Consumer Protection

Tax Relief Company Red Flags: 12 Warning Signs to Spot Before You Pay (2026)

The short answer: the biggest tax relief company red flags are a guaranteed settlement quoted before anyone reviews your IRS transcripts, a large upfront fee, "pre-qualified for Fresh Start" cold calls, no named enrolled agent, CPA, or attorney on your case, and pressure to sign today. Any one of these should stop you before you pay.

You're a sole proprietor with $61,200 in back self-employment tax, and the voicemail says you've been "pre-approved to settle for a fraction of what you owe — but the program closes Friday." That call landed at exactly the moment you're most likely to say yes. That's the design. The good news: telling a legitimate firm from a boiler room takes about an hour of checking, and every check is on this page.

Here's why the calls found you: federal tax liens are public record, and lead-generation shops mine them the day they're filed. And with the IRS workforce cut roughly 27% in 2025 — humans harder to reach, automated notices still firing — scared taxpayers are an easier sell in 2026 than they've been in a decade.

⏱ The real clock: there's no deadline printed on a sales pitch — but your balance grows every month it sits. The failure-to-pay penalty adds 0.5% per month, interest compounds on top, and the IRS's automated notice sequence keeps escalating while a bad firm "investigates." Months lost to a stall are the most expensive part of hiring wrong.

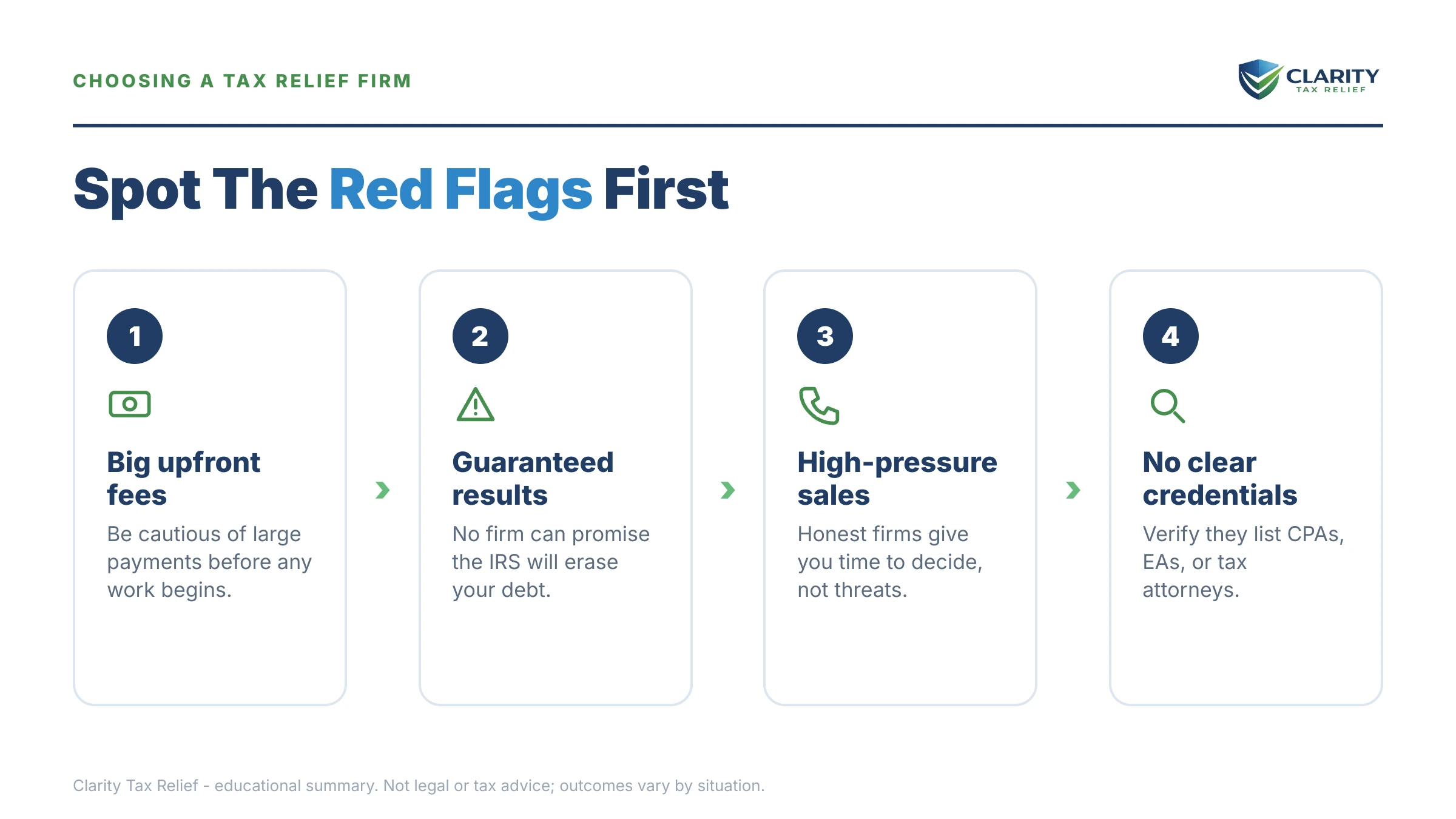

The 12 tax relief company red flags to watch for in 2026

A settlement quoted before anyone has seen your IRS transcripts is the single most reliable sign of a tax relief scam. Everything on this list flows from that same trick: promising an outcome before doing the math that determines it.

- A settlement number on the first call. Nobody can know what the IRS will accept without your transcripts, income, assets, and allowable expenses. A firm quoting "$4,000" before pulling a single record is quoting fiction — the number exists to get your card, not to describe your case.

- "Pennies on the dollar" promises. This slogan survives because settlements occasionally do happen when collection potential is genuinely low — but the IRS accepted roughly 1 in 5 offers in FY2024. Presenting a minority outcome as a sure thing is the core of the scam, and it's the exact claim that has drawn FTC enforcement against tax relief firms.

- "You're pre-qualified for the Fresh Start program." Fresh Start was a set of IRS policy changes, not a program with an enrollment window — so nobody can pre-qualify you for it. See is the IRS Fresh Start program real for what the term actually covers.

- Thousands upfront before any investigation. The legitimate sequence is: file a power of attorney, pull your transcripts, review your finances, then quote resolution work. Firms collecting $3,000–$8,000 before knowing what you owe are selling before diagnosing. Baseline the numbers with how much does tax relief cost.

- Percentage-of-savings or open-ended pricing. A fee tied to "what we save you" invites inflated claims, and unpriced "phase two" billing means the quote you signed isn't the price you'll pay. Insist on one written number — the tradeoffs are covered in tax relief flat fee vs. hourly pricing.

- Manufactured urgency. "Sign today or the IRS moves on your accounts this week." Real deadlines exist — an LT11 final notice starts an actual 30-day clock — but they're printed on IRS notices, not invented by salespeople. A firm that fabricates deadlines to close you will fabricate progress reports to keep you.

- Implied government affiliation. Mailers styled to look like IRS notices, "Federal Fresh Start Hotline" branding, callers claiming to be "assigned to your case." No private company is affiliated with the IRS, and real IRS contact begins with postal mail from the IRS itself.

- They called you first. Lien filings are public; boiler rooms buy the lists and dial the same day. A cold call telling you you've been "flagged" is describing their lead sheet, not your IRS file. Legitimate firms answer inquiries — they don't hunt strangers.

- Everyone gets an Offer in Compromise. If the recommendation is an OIC before anyone has run your numbers, you've reached a mill — a firm that files doomed offers for a fee. The IRS has warned about these operations on its Dirty Dozen scams list; the full anatomy is in OIC mills: how the scam works.

- No named EA, CPA, or attorney. Only those three credentials can represent you before the IRS in collections. Ask who will sign your Form 2848. If the answer is "our team of experts" or a "senior tax analyst" who can't appear on that form, you're talking to sales. When a lawyer specifically matters is covered in tax relief attorney vs company.

- They tell you to ignore the IRS. "Don't open the mail — we handle everything." A real representative does take over IRS contact after filing Form 2848, but you should still see every notice and know every deadline. Firms that cut you off from your own case are usually hiding that nothing is happening.

- No verifiable footprint. A months-old LLC, no physical address, a name that changed after complaints piled up, glowing reviews only on its own site. Search the company name plus "complaints," and check your state attorney general's actions before you check anything else.

What happens if you hire the wrong tax relief firm

The most expensive part of hiring the wrong firm isn't the fee — it's the IRS rights and deadlines that expire while the firm stalls. The pattern repeats so consistently it can be written as a sequence:

- You pay the upfront fee. Often thousands, often financed, charged before anyone has pulled your IRS record.

- The "investigation phase" begins — and stretches. Weeks of silence become months. Calls go to voicemail; status updates say "in review."

- The IRS keeps moving. Its collection sequence is automated and never paused for your contract. A CP504 arrives, then an LT11 final notice — which starts a real 30-day window to request a Collection Due Process hearing. If the firm lets that window lapse, you lose your strongest pre-levy appeal right.

- Enforcement lands while you're "represented." A bank levy freezes funds for a 21-day hold before they're gone; a wage levy runs continuously until released. The firm now quotes an additional fee to "handle the emergency" it allowed.

- The firm ghosts, rebrands, or demands more. You're out the fee, months of time, and your best options. If you're already at this stage, start with "a tax relief company took my money" — there is a recovery path, and your IRS case can be restarted.

Holding a quote you're not sure about?

Read us their pitch — the promised settlement, the fee, the "deadline." An experienced tax professional will run the same eligibility math the IRS runs on your actual numbers and tell you plainly whether the offer is real, free and without pressure. We're a tax relief company too — hold us to every test on this page.

What legitimate tax relief actually looks like: options, eligibility, and real costs

Every legitimate tax relief outcome comes from one of a handful of IRS programs, and each has a means test the sales pitch skips. There is no secret program, no insider channel — a good firm's value is doing this math correctly and executing fast, not accessing anything you can't. (The full DIY map lives in our guide to how to settle tax debt yourself.)

| The pitch you'll hear | The actual IRS program | Who genuinely may qualify |

|---|---|---|

| "Settle for a tiny fraction" | Offer in Compromise (Form 656) | Only taxpayers whose assets plus future income fall short of the balance; the IRS accepted roughly 1 in 5 offers in FY2024 |

| "Enroll in Fresh Start before it closes" | Ordinary payment plans | Anyone can request one: up to 180 days short-term, or up to 72 months online for balances of $50,000 or less |

| "We'll wipe your penalties" | First-Time Abate / reasonable cause (plus AEP starting summer 2026) | Clean compliance the prior 3 years, or a documented cause beyond your control — AEP will apply automatically, no firm required |

| "We'll stop IRS collections" | Currently Not Collectible status | Only when allowable-expense math shows paying would cause hardship; the debt and interest remain |

| "One-time forgiveness — this week only" | No such standalone program exists | Nobody — it's a marketing label pasted over the options above; see "IRS one-time forgiveness," debunked |

| Option | IRS fees | Typical professional fee | Typical timeline |

|---|---|---|---|

| Short-term plan (up to 180 days) | $0 setup | Usually none needed — DIY online | Same day |

| Long-term installment agreement | Setup fee varies; lowest with direct debit, waivable for low income | Typically a few hundred to ~$1,500 | Days to a few weeks |

| Offer in Compromise | $205 application fee + 20% down on lump-sum offers (both waived with low-income certification) | Typically $2,500–$7,500 | Commonly 6–12+ months; auto-accepted if the IRS doesn't decide within 2 years |

| Currently Not Collectible | $0 | Often $1,000–$3,000 | Weeks to a few months |

| Penalty abatement | $0 | Often a few hundred to ~$1,500 — and AEP makes qualifying relief automatic starting summer 2026 | Weeks to months |

A worked example: $61,200 and the "settle it for $4,000" pitch

Say you're a self-employed sole proprietor who owes $61,200 across two years, and a cold-caller promises to settle it for about $4,000. The IRS decides offers using Reasonable Collection Potential — your net asset equity plus a multiple of your monthly disposable income. Run the hypothetical numbers:

- Assets: equity in your work truck and tools of $9,500, plus $2,100 in the bank = $11,600.

- Future income: $6,400/month in net self-employment income minus $5,700 in IRS allowable living expenses = $700/month disposable. For a lump-sum offer that's multiplied by 12: $8,400.

- RCP: $11,600 + $8,400 = $20,000 — the realistic floor for an acceptable offer. Five times the pitch, and still a genuine saving against $61,200. You can rough out your own number with our Offer in Compromise Calculator — it estimates, it doesn't promise.

Now flip one variable. If your disposable income is $1,500/month instead of $700, future income alone becomes $18,000, RCP climbs to $29,600, and if the IRS's math shows it can collect the full $61,200 within the collection statute, the offer fails entirely — after you've paid the mill's fee. The honest answer then is a payment plan. At $61,200 you're above the $50,000 online threshold, so you'd either submit financials on a Form 433 series statement or pay the balance down: pay $11,300 to reach $49,900, and a 72-month online agreement runs roughly $695/month ($49,900 ÷ 72) while interest continues to accrue. Real acceptance data is in our offer in compromise acceptance rate breakdown — any firm quoting you an outcome should be able to walk you through this exact arithmetic on your numbers.

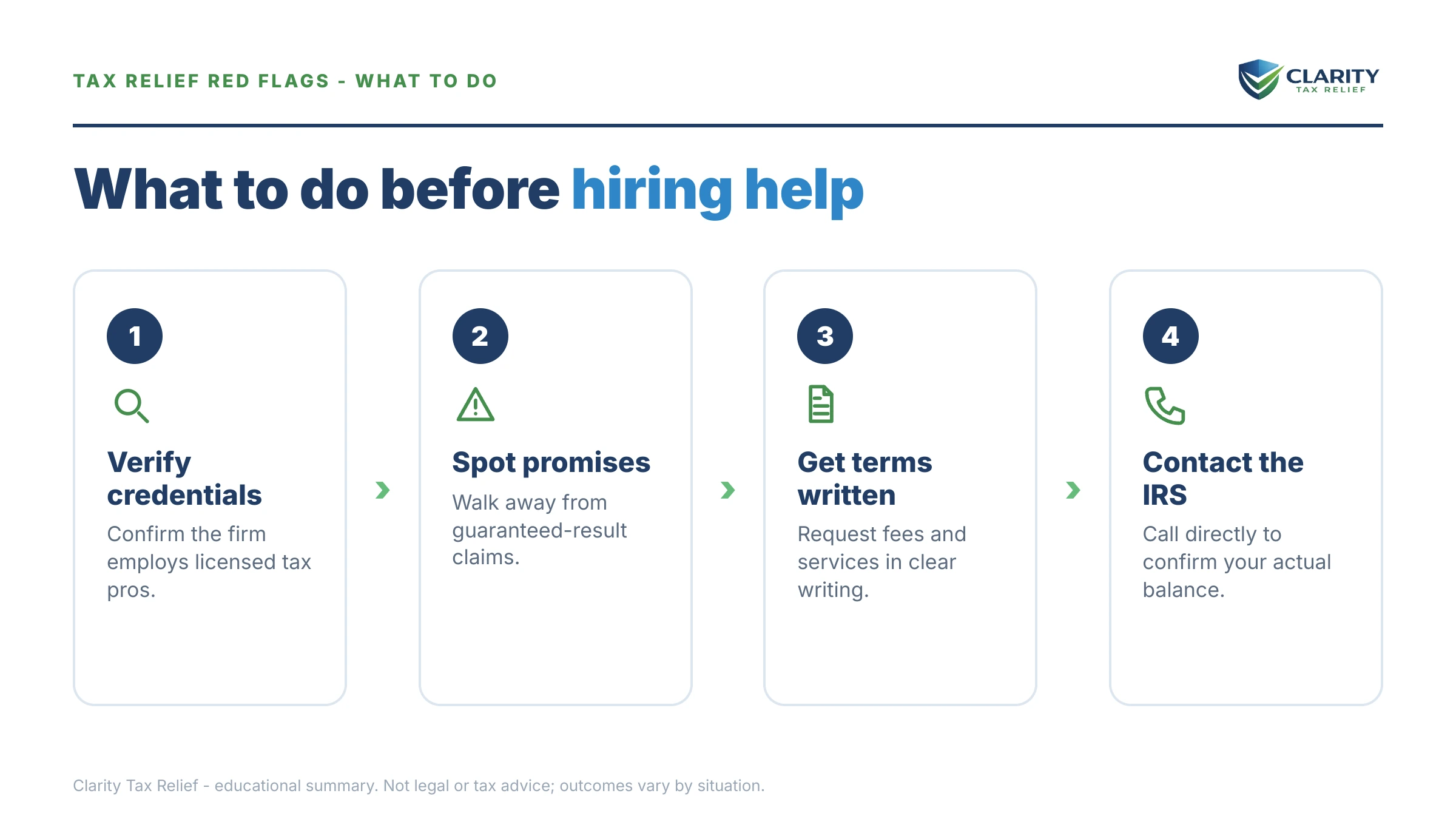

How to vet a tax relief company, step by step

Vetting a tax relief company takes about an hour and protects both your money and your IRS deadlines. Work through it before any signature:

- Pull your own IRS records first. Set up your IRS online account and check your real balance, tax years, and notice status before anyone pitches you — you can't evaluate a promise without knowing your own numbers.

- Verify the credential by name. Ask for the specific enrolled agent, CPA, or attorney who will sign your Form 2848, then confirm the credential independently through the state bar, state board of accountancy, or the IRS enrolled agent verification process.

- Get the full fee in writing. Demand one flat, all-inclusive figure tied to defined work before you sign anything — and walk if the answer involves percentages of savings or unpriced future phases.

- Make them show the math. A legitimate firm reviews your income, equity, and allowable expenses before naming a program or an outcome; anyone quoting results first is guessing at your expense.

- Sleep on it and compare. A real firm's quote will still stand tomorrow. Get a second opinion from at least one other firm — pressure to sign on the first call is itself a red flag.

For the full interview script, use our questions to ask a tax relief company checklist, and the broader buyer's guide at how to choose a tax relief company.

When you can handle this yourself — and when help genuinely matters

If you owe $50,000 or less and agree with the balance, you can usually set up an IRS payment plan online yourself in under an hour — no company required. The same is true for a short-term 180-day plan (no setup fee), a single first notice you agree with, and first-time penalty relief — which becomes automatic for qualifying penalties when AEP launches in summer 2026. Any firm charging you meaningfully for those is charging for a form you could file. Start with the IRS payment plans page, and screen an offer yourself with the IRS's own Offer in Compromise pre-qualifier.

Experienced help changes outcomes in a narrower set of situations: a levy already in motion, multiple unfiled years that must be sequenced before any resolution, business or payroll tax debt where personal liability is on the table, an assigned revenue officer, or OIC math built on fluctuating self-employment income — where how income and equipment equity are presented can swing the result by five figures. If you can't afford professional help at all, you may have options through a Low Income Taxpayer Clinic or the Taxpayer Advocate Service — legitimate firms will tell you that, too.

Sales-pitch terms, decoded

These are the six terms every pitch leans on — here's what each actually means:

- Fresh Start: a 2011–2012 set of IRS policy changes that expanded payment plans and offer terms — not a program you enroll in, and it has no deadline.

- Offer in Compromise (Form 656): a means-tested settlement the IRS accepts only when its math shows it can't collect the full balance.

- Reasonable Collection Potential (RCP): the IRS formula — net asset equity plus a multiple of monthly disposable income — that sets the minimum acceptable offer.

- Form 2848: the power-of-attorney form naming your actual representative; whoever signs it is your case, everyone else is sales. Walkthrough: Form 2848 instructions.

- Enrolled agent (EA): a federally credentialed tax practitioner with unlimited rights to represent taxpayers before the IRS.

- "Investigation phase": industry shorthand for pulling your IRS transcripts — legitimate work that should take weeks, not months, and should end in written findings you get to see.

Tax relief red flag questions, answered

How do I know if a tax relief company is legitimate?

Check three things before you pay: a named enrolled agent, CPA, or attorney who will personally represent you; a written flat fee covering the full resolution; and a review of your IRS transcripts before anyone quotes an outcome. A legitimate firm files Form 2848, looks at your actual IRS record first, and will tell you when you don't need its help at all.

Is settling tax debt for pennies on the dollar real?

Occasionally — but only when the IRS's own math supports it. An Offer in Compromise is accepted when your assets plus future income genuinely cannot cover the balance, and the IRS accepted roughly 1 in 5 offers in FY2024. Any company quoting a settlement percentage before analyzing your equity and income is selling a slogan, not a result.

How much should a tax relief company charge?

Market rates typically run from a few hundred dollars for a simple payment-plan setup to roughly $2,500–$7,500 for an Offer in Compromise, with complex business or multi-year cases costing more. The structure matters more than the number: a written flat fee tied to defined work. Percentage-of-savings pricing, open-ended billing, and surprise 'phase two' charges are all red flags.

What is an offer in compromise mill?

An OIC mill pushes nearly every caller toward an Offer in Compromise regardless of eligibility, collects a large fee, and files offers the IRS predictably rejects. The IRS has repeatedly warned about these mills on its annual Dirty Dozen scams list. Because eligibility is a math test — assets plus future income versus the balance — an honest firm can tell you after one financial review whether an offer is even plausible.

Can a tax relief company stop IRS collections immediately?

No firm can stop all collections instantly, and any that promises to should be avoided. What a representative can do quickly is file Form 2848, get on record with the IRS, and request collection holds while a resolution is negotiated; a levy causing verifiable hardship can sometimes be released within days. Interest and penalties keep accruing under every program until the balance is resolved.

What credentials should a tax relief representative have?

Only three credentials allow someone to represent you before the IRS in a collection case: enrolled agent, CPA, or attorney. Ask for the name and credential of the specific person who will be listed on your Form 2848 — not the company's 'team of experts.' If the person you're talking to is a 'consultant' or 'senior tax analyst' who can't appear on that form, you're talking to a salesperson.

What can I do if I already paid a tax relief company that did nothing?

Demand a written case status and an itemized accounting of work performed, then request a refund in writing. If that fails, dispute the charge with your card issuer and file complaints with your state attorney general and the FTC. Restart your IRS case immediately — the IRS never paused while the firm stalled, so check your notices and deadlines first.

Is the IRS Fresh Start program real?

Fresh Start was a real set of IRS policy changes from around 2011–2012 that expanded payment-plan thresholds and Offer in Compromise terms — but it is not an application, a hotline, or an enrollment window. There is nothing to 'enroll in' and no deadline to beat. Companies claiming the program is 'closing soon' are wrapping ordinary IRS options in fake urgency.

Your next 24 hours

- Find the fee and the name. Pull out any contract or quote you've been given and locate two things: the total all-in fee in writing, and the named enrolled agent, CPA, or attorney who will represent you. If either is missing, you have your answer.

- Gather your real picture. Your last filed return, every IRS notice you've received, and a rough list of monthly income and expenses — that's everything an honest eligibility review needs, and everything a dishonest one skips.

- Get a free second opinion. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will run the IRS's own eligibility math on your numbers and tell you plainly if you can handle it yourself. Penalties and interest accrue monthly whichever way you go, so the one wrong move is letting it sit.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.