IRS Programs & Data

Offer in Compromise Acceptance Rate: What the Real IRS Numbers Show (2026)

The short answer: the offer in compromise acceptance rate was roughly 1 in 5 in FY2024 — about 20% of offers accepted. Acceptance isn't a lottery. Offers succeed when the amount offered matches or beats the IRS's calculation of what it could ever collect from you, and fail on math, missing documents, and unfiled returns.

You've got a levy warning sitting next to the rent bill, a $4,800 IRS balance, and a feed full of ads swearing the government "settles tax debt" every day. Before you spend $205 and months of waiting to find out whether that's true for you, look at the number the ads never quote — and the specific math that decides which side of it you land on.

This page breaks down why the rate sits where it does, the difference between a rejected offer and a returned one (they're counted very differently), and a worked $4,800 example showing exactly how the IRS would score a renter's offer. The comparison tables below also show when an offer is simply the wrong tool — which, at small balances, it often is.

⏱ The clocks that actually run: there is no deadline to apply for an offer in compromise — but two real clocks run anyway. Penalties and interest keep accruing on your balance every month until a resolution is in place. And once you file, the IRS has 2 years to decide your offer; if it doesn't, the offer is deemed accepted by law — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count.

Why the offer in compromise acceptance rate is stuck near 1 in 5

The IRS accepted roughly 1 in 5 offers in compromise in FY2024, and the rate stays low because most offers fail predictable, avoidable tests. An offer in compromise is not a negotiation over how sad your situation is. It's an audit of your finances against one formula, and the formula produces a number before anyone reads your hardship letter.

That formula is Reasonable Collection Potential (RCP): what the IRS could realistically collect from your assets and future income before the 10-year collection statute runs out. Offer at least your RCP and the offer is viable. Offer less — or fail to document your numbers — and it isn't, no matter who filed it for you.

The headline rate also pools three very different groups: people whose finances genuinely can't cover the debt, people who could clearly full-pay but applied anyway because an ad told them to, and clients of OIC mills that file doomed applications to earn a fee. Your personal odds aren't 20%. Depending on the math, they're close to zero — or far better than the average. The "pennies on the dollar" pitch survives precisely because a blended statistic hides that split.

One more 2026 wrinkle: with the IRS workforce down roughly 27% after the 2025 cuts, offer reviews are moving slower — which makes the 2-year deemed-acceptance rule more relevant than it has been in years, and makes a clean, complete application (one that doesn't bounce back for missing pages) worth even more.

Returned vs. rejected: the number behind the number

Many offers never get a yes-or-no decision at all — they are returned unprocessed for paperwork problems before an examiner ever runs the math. Understanding the two failure modes tells you where offers actually die:

- Returned offers bounce for processability problems: an unfiled required return, a missing application fee or down payment, incomplete Form 433-A(OIC) sections, falling behind on current-year taxes, or an open bankruptcy case. A returned offer comes with no appeal rights — you lose months and start over.

- Rejected offers were reviewed and turned down on the numbers, usually because the IRS computed an RCP higher than the amount offered. A rejection letter includes the IRS's worksheet and a 30-day window to appeal.

This distinction is the single most useful thing on this page. The paperwork failures are entirely preventable before you file. The math failures are knowable before you file. Which means the part of the acceptance rate you control is much larger than the 1-in-5 headline implies.

| Factor | Effect on your offer | Why |

|---|---|---|

| Unfiled required returns | Offer returned, unreviewed | Non-filers fail the processability screen before the math is ever run |

| Offer amount below your RCP | Rejection | The IRS won't accept less than it calculates it can collect on its own |

| Renting instead of owning | Helps | No home equity to add to the asset side of the RCP formula |

| Undocumented living expenses | Hurts | Unproven expenses get disallowed, which inflates your disposable income |

| Low-income certification (AGI ≤ 250% of poverty) | Helps | Waives the $205 fee, the 20% down, and payments during review — a rejection costs $0 |

| Recently transferred or spent-down assets | Hurts | The IRS can add "dissipated assets" back into the RCP as if you still had them |

| Behind on this year's withholding or estimates | Hurts | The IRS won't settle old years while a new balance is actively forming |

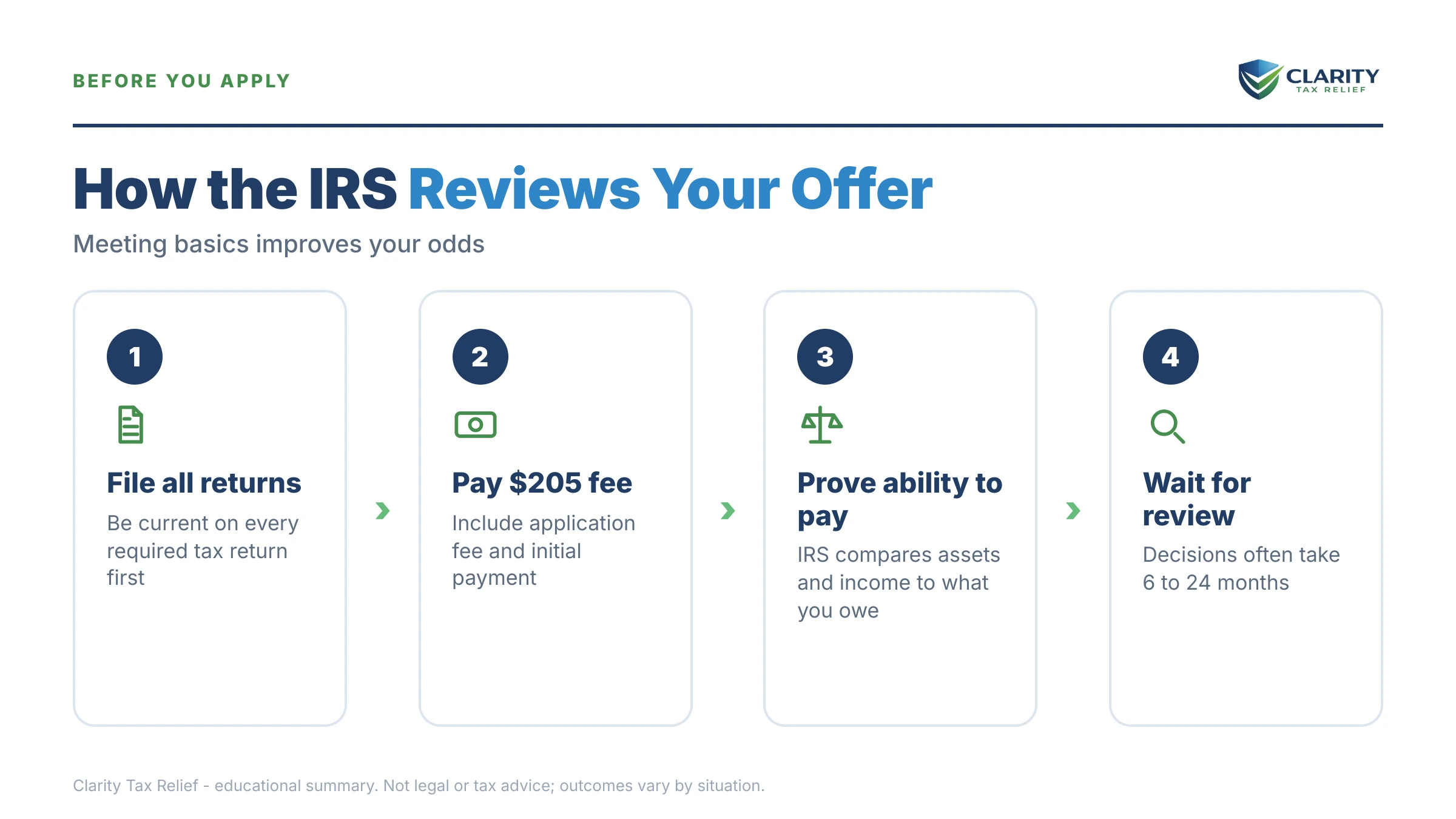

How the IRS decides: the Reasonable Collection Potential math

The IRS accepts an offer when it equals or exceeds your Reasonable Collection Potential — your net asset equity plus 12 months of monthly disposable income for a lump-sum offer (24 months for a periodic-payment offer). Disposable income is your actual income minus the IRS's allowable living expense standards, not minus what you actually spend. That gap between "allowable" and "actual" is where most rejections are born.

The mechanics — Form 656, Form 433-A(OIC), the fee, the review process — are covered in our hub on how an offer in compromise actually works. Here, the only question is the one the acceptance rate turns on: what number does the formula produce for you? You can estimate it in a few minutes with our Offer in Compromise Calculator before spending anything on an application.

A worked example: $4,800 owed, renting, levy warning in hand

Say you owe $4,800, you rent, and your take-home pay is $2,900 a month. This is hypothetical, and the arithmetic is the point:

- Income vs. allowable expenses: rent and utilities $1,650, plus the IRS national standards for food, clothing, and miscellaneous, vehicle operating costs, and health costs — say $2,750 total allowable. Disposable income: $2,900 − $2,750 = $150/month.

- Future income component: $150 × 12 (lump-sum multiplier) = $1,800.

- Assets: $600 in checking (largely covered by the small cash allowance the form permits), a $4,000 car with a $3,500 loan — after the IRS's quick-sale discount, effectively $0 equity. No house, no retirement account. Asset component: roughly $0–$300.

- RCP: about $1,800–$2,100. Since that's below the $4,800 owed, an offer of roughly $2,100, fully documented, is genuinely viable — the profile of offers that land in the accepted fifth.

Now flip one variable. If your disposable income were $300/month instead of $150, the future income component becomes $3,600 — and with any asset equity at all, the IRS concludes you can full-pay $4,800 through a payment plan and rejects the offer. At small balances, a $150/month swing in the expense math is the entire difference between accepted and rejected. That sensitivity is why documentation, not persuasion, decides these cases.

Cost check on the viable version: a $2,100 lump-sum offer needs the $205 fee plus 20% down ($420) with Form 656, with the rest due in a few installments after acceptance. If your AGI qualifies for the OIC low-income certification — at or below 250% of the federal poverty level — the fee, the down payment, and payments during review are all waived.

Five situations that change your acceptance odds

Married, but only one spouse owes. The IRS still looks at household income and household expenses to figure your share of disposable income, even when your spouse isn't liable. A non-liable spouse's paycheck can quietly raise your RCP above the debt.

Self-employed or 1099. Your 433-A(OIC) must include business income, receivables, and equipment, and irregular income gets averaged — usually over recent months of bank statements. Sloppy records read as understated income, and understated income reads as rejection.

Homeowner vs. renter. Home equity flows almost straight into RCP. A renter with the same income and same debt is often a viable candidate where a homeowner with $60,000 of equity is not. If you own a business that owes, the math changes again — see business offer in compromise.

Multiple years, some unfiled. One offer covers every assessed balance, but every required return must be filed first or the whole package is returned unreviewed. File first, offer second — the order isn't optional.

You also owe a state. An IRS acceptance does nothing to state debt, and state programs run on their own rules and their own math. California's version is covered in our FTB offer in compromise guide.

What happens if you wait while a levy is in motion

An IRS wage levy is continuous — it attaches to every paycheck until the IRS releases it — while a bank levy holds your funds for 21 days before they're sent to the Treasury. If a levy warning is already on your table, the collection sequence keeps moving while you research settlement percentages. The stages, in order:

- CP504 — Notice of Intent to Levy. The IRS can seize your state tax refund at this stage. It is not yet the final notice.

- LT11 / Letter 1058 — Final Notice of Intent to Levy. This starts a 30-day clock and your Collection Due Process rights. After the 30 days, wage and bank levies become legal.

- Wage levy. A portion of every paycheck goes to the IRS, continuously, until the levy is released or the debt is resolved.

- Bank levy. Funds in the account are frozen for 21 days, then sent. New deposits after the levy date aren't taken — but the levy can be repeated.

Here's where the offer intersects the sequence: once the IRS accepts your offer as processable, it generally suspends new levy action while the offer is reviewed (your transcript will show code 480 during the pending period). But a levy already clamped onto your paycheck isn't automatically released by filing — and the collection statute pauses while your offer is pending, so a hopeless offer just extends how long the IRS can chase you. The order you act in genuinely changes the outcome.

| Stage | What it means | What a pending offer changes |

|---|---|---|

| CP14 (first bill) | Balance due; about 21 days before escalation begins | Filing anything now — offer or plan — stops the sequence at its cheapest point |

| CP504 | IRS can seize your state tax refund | A processable offer generally suspends new levy action while under review |

| LT11 / Letter 1058 | Final notice; 30-day clock; Collection Due Process rights attach | You can propose an offer inside a timely CDP hearing, freezing levies while it's heard |

| Active wage levy | Continuous — every paycheck until released | Not automatically released by filing; request release as a separate step |

| Active bank levy | 21-day hold before the bank sends the funds | The hold window is the time to act; a pending offer helps prevent the next one |

Levy notice on the table and weighing an offer?

Before you spend $205 finding out your RCP the hard way, let an experienced tax professional run the math on your $4,800 (or $48,000) — and check whether the levy can be paused first. Free, confidential, no pressure.

Is an offer even the right tool at $4,800? Your options compared

For a $4,800 balance, an online payment plan runs about $67 a month over 72 months before interest — which is exactly why the IRS rejects offers from people who can afford one. The acceptance rate isn't just about how offers are scored; it's about how many people file offers when a different tool fit better. Compare the real costs:

| Option | Upfront cost | Ongoing cost | Typical timeline |

|---|---|---|---|

| Lump-sum OIC | $205 fee + 20% of the offer | Balance of the offer in a few installments after acceptance | Often many months to over a year; deemed accepted at 2 years if no decision (narrow exceptions apply) |

| OIC with low-income certification | $0 — fee and down payment waived | No payments during review; offer amount after acceptance | Same review timeline; rejection costs nothing out of pocket |

| Short-term payment plan (up to 180 days) | $0 setup | Interest + 0.5%/month late-pay penalty until paid | Set up online the same day |

| 72-month online installment agreement (balances ≤ $50,000) | Modest setup fee, lower with direct debit | ~$67/month on $4,800, plus accruing interest and penalty | Online approval, usually same day |

| Guaranteed installment agreement (≤ $10,000) | Setup fee | ~$133/month to pay $4,800 within 3 years | IRS must accept if you meet the statutory conditions |

| Currently Not Collectible | $0 | Balance keeps growing; refunds offset; collection paused | Lasts until finances improve; IRS reviews periodically |

The honest read for our $4,800 renter: with $150/month of genuine disposable income, the $67/month plan is survivable — and simpler. The offer only wins if the hardship is real, documented, and durable, or if low-income certification makes the attempt free. If paying anything would break your budget, compare CNC vs offer in compromise — hardship status pauses collection without the application gauntlet. And if the debt is large, old, and tangled with other debts, the bankruptcy or offer in compromise question deserves a real answer before either move.

How to improve your offer in compromise acceptance odds, step by step

- File every missing tax return. The IRS returns offers from non-filers without reviewing them, so confirm every required return is filed before Form 656 goes in the mail.

- Run the Reasonable Collection Potential math first. Add 12 months of your monthly disposable income to your net asset equity; if the total is more than you owe, an offer will almost certainly be rejected.

- Get current on this year's taxes. Fix your withholding or make this quarter's estimated payment — an offer can be returned or rejected if you are falling behind on the current year while asking to settle old years.

- Document every figure on Form 433-A(OIC). Attach proof for income, rent, utilities, and medical costs; unsupported expenses get disallowed, which raises your Reasonable Collection Potential and sinks the offer.

- Offer at least your RCP and pick the right payment terms. Submit Form 656 with the $205 fee and 20% down for a lump-sum offer — or attach the low-income certification, which waives both if your AGI is at or below 250% of the federal poverty level.

Line-by-line help with the forms lives in our Form 656 walkthrough and Form 433-A walkthrough. And know the review is slow by design — our guide to how long an offer in compromise takes maps the stages so silence doesn't read as rejection.

When you can handle this yourself — and when help changes the outcome

You don't need professional help for everything on this page. Handle it yourself when:

- Your balance is small and a 180-day short-term plan or an online installment agreement fits your budget — both are self-serve on IRS.gov in under an hour;

- Your finances are simple — one W-2, renting, no business income — and your own RCP math clearly shows an offer is viable or clearly shows it isn't;

- You qualify for low-income certification, which makes a careful DIY offer a zero-fee attempt.

Experienced help earns its cost in specific situations: a levy is already in motion and release needs to be sequenced before or alongside the offer; you have multiple unfiled years that must be reconstructed before anything is processable; you're self-employed and the income-averaging math is contestable; the debt is business or payroll tax; or your first offer was rejected and the appeal turns on disputed expense figures. In those cases, the difference between a returned offer and an accepted one is usually preparation — not connections, and never a secret program.

If that second list sounds like your file, a free case review will tell you in ten minutes whether an offer is worth pursuing before you spend a dollar on it — the 2-minute form or (888) 825-7779.

Terms in OIC paperwork, decoded

- Reasonable Collection Potential (RCP): the IRS's calculation of everything it could collect from your assets and future income — the number your offer must meet or beat.

- Doubt as to collectibility: the most common offer basis — you owe the tax, but your finances can't cover it before the collection statute expires.

- Processable offer: an application that passes the intake screen (all returns filed, fee or certification included, forms complete) and earns an actual review.

- Returned offer: an application sent back unreviewed for a processability failure — no decision, no appeal rights.

- Low-income certification: the Form 656 checkbox for AGI at or below 250% of the federal poverty level that waives the fee, the down payment, and payments during review.

- Two-year rule: if the IRS doesn't decide your offer within 2 years of receipt, it's deemed accepted by law — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count.

- Five-year compliance clause: after acceptance, you must file and pay on time for five years — default, and the compromised debt comes back.

Offer in compromise acceptance rate: your questions, answered

What percentage of offers in compromise does the IRS accept?

The IRS accepted roughly 1 in 5 offers in compromise in fiscal year 2024 — about a 20% acceptance rate. That figure pools every offer filed, including thousands submitted by people who could clearly pay in full and by mills that file doomed applications for a fee. Applicants whose offer matches a properly documented Reasonable Collection Potential see far better results than the headline number suggests.

Why does the IRS reject most offers in compromise?

Most offers fail for one of three reasons: the amount offered is below the IRS's calculation of Reasonable Collection Potential, the financial disclosure has gaps or unsupported expenses, or the taxpayer's own numbers show they could pay in full through a payment plan. A separate group never gets reviewed at all — offers are returned unprocessed when returns are unfiled, the fee is missing, or the forms are incomplete.

What is the difference between a returned offer and a rejected offer?

A returned offer never got a decision — the IRS sent it back for a processability problem like unfiled returns, a missing fee, or incomplete forms, and there is no appeal. A rejected offer was actually reviewed and turned down on the math, and you have 30 days from the rejection letter to appeal using Form 13711. The distinction matters because a rejection comes with appeal rights and the IRS's own worksheet showing its numbers; a return gives you neither.

Does hiring a tax professional increase my acceptance odds?

The IRS doesn't publish acceptance rates by representation, so no honest firm can quote one. Where experienced help genuinely changes outcomes is before filing: running the Reasonable Collection Potential math to see whether an offer is viable at all, documenting allowable expenses so they aren't disallowed, and choosing between an offer, hardship status, or a payment plan. A professional who files a doomed offer is worse than no professional.

Can the IRS levy my paycheck while my offer is pending?

Generally no — once the IRS accepts your offer as processable, it suspends new levy action while the offer is under review, and transcript code 480 marks the pending period. Two cautions: a levy already in place is not automatically released just because you filed, and an offer submitted purely to stall collection can be flagged and returned. If a levy is already active, request its release as a separate step.

Do I lose my $205 fee and 20% down payment if my offer is rejected?

The $205 application fee is not refunded, and the 20% down payment is not returned either — but it isn't wasted, because the IRS applies it to your tax balance. That is why the low-income certification matters so much: if your AGI is at or below 250% of the federal poverty level, the fee, the down payment, and payments during review are all waived, so a rejection costs you nothing out of pocket.

What happens if my offer in compromise is rejected?

You get a rejection letter showing the IRS's Reasonable Collection Potential calculation, and you have 30 days to appeal with Form 13711. Many rejections turn on one disputed figure — a disallowed expense or an overvalued asset — and appeals officers can settle on numbers the examiner wouldn't. If an appeal isn't viable, you can fix the weakness and reapply, or pivot to a payment plan or Currently Not Collectible status.

Is the acceptance rate better for small tax debts like $5,000?

The IRS doesn't publish acceptance rates by debt size, and qualification is means-tested, not size-tested. Small balances actually face a structural headwind: the smaller the debt, the more likely your disposable income and assets can cover it, which leads the IRS to conclude you can pay in full through a plan. A $4,800 debt with genuine, documented hardship can absolutely be settled — but the hardship, not the small balance, is what qualifies it.

Does the IRS Fresh Start program guarantee my offer will be accepted?

No. 'Fresh Start' is the name attached to a set of collection-policy changes from over a decade ago — it loosened some offer math, but it is not a separate program you enroll in, and it guarantees nothing. Any company implying Fresh Start means easy or automatic settlement is marketing, not law. Every offer still runs through the same Reasonable Collection Potential review as every other offer.

If your offer was already turned down, start with OIC rejected — now what and the guide to appealing an OIC rejection with Form 13711 — the 30-day appeal window is short, and it's the one stage where the IRS shows you its math. Primary sources worth reading before you file: the IRS's official Offer in Compromise page, its payment plans and installment agreements page for the alternatives, and the Taxpayer Advocate Service if collection is causing hardship the normal channels won't fix.

Your next 24 hours

- Identify which notice you're actually holding. Look at the top-right code — CP504 and LT11 set very different levy clocks, and LT11's 30-day window is the one that matters most.

- Gather the RCP inputs: your last filed return, two months of pay stubs or bank statements, your rent and utility bills, and balances on your accounts and car loan. That's everything the acceptance math needs.

- Get the math run free before you spend the $205. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will tell you whether your numbers put you in the accepted fifth, and whether the levy can be paused first while interest and penalties are still accruing.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.