IRS Questions Answered

Aggregated PAA Harvest 2026: The IRS Tax Debt Questions Everyone Asks, Answered

The short answer: this page is an aggregated PAA harvest — the "People Also Ask" questions taxpayers with IRS debt search most in 2026, answered in one place. The three facts that matter behind all of them: penalties and interest grow monthly, collection escalates on a fixed sequence, and every balance has a legal resolution path.

It's 11 p.m. and you're six searches deep: does the IRS forgive debt… can they take my paycheck… will I go to jail. Each answer sends you to a different page, and the picture never quite assembles. That's what this page fixes — every question answered directly, with the 2026 numbers, so you can stop searching and pick your one next move.

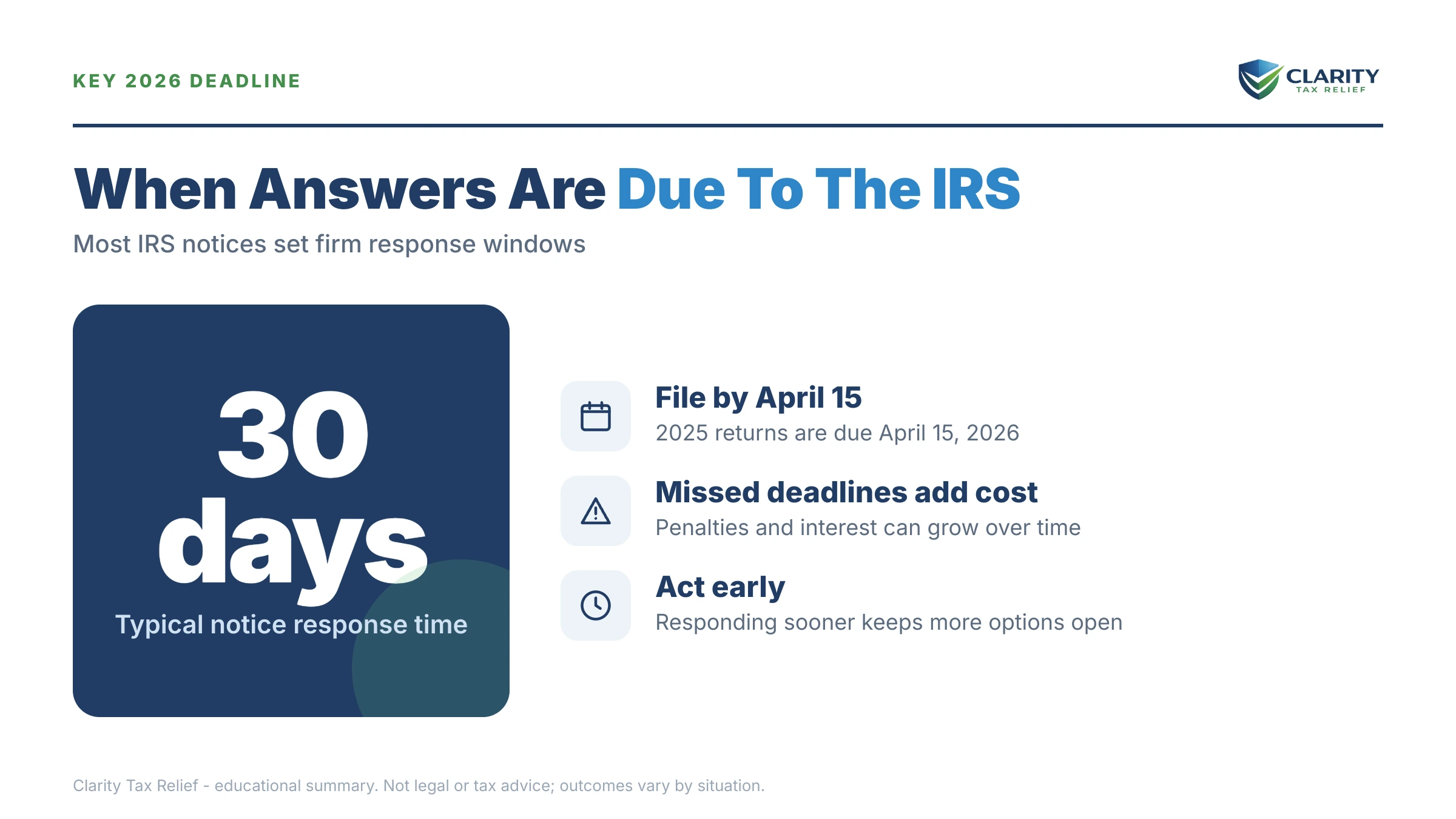

⏱ The only clock that matters: there is no single deadline when you owe the IRS — but the failure-to-pay penalty adds 0.5% of the balance every month, interest compounds on top, and each unanswered notice moves you one automated step closer to a levy. The clock is already running; every option below stops it faster than waiting does.

What this aggregated PAA harvest covers

These are the questions Google's "People Also Ask" boxes surface most for taxpayers who owe. They cluster into six themes: why you owe and how fast it grows, what happens if you never pay, what the IRS can actually take, what your options are, whether forgiveness is real, and what to do first. Each answer links to a deeper guide when your situation needs one.

Why do I owe the IRS — and how fast is the balance growing?

An unpaid IRS balance grows two ways at once: a monthly penalty and daily-compounding interest. The failure-to-pay penalty runs 0.5% of the unpaid tax per month, and interest accrues on the whole balance — tax, penalties, and prior interest together.

If you also didn't file, the math gets ten times worse. The failure-to-file penalty is 5% per month — which is why filing on time, even with zero payment attached, is always the cheaper move. You can estimate your own accrual with our Penalty & Interest Calculator.

And the source of the debt matters less than people think. Whether the balance came from under-withholding, a side gig, or a one-time event, the IRS collects it the same way. Three surprise-bill scenarios dominate the search results:

- A settled credit card became taxable income. Forgiven debt over $600 usually generates a Form 1099-C — see 1099-C cancelled debt taxes for the insolvency exception that can erase that income.

- Online selling triggered a 1099-K. The reporting threshold reverted to $20,000 and 200 transactions — the $600 rule is dead — but balances assessed under the old rules still stand. Details in our guide to the 1099-K $20,000 threshold for 2026.

- An early retirement withdrawal landed with tax plus a penalty. If you cashed out a retirement account and the bill arrived a year later, start with the 401(k) withdrawal tax bill you can't pay.

What happens if you never pay the IRS?

If you never pay, the IRS escalates through a fixed, automated notice sequence that ends in liens and levies — not immediately, but inevitably. The order matters because each stage removes an option you have today:

- CP14 — the first bill. No enforcement yet; typically about 21 days to respond before the sequence advances. The full breakdown is in our CP14 notice guide.

- CP501 and CP503 — reminders. Still just bills, arriving on an automated cadence while the balance compounds monthly.

- CP504 — Notice of Intent to Levy. The IRS can now seize your state tax refund under IRC §6331(d), and a federal tax lien becomes a realistic next step.

- LT11 or Letter 1058 — the final notice. A 30-day clock starts on your Collection Due Process rights (requested on Form 12153). After it runs, wages and bank accounts are fair game. See the LT11 notice guide.

- Levy. A bank levy freezes funds with a 21-day hold before the money leaves; a wage levy repeats every payday until released.

Two more consequences ride alongside the notices. Once your total certified debt reaches $66,000 (the 2026 threshold), the IRS can certify you to the State Department, which can deny or revoke your passport. And the IRS can offset every future tax refund against the balance until it's gone.

The counterweight: collection isn't forever. The IRS generally has 10 years from assessment to collect — the CSED — though appeals, offers, and bankruptcy pause that clock. The full rules are in our guide to the 10-year collection statute.

| Notice or stage | Response window | What's at stake if it passes |

|---|---|---|

| CP14 (first bill) | Typically 21 days from the notice date | The cheapest fix; penalties and interest keep compounding |

| CP501 / CP503 (reminders) | Date printed on the notice | No new rights lost, but escalation continues automatically |

| CP504 (intent to levy) | Date printed on the notice | State tax refund can be seized; lien filing becomes likely |

| LT11 / Letter 1058 (final notice) | 30 days | Your Collection Due Process hearing right (Form 12153) — the strongest appeal you get |

| Bank levy issued | 21-day bank hold | The frozen funds leave your account for the IRS |

| Passport certification | Certified debt reaches $66,000 (2026) | State Department can deny or revoke your passport |

One 2026 reality check: the IRS workforce shrank roughly 27% in 2025, so reaching a human is genuinely harder — but these notices, liens, and levies come from automated systems that never stopped. Slower phones don't mean slower enforcement.

Done searching one scared question at a time?

Whatever your balance or letter says, an experienced tax professional can map your exact spot on this ladder and the option that fits — free and confidential. Penalties and interest accrue monthly either way; a plan stops the escalation.

What are my options if I can't pay the IRS in full?

Every IRS balance has at least four legal resolution paths, and which one fits is decided by your numbers — not by marketing. The eligibility thresholds below are the 2026 figures; the step-by-step mechanics of each live in our pillar on how to settle tax debt yourself.

| Option | Who typically qualifies | Key 2026 numbers |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup fee; interest and penalties continue until paid |

| Guaranteed installment agreement | Owe $10,000 or less and current on all filings | The official program name — approval criteria are set by law |

| Streamlined installment agreement | Owe $25,000 or less — or up to $50,000 with direct debit | Up to 72 months, set up online, no financial statement required |

| Non-streamlined agreement | Balances above $50,000 | Financial disclosure (Form 433-F) required; terms negotiated |

| Currently Not Collectible (CNC) | Paying anything would leave you unable to cover basic living expenses | Collection pauses; debt and interest remain; the 10-year clock keeps running |

| Offer in Compromise (OIC) | Assets plus future income are worth less than the debt, by the IRS's own formula | $205 fee; 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance record for the prior 3 years | Removes penalties, not tax; AEP makes relief automatic starting summer 2026 |

Two of these deserve one extra sentence each. Hardship status is explained honestly in our guide to Currently Not Collectible status — it pauses collection, but the balance keeps growing. And penalty relief is the most under-used option on the list: if the prior three years were clean, first-time penalty abatement can strip penalties from the balance, and starting summer 2026 the new Automatic Exemption from Penalty (AEP) applies that relief without you even asking.

Worked example: single, W-2, and $48,300 in the hole

Say you're a single W-2 employee who owes $48,300 across two tax years. Here's the honest math on each path, all figures hypothetical:

- Short-term plan (180 days): $48,300 ÷ 6 months ≈ $8,050 a month. Realistic only with a bonus, a tax refund elsewhere, or savings to drain.

- Streamlined installment agreement: because $48,300 is under the $50,000 direct-debit ceiling, you can set this up online with no financial disclosure. $48,300 ÷ 72 months ≈ $671 a month just to divide the principal — and since interest plus the 0.5% monthly penalty (roughly $242 in month one, before interest) keep accruing, a realistic payment runs meaningfully higher so the balance actually falls.

- Offer in Compromise: only viable if the IRS's formula says it could never collect $48,300 from you. A renter with an older car and a paycheck that barely covers IRS allowable expenses might show a collection potential far below the balance. But steady W-2 wages with room above allowable expenses — or home equity — usually means the math shows full collection is possible, and the offer fails.

- Do nothing: the notice ladder above runs its course, and while $48,300 sits below the $66,000 passport-certification threshold today, monthly penalties and compounding interest steadily close that gap.

For this profile, the streamlined agreement is usually the realistic answer — set up in an afternoon, enforcement stopped, and penalty abatement pursued separately to shrink what the plan has to repay.

How to respond when you owe the IRS, step by step

- Pull your IRS records. Log into your IRS online account and list every year with a balance and every missing return — you're resolving the whole picture, not one letter.

- File anything unfiled. Filing stops the 5%-per-month failure-to-file penalty and is required before the IRS will approve any payment plan or offer.

- Verify the balance. Match the IRS figure against your return — misapplied payments and wrong-year postings are common and fixable with proof.

- Choose the option your numbers support. Use the eligibility table above: under $50,000 with steady income points to a streamlined plan (online, or by mail on Form 9465); genuine hardship points to CNC or an offer.

- Set it up before the next notice lands. Every step down the escalation ladder removes options — even a plan started today stops the sequence.

Will the IRS take my paycheck, bank account, or refund?

The IRS can reach all three — but only the refund goes without a final warning. Refund offset is automatic: any federal refund you're due gets applied to the back balance, year after year, until it's paid.

Paychecks and bank accounts require the final-notice process first (LT11 or Letter 1058, plus the 30-day window). After that, the two levies behave very differently. A bank levy is a snapshot — it grabs what's in the account that day, then the bank holds it 21 days before remitting, which is your window to negotiate a release. A wage levy is continuous: it hits every paycheck until the IRS releases it, leaving you only a small exempt amount based on filing status and dependents.

Federal benefits aren't fully safe either: the Federal Payment Levy Program can take up to 15% of Social Security payments. What the IRS can't do is levy while a payment plan, accepted hardship status, or pending offer is on file — which is exactly why setting something up beats waiting.

What if I haven't filed in years?

Unfiled returns are the one problem that must be fixed before any other, because the IRS won't approve a plan, hardship status, or offer while required returns are missing. Three facts reshape most non-filers' fear:

- Filing is cheaper than hiding, always. The math is in file even if you can't pay — the file-late penalty is ten times the pay-late penalty.

- The IRS may have "filed" for you. A substitute-for-return uses no deductions, no credits, and the worst filing status — meaning the assessed balance is usually inflated, and filing your real return can shrink it.

- Old refunds expire. You generally have three years to claim a refund for an unfiled year. Non-filers are often owed money for recent years — but only if they file in time.

Is IRS tax debt forgiveness actually real?

Forgiveness is real, narrow, and math-tested — and everything advertised beyond that is marketing. The genuine article is the Offer in Compromise: the IRS agrees to accept less than the balance when its own formula shows the debt exceeds what it could ever collect from your assets and future income. How that formula works — and why the IRS accepted only about 1 in 5 offers in FY2024 — is covered in how an offer in compromise actually works.

Any firm promising to settle your debt for "pennies on the dollar" before it has seen a single financial document is describing a sales pitch, not a program — the eligibility math exists before anyone signs anything. Two honest footnotes: low-income taxpayers (AGI at or below 250% of the poverty level) get the $205 fee, the 20% down payment, and payments during review all waived; and if the IRS doesn't decide an offer within two years, it's accepted by law.

The other real endpoint is time: the 10-year collection statute genuinely extinguishes debt at the CSED. But the clock pauses during offers, appeals, and bankruptcy, so "wait it out" is a strategy that usually costs a decade of liens, levies, and offsets — and often still fails, since certification of a large balance can also cost you a passport. See passport revoked for tax debt if you're anywhere near the $66,000 line.

When you can handle this yourself — and when help changes the outcome

Most people with one balance-due year and a debt under $50,000 can resolve this themselves, online, in under an hour. If you agree with the amount, your returns are filed, and a 72-month payment fits your budget, set up the streamlined agreement directly and stack penalty abatement on top. You don't need to pay anyone for that.

Experienced help earns its cost in specific situations: a levy or garnishment already in motion (release negotiations are time-boxed and technical), multiple unfiled years (the order you file in changes the total assessed), balances over $50,000 (financial-disclosure negotiation determines your payment), Offer in Compromise math (most rejections are avoidable valuation errors), and any business or payroll tax debt (personal liability rules apply). If any of those describes you, a free review before you act costs nothing and can change what you ultimately pay.

Free and official resources exist too: IRS.gov/payments for paying or starting a plan, the IRS's own payment plans page for eligibility details, and the independent Taxpayer Advocate Service if IRS processes themselves are causing you hardship.

Terms you keep seeing, decoded

- Lien: the government's legal claim against your property as security for the debt — it doesn't take anything, but it clouds titles and shows up in public records.

- Levy: the actual seizure — money from a bank account, a slice of every paycheck, or a state refund.

- CSED: Collection Statute Expiration Date — the day, generally 10 years after assessment, when the IRS's right to collect that balance ends.

- CDP hearing: the Collection Due Process appeal (Form 12153) triggered by the final levy notice — your strongest formal chance to propose an alternative before enforcement.

- CNC: Currently Not Collectible — hardship status that pauses collection while the debt, and interest, remain.

- RCP: Reasonable Collection Potential — the IRS's formula (assets plus future income) that decides whether an Offer in Compromise can be accepted.

The questions people also ask, answered

Does the IRS ever forgive tax debt?

Yes, but only through defined programs with strict math — there is no general amnesty. An Offer in Compromise can settle a debt for less than the balance when your assets and income genuinely can't cover it, but the IRS accepted roughly 1 in 5 offers in FY2024. Separately, the 10-year collection statute can end a debt, though appeals, offers, and bankruptcy pause that clock.

How long can the IRS collect back taxes?

Generally 10 years from the date each balance was assessed — the Collection Statute Expiration Date, or CSED. The clock pauses while an Offer in Compromise, Collection Due Process appeal, or bankruptcy is pending, so many debts run longer than 10 calendar years. Each tax year has its own CSED, so a 2019 balance and a 2022 balance expire at different times.

Can the IRS take money from my bank account without warning?

Not without notice — the IRS must send a final notice of intent to levy (LT11 or Letter 1058) and wait 30 days before levying most accounts. But if you've moved or stopped opening mail, that notice may have satisfied the law without ever reaching you. Once a bank levy lands, the bank holds the funds for 21 days before sending them to the IRS — that hold is your window to get the levy released.

Can you go to jail for owing the IRS?

No — simply owing tax you can't pay is a civil matter, and the IRS resolves it with liens, levies, and payment programs, not handcuffs. Criminal exposure comes from willful acts: filing false returns, hiding income, or refusing to file year after year despite the ability to do so. If you filed honestly and just can't pay, jail is not on the table.

Does owing the IRS affect your credit score?

Not directly — the three credit bureaus removed tax liens from credit reports in 2018, so an IRS balance does not lower your score. But a filed Notice of Federal Tax Lien is still a public record that mortgage lenders find during underwriting, and it can block or complicate a home purchase or refinance until it is addressed.

How much can the IRS take from my paycheck?

More than almost any other creditor. An IRS wage levy is continuous — it repeats every payday until it is released — and instead of capping what the IRS takes, the law only protects a small exempt amount based on your filing status and dependents. Everything above that exempt amount goes to the IRS, which for many workers is most of the check.

Should I file my return if I can't pay what I owe?

Always file. The failure-to-file penalty runs 5% of the unpaid tax per month — ten times the 0.5% monthly failure-to-pay penalty — and each can build toward a 25% cap. Filing on time and paying nothing costs roughly a tenth of what not filing costs. Filing is also required before the IRS will approve any payment plan or offer.

Is the IRS Fresh Start program real?

Fresh Start is real, but it is not a new forgiveness program — it is the name the IRS gave a set of changes that expanded existing programs like streamlined installment agreements and the Offer in Compromise. Companies advertising a special 2026 Fresh Start initiative that erases debt are selling access to programs you can apply to directly, on eligibility the IRS alone decides.

Your next 24 hours

- Find your most recent IRS notice and circle two things: the notice date and the total balance. Those two numbers place you on the escalation ladder above and tell you which rights are still open.

- Gather your last filed return, income documents for any unfiled year (W-2s, 1099s), and a rough monthly budget — every option in the table above is chosen from exactly those inputs.

- Get a free case review — call (888) 825-7779 or use the 2-minute form at the link above. There's no single statutory deadline on a growing balance, but penalties and interest accrue every month until something is in place; a plan started this week stops the sequence where it stands.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.