which of these you're holding. Where you sit in this sequence determines how urgent the tax side of your problem is — separate from the refund fight.

Paid a tax relief firm and got nothing?

Send us your transcripts and the contract. An experienced tax professional will tell you exactly what the company did or didn't do, where your IRS account stands, and your fastest real fix — free, confidential, no pressure. Penalties and interest are accruing either way; find out where you actually stand.

How to get your money back from a tax relief company

You have at least six recovery channels, and the fastest one is usually a credit card chargeback. Use several at once — they don't conflict, and each creates pressure the others can use.

| Recovery channel | What it can get you | Window | Cost |

|---|---|---|---|

| Written refund demand | Full or partial refund under their own guarantee terms | Now — do this first; it strengthens every other channel | Free |

| Credit card chargeback | Reversal of the charge back to your card | Generally 60 days from the statement date; issuers often take services-not-received disputes later | Free |

| Bank / ACH dispute | Reversal of a debit or transfer | Windows are shorter and vary by bank — call immediately | Free |

| State attorney general complaint | Investigation, mediation, sometimes restitution | No fixed deadline; sooner is stronger | Free |

| FTC and CFPB reports | Federal enforcement record; CFPB routes your complaint to the company for response | Anytime | Free |

| Small claims court | Judgment up to your state's limit (often $5,000–$10,000) | Your state's contract statute of limitations | Modest filing fee |

The refund demand. One page, sent by email and certified mail: the date you signed, what the contract promised, what your IRS transcripts prove was never done, the amount you paid, and a firm response deadline (two weeks is reasonable). Reread the guarantee language first — many contracts refund only the "resolution phase" fee, which tells you what to fight for and what to write off.

The chargeback. Call the number on the back of your card, say you're disputing a charge for services not received, then follow up in writing. Your evidence package: the contract, the sales promises (texts and emails count), your payment records, and transcripts showing no filings. If the charge is older than 60 days, dispute anyway — the failure only became apparent later, and issuers frequently accept that reasoning for non-performance.

The attorney general. File a consumer complaint with the AG in your state and in the company's home state. Firms that ignore customers for months often respond to an AG inquiry within weeks, because a pattern of complaints is what triggers enforcement. Then file federal reports at ReportFraud.ftc.gov and with the CFPB complaint system — the FTC won't resolve your individual case, but bans and shutdowns are built from reports like yours.

Small claims. For a typical fee, this is the right-sized lawsuit: no lawyer required, and your claim is simple breach of contract. Many defendants settle when served rather than explain an empty case file to a judge. If your losses are large or the conduct looks criminal, that's different territory — our tax relief attorney vs company guide covers when a lawyer earns their fee.

One more report worth filing: if an enrolled agent, CPA, or attorney was named on your Form 2848, their conduct can be reported to the IRS — Form 14157 covers preparer and practitioner complaints, and the IRS Office of Professional Responsibility disciplines credentialed representatives. It won't refund you, but it protects the next person and adds weight to your other filings.

Meanwhile, your $8,900 IRS debt still needs a real fix

An IRS balance of $10,000 or less in tax qualifies for a guaranteed installment agreement — a plan the IRS must accept if you've filed all required returns and can pay within three years. That's worth sitting with for a second: for many people in this situation, the fix the company charged thousands for is something the IRS is required to give you.

Say you're a 1099 contractor who owed $8,900 when you hired the firm, and paid them $3,800 — an $800 "investigation" fee plus $3,000 for "resolution." Fourteen months of nothing later, here's the arithmetic. The failure-to-pay penalty alone added roughly 0.5% × $8,900 = $44.50 a month — about $623 over 14 months — and compounding interest added several hundred dollars more, pushing the total balance past $10,200. You can estimate your own accruals with our IRS penalty and interest calculator.

Two things follow from that math. First, the guaranteed agreement's $10,000 line looks at tax, not penalties and interest — so the $8,900 still qualifies even though the total has climbed higher. Spread over 36 months, roughly $10,200 works out to about $285–$300 a month while interest continues. Second, the $3,800 fee could have paid down over 40% of the original tax. That's the real cost of the detour.

And the settlement they promised? With steady contractor income, the IRS's collection-potential math on an $8,900 debt almost always shows you can pay in full over time — meaning an Offer in Compromise was likely never viable for you, and a competent reviewer would have said so in the first call. What may be genuinely recoverable is the penalty: with a clean compliance history for the prior three years, first-time penalty abatement can remove the failure-to-pay penalty, and starting summer 2026 the IRS's Automatic Exemption from Penalty (AEP) applies similar relief automatically in eligible cases.

Setting the plan up takes under an hour: here's how to set up IRS payment plan online (or file Form 9465 by mail), and our pillar on how to settle tax debt yourself walks through every resolution option — payment plans, hardship status, offers, penalty relief — so you can see the whole board before deciding whether you need anyone's help at all.

How to respond, step by step

- Revoke the power of attorney. If the company filed Form 2848, revoke it — write "REVOKE" across a copy of the form, re-sign and date it, and send it to the IRS — so they can no longer speak to the IRS for you.

- Demand your refund in writing. Send an email plus a certified letter citing the contract, what was promised, what was never done, and a firm response deadline.

- Dispute the charges. Call your card issuer or bank the same day — the Fair Credit Billing Act window generally runs 60 days from your statement date.

- Report the company. File with your state attorney general, the FTC, and the CFPB; if a credentialed practitioner misbehaved, add Form 14157 to the IRS.

- Pull your IRS transcripts. Confirm exactly what was — or wasn't — filed on your account and what your balance is today.

- Set up your own fix or get a second opinion. A balance in the $8,900 range usually resolves with a payment plan you can open online in under an hour.

When you can handle this yourself — and when help changes the outcome

Most of the recovery fight needs no professional at all. The refund demand, the chargeback, the AG and FTC complaints, and a small claims filing are all built for consumers — and if your remaining tax balance is under $10,000 with all returns filed, the payment plan is genuinely a do-it-yourself job. You do not need to pay a second company to undo the first one's damage in that situation.

Experienced help changes the outcome when the neglect left real wreckage: a levy or garnishment already in motion, a final notice whose 30-day appeal window is running, multiple unfiled years the firm ignored, an Offer in Compromise filed and abandoned mid-review, or a balance that grew past $50,000 while the file sat. Those cases have deadlines and sequencing that are unforgiving of a second mistake. If you do hire again, vet differently this time — start with our questions to ask tax relief company list and the buyer's checklist in how to choose a tax relief company.

Terms in your contract and on your account, decoded

- Investigation phase — the upfront fee for "reviewing your case"; in practice, often just pulling the same transcripts you can pull free in 20 minutes.

- Resolution phase — the second, larger fee for actually doing the work; check whether the money-back guarantee covers this fee, the first one, or neither.

- Form 2848 (power of attorney) — the form authorizing the company to represent you before the IRS; revocable by you at any time.

- CAF number — the IRS-issued ID for authorized representatives; a "professional" without one was never able to represent anyone.

- Offer in Compromise — the real IRS settlement program; means-tested, slow, and accepted roughly 1 in 5 times, not a coupon anyone can invoke.

- Chargeback — a card issuer reversing a charge after you dispute it; your strongest fast-money remedy for services never delivered.

Tax relief refund questions, answered

Can I get my money back from a tax relief company?

Often, yes — especially if you paid by credit card and can show the company did little or nothing. The strongest paths are a written refund demand citing the contract, a card chargeback, a state attorney general complaint, and small claims court. Recovery is hardest when you paid by wire or the company has dissolved, which is why moving quickly matters.

How long do I have to dispute the charge on my credit card?

Under the Fair Credit Billing Act, you generally have 60 days from the date of the statement showing the charge to dispute it in writing. If the charge is older, call your issuer anyway — many card networks accept services-not-received disputes later, because the company's failure to perform only became apparent months after you paid.

How do I know if the tax relief company filed anything with the IRS?

Check your IRS online account and pull your account transcripts — every filing, payment, and status change appears there. A pending Offer in Compromise shows as transcript code 480; a payment plan shows as an active installment agreement. If your transcripts show nothing but growing penalties and interest since you hired the firm, that is your evidence of non-performance.

Should I report the company to the FTC or my state attorney general?

Both — they do different jobs. Your state attorney general handles individual consumer complaints and can pressure the company toward restitution; firms often respond faster to an AG letter than to yours. The FTC does not resolve individual cases, but your report feeds enforcement — the FTC has permanently banned tax relief operators over deceptive settlement claims, including an action in 2026.

Can I sue a tax relief company in small claims court?

Yes, and for typical fees it is often the right-sized remedy. Small claims limits vary by state — commonly $5,000 to $10,000 — filing fees are modest, and you do not need a lawyer. Your claim is breach of contract: they promised specific services, you paid, they did not perform. Bring the contract, payment records, correspondence, and transcripts showing nothing was filed.

Will the IRS reduce my debt because a company scammed me?

The tax itself does not shrink because you were defrauded, but penalties sometimes can. If you have a clean compliance history for the prior three years, first-time penalty abatement can remove the failure-to-pay penalty — and starting summer 2026, the IRS's Automatic Exemption from Penalty applies some relief with no request needed. Reliance on a bad advisor can also support reasonable-cause relief in some situations.

Are all tax relief companies scams?

No — legitimate firms staffed by enrolled agents, CPAs, and attorneys resolve real cases every day. The dividing line is honesty up front: a real firm reviews your finances before quoting an outcome, puts fees in writing, and tells you when a simple payment plan you could set up yourself is the right answer. A sales floor that promises a settlement before seeing a single number is the warning sign.

Your next 24 hours

- Find the charges. Pull the exact dates and amounts from your card or bank statements — your dispute window runs from the statement date, so this determines how fast you need to call.

- Gather your file. The signed contract, every email and text with the company, payment receipts, and any IRS notices that have arrived — this one stack powers the chargeback, the AG complaint, and small claims all at once.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map what the company left undone and your cheapest path to closing the debt — because penalties and interest are still posting to your balance every month it stays open.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.