Tax Relief Industry

Offer in Compromise Mill: How the Scam Works and How to Spot One in 2026

The short answer: an offer in compromise mill is a tax-relief operation that charges thousands of dollars upfront to file IRS settlement offers for people whose finances don't qualify. The tell: they promise results before reviewing your finances. The IRS accepted roughly 1 in 5 offers in FY2024 — eligibility is means-tested math, not marketing.

The rep on the phone said the words that made your stomach unclench for the first time in months: a government program can settle your IRS debt, you're pre-qualified, and the special rate ends Friday. Now you're searching the company's name plus "scam" — which is exactly the right instinct. This page shows you how the mill playbook works, what the real numbers look like, and what to do whether you're being pitched right now or already paid.

⏱ The real clock: an offer in compromise mill carries no IRS deadline — but your debt does. The failure-to-pay penalty adds 0.5% every month, interest compounds daily, and any unfiled year racks up a failure-to-file penalty of 5% per month (capped at 25% per year). Every month a mill stalls, the balance grows.

Why an OIC mill found you

Mills find their customers through public records and purchased lead lists — the call that feels eerily well-informed usually is. When the IRS files a Notice of Federal Tax Lien, that filing is a public record; lead-generation companies scrape lien filings and court records, then sell your name to whoever pays. State tax warrants — public civil judgments in states like New York — feed the same pipeline.

The rest come in through advertising built around two phrases: "Fresh Start" and "pennies on the dollar." Both are engineered to sound like a new amnesty. Neither is. Fresh Start is a set of policy expansions to ordinary IRS programs — not a forgiveness program you enroll in, and no private company has special access to it. The "pennies on the dollar" line has been the target of FTC enforcement for years; in 2026 the FTC permanently banned a major tax-relief operator from the industry over exactly these claims. If you've heard the related pitch about "one-time forgiveness," see our breakdown of the IRS one-time forgiveness myth.

The mill playbook: how the tax settlement scam actually runs

An OIC mill's product is the fee, not the resolution — the IRS itself has repeatedly named OIC mills in its annual Dirty Dozen list of tax scams. The playbook is consistent enough to describe stage by stage:

Stage 1 — the hook. A radio ad, robocall, or search ad promises settlement of tax debt through a "new government program." The salesperson is a commissioned closer, not a tax practitioner. Urgency is manufactured: the program is "expiring," or — a 2026 favorite — "the IRS is in chaos after the layoffs, so act now." (The staffing cuts are real; the expiring program is not.)

Stage 2 — the five-minute pre-qualification. You're told you "qualify" after a call that never examines your bank statements, assets, or IRS transcripts. That's the impossible part: OIC eligibility is a financial calculation the IRS performs on a full disclosure. Nobody can know your answer in five minutes — and a real firm won't pretend to.

Stage 3 — the split fee. The contract divides payment into an "investigation phase" and a larger "resolution phase," typically totaling thousands of dollars. The investigation phase is usually just pulling your IRS transcripts — something you can do yourself, free, through your IRS online account in about fifteen minutes.

Stage 4 — the stall. Months pass. Your calls reach rotating "case managers" with no credentials. Meanwhile the IRS notice sequence keeps advancing (more on that below), because hiring a company does nothing, by itself, to pause collection.

Stage 5 — the ending. One of three things happens: nothing gets filed at all; a Form 656 gets filed and returned because you weren't filing-compliant; or a doomed offer gets filed, sits for months, and is rejected because the math never worked. The company then points to the fine print — it promised to "pursue" a settlement, not obtain one. The pattern mirrors the ERC promoter scandal; if that one touched you too, see ERC mill claim problems.

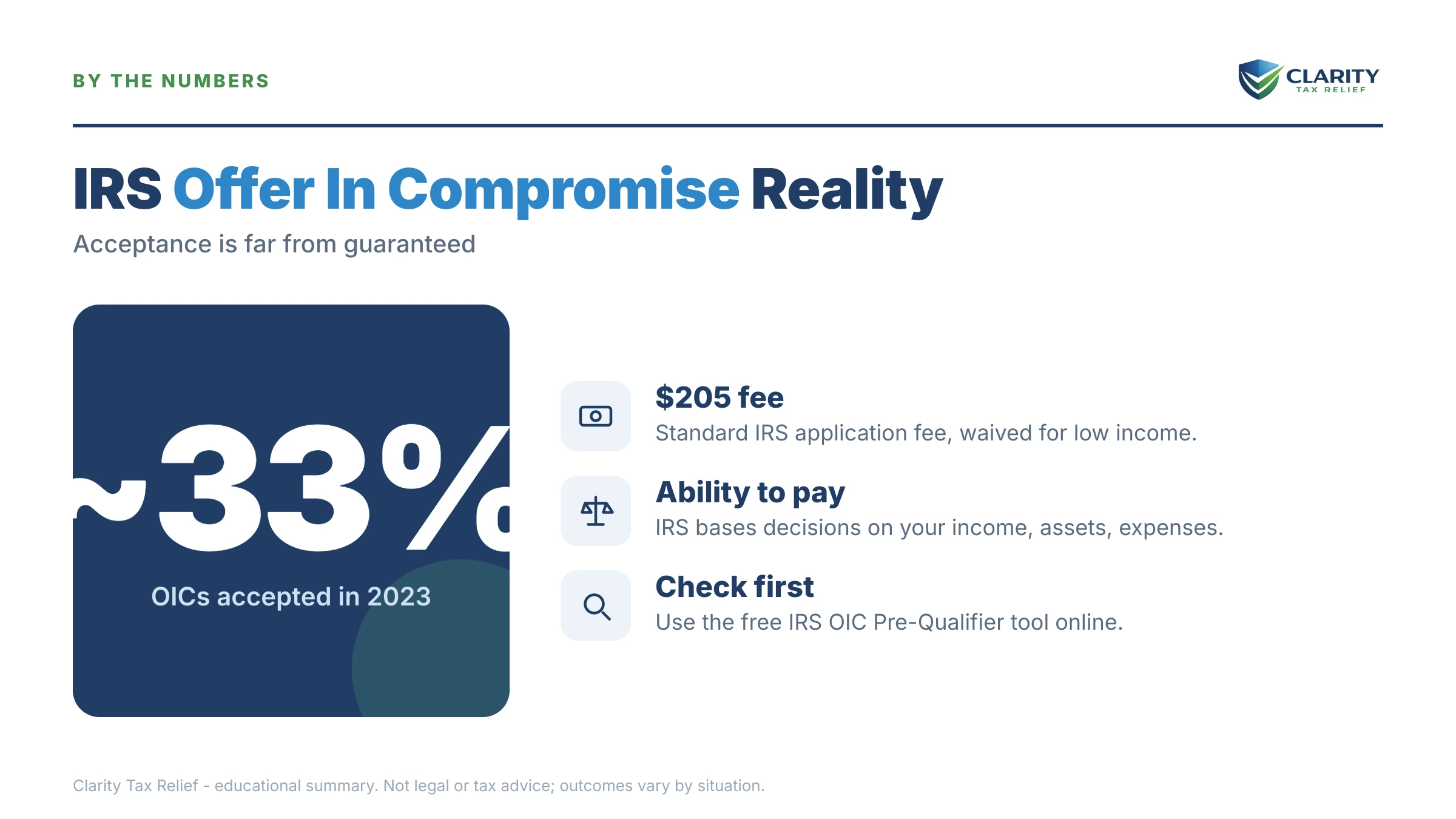

The real offer in compromise math mills hope you never run

The IRS accepts an offer only when it concludes it could never collect the full debt — and it accepted roughly 1 in 5 offers in FY2024. The full mechanics live in our guide to how an offer in compromise actually works; here is the one number that decides everything.

It's called Reasonable Collection Potential (RCP): the equity in your assets plus what the IRS believes it can take from your future income after allowable living expenses. If your RCP is $15,000 and you owe $6,200, your offer is rejected — the IRS can simply collect the full amount. If your RCP is $2,000 against a $60,000 debt, an offer becomes genuinely realistic. You can run a rough version of this math yourself in a few minutes with our Offer in Compromise Calculator — it estimates, it doesn't promise, but it will tell you more truth than any sales call.

The real costs are modest, which is its own tell about mill pricing: the IRS application fee is $205, plus 20% down on a lump-sum offer — and low-income certification (income at or below 250% of the federal poverty level) waives the fee, the down payment, and payments during review entirely. For the acceptance data by year, see the OIC acceptance rate with real IRS numbers.

A worked example: the $6,200 gig worker a mill loves

Say you drive for delivery apps, haven't filed for three years, and once the returns are prepared you'd owe about $6,200 in total tax. A mill quotes you $4,500 — "investigation" now, "resolution" later — to settle it. Run the math the salesperson didn't:

- The fee is 73% of the debt. $4,500 ÷ $6,200 = 0.73. Nearly three-quarters of the balance goes to the company before the IRS sees a dime.

- The offer can't even be processed. The IRS won't consider an OIC while required returns are unfiled. With three missing years, Form 656 comes straight back. (Start with our guide if you haven't filed in 3 years — filing also stops the 5%-per-month failure-to-file penalty, which is ten times the late-payment penalty.)

- The math is doomed anyway. Suppose that after IRS allowable expenses you clear even $200 a month of spare income. The IRS multiplies that by roughly a year's worth (more for periodic offers) and adds asset equity — call it $2,400 in future income plus, say, $4,000 of equity in your car. That RCP of roughly $6,400 exceeds the $6,200 debt, so the offer is rejected: the numbers say you can pay in full.

- The boring fix is cheap. File the three returns, then set up a payment plan online. At $6,200, you're under the $10,000 threshold for a guaranteed installment agreement, and a long-term plan spread across 72 months runs about $86 a month ($6,200 ÷ 72) before continuing interest and the 0.5% monthly penalty. That $4,500 mill fee, sent to the IRS instead, would have wiped out most of the balance on day one.

This is hypothetical, and your numbers will differ — but the structure of the trap doesn't. Mills profit most from small balances, because small balances almost never qualify for an offer and almost always resolve with a payment plan the mill could never justify charging thousands for.

What happens to your IRS account while a mill stalls

Hiring a company does nothing, by itself, to pause IRS collection — the automated notice sequence keeps advancing while your file sits in a drawer. In 2026 this matters more than ever: the IRS workforce was cut roughly 27% in 2025, but the notices, liens, and levies are generated by automated systems that never stopped. Here's what continues while the "case manager" tells you it's being handled:

- The bills keep coming. A CP14 gives you about 21 days at the cheapest moment to resolve; CP501 and CP503 reminders follow, each adding accrued penalties and interest to the balance.

- CP504 arrives. The IRS can now seize your state tax refund under IRC §6331(d), and a federal tax lien — a public record that feeds the next round of mill calls — becomes likely.

- LT11 / Letter 1058 starts a 30-day clock. This is the final notice of intent to levy. Requesting a Collection Due Process hearing on Form 12153 within 30 days is a genuine legal right — one that expires whether or not anyone at the mill is watching your mail.

- Levies begin. A bank levy freezes funds for a 21-day hold before the money leaves; a wage levy is continuous until released.

- Unfiled years get worse on their own. The IRS can file a substitute return for each missing year — computed with no deductions, no mileage, no business expenses — turning a manageable gig-work balance into an inflated assessment.

Been quoted thousands to "settle" your tax debt?

Before any money moves, get a second opinion. An experienced tax professional will pull your real IRS numbers, run the actual offer math, and tell you honestly if a simple payment plan solves this for a fraction of that quote — free, confidential, no pressure, no countdown timer.

Your real options for the debt a mill wants to "settle"

Every legitimate path to resolving a tax debt has a published cost and a knowable timeline — which is exactly why mills avoid discussing them. Here's the honest menu, using a $6,200 balance as the reference point:

| Option | Upfront cost | Typical timeline | Best fit |

|---|---|---|---|

| Short-term payment plan | $0 setup | Up to 180 days | You can pay in full within six months |

| Long-term installment agreement | Modest setup fee (reduced or waived for low income) | Up to 72 months online for balances ≤ $50,000 | Steady income; need monthly payments |

| Guaranteed installment agreement | Setup fee only | Short payoff term | Balance ≤ $10,000, returns filed — the IRS must accept when the conditions are met |

| Currently Not Collectible | $0 | Until finances improve (IRS reviews periodically) | Genuine hardship; debt remains and interest accrues |

| Legitimate Offer in Compromise | $205 fee + 20% down (both waived with low-income certification) | Several months to 1–2 years | Assets and income genuinely can't cover the debt |

| Penalty abatement (FTA / AEP) | $0 | Weeks to a few months; AEP becomes automatic starting summer 2026 | Clean compliance history for the prior 3 years |

| Low Income Taxpayer Clinic | Free | Varies by clinic | Income-qualified taxpayers in collection disputes |

| Typical OIC mill package | Often thousands of dollars upfront | Months of stalls, frequently no resolution | No one — this row is the warning |

Two comparisons deserve their own reads if your situation is genuine hardship rather than a payment-plan case: CNC vs offer in compromise covers when a collection pause beats a settlement attempt, and bankruptcy or offer in compromise covers when older income-tax debt makes bankruptcy the stronger tool. Note the penalty-relief row, too: with a clean prior three years, first-time abatement can remove penalties at no cost — and the new Automatic Exemption from Penalty (AEP) applies automatically starting summer 2026, no request and certainly no $4,500 fee required.

And here is the sequence a mill will never mention, because it exposes the whole pitch: file first, abate penalties second, then resolve the remaining balance. Done in that order, many "settle my debt" cases shrink to a number a payment plan handles easily.

How to respond to an offer in compromise mill, step by step

- Pause before paying. Refuse to sign or pay anything on the first call, no matter what discount supposedly expires tonight.

- Ask who will represent you. Get the full name and credential — EA, CPA, or attorney — of the person who would sign your Form 2848, then verify it independently.

- Pull your own IRS records. Log into your IRS online account and confirm your real balance and which returns are missing before anyone quotes a fix.

- Demand the fee agreement in writing. Every phase, every dollar, and exactly what you get if the offer is rejected or returned.

- Compare the quote to the options table above. If a payment plan clears the debt for less than the fee, the pitch fails its own math.

- Report and recover if you already paid. Demand a written refund, dispute the card charge, and file complaints with your state attorney general and the FTC.

While you're vetting, keep our tax relief red flags checklist and the list of questions to ask a tax relief company open in another tab — five minutes with either one ends most mill calls.

Mill red flags vs. what a legitimate firm does

The difference between a mill and a legitimate firm shows up before any money changes hands — in what they say on the very first call. Use this side by side:

| Mill red flag | What a legitimate firm does |

|---|---|

| Promises a settlement or quotes savings on the first call | Pulls IRS transcripts and analyzes your finances before predicting anything |

| Says you're "pre-qualified" for Fresh Start | Explains that eligibility is means-tested and shows you the actual math |

| Large upfront fee split into vague "phases" | Written flat fee tied to named deliverables |

| Anonymous rotating "case managers" | A named EA, CPA, or attorney signs Form 2848 and appears on your IRS file |

| Ignores your unfiled returns | Gets you filing-compliant first, because the IRS requires it before any offer |

| Pressure to sign today; the discount "expires tonight" | Puts the quote in writing and gives you time to compare |

| Guarantees an outcome or ties a refund to IRS acceptance | States plainly that no outcome is guaranteed — because none is |

Already paid a tax relief mill? How to get your money back

Money paid to a mill is sometimes recoverable, and the odds improve the faster you move. Work these channels in parallel, not one at a time:

- Written refund demand. Cite the specific services in your contract that were never delivered — no transcripts pulled, no returns filed, no Form 656 submitted. Send it in writing and keep a copy; it becomes evidence in every step below.

- Card chargeback. If you paid by credit card, dispute the charge for services not rendered. Chargeback windows are limited, so this comes first, not last.

- State attorney general and FTC. File a complaint with your state AG's consumer protection division and with the FTC at ReportFraud.ftc.gov. Consumer refunds have come out of enforcement actions against these companies, and complaint volume is what triggers them.

- IRS complaint. If someone at the company actually prepared or filed anything with the IRS on your behalf, Form 14157 (Return Preparer Complaint) puts their conduct in front of the IRS directly.

- Take back control of your case. Revoke any Form 2848 power of attorney the mill holds, so nothing else gets filed in your name — and so your notices come to you.

Our full recovery guide — a tax relief company took my money — walks through each channel with timelines and template language. One caution while you fight for the refund: the IRS debt itself hasn't paused, so run the recovery track and the resolution track at the same time.

When you can handle this yourself — and when help genuinely matters

Most small tax debts never need professional representation, and any honest firm will say so. You can confidently do it yourself when:

- You agree with the balance and it's under $10,000 with your returns filed — a guaranteed installment agreement or a $0-setup short-term plan takes minutes online.

- You can pay in full within 180 days — set up the short-term plan and be done; there is nothing a firm can add.

- Your income qualifies for free help — a Low Income Taxpayer Clinic provides real representation at no cost, which beats any paid option at any price.

Experienced help changes outcomes in a narrower set of situations: a levy already in motion (release negotiations are time-critical), multiple unfiled self-employment years where income must be reconstructed from 1099s and bank records, business or payroll tax debt with personal-liability exposure, and genuine OIC candidates — where getting the RCP math and asset valuations right is the difference between acceptance and a rejected offer that merely paused the collection statute. The irony of the mill economy is that real representation exists for exactly these cases; mills just sell it to everyone else.

If a levy is running, returns are missing, or your own math says an offer might genuinely fit, have an experienced tax professional review your file free before another month of penalties posts.

Terms the sales rep used, decoded

- Fresh Start Program — a set of IRS policy expansions to existing programs (payment plans, lien thresholds, OIC terms); not a new amnesty, and not something you enroll in.

- "Pre-qualified" — a sales term, not an IRS status; the IRS decides eligibility only after reviewing a full financial disclosure.

- Reasonable Collection Potential (RCP) — the IRS's calculation of the most it could ever collect from your assets and future income; your offer generally has to meet or beat it.

- Form 656 — the actual Offer in Compromise application, filed with a financial disclosure (Form 433-A (OIC)) and the $205 fee.

- "Investigation phase" — mill billing language for pulling your IRS transcripts, which you can do free through your IRS online account.

- CSED — the Collection Statute Expiration Date, the 10-year limit on IRS collection from assessment; a pending offer pauses that clock.

Offer in compromise mill FAQs

How do I know if a tax relief company is an offer in compromise mill?

The clearest tell is a settlement promise before anyone has seen your finances. A legitimate firm reviews your IRS transcripts, income, and assets before saying whether an offer is realistic; a mill tells you that you are pre-qualified after a five-minute phone call. Other red flags: large upfront fees split into vague phases, no named EA, CPA, or attorney on your case, and pressure to sign the same day.

Is the IRS Fresh Start program real?

Real, but not what the ads describe. Fresh Start was a set of IRS policy changes that expanded ordinary programs — payment plans, lien thresholds, and the Offer in Compromise. It is not a new forgiveness program, there is no enrollment deadline, and no company has special access to it. Any pitch that treats Fresh Start as a limited-time amnesty is marketing, not tax law.

Can the IRS really settle tax debt for less than the full amount?

Yes — the Offer in Compromise is a real IRS program, but it is means-tested math, not negotiation. The IRS accepted roughly 1 in 5 offers in FY2024, and acceptance turns on whether your assets and future income genuinely cannot cover the debt before the collection statute runs out. If the numbers show you can pay, the offer is rejected no matter who files it.

What does a legitimate offer in compromise actually cost?

The IRS charges a $205 application fee, and lump-sum offers require 20% of the offer amount up front. If your income is at or below 250% of the federal poverty level, low-income certification waives the fee, the down payment, and payments during review. Professional preparation fees vary, but a legitimate firm quotes them in writing after reviewing your finances — not before.

Can I file an offer in compromise if I have unfiled tax returns?

No — the IRS will not process an offer until all required returns are filed. This is the detail mills routinely skip: they collect the fee, submit Form 656, and the IRS sends the package back for non-compliance. If you have unfiled years, getting those returns done is step one of any real resolution, and it usually shrinks the problem by stopping the 5%-per-month failure-to-file penalty.

Does filing an offer in compromise stop IRS collection?

Generally, yes — the IRS suspends most collection activity, including levies, while an offer is pending. But interest keeps accruing, and the 10-year collection statute pauses during review, so a doomed offer just gives the IRS more time to collect later. Mills sometimes file hopeless offers precisely because the pause looks like progress to the client.

How long does an offer in compromise take?

Most offers take several months to well over a year from submission to decision, and complex or appealed cases run longer. One safeguard works in your favor: if the IRS does not make a decision within 2 years, the offer is accepted automatically by law. Add preparation time — gathering financials and filing any missing returns — before that clock even starts.

Can I get my money back from a tax relief company that did nothing?

Sometimes — and it is worth pursuing. Start with a written refund demand citing the undelivered services in your contract, then dispute the charge with your credit card company if you paid by card. File complaints with your state attorney general and the FTC; consumer refunds have come out of enforcement actions against these companies. Move quickly — chargeback windows are limited.

Are pennies-on-the-dollar ads illegal?

The promise is what regulators target. The FTC has sued and banned tax-relief operators for promising settlements they could not deliver, and the IRS has repeatedly named OIC mills in its annual Dirty Dozen list of tax scams. A company can lawfully advertise the Offer in Compromise program — what it cannot lawfully do is promise or guarantee a settlement before analyzing your finances.

Is every tax relief company a scam?

No — legitimate tax representation is a real, regulated profession. Enrolled agents, CPAs, and tax attorneys are authorized to represent you before the IRS under Circular 230 and can genuinely change outcomes in levy, multi-year, and offer cases. The difference is process: a legitimate firm investigates first, quotes in writing, and tells you when a simple payment plan is the better answer.

For the program's official terms — fees, forms, and eligibility — go straight to the source: the IRS's Offer in Compromise page. If a mill has left your IRS case in genuine disarray and you're getting nowhere, the independent Taxpayer Advocate Service exists for exactly that.

Your next 24 hours

- Find the fee breakdown on whatever the company sent you — the contract or quote — and note who, by name and credential, would actually represent you. If no name appears anywhere, you already have your answer.

- Gather your paper: your last filed return, any IRS notices you've received, and income records (1099s, 1099-Ks, bank statements) for any unfiled years. Whoever helps you — paid or free — needs these on day one.

- Get a real second opinion before any money moves: the 2-minute form at the free case review, or (888) 825-7779. There's no fake countdown here — the only clock is the 0.5% monthly penalty and daily interest quietly compounding on your balance, and that clock is real.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.