Tax Relief Companies

Anthem Tax Services Alternative: How to Choose Better Help in 2026

The short answer: the best Anthem Tax Services alternative depends on your balance, not the brand — every legitimate firm uses the same IRS programs. Compare firms on four things: a named credentialed representative, flat written fees, a real financial investigation before any settlement talk, and clear refund terms. Or handle simpler steps yourself, free.

You've sat through the sales call — maybe two of them by now — and the quotes don't match, the promises don't quite match, and you're the one who still owes the IRS while you decide. That hesitation is healthy. A tax relief contract is often a four-figure purchase, and comparing before you sign is exactly what a careful buyer does.

Here's the fact that reframes the whole search: no tax relief company has access to any IRS program that another firm — or you — doesn't have. Anthem Tax Services, Clarity, a solo enrolled agent down the street: all of them work with the identical menu of installment agreements, hardship status, penalty relief, and the Offer in Compromise. What you're actually shopping for is execution, honesty, and price. This guide shows you how to compare all three, with the real math for a five-figure balance.

⏱ The clock that actually matters: there's no deadline to pick a firm — but the IRS never pauses while you shop. Interest compounds daily, the failure-to-pay penalty adds 0.5% per month, and any notice you're holding keeps its printed response date whether or not you've signed with anyone.

Why people search for an Anthem Tax Services alternative

Most people comparing Anthem Tax Services alternatives fall into three groups: quote-shoppers, mid-case clients frustrated with pace or communication, and buyers doing due diligence before a large payment. None of those requires believing anything bad about Anthem — it's an established firm, and comparison shopping is simply what you should do before spending thousands of dollars on any service you can't easily evaluate from the outside.

What changes between firms is not the destination but the drive: how accurately your financials get presented to the IRS, how fast filings actually go out, whether a credentialed person or a case coordinator answers your calls, and what the whole thing costs. Those differences are real, and they're measurable if you know what to ask — that's the framework below, and it applies identically whether you're weighing an Alleviate tax relief alternative, a Fortress tax relief alternative, or an Ideal tax alternative.

One 2026-specific reason to compare carefully: the IRS cut roughly 27% of its workforce in 2025. Firms that relied on quick phone resolutions are slower now, because the humans they used to call are gone. The firms doing well in 2026 are the ones filing complete, correct paperwork the first time — because a rejected or incomplete submission can now sit for months before anyone looks at the resubmission.

What the IRS does while you compare companies

The IRS collection sequence advances on autopilot while you compare quotes — no firm can pause it just by being hired. If you're holding notices right now, here's the order the machine escalates in, regardless of who eventually represents you:

- CP14 — the first bill, with roughly 21 days before the sequence advances. This is the cheapest stage to resolve anything.

- CP501 / CP503 — reminder notices. Still just bills, but the balance grows every month the comparison shopping drags on.

- CP504 — intent to levy under IRC §6331(d). The IRS can now take your state tax refund. This is not the final notice, but it's the last quiet one.

- LT11 / Letter 1058 — the final notice of intent to levy. It starts a 30-day clock to request a Collection Due Process hearing on Form 12153. Miss it, and wage and bank levies can proceed.

- Passport certification — once a debt over the $66,000 2026 threshold becomes "seriously delinquent" (a lien filed or levy issued), the IRS can certify it to the State Department, which can deny or revoke your passport. At $83,100, this reader is already over the line — see passport revoked for tax debt for how certification works.

The practical takeaway: compare firms deliberately, but on a calendar measured in days, not months. Every stage you slide down that list removes an option and adds cost.

Comparing firms while the IRS keeps mailing?

Before you sign anyone's contract, get a free second opinion on your case. An experienced tax professional will pull your actual IRS balances, tell you which programs your numbers genuinely fit, and quote a flat fee — so you can compare every firm, including us, against the truth.

The options any firm can use — Anthem or its alternatives

Every tax relief company, from national brands to solo practitioners, resolves debt through the same seven IRS paths. When a sales call names a program, check it against this table — the eligibility rules are set by the IRS, not the firm. (The full do-it-yourself version of this menu lives in our guide to how to settle tax debt yourself.)

| Option | Eligibility at $83,100 | Cost & the catch |

|---|---|---|

| Short-term payment plan | Only if you can pay in full within 180 days | $0 setup; interest and penalties keep accruing until paid |

| Streamlined installment agreement | Not yet — requires the balance at or below $50,000, so a ~$33,100 paydown first | Up to 72 months online, no financial disclosure; accruals continue |

| Non-streamlined installment agreement | Available now with full financials (Form 433-F) | Payment set by your ability to pay under IRS expense standards |

| Partial-pay installment agreement | If financials show you can't full-pay before the 10-year collection statute ends | Pays less than the total; IRS re-reviews your finances periodically |

| Currently Not Collectible | Only with documented hardship — paying would leave you unable to cover basic living costs | Collection pauses; the debt, interest, and refund offsets remain |

| Offer in Compromise | Only if your assets plus future income total less than $83,100 | $205 fee + 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance history for the prior 3 years | Removes penalties, not tax; the new Automatic Exemption from Penalty starts applying automatically in summer 2026 |

Notice what's not on the list: any program that erases tax debt just because you hired a company. If a pitch — from any firm — describes something that doesn't map to one of these seven rows, ask them to name the IRS program. The honest ones can, instantly. Our guides to Currently Not Collectible status and how an offer in compromise works go row-by-row deeper.

Worked example: a 1099 contractor with an $83,100 balance

A hypothetical case shows exactly what any competent firm should tell you before quoting a fee. Say you're a 1099 contractor who owes $83,100 across two years of self-employment tax that snowballed once penalties posted. Here's the real math on each path:

Full-pay plan with financials. At $83,100 you're above the $50,000 streamlined line, so the IRS wants Form 433-F. Suppose the IRS allowable-expense standards leave you $1,350 a month of ability to pay: $83,100 ÷ $1,350 ≈ 62 months before accruing interest and the 0.5% monthly penalty stretch it further. Our guide to an IRS payment plan over $50,000 covers what the financial review looks like.

Paydown to streamlined. If you can raise $33,100 — savings, a vehicle sale, borrowed funds — the remaining $50,000 qualifies for an online agreement at roughly $695 a month over 72 months ($50,000 ÷ 72 = $694.44), with no financial disclosure at all. Sometimes the smartest "resolution" is a wire transfer, and an honest firm will say so even though it shrinks their fee.

Offer in Compromise. The IRS calculates Reasonable Collection Potential: your asset equity plus a multiple of monthly disposable income. Suppose you have $7,500 of equity in your work truck and tools, and the allowable-expense math leaves $500 a month of disposable income. A lump-sum offer uses 12 months of that: $7,500 + ($500 × 12) = $15,500 minimum offer, filed on Form 656 with the $205 fee and a 20% down payment ($3,100) unless you qualify for low-income certification (AGI at or below 250% of the poverty line, which waives the fee, the down payment, and payments during review). You can rough out your own numbers with our Offer in Compromise Calculator before any sales call frames them for you.

The 1099-specific catch every sales call skips: none of these resolutions survives if your current-year quarterlies go unpaid. An installment agreement defaults and a pending offer gets returned the moment you fall behind on this year's estimated taxes. Any firm quoting you a fee without asking about your 2026 quarterly payments hasn't scoped your case — they've scoped your credit card.

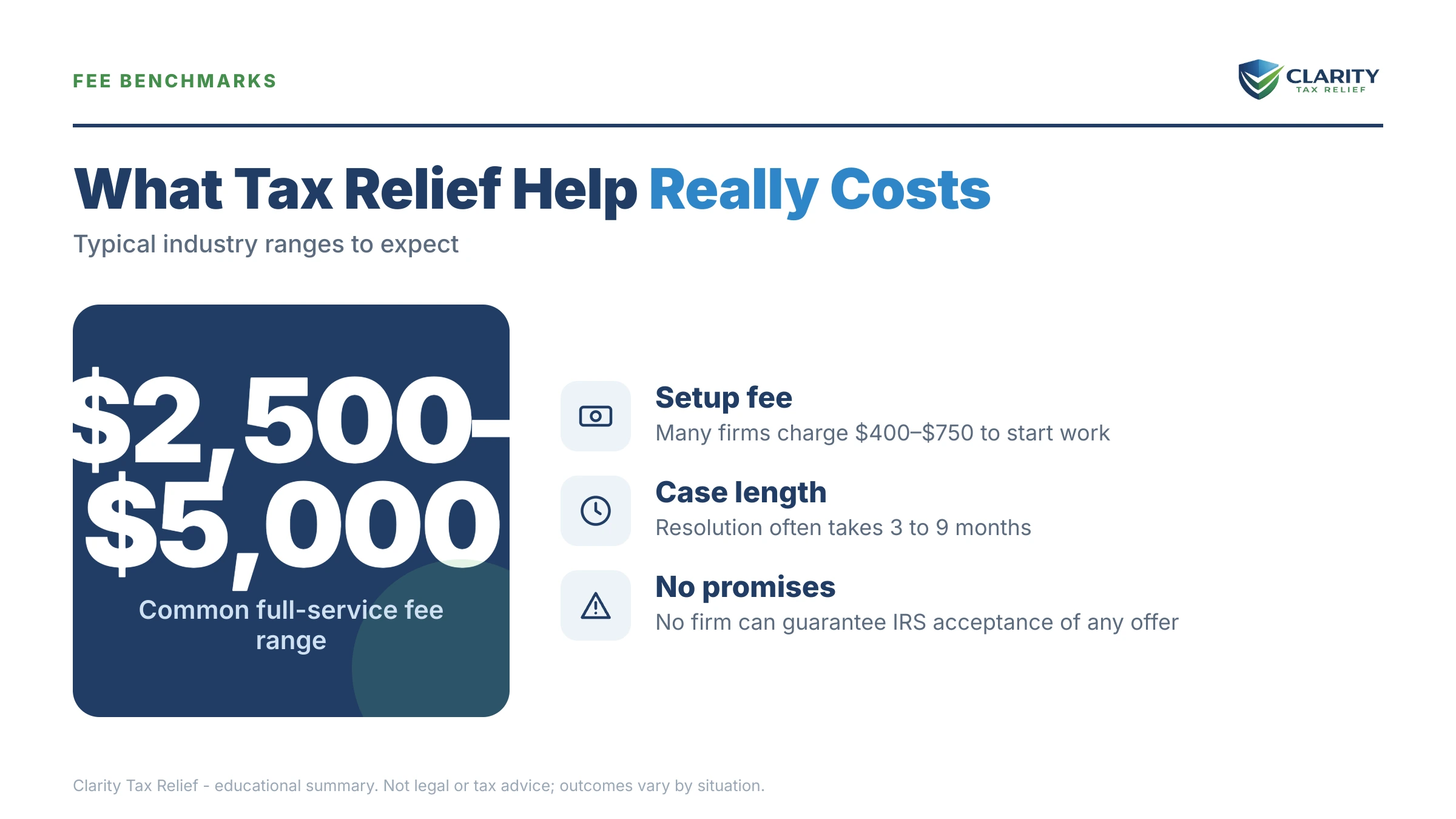

What a fair fee looks like — and the pricing red flags

A fair tax relief fee is flat, scoped in writing, and quoted only after someone has looked at your actual IRS account. In today's market, an installment agreement with financial disclosure commonly runs roughly $2,000–$4,000, while a full Offer in Compromise case commonly runs $5,000–$8,500 or more — with wide variation by firm and complexity. Our breakdown of how much does tax relief cost maps the ranges by resolution type.

The pricing structures to walk away from, at any firm:

- A settlement quoted before your financials are reviewed. Nobody can price an offer without your Reasonable Collection Potential — this is the signature move of an OIC mill.

- Open-ended monthly billing with no defined deliverable. It rewards slow work; you pay more the longer your case drags.

- The full fee due before an investigation phase. Paying thousands before anyone pulls your transcripts means you're buying a plan built on guesses.

- Percentage-of-savings pricing. It incentivizes overstating what you "saved" against penalties the IRS might have removed for free.

The complete buyer's checklist — including contract terms and refund language — is in how to choose a tax relief company and the companion tax relief company red flags list.

IRS deadlines and rights that don't pause during your search

Certain IRS notices carry rights that expire on a printed date — and no firm's onboarding process protects a deadline you've already missed. If any of these is in your mail pile, calendar the date before you sign anything:

| Notice in hand | Response window | What's at stake if it passes |

|---|---|---|

| CP14 (first bill) | Typically 21 days from the notice date | The cheapest resolution stage; the automated sequence advances |

| CP504 (intent to levy) | The date printed on your notice | Your state tax refund becomes seizable; lien filing becomes likely |

| LT11 / Letter 1058 (final notice) | 30 days from the notice date | Your Collection Due Process hearing right (Form 12153); after it, wage and bank levies can proceed |

| CP508C (passport certification) | Applies at $66,000+ seriously delinquent debt | Passport denial or revocation until the debt is being resolved |

| CP523 (payment plan default) | The termination date printed on the notice | Your existing installment agreement — and the levy protection that came with it |

A useful screening question for any firm you interview: read them the notice number you're holding and ask what deadline it carries. A competent shop answers from memory. A sales floor changes the subject to the contract.

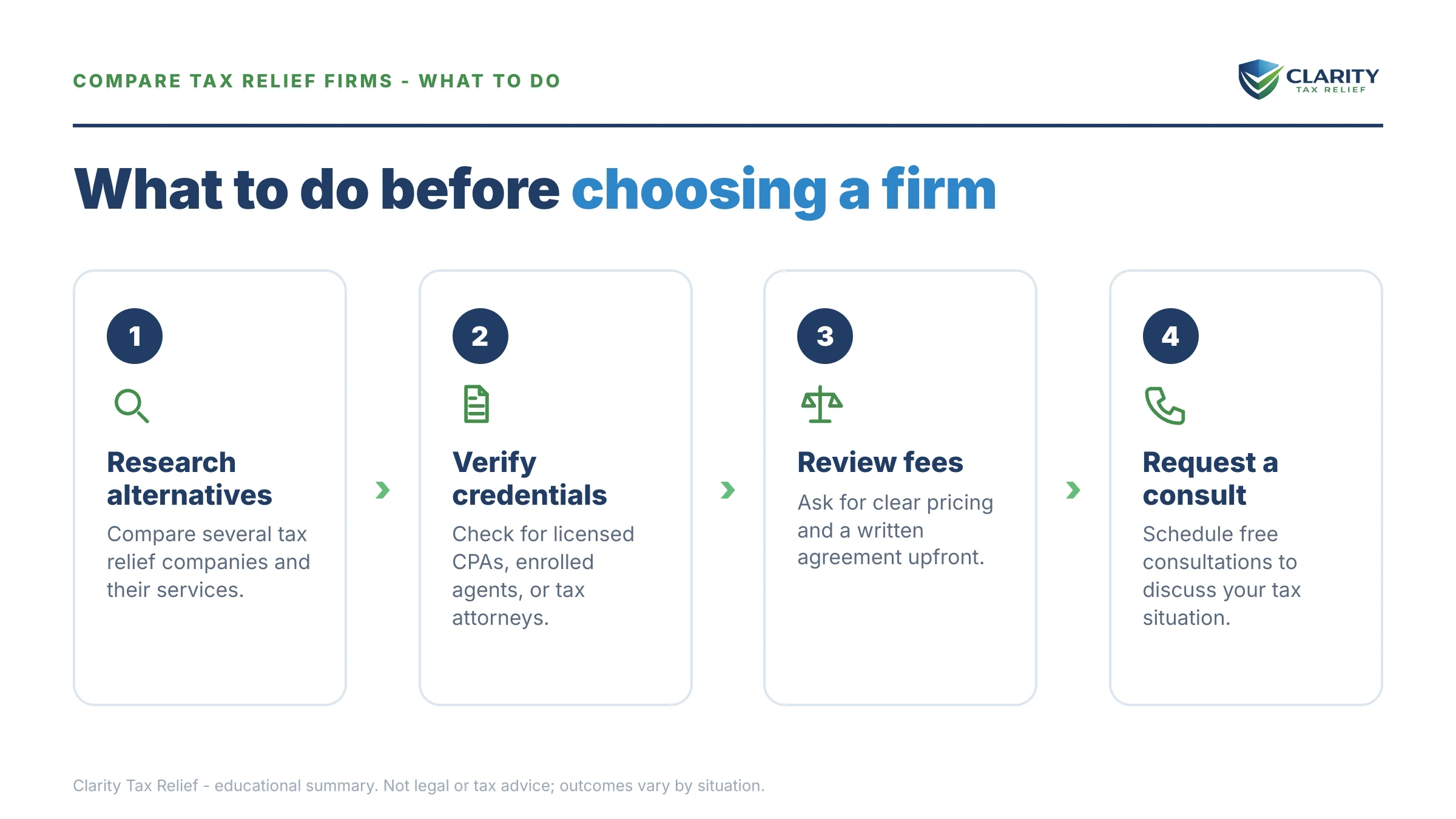

How to choose an Anthem Tax Services alternative, step by step

- Pull your own IRS records first — log into your IRS online account and download account transcripts so no sales call can scare you with numbers you can't verify.

- Get every fee in writing — a flat, scoped, phase-by-phase quote from at least two firms before you sign anything.

- Verify who will actually represent you — ask for the name and credential (EA, CPA, or attorney) that goes on your Form 2848 power of attorney.

- Test the pitch against your math — any firm that promises a settlement before reviewing your full financials is selling, not advising.

- Calendar your deadlines before onboarding — note the response date on any IRS notice you're holding, because those clocks don't pause while a new firm ramps up.

Step three deserves emphasis: Form 2848 is the whole ballgame. The person named on that power of attorney is the only one legally speaking to the IRS for you. At some firms it's the experienced tax professional you met; at others it's someone you'll never talk to. Ask for the name before you pay, not after.

When you don't need any tax relief company at all

An honest comparison of alternatives to Anthem includes the free one: yourself. You genuinely don't need a firm — any firm — when:

- You can pay in full within 180 days. The short-term plan has no setup fee and takes minutes at IRS.gov/payments.

- Your balance is under $50,000 and you agree with it. A streamlined agreement sets up online with no financial disclosure — see the IRS's own payment plans page.

- Your only problem is a penalty and your prior three years are clean. First-time penalty abatement is a phone call or short letter — and starting summer 2026, the new Automatic Exemption from Penalty applies without any request at all.

- You can't afford anything, including a fee. The Taxpayer Advocate Service and Low Income Taxpayer Clinics exist for exactly this, free.

Experienced help changes outcomes in the opposite situations: a balance over $50,000 where the financial presentation on Form 433-F directly sets your payment, a levy already in motion, multiple unfiled years that must be sequenced before any resolution, business or payroll debt, and Offer in Compromise math where a single misvalued asset can sink an otherwise viable offer (the IRS's own Offer in Compromise page shows how strict the criteria run). At $83,100 with self-employment income, you're squarely in the second category — which is why comparing firms carefully, rather than skipping firms entirely, is the right instinct.

Tax relief sales terms, decoded

Every sales call in this industry uses the same vocabulary. Here's what each phrase actually means:

- Investigation phase — pulling your IRS transcripts and financials to see what you truly owe and qualify for; legitimate and necessary, but it should be cheap and produce a written findings summary you keep.

- Resolution phase — the actual filing work (agreement, offer, abatement request); this is where most of the fee should sit, scoped to a named outcome.

- Fresh Start Program — a 2011–2012 set of IRS threshold expansions, not a special program a firm enrolls you in; every option it refers to is on the table above.

- Power of attorney (Form 2848) — the document authorizing a specific credentialed person to represent you; you can revoke it and switch representatives at any time.

- "Pennies on the dollar" — a marketing phrase, not a program. Offers in Compromise are real but means-tested, and the IRS accepted roughly 1 in 5 in FY2024; any firm leading with this phrase is telling you how it sells.

Anthem Tax Services alternative FAQs

Is Anthem Tax Services a legitimate company?

Anthem Tax Services is an established tax relief firm — searching for an alternative doesn't mean it's a scam. Most people comparing alternatives are price-shopping quotes, unhappy with communication pace, or doing due diligence before a large payment. Whatever firm you consider, verify the same three things: a named credentialed representative, a flat written fee, and no settlement talk before anyone has reviewed your finances.

Can a different tax relief company get me a better IRS settlement than Anthem?

No firm can get you a program you don't qualify for — every company works with the same IRS options: payment plans, Currently Not Collectible status, penalty abatement, and the Offer in Compromise. The IRS accepted roughly 1 in 5 offers in FY2024, and acceptance turns on your financial math, not the firm's letterhead. Where firms genuinely differ is accuracy, speed, communication, and price.

How much should a tax relief company charge for an $83,100 case?

Fees vary widely, but a case in this range commonly runs from roughly $2,000–$4,000 for a payment-plan resolution requiring financial disclosure to $5,000–$8,500 or more for a full Offer in Compromise. Insist on a flat, scoped fee in writing before paying anything. Be wary of open-ended monthly billing with no defined end point — that pricing model rewards slow work.

Can I switch tax relief companies in the middle of my case?

Yes. You can revoke a firm's power of attorney (Form 2848) at any time and authorize a new representative, and your IRS case history stays intact — the IRS tracks your account, not your firm. Before switching, request your file, ask exactly what has been filed so far, and check your contract's refund terms for unearned fees.

Does hiring a tax relief company stop IRS collections?

Hiring a firm by itself stops nothing — only specific filings do. A processed installment agreement, an approved Currently Not Collectible determination, a pending Offer in Compromise, or a timely Collection Due Process request (Form 12153 within 30 days of an LT11) each pause enforcement in different ways. If a salesperson tells you collections stop the moment you sign, treat that as a red flag.

Should I hire an enrolled agent, CPA, or tax attorney instead of a big company?

For most back-tax work — payment plans, penalty abatement, offers — an enrolled agent or CPA has identical IRS representation rights to an attorney and often costs less. A tax attorney matters when there's potential fraud exposure, litigation, or a need for attorney-client privilege. Big firm versus boutique matters far less than who is actually named on your Form 2848.

Can I resolve $83,100 in tax debt without hiring anyone?

You can handle parts of it yourself: IRS online payment plans, first-time penalty abatement requests, and transcript pulls are all free DIY steps. At $83,100, though, you're above the $50,000 streamlined threshold, so the IRS will require full financial disclosure — and how those financials are presented directly changes your monthly payment or offer amount. That's where experienced help most often pays for itself.

Your next 24 hours

- Pull your real numbers. Log into your IRS online account and note the exact balance for each tax year — this is the figure every quote should be built on, not the one from a sales script.

- Gather three things: your last filed return, every IRS notice you've received (check each one for a printed response date), and three months of income records — 1099s, bank deposits, invoices.

- Get a free comparison point. Call (888) 825-7779 or use the 2-minute form for a free case review — an experienced tax professional will tell you which programs your numbers actually fit and quote a flat fee, so every firm you're considering gets measured against the same truth. Interest and penalties accrue monthly while you decide, so decide on a short calendar.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Clarity Tax Relief is not affiliated with Anthem Tax Services, and nothing here is a statement about any specific firm's practices.