Hiring Help

Questions to Ask a Tax Relief Company Before You Hire One (2026)

The short answer: before hiring a tax relief company, ask: who will work your case and their credential (EA, CPA, or attorney); the total fee in writing; which IRS program they recommend and why your numbers fit; when they'll file Form 2848; and the refund policy. A firm promising outcomes before reviewing your finances is guessing.

The sales call went well — maybe too well. The rep was warm, the quote landed somewhere around $5,000, and the pitch ended with "we can probably get this reduced." Now the engagement agreement is sitting in your inbox and you're not sure what you'd actually be buying.

That hesitation is your best asset. The right questions to ask a tax relief company will tell you more in ten minutes than a hundred five-star reviews — because the honest firms answer them easily, and the sales floors can't.

⏱ The real clock: there's no letter deadline for choosing help, but your balance doesn't wait. The failure-to-pay penalty adds 0.5% per month, plus daily-compounding interest, while you compare firms — and IRS notices keep escalating on their own schedule. Take days to vet a company, not weeks, and never let an open-ended "investigation phase" drift for months.

Why the questions matter more than the reviews

"Tax relief" is a marketing category, not a credential — anyone can sell it, but only enrolled agents, CPAs, and attorneys can actually represent you before the IRS. That gap between who sells and who works is where almost every horror story in this industry starts.

The stakes are real: the FTC has permanently banned tax-relief operators for charging thousands on the promise of settlements they never delivered. Reviews can be bought, buried, or filtered. A pointed question on a live call cannot.

This article gives you the exact questions and the answers you should hear. For the broader selection framework — comparing firms once they've passed the interview — see our full guide on how to choose a tax relief company.

What happens if you hire the wrong tax relief firm

The most expensive mistake in tax relief isn't the fee — it's the months of IRS escalation that pass while a bad firm does nothing. The failure pattern is remarkably consistent, and it runs in this order:

- You pay a large upfront fee based on a phone quote from someone who never saw your transcripts or your budget.

- The "investigation phase" begins — the firm may file a power of attorney and pull transcripts, then goes quiet for weeks or months.

- IRS notices keep arriving, because hiring a firm does not pause collections. Signing an engagement letter changes nothing at the IRS; only an actual resolution — a payment plan, hardship status, or a pending offer — changes your collection status.

- A second, larger fee request appears — the "resolution phase" costs more than anyone mentioned on the sales call, and you're already invested.

- The case closes with a standard payment plan you could have set up online yourself — or the firm stops returning calls entirely, and your balance is now bigger than when you started.

If you're reading this because stage five already happened, go straight to our guide for when a tax relief company took my money — there are concrete recovery steps, and you can hire a new representative at any time.

Holding someone else's quote right now?

Get a free second opinion before you sign anything — including with us. Tell an experienced tax professional what you were quoted and what program was pitched, and we'll tell you whether it actually fits your numbers — or whether you don't need to hire anyone at all. Penalties and interest accrue monthly while you decide, so get clarity this week.

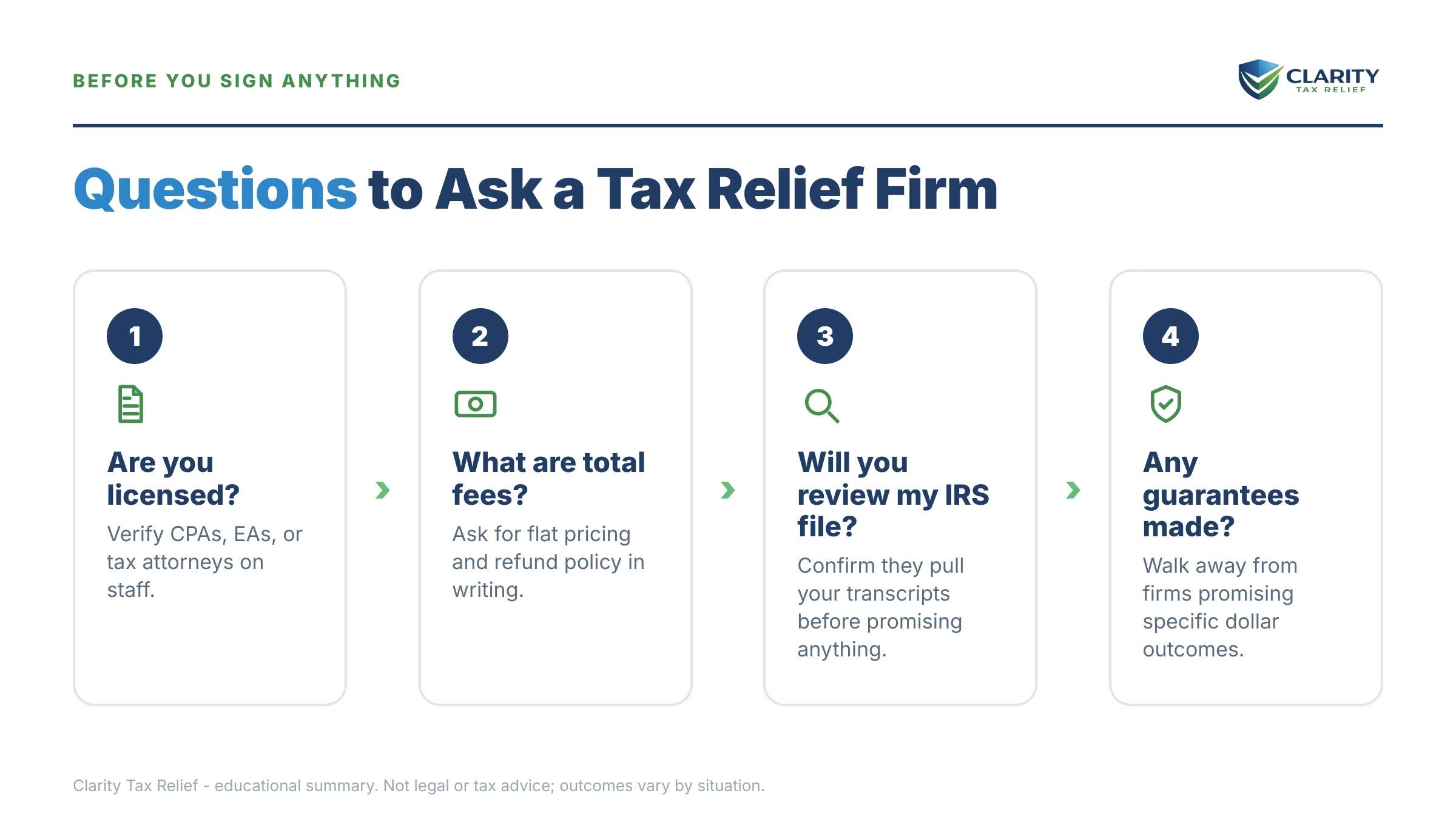

The 12 questions to ask a tax relief company — and the answers you should hear

Twelve questions separate a real tax resolution practice from a sales floor. Ask them in order; most bad firms disqualify themselves by question five.

Who actually does the work (questions 1–3)

1. "Who will work my case, by name — and what credential do they hold?" The person on the sales call is almost always a commissioned rep, not a practitioner. You want a specific name and a specific credential — enrolled agent, CPA, or attorney — that you can verify independently. "Our team of tax experts" is not an answer; it's an evasion.

2. "When will you file Form 2848, and whose name goes on it?" Form 2848 is the power of attorney that lets a practitioner speak to the IRS for you. Until it's filed, nobody is representing you — no matter what you've paid. A good answer: a named practitioner, filed within the first week.

3. "How long have you operated under this name?" Rebranding after a wave of complaints is a known move in this industry. Ask directly whether the company has done business under other names, then verify with your state attorney general's complaint database.

The money (questions 4–6)

4. "What is the total fee, in writing, and exactly what does it cover?" Honest firms quote a flat fee tied to a defined scope: which years, which returns, which resolution. Vague "phases" with open-ended pricing are how a $1,500 engagement becomes $8,000. Our comparison of tax relief flat fee and hourly pricing shows which model fits which case.

5. "Is the investigation fee separate from the resolution fee?" The classic trap is a modest upfront "investigation" charge, followed by a much larger resolution quote once you're emotionally and financially invested. A trustworthy firm tells you both numbers — or the realistic range for phase two — before you pay for phase one.

6. "Where is the refund policy in the contract — not on the phone?" Verbal assurances evaporate. If the written agreement doesn't say what you get back when the firm can't deliver what it described, assume the answer is nothing.

The promised outcome (questions 7–9)

7. "Which specific IRS program are you recommending, and why do my numbers fit it?" Every legitimate outcome has a name: installment agreement, Offer in Compromise, Currently Not Collectible, penalty abatement. A real practitioner names the program and ties it to your income, assets, and expenses. "We'll get you into the Fresh Start program" names nothing — Fresh Start is a label for standard IRS policies anyone can use.

8. "What did you review before quoting that outcome?" The only honest basis for predicting a result is your IRS transcripts plus a financial analysis — the same data the IRS itself will use. Nobody can responsibly forecast a settlement from a 20-minute phone call. If they haven't seen your numbers, they're quoting a script.

9. "What's my realistic Offer in Compromise picture — show me the math." The "pennies on the dollar" pitch is the oldest scam in this industry: the IRS accepted roughly 1 in 5 offers in FY2024, and acceptance turns entirely on a formula called Reasonable Collection Potential — your asset equity plus a multiple of your monthly disposable income. You can sanity-check any settlement pitch yourself in minutes with our Offer in Compromise Calculator, which estimates what an offer might look like for your finances. A firm that quotes a settlement without RCP math is running an offer in compromise mill play.

The working relationship (questions 10–12)

10. "Who is my point of contact, and how often will I hear from you?" You want a named case manager and a stated update cadence. "We'll call you when there's news" translates to silence.

11. "What deadlines are live on my account right now?" A real practice checks for active notices, levy clocks, and response windows before quoting anything — because a levy in motion changes the entire strategy. A firm that quotes first and checks later is selling, not diagnosing.

12. "What happens if the IRS contacts me directly while you're working?" With a Form 2848 on file, your representative receives copies of your notices and handles the contact. The correct answer includes "forward us anything you receive immediately." The wrong answer — and it happens — is "just ignore IRS mail; we've got it."

Pressure-test the promise: what each IRS program really requires

Every outcome a tax relief company can deliver is a standard IRS program with published eligibility rules — which means every promise can be checked. Use this table against whatever was pitched to you:

| IRS program | Who typically qualifies | If a firm promises it, ask… |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days; $0 setup fee | "Why would I pay you for something free that takes minutes online?" |

| Streamlined installment agreement | Balance of $50,000 or less with returns filed; up to 72 months, set up online | "What financial analysis produced my monthly payment number?" |

| Guaranteed installment agreement | Balance of $10,000 or less with a clean recent compliance history | "If I qualify automatically, what exactly is your fee for?" |

| Offer in Compromise | Assets plus future income (RCP) genuinely below the debt; $205 fee and 20% down on lump-sum offers (both waived with low-income certification) | "Show me the RCP math that says my offer beats what the IRS could collect." |

| Currently Not Collectible | Paying anything would leave you unable to cover IRS-allowed basic living expenses | "Which allowable-expense standards did you apply to my budget?" |

| Penalty abatement | First-time relief needs a clean prior three years; reasonable cause needs a documented event like illness or disaster | "Which penalties, which years, and under which relief rule?" |

One 2026-specific note on that last row: starting in summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies many first-time penalty removals automatically, with no request needed. A firm charging you to "fight for" a penalty the IRS is about to remove on its own is charging you for weather. Details in our first time penalty abatement guide.

What tax relief should cost in 2026

Every program a firm can deliver has a published IRS price — and it's a fraction of any professional fee, which is exactly why question 4 matters. The fee ranges below are commonly quoted market figures, not our pricing or anyone's promise; get your own quote in writing.

| Resolution | IRS's own cost | Commonly quoted firm fee | Typical timeline |

|---|---|---|---|

| Short-term plan (180 days) | $0 setup | $0 — you rarely need help | Same day, online |

| Installment agreement | Small online setup fee; lower with direct debit, waived or reimbursed for low-income taxpayers | ~$1,000–$2,500 | Days to a few weeks |

| Offer in Compromise | $205 application fee + 20% down on lump-sum offers (both waived with low-income certification) | ~$3,500–$7,500+ | Often many months; if the IRS doesn't decide within 2 years, the offer is accepted by law, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count |

| Currently Not Collectible | $0 | ~$1,500–$3,000 | Typically weeks to a couple of months |

| Penalty abatement | $0 | ~$500–$2,500 | Sometimes a single phone call; written requests take longer |

Two things to notice. First, interest and penalties keep accruing under every option until the balance is resolved — no firm can switch that off. Second, the fee is defensible only when the work is genuinely complex; for the full breakdown of what drives pricing up or down, see how much does tax relief cost.

Say you owe $13,600: pressure-testing a $5,500 quote

A hypothetical makes the questions concrete. Say you and your spouse filed jointly, under-withheld, and now owe $13,600, including about $1,150 in penalties. A tax relief salesperson quotes $5,500 and hints the debt "could be settled."

Run the settlement math first. Suppose you have $45,000 of home equity and, after IRS allowable living expenses, about $500 a month left over. A lump-sum offer is measured against roughly your equity plus 12 months of that surplus:

$45,000 + ($500 × 12) = $51,000 of collection potential — against a $13,600 debt.

The IRS formula says you can pay in full, so an Offer in Compromise is dead on arrival. Any firm pitching settlement to this couple either never looked or didn't care.

Now the realistic path. At $13,600, you're under the $50,000 online threshold: a streamlined plan over the maximum 72 months starts around $13,600 ÷ 72 ≈ $189 a month, though paying $450 a month clears the base balance in about 31 months and sharply cuts the interest and 0.5% monthly late-payment penalty that keep accruing. And if your prior three years are clean, first-time abatement (or the new AEP) may remove that $1,150 in penalties for free.

Bottom line: the $5,500 fee would buy this couple a payment plan they could set up online in twenty minutes, plus a penalty request that costs nothing. That's the entire reason questions 7 and 8 exist. If instead this couple had a bank levy in motion, three unfiled years, or a payroll tax problem, a fee in that range could genuinely earn its keep — the point is that the numbers, not the pitch, decide.

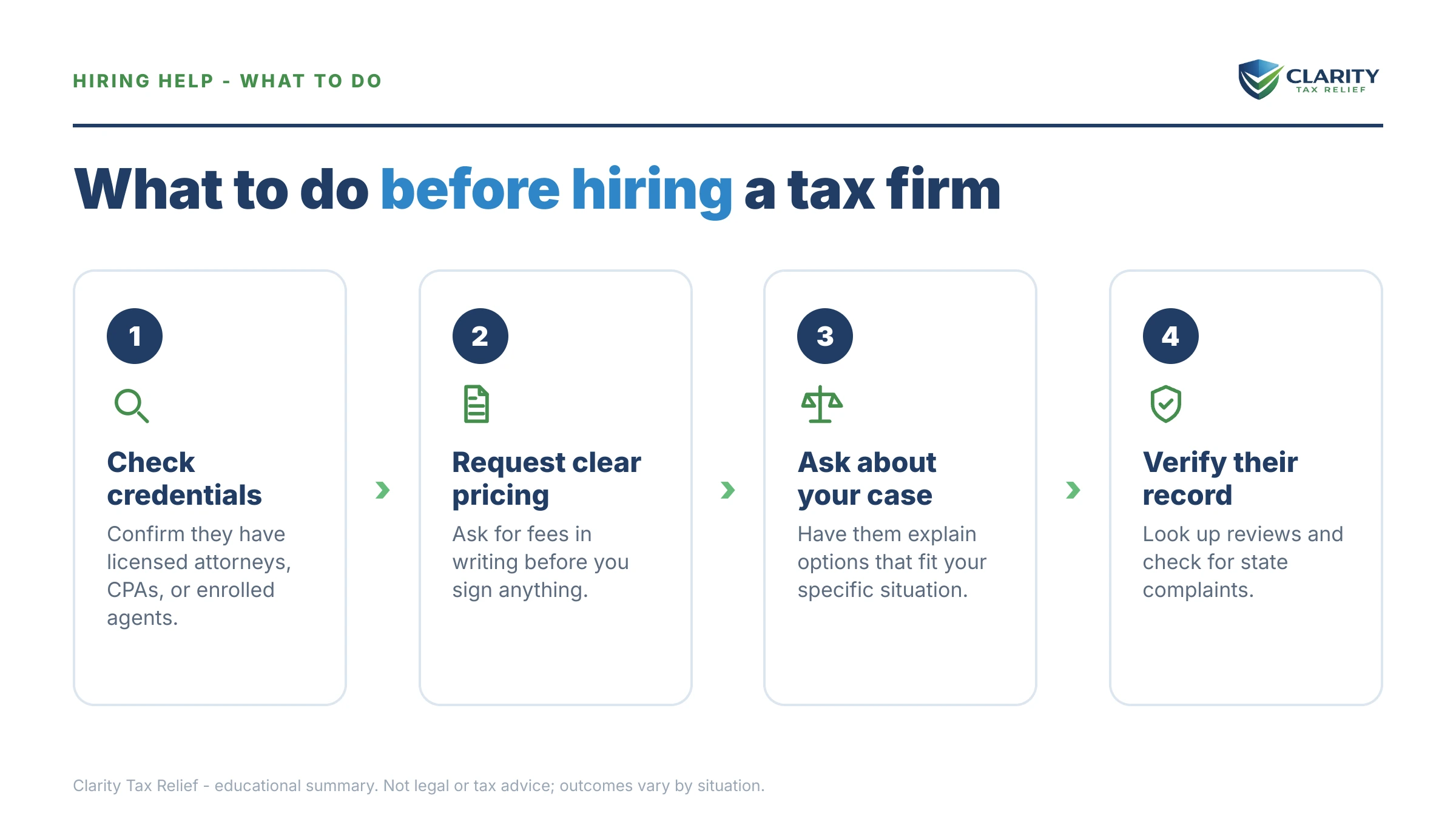

How to vet a tax relief company, step by step

- Verify the credential. Look up the named EA, CPA, or attorney who would sign your Form 2848 — through the IRS enrolled agent directory, your state bar, or the state board of accountancy — before the sales call ends.

- Get the total fee and scope in writing. The written quote should name the full fee, every phase it covers, what triggers additional charges, and the refund policy.

- Compare the quote against the IRS's own price. Check what the recommended program costs directly from the IRS — a $0 short-term plan or a $205 offer application — so you know exactly what the fee is buying.

- Check the complaint record. Search the company's name plus "complaint" and "refund," and check your state attorney general's office, before you read a single review.

- Get a second opinion before signing. Any reputable firm will review your transcripts and put its quote in writing; if two firms recommend different programs, make each one explain why.

Wondering what a legitimate first call looks like from the inside? Our walkthrough of a tax relief consultation, what to expect shows the difference between a diagnosis and a pitch.

When you can handle this yourself — and when help earns its fee

The IRS lets most taxpayers set up a payment plan online with no professional involved — a balance of $50,000 or less qualifies for up to 72 months. You likely don't need to hire anyone when:

- You agree with the balance and can pay within 180 days — the short-term plan is free and takes minutes at the IRS payment plans page.

- You owe under $50,000 with steady income — follow our walkthrough on how to set up irs payment plan online and you're done the same day.

- Your only problem is a single penalty with a clean history — first-time abatement is often one phone call, and AEP may soon handle it automatically.

The full do-it-yourself playbook — every program, in order — is in our pillar guide on how to settle tax debt yourself. And if any professional fee would be a hardship, low income taxpayer clinic programs, coordinated through the Taxpayer Advocate Service, represent qualifying taxpayers at no charge.

Experienced help genuinely changes outcomes when a levy or garnishment is already in motion, when multiple years are unfiled, when you dispute what the IRS says you owe, when the debt is business or payroll tax, or when the OIC math is close enough that presentation decides it. And if your situation involves potential criminal exposure or Tax Court, read tax relief attorney vs company before hiring either.

Terms you'll hear on the sales call, decoded

- Enrolled agent (EA): a federally credentialed practitioner authorized to represent taxpayers before the IRS in all 50 states — one of only three credentials that can.

- Form 2848: the power-of-attorney form that lets a practitioner deal with the IRS for you; until it's filed, nobody is representing you.

- Investigation phase: industry shorthand for pulling your transcripts and diagnosing the case — useful work, but it does not pause collections by itself.

- Offer in Compromise: the IRS program for settling a debt below the balance when the numbers prove you can't pay it — means-tested, not a discount anyone can buy.

- Reasonable Collection Potential (RCP): the IRS formula — asset equity plus a multiple of monthly disposable income — that decides whether an offer can be accepted.

- Fresh Start: a marketing-friendly label for standard IRS collection policies, not a special program that firms unlock.

Hiring a tax relief firm: your questions, answered

What should I ask a tax relief company before hiring them?

Ask five things at minimum: who will work your case and what credential they hold, the total fee in writing, which IRS program they recommend and why your finances fit it, whether a Form 2848 power of attorney will be filed in the first week, and the refund policy. A firm that answers all five plainly deserves a second call; a firm that dodges the fee question does not.

How much does a tax relief company cost?

Flat fees commonly run from about $1,000–$2,500 for a straightforward payment-plan case to $3,500–$7,500 or more for an Offer in Compromise or multi-year representation. The number matters less than the scope: ask whether the quote covers everything through resolution, or whether a separate "investigation" fee comes first and the real fee arrives later. Get every dollar in writing before paying anything.

Can a tax relief company really settle my tax debt for less than I owe?

Sometimes — through the IRS Offer in Compromise program — but only when your assets and future income genuinely cannot cover the debt. The IRS accepted roughly 1 in 5 offers in FY2024, and it runs the math on your finances, not on a firm's marketing. Any company quoting a settlement figure before reviewing your income, expenses, and assets is guessing.

Is the IRS Fresh Start program something only tax relief companies can access?

No. "Fresh Start" is a label for standard IRS collection policies — expanded payment plans, higher lien thresholds, streamlined offers — that any taxpayer can use directly for free. Companies pitching Fresh Start as a secret or expiring program are using it as a sales hook. What a good firm actually sells is judgment: knowing which program fits your numbers and executing it correctly.

What are the biggest red flags when hiring a tax relief company?

Promised outcomes before anyone reviews your transcripts or finances, "pennies on the dollar" pitches, guaranteed settlements, large upfront fees with vague scopes, pressure to sign the same day, and no named EA, CPA, or attorney on your case. Any one of these is a reason to slow down; two or more is a reason to hang up.

Should I hire a tax attorney or a tax relief company?

For most collection cases — payment plans, offers, penalty relief — an enrolled agent or CPA at a reputable firm can do everything an attorney can, usually for less. You specifically want an attorney when there is potential criminal exposure, you need attorney-client privilege, or your case is headed to Tax Court. Ask any firm which of its practitioners would handle your file and why.

What can I do if a tax relief company took my money and did nothing?

Demand a written case status and itemized accounting, then request a refund in writing with a deadline. If that fails, dispute the charge with your card issuer and file complaints with your state attorney general and the FTC. Also check whether a Form 2848 was ever filed on your IRS account — and know that you can hire a new representative at any time.

Do I need a tax relief company for a $13,600 tax debt?

Often not. A $13,600 balance fits the IRS's streamlined installment agreement rules, which let you set up a plan online without submitting financial statements, and first-time penalty abatement may trim the balance for free. Help earns its fee when there is a levy in motion, unfiled years, a disputed amount, or business or payroll debt — not for a simple plan you can start yourself.

Your next 24 hours

- Pull your own numbers. Log into your IRS online account at IRS.gov (or find your most recent notice) so you know the exact balance and tax years before any salesperson tells you what they are.

- Gather the paper. Your last filed return, every IRS notice you've received, and a rough monthly income-and-expense picture — every honest quote in this industry starts from these three things.

- Get a free second opinion. Bring this article's 12 questions — and any quote you've been given — to a free case review at the 2-minute form or (888) 825-7779. Penalties and interest accrue every month a balance sits unresolved, so a clear answer this week beats a sales pitch next month.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Fee ranges cited are commonly quoted market figures, not quotes or promises.