Tax Relief Programs

IRS One Time Forgiveness in 2026: What's Real, What's Marketing, and What You Can Actually Get

The short answer: "IRS one time forgiveness" is not an official IRS program — it's advertising shorthand. The closest real thing is First-Time Penalty Abatement, which removes penalties (not tax) after three clean years. Actual debt reduction happens only through an Offer in Compromise or the 10-year collection statute, and both are strictly means-tested.

You heard the ad on the radio, or a video promised the IRS will "forgive your debt one time if you just ask." Now you're searching to see if it's true before you owe another month of interest. Here's the honest version: the phrase is invented, but several real programs sit behind it — and one of them probably fits you.

⏱ The real clock: there is no application deadline for "one-time forgiveness," because no such program exists. The clock that actually matters is accrual — the 0.5% monthly failure-to-pay penalty plus daily-compounding interest add to your balance every month you wait for forgiveness that isn't coming.

Why "IRS one time forgiveness" is everywhere — and what the ads are really selling

The IRS has never operated a program called "one-time forgiveness" — the phrase was coined by tax-relief marketers, mostly as a repackaging of First-Time Penalty Abatement and the 2011-era Fresh Start changes. It survives because it converts: "forgiveness" sounds like a gift, while "installment agreement" sounds like homework.

The same thing happened with "Fresh Start," which was a real set of policy changes but is now used as if it were a secret application. We've broken that down separately in is the IRS Fresh Start program real — the pattern is identical: real programs, renamed to sound like amnesty.

This matters for a practical reason. If you call a company asking for "one-time forgiveness," you can't evaluate what they quote you, because you don't know which actual program they mean. The rest of this guide names each real program behind the phrase, what it does, and the eligibility line for each — so you can hold any pitch, including ours, against the facts. The image below shows how the marketing language maps to the real IRS programs at a glance.

The one real "one-time" break: First-Time Penalty Abatement (and its 2026 replacement)

First-Time Penalty Abatement (FTA) removes failure-to-file, failure-to-pay, and failure-to-deposit penalties if you had no penalties in the prior three tax years — and it's the only IRS relief that genuinely resembles a one-time courtesy. It's administrative, not means-tested: no financial disclosure, no hardship proof, no fee. You ask; if your record is clean, penalties come off, along with the interest that accrued on those penalties.

Three details the ads leave out:

- It removes penalties, never tax. If most of your balance is the tax itself, FTA shrinks the bill but doesn't settle it.

- It isn't strictly one-time. You can qualify again after another three penalty-free years — provided you've also filed all required returns and paid, or arranged to pay, what you owe at the time you ask. Our full first time penalty abatement guide covers how to request it and what to say.

- It's being replaced. Starting summer 2026, the IRS is rolling out the Automatic Exemption from Penalty (AEP) — the same relief applied automatically, with no request needed. If you're reading this mid-2026, check whether your penalty was already exempted before filing anything.

Interest on the tax itself is a different animal — the IRS almost never waives it except when its own error caused the delay. See can IRS interest be waived for the narrow exceptions. To see what penalties and interest are actually adding to your balance each month, you can estimate it with our IRS Penalty & Interest Calculator.

What happens if you wait for forgiveness that isn't coming

A tax debt left alone doesn't sit still — it grows monthly while the IRS's automated notice stream escalates toward levy. Nothing about the "one-time forgiveness" myth pauses this sequence. Here's the order it runs in:

- Accrual, every month: the 0.5% failure-to-pay penalty plus interest compound on your balance from the original due date forward.

- Balance-due notices (CP14, then CP501/CP503): bills and reminders. No enforcement yet, but every option is cheapest at this stage.

- CP504 — Notice of Intent to Levy: the IRS can now seize your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 / Letter 1058 — Final Notice: starts a 30-day clock and your Collection Due Process rights. After it runs, wage garnishment and bank levies are on the table.

- Enforcement: a bank levy holds funds for 21 days before they're taken; a wage levy continues paycheck after paycheck until released.

In 2026 there's an extra wrinkle: the IRS workforce shrank roughly 27% in 2025, so reaching a human is harder than ever — but the notice and levy systems are automated and never stopped. The machine escalates on schedule whether or not anyone answers the phone.

Sold on "forgiveness" and not sure what's true?

Before you pay anyone — including us — get a free review of your actual IRS account. An experienced tax professional will tell you which real program fits your numbers, while penalties and interest are still small enough to matter.

IRS one-time forgiveness vs. the real programs behind it (2026)

Every "forgiveness" claim in an advertisement maps to one of five real IRS programs, each with a hard eligibility line. This table is the translation key:

| What the ad calls it | The real IRS program | Who may qualify | What it actually does |

|---|---|---|---|

| "One-time forgiveness" | First-Time Penalty Abatement (becoming AEP, summer 2026) | No penalties in the prior 3 tax years | Removes penalties and the interest on them — never the tax itself |

| "Settle for less" | Offer in Compromise (Form 656; $205 fee, waived for low-income filers) | Income and assets genuinely can't cover the debt — roughly 1 in 5 offers accepted in FY2024 | Settles the debt for your Reasonable Collection Potential |

| "Fresh Start forgiveness" | Streamlined installment agreements | Balances up to $50,000 — set up online, up to 72 months | More time to pay; no reduction, interest keeps accruing |

| "Hardship forgiveness" | Currently Not Collectible status | IRS allowable living expenses meet or exceed your income | Pauses collection; the debt and interest remain on the books |

| "Debt disappears after 10 years" | Collection statute expiration (CSED) | Everyone — 10 years from assessment, paused by appeals, a pending OIC, or bankruptcy | Unpaid balance expires — if the IRS doesn't collect it first |

Only two rows on that table ever erase tax you legitimately owe — an accepted Offer in Compromise and the CSED. For how the offer math actually works, start with how does an offer in compromise work; for the 10-year clock and its tolling traps, see does IRS debt go away after 10 years. If your problem is cash flow rather than the total, IRS Currently Not Collectible status and payment plans are the workhorses, and our hub on how to settle tax debt yourself walks through setting each one up without hiring anyone.

The real clocks and rights behind tax-debt relief

"Forgiveness" marketing hides the fact that real relief runs on specific, enforceable timelines. These are the ones worth knowing:

| The clock | How long | What it means for you |

|---|---|---|

| Collection statute (CSED) | 10 years from assessment | Unpaid debt expires — but appeals, a pending OIC, or bankruptcy pause the clock |

| OIC review window | 2 years | If the IRS doesn't decide your offer within 2 years, it's automatically accepted — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count |

| LT11 / Letter 1058 response | 30 days | Your window to file Form 12153 and lock in Collection Due Process rights before levy |

| AEP rollout | Starts summer 2026 | Eligible penalties come off automatically — no request or letter required |

| Passport certification | Triggers at $66,000 (2026) | Seriously delinquent debt above this threshold can block passport issuance or renewal |

A worked example: a married couple owing $11,300

Say you and your spouse filed jointly on time for 2024 but couldn't pay, and by mid-2026 the balance is $11,300 — roughly $9,900 in tax, $740 in failure-to-pay penalties (0.5% per month, about 15 months in), and $660 in interest. This is a purely hypothetical illustration; here's how each "forgiveness" path actually plays out:

- First-Time Penalty Abatement: if your 2021–2023 returns were penalty-free, the $740 in penalties comes off, plus the slice of interest charged on those penalties. New balance: roughly $10,500. That's real money for one phone call — but it's a 7% haircut, not forgiveness.

- Payment plan: at $10,500, you're under the $50,000 online threshold. Spread over the maximum 72 months, the floor payment is about $146/month — but interest keeps accruing, so paying $325/month and clearing it in around three years costs meaningfully less overall. Compare funding options in best way to pay the IRS.

- Offer in Compromise: here's where honesty bites. With two W-2 incomes leaving, say, $400/month after IRS allowable expenses, plus $8,000 of equity in vehicles and savings, your Reasonable Collection Potential runs roughly $400 × 12 + $8,000 = $12,800 — more than the $10,500 you'd owe after abatement. The IRS would reject the offer, and any firm that charged you thousands to file it knew the math going in.

For this couple, the winning sequence is abatement first, then a payment plan — total cost far below what an "OIC mill" would charge just in fees. That's the pattern for most balances in this range.

How to get real IRS forgiveness, step by step

- Pull your real numbers. Log into your IRS online account and get your balance by tax year, split into tax, penalties, and interest. Every good decision starts from these figures, not from an advertiser's estimate.

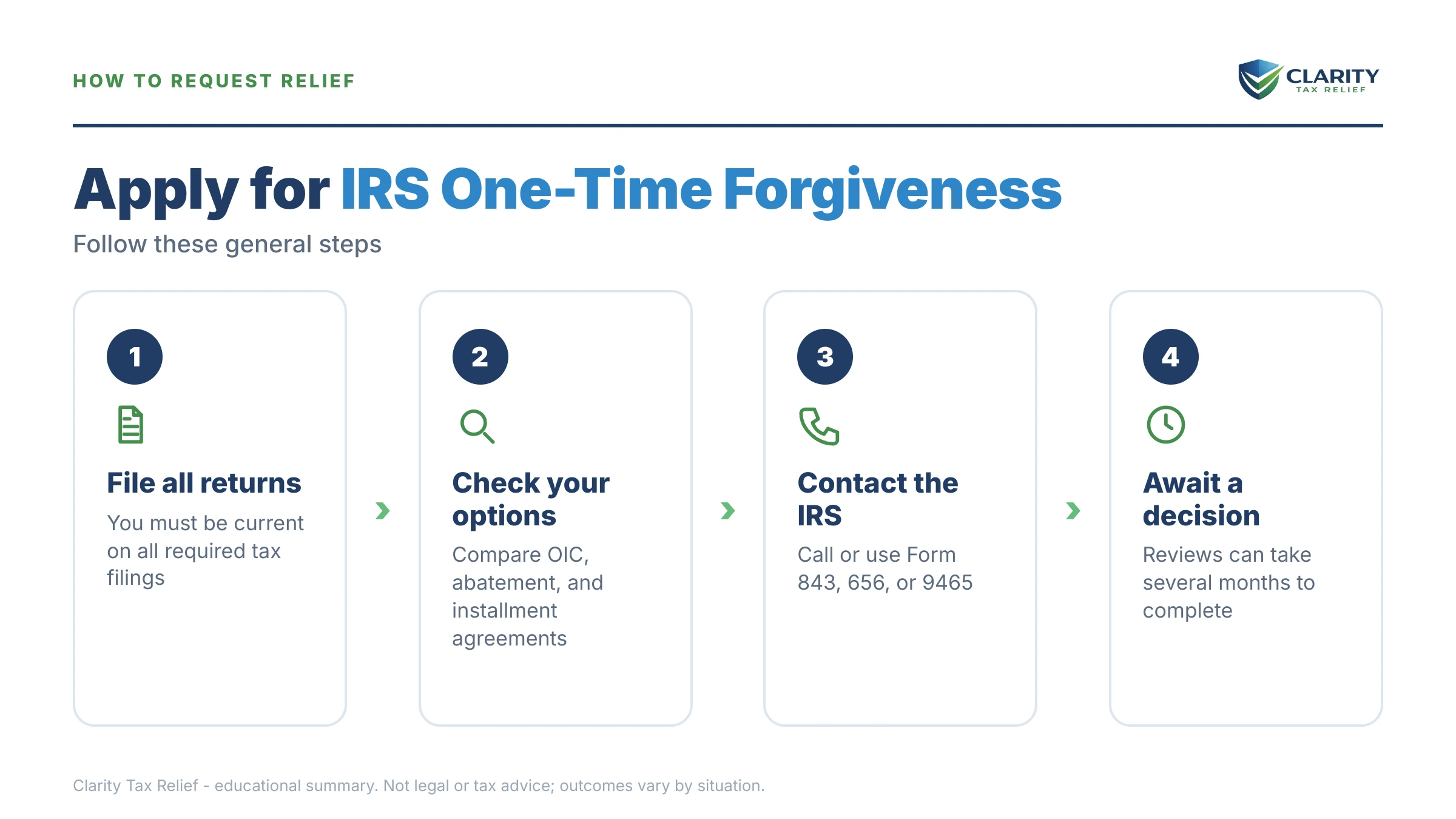

- Request penalty relief first. If your prior three years were penalty-free, ask for First-Time Penalty Abatement by calling the number on your notice or filing Form 843. From summer 2026, the Automatic Exemption from Penalty applies this relief automatically for eligible taxpayers.

- Match your finances to one program. Balances up to $50,000 can go on a payment plan online for up to 72 months. If allowable expenses consume your income, ask about Currently Not Collectible status. Consider an Offer in Compromise only if your assets and income genuinely can't cover the debt.

- Set it up before the notice sequence escalates. An arrangement you start today stops the march toward levy. Waiting for a forgiveness program that doesn't exist only adds monthly penalties and daily interest.

- Vet anyone promising forgiveness. Before paying any company, ask which specific IRS program they'd pursue, what their fee covers in writing, and who will actually work your case. Walk away from anyone who promises a result before reviewing your finances.

When you can handle this yourself — and when the myth costs you money

Most people searching for one-time tax forgiveness can resolve their balance without paying anyone. You likely don't need professional help if:

- You can pay the full balance within 180 days — a short-term plan costs $0 to set up and stops the notice sequence cold.

- Your balance is under $50,000, you agree with it, and you just need a monthly plan — the online application takes minutes.

- Your only issue is penalties after a clean three-year history — FTA is a phone call, and AEP may already have handled it.

Experienced help changes outcomes in specific situations: a levy already in motion, multiple unfiled years that must be sequenced before any agreement, business or payroll tax debt where personal liability is in play, and Offer in Compromise math where valuation judgment calls swing the result by thousands. It also matters when you're being sold — the schemes we document in tax relief scams and offer in compromise mill all start with the word "forgiveness."

Terms the "forgiveness" ads use, decoded

- FTA (First-Time Abate): administrative removal of penalties after three clean compliance years — the real kernel inside "one-time forgiveness."

- AEP (Automatic Exemption from Penalty): the successor to FTA starting summer 2026, applied automatically with no request.

- OIC (Offer in Compromise): the only program that settles tax debt for less than you owe, based on documented finances.

- RCP (Reasonable Collection Potential): the IRS's formula — asset equity plus a multiple of monthly disposable income — that sets the minimum acceptable offer.

- CNC (Currently Not Collectible): hardship status that pauses collection without reducing the debt.

- CSED (Collection Statute Expiration Date): the date, 10 years after assessment, when unpaid debt legally expires — subject to pauses.

IRS one-time forgiveness questions, answered

Is the IRS one-time forgiveness program real?

No IRS program is named "one-time forgiveness" — the phrase is advertising shorthand used by tax-relief marketers. The real relief behind it lives in First-Time Penalty Abatement, Offers in Compromise, payment plans, and Currently Not Collectible status, each with its own means test. If a company says you're "pre-approved for one-time forgiveness" before seeing your IRS records, they're guessing — nobody can know that without your file.

How do I qualify for IRS one-time forgiveness?

You qualify for the specific programs behind the phrase, not the phrase itself. You may qualify for First-Time Penalty Abatement if you had no penalties in the prior three years; for an Offer in Compromise if your income and assets genuinely can't cover the full debt; and for hardship status if IRS allowable expenses consume your income. Each is decided on your documented finances — never on a sales call.

Does the IRS ever forgive tax debt completely?

Yes, in two narrow ways: an accepted Offer in Compromise wipes the remaining balance once you pay the offer amount, and any debt still unpaid when the 10-year collection statute expires goes away. Neither is easy — the IRS accepted roughly 1 in 5 offers in FY2024, and the 10-year clock pauses during appeals, a pending offer, or bankruptcy, so it often runs longer than 10 calendar years.

How much will the IRS settle for in an offer in compromise?

The IRS settles for your Reasonable Collection Potential — the equity in what you own plus a multiple of your monthly disposable income — not a percentage of the debt. Two couples owing the same $11,300 can get completely different answers depending on home equity, cars, and cash flow. Anyone quoting a settlement percentage before reviewing your financials is guessing, and that's a red flag.

What is first-time penalty abatement — and is it really one-time?

First-Time Penalty Abatement removes failure-to-file, failure-to-pay, and failure-to-deposit penalties if you had no penalties in the prior three tax years — and despite the name, it isn't strictly one-time. You can qualify again after another three penalty-free years — provided you've also filed all required returns and paid, or arranged to pay, what you owe at the time you ask. It removes penalties and the interest charged on them, never the underlying tax. Starting summer 2026, the IRS is replacing FTA with the Automatic Exemption from Penalty, which applies automatically with no request needed.

Does IRS tax debt go away after 10 years?

Unpaid IRS debt generally expires 10 years from the date it was assessed — that's the Collection Statute Expiration Date. But the clock pauses while an appeal, Offer in Compromise, or bankruptcy is pending, so the real window is often longer. The IRS also tends to collect harder as the date approaches, so waiting it out is rarely a plan; it's usually a decade of liens, levies, and offset refunds.

Can I go to jail if I can't pay the IRS?

No — owing taxes you honestly reported is a civil matter, not a crime. Criminal exposure requires willful conduct like tax evasion, filing a fraudulent return, or deliberately refusing to file for years. If you filed truthfully and simply can't pay, the worst-case tools are financial: liens, levies, and garnishment — all of which have documented defenses and payment alternatives.

Is "settle your tax debt for pennies on the dollar" a scam?

The phrase itself is a warning sign — regulators have shut down tax-relief firms for making exactly these promises. Real settlements exist through the Offer in Compromise, but the amount is set by IRS financial math, not by a company's promise, and roughly 1 in 5 offers were accepted in FY2024. A legitimate firm names the specific program, states its fee in writing, and never promises a result before analyzing your finances.

Your next 24 hours

- Find your real balance. Log into your IRS online account (or grab your most recent notice) and write down three numbers for each year: tax, penalties, interest. The penalty line is your abatement target.

- Gather three documents: your last filed return, your latest IRS notice, and a rough monthly income-and-expenses picture for your household. That's everything needed to match you to a real program.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form — an experienced tax professional will name the specific program your numbers support, before another month of penalties and interest posts to your account.

The primary sources, if you want to verify anything on this page yourself: the IRS's own pages on payment plans and installment agreements and the Offer in Compromise, plus the independent Taxpayer Advocate Service — none of them mention a "one-time forgiveness" program, because it doesn't exist.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.