Tax Relief Companies

Community Tax Alternative: How to Choose the Right Tax Relief Help in 2026

The short answer: the best Community Tax alternative isn't a name — it's a checklist. Choose a firm that verifies your IRS balance first, quotes a flat written fee, names the credentialed person (EA, CPA, or attorney) working your case, and never promises a settlement before reviewing your finances. Compare at least two firms against those four tests.

You've already sat through at least one sales call. Maybe Community Tax quoted you a resolution plan, maybe you're comparing before anyone gets your credit card — and with a $68,500 balance and a refinance on your calendar, this isn't a decision you can afford to get wrong. The good news: choosing well is a checklist, not a gamble, and this guide is the checklist.

One disclosure up front: Clarity Tax Relief is itself one of the alternatives. So read this as a framework, not a verdict — every test below applies to us just as hard as it applies to anyone else.

⏱ The real clock: there's no notice deadline on comparison shopping — but the IRS failure-to-pay penalty (0.5% per month) plus interest posts to your balance every month you deliberate. And once a debt passes $66,000 (the 2026 threshold), passport certification becomes possible if it goes seriously delinquent. Compare carefully, but compare fast.

Why people search for a Community Tax alternative

Most searches for a Community Tax alternative come down to three fit questions: fee clarity, direct access to the credentialed person on your case, and specialization. None of those are accusations — they're the same questions you should ask about any large national firm, ours included.

Community Tax is one of the bigger national tax-resolution companies, handling everything from tax prep to full collection cases. High-volume firms can do good work. But scale changes the client experience in ways that matter to some people and not others.

The most common reasons readers tell us they're shopping around:

- They want the EA, CPA, or attorney directly — not a case-manager layer between them and the person who actually negotiates with the IRS.

- They want the whole fee in writing before phase one — what the investigation costs, what resolution costs, and what triggers a refund.

- Their problem is specialized — payroll tax, state debt, or a large balance that needs someone who works that exact case type weekly.

- They want a second opinion on a quoted plan before committing thousands of dollars. A second opinion costs nothing; unwinding a bad engagement can cost far more.

If you're comparing several firms at once, our Anthem Tax Services alternative, Fortress Tax Relief alternative, and Ideal Tax alternative guides use this same framework, so you can line every quote up side by side.

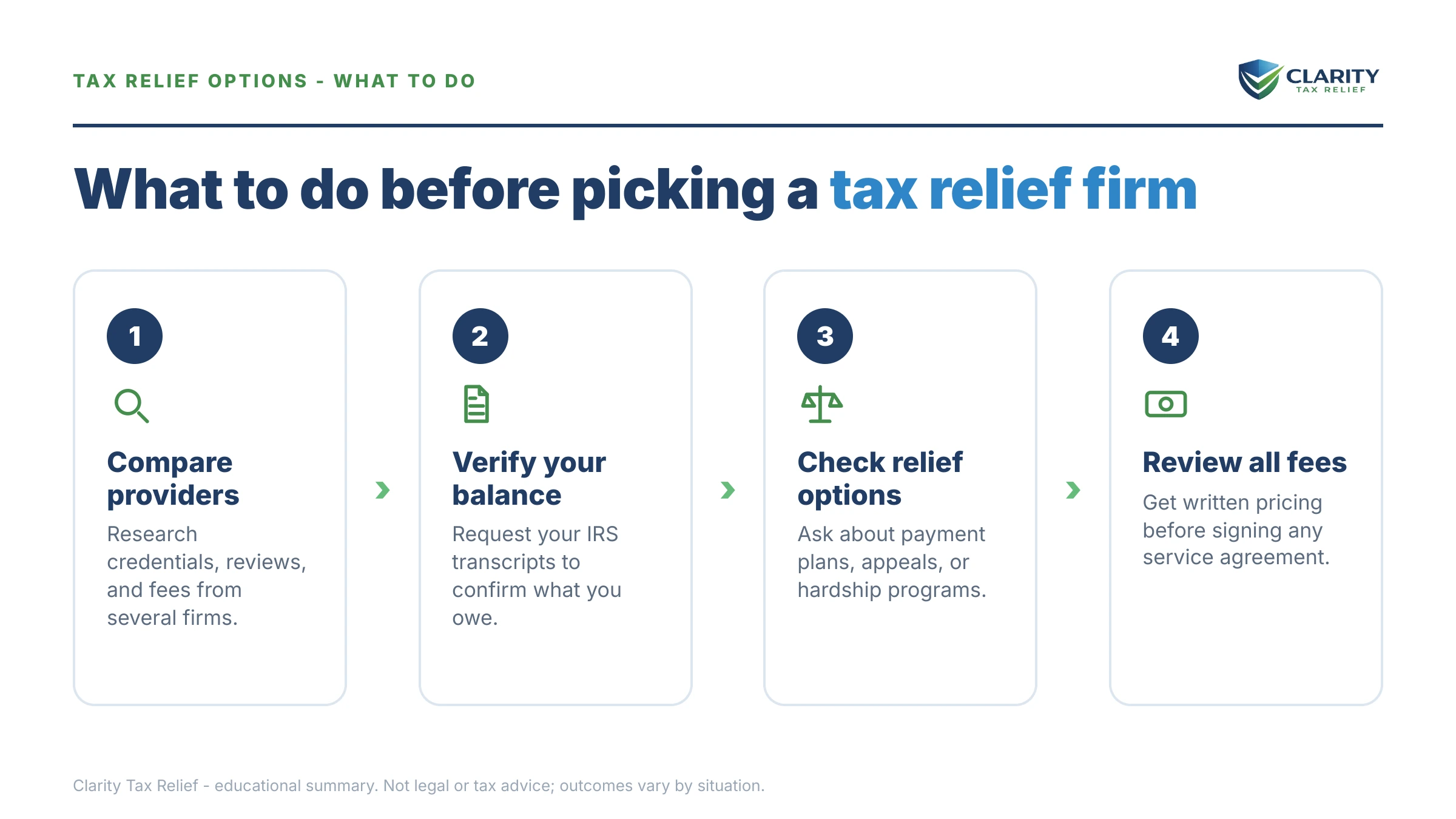

The four tests that separate a good firm from an expensive mistake

Four tests separate a trustworthy tax relief firm from a costly one, and every test can be run in a single phone call. This is the compressed version of our full guide on how to choose a tax relief company:

- Test 1 — Balance verification before promises. A serious firm pulls your IRS transcripts (or has you pull your online account) before quoting a resolution. Anyone who names your outcome before seeing your numbers is guessing — or selling.

- Test 2 — A flat written fee, phased. Investigation first, resolution second, refund terms spelled out in the engagement letter. Verbal estimates and "percentage of savings" pricing are walk-away signals.

- Test 3 — A named, credentialed representative. Ask who signs Form 2848 — the power of attorney that lets someone speak to the IRS for you. If the answer is vague, the salesperson doesn't know either.

- Test 4 — No settlement promises. "Pennies on the dollar" is a marketing fiction, not a program — IRS settlement eligibility is means-tested against your actual assets and income, and regulators have shut firms down over exactly these promises. The full list of warning signs is in our tax relief company red flags checklist.

Run those four, then use our list of questions to ask a tax relief company on the follow-up call. A firm that resents the questions has answered them.

What waiting costs you: the IRS clock runs while you compare

IRS penalties and interest post to a $68,500 balance every single month you spend deciding between firms. The collection notices run on an automated sequence, and no consultation call pauses it:

- CP14 — the first bill, with roughly 21 days to pay before the sequence continues (10 business days when the balance is $100,000 or more).

- CP501 / CP503 — reminder notices. Still just bills, but the balance compounds while they arrive.

- CP504 — Notice of Intent to Levy. The IRS can seize your state tax refund, and a Notice of Federal Tax Lien becomes a live risk — the exact event that complicates a refinance, since the lien attaches to your home.

- LT11 / Letter 1058 — the final notice. It starts a 30-day clock with Collection Due Process appeal rights (Form 12153); after that, wage garnishment and bank levies are on the table.

Two 2026-specific pressures stack on top. First, a balance over $66,000 that goes seriously delinquent can be certified to the State Department, blocking passport renewal — details in our guide to passport revoked for tax debt. Second, IRS staffing fell roughly 27% in 2025, which means longer phone waits for you — but the levy and lien systems are automated and never stopped. Slow humans, fast machines: the worst combination for someone who waits.

Comparing firms with $68,500 on the line?

Send us the quote you were given — or just your latest IRS notice. An experienced tax professional will verify your real balance, map your actual options, and tell you honestly whether you need a firm at all. Free, confidential, and the interest clock is the only pressure: penalties keep posting every month this sits.

The options every firm is actually selling: IRS programs and who qualifies

Every legitimate firm — Community Tax, Clarity, a solo enrolled agent — can only use the same IRS programs, because the IRS runs the programs, not the firms. What you're really buying is judgment about which program fits and execution getting it approved. The general playbook lives in our guide to how to settle tax debt yourself; here's the map, with the $50,000 threshold that matters most at your balance:

| Option | Basic eligibility | Upfront cost | Fit for a $68,500 balance |

|---|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup | Works if refinance cash-out or savings can clear it fast |

| Streamlined installment agreement | Balance $50,000 or less; up to 72 months online | Setup fee (reduced online / with direct debit) | Not directly — you'd need to pay the balance below $50,000 first |

| Non-streamlined installment agreement | Balance over $50,000; requires Form 433-F or 433-A financials | Setup fee | The default path at this amount |

| Offer in Compromise (Form 656) | Assets plus future income genuinely can't cover the debt | $205 fee + 20% down on lump-sum offers (waived with low-income certification) | Home equity usually prices refinance-ready homeowners out — run the math first |

| Currently Not Collectible | Paying anything would prevent basic living expenses | $0 | Unlikely with refinance-level income, but real for genuine hardship |

| Penalty relief (FTA / AEP / Form 843) | Clean compliance history or reasonable cause | $0 | Stacks on top of any option above to trim the total |

Two 2026 notes on that table. First, penalty relief is changing: First-Time Abatement is being replaced by the Automatic Exemption from Penalty (AEP) starting summer 2026, which applies automatically with no request — so don't let any firm bill you heavily for relief the IRS may grant on its own. Second, the IRS accepted roughly 1 in 5 offers in FY2024, and unpaid offers are auto-accepted only if the IRS fails to decide within 2 years — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. An Offer in Compromise is real, but it is math, not mercy.

Worked example: $68,500, a house, and a refinance on the calendar

Say you owe $68,500 and plan to refinance a home worth $420,000 with a $260,000 mortgage. This is hypothetical, but the arithmetic is exactly what any honest firm should walk you through on the first call:

- The offer math. For an Offer in Compromise, the IRS calculates Reasonable Collection Potential — roughly your equity at quick-sale value plus future income. Quick-sale value: $420,000 × 80% = $336,000. Minus the $260,000 mortgage = $76,000 in reachable equity. That alone exceeds the $68,500 debt, so the IRS sees a full-pay case — an offer is almost certainly dead on arrival, no matter who files it. You can estimate where your own numbers land with our Offer in Compromise Calculator.

- The payment-plan math. At $68,500 you're above the $50,000 online threshold. Path A: submit Form 433-F financials for a non-streamlined agreement — our guide to an IRS payment plan over $50,000 covers what the IRS looks at. Path B: pay $18,500 down (savings, or the refinance cash-out itself), then set up the remaining $50,000 online — $50,000 ÷ 72 months ≈ $695/month, while interest and the late-payment penalty keep accruing on the declining balance.

- The refinance math. If no Notice of Federal Tax Lien has been filed yet, resolving the balance now keeps your closing clean — see can I refinance with an IRS lien. If a lien is already recorded, your lender will likely require a payoff at closing or a tax lien subordination on Form 14134 so the new mortgage takes priority. And if the refinance can produce the full $68,500 in cash-out, a $0-setup 180-day short-term plan can bridge you to the closing date.

- The passport math. At $68,500 you're over the $66,000 certification threshold — but a debt in a good-standing payment plan is generally not certified as seriously delinquent. One more reason the plan matters more than the firm.

Notice what just happened: ten minutes of arithmetic ruled out the product some firms would happily charge you to pursue. That's the entire value of a second opinion.

Owe a different amount? Realistic options by balance band

Your balance decides which IRS options are realistically open before any firm gets involved — up to 72 months to pay is available at most bands, but the paperwork changes sharply at each threshold:

| You owe | Realistic options | Watch out for |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement — approval is essentially procedural if your filings are current | Interest still accrues; file every missing return first |

| $10,000–$25,000 | Streamlined plan, up to 72 months, no financial disclosure | A missed payment can default the agreement |

| $25,001–$50,000 | Streamlined plan with direct debit; full online setup | Direct debit is generally required at the top of this band |

| $50,001–$100,000 | Non-streamlined plan with Form 433-F, an OIC if equity and income are genuinely low, or pay down below $50,000 | Lien filing risk; passport certification above $66,000 |

| Over $100,000 | Full financial review, often with an assigned revenue officer; every option is documentation-heavy | Get representation lined up before making contact |

How to vet a Community Tax alternative, step by step

- Verify your balance directly with the IRS — log into your IRS online account so every firm quotes the same verified number, not your guess.

- Demand the fee in writing — a flat, phased fee with refund terms in a signed engagement letter, never a verbal estimate or a percentage of promised savings.

- Confirm who actually works your case — ask for the name and credential (EA, CPA, or attorney) of the person who will sign Form 2848 as your representative.

- Compare two firms on identical facts — give each the same balance, income, and equity numbers, and reject any firm that promises a settlement before reviewing them.

- Protect the account while you decide — even a basic payment arrangement stops the notice escalation while you finish comparing, though interest and penalties continue to accrue.

When you don't need any firm at all

You do not need a tax relief company — Community Tax, Clarity, or anyone else — to set up a straightforward IRS payment plan. Be honest with yourself about which case you have:

Handle it yourself when: you agree with the balance, it's one tax year, it's under $50,000 (online setup in under an hour), or you can pay in full within 180 days on a $0-setup short-term plan. The IRS's own pages cover it: payment plans and installment agreements and the Offer in Compromise program. If money for professional help is genuinely tight, the Taxpayer Advocate Service and Low Income Taxpayer Clinics exist for exactly that.

Experienced help tends to change the outcome when: a levy is already in motion, multiple years are unfiled, the debt is business or payroll tax, the balance is over $50,000 and financial disclosure will decide your monthly payment, or — like our example homeowner — a lien and a refinance are about to collide and the sequencing of payoff, subordination, and closing determines whether the loan funds. In those cases, the negotiation isn't filling out a form; it's how your Form 433 numbers get presented and defended.

Community Tax alternative FAQs

Is Community Tax a legitimate company?

Community Tax is an established national tax-resolution firm, and searching for an alternative does not mean it's a scam. Most people comparing alternatives are weighing fit: fee structure, how much direct access they get to the credentialed person on their case, and whether a high-volume model suits a complex situation. Vet any firm you consider — including ours — on written fees, verifiable credentials, and whether anyone promises results before reviewing your finances.

How much should a tax relief company charge?

Fees vary with case complexity, so the structure matters more than the sticker price. Look for a flat, phased fee in writing — typically an investigation phase before a resolution phase — with refund terms spelled out in the engagement letter. Walk away from any firm that quotes a settlement amount, demands the full fee before pulling your IRS transcripts, or prices its work as a percentage of promised savings.

Can I switch tax relief companies in the middle of my case?

Yes — you can revoke a firm's power of attorney and hire new representation at any time. Request your complete case file, check your contract's refund terms for unearned fees, and have the new representative file Form 2848 promptly so IRS notices don't fall into a gap. Timing matters most if a deadline is pending, such as a Collection Due Process hearing or an Offer in Compromise under review.

Does hiring a tax relief company stop IRS collections?

No firm can freeze the IRS, and any company claiming it can stop all collections instantly is misleading you. What representation actually does: a filed Form 2848 puts a professional between you and the IRS, and a pending installment agreement or Offer in Compromise generally pauses levy action while it's under review. Interest and penalties continue to accrue the entire time, under any firm's watch.

Can I resolve a $68,500 tax debt with the IRS myself?

Yes, it's possible — but above $50,000 you can't simply set up a payment plan online; the IRS requires financial disclosure on Form 433-F or 433-A, or paying the balance below the $50,000 threshold first. DIY works best when you agree with the balance, have one tax year involved, and have straightforward finances. Experienced help tends to change outcomes when a lien threatens a refinance, multiple years are unfiled, or offer math is involved.

Will owing the IRS stop my mortgage refinance?

A balance alone often won't, but a filed Notice of Federal Tax Lien attaches to your home and most lenders won't close over it. Your paths are paying the lien off at closing, requesting subordination on Form 14134 so the new mortgage takes priority, or documenting an established payment plan, depending on the lender. Resolving the balance before a lien is filed is dramatically simpler than untangling one after.

Should I hire an enrolled agent, CPA, or tax attorney instead of a national firm?

All three credentials carry unlimited rights to represent you before IRS collections, so for most balance-due cases an enrolled agent or CPA is fully equipped. A tax attorney earns the premium when there's potential fraud exposure, litigation, or complex business liability. Whoever you choose — solo practitioner or national firm — the question is the same: which credentialed person signs Form 2848 and actually works the case.

Your next 24 hours

- Pull your exact balance. Log into your IRS online account (or grab the amount box on your latest notice) so every firm you talk to is quoting against the same verified number.

- Gather your comparison file. The latest IRS notice, your last filed return, a recent pay stub or income statement, your mortgage balance — and any quote or engagement letter you've already been handed.

- Get the free second opinion. Call (888) 825-7779 or use the 2-minute form for a no-pressure case review. Whichever firm you ultimately choose, decide before another month of penalties and interest posts to the balance.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Clarity Tax Relief is a competitor of the firms discussed; company names are referenced for comparison purposes only.