Tax Debt Basics

Tax Resolution Terms Glossary: Every IRS Term in Plain English (2026)

The short answer: tax resolution is the process of settling an IRS debt through an official program — a payment plan, an Offer in Compromise, hardship status, or penalty relief. This tax resolution terms glossary defines every term on your notices and transcripts in plain English, with the 2026 numbers and thresholds that actually apply.

You just spent forty minutes on hold, and the notes you scribbled say CSED, CDP, 433-F, RCP — none of which the agent slowed down to explain. Or you're holding a letter that says "levy" and you're not sure if that means your bank account is already gone. It isn't the words that put you in danger; it's acting late because you didn't know what they meant. Every term below gets one plain-English definition, and where a number matters — a threshold, a percentage, a day count — you get the 2026 figure.

⏱ The real clock: a glossary has no response deadline — but your balance does. The failure-to-pay penalty adds 0.5% every month and interest compounds daily while a debt sits unresolved, so every term you decode here is worth acting on this week, not next quarter.

Why the IRS speaks in codes — and why one glossary isn't enough without numbers

The IRS uses at least four separate vocabularies, and they overlap on your paperwork. Notice numbers (CP14, LT11) identify the letter you received. Form numbers (433-F, 656) identify the paperwork you file back. Program names (installment agreement, Offer in Compromise) identify how the debt gets resolved. And legal terms (assessment, statute, lien) identify what the IRS can and can't do to you.

Most glossaries define the words and stop. That's not enough, because nearly every term in tax resolution comes attached to a number — a dollar threshold, a monthly percentage, or a day count — and the number is what decides your options. So this page pairs each definition with its 2026 figure. For the full walkthrough of how to actually apply these programs on your own, the companion guide on how to settle tax debt yourself goes step by step; this page is the dictionary you'll keep open next to it.

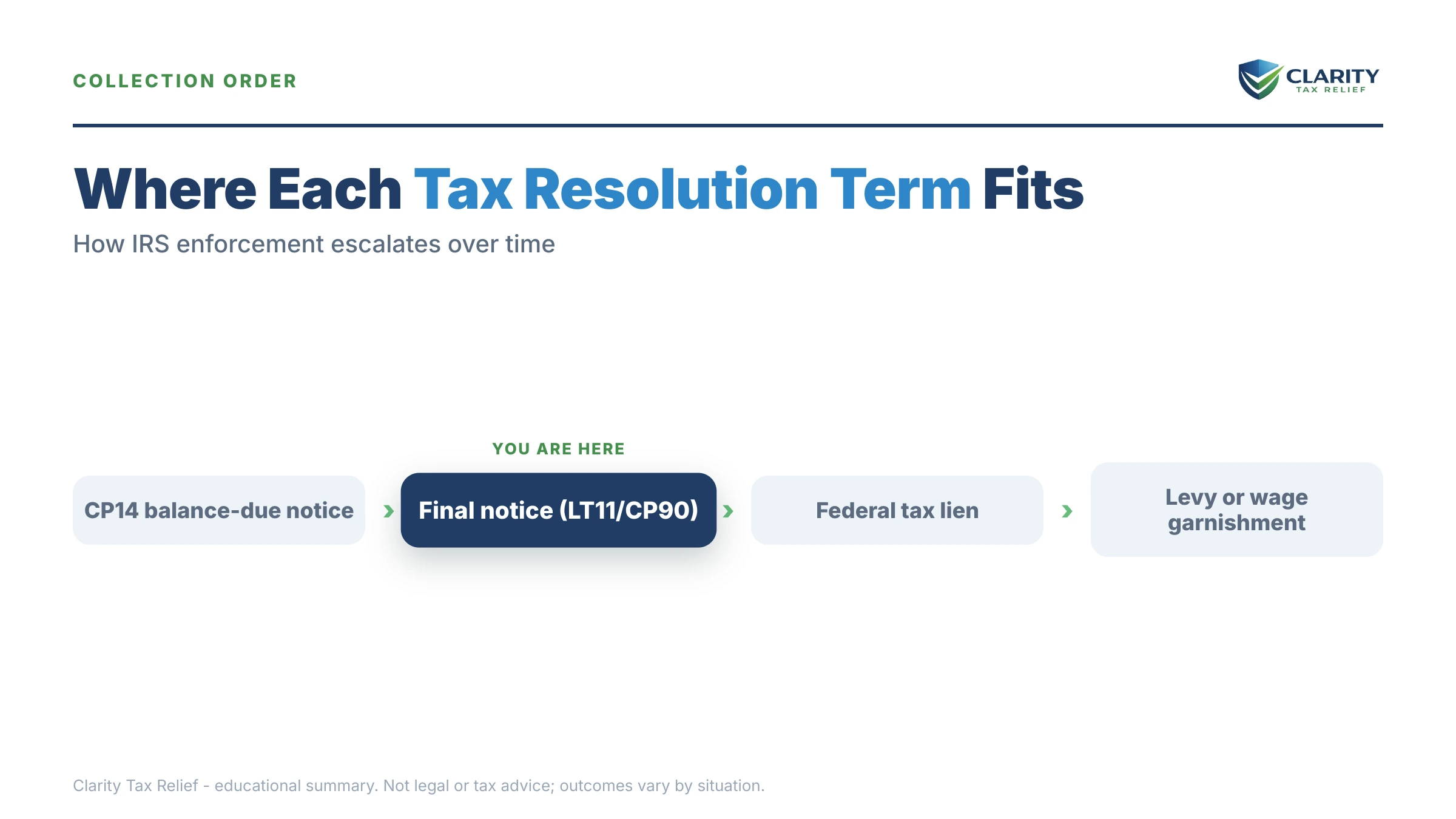

The collection sequence, term by term: what each notice name means

IRS collection notices arrive in a fixed, automated order, and each notice name marks a stage with more enforcement power than the last. Here is the sequence decoded, from first bill to seizure:

- CP14 — first bill. "CP" means computer paragraph: an automated notice. A CP14 says a return posted with a balance due; you typically have about 21 days before the next notice queues up (10 business days when the balance is $100,000 or more). No enforcement yet.

- CP501 / CP503 — reminder notices. Still just bills. The only thing changing is the balance, which grows monthly with penalties and interest.

- CP504 — Notice of Intent to Levy. Despite the scary title, this notice authorizes the IRS to seize your state tax refund under IRC §6331(d). It is not the final notice — but it means the final one is next.

- LT11 / Letter 1058 — Final Notice of Intent to Levy. "LT" letters come from the Automated Collection System; Letter 1058 is the revenue-officer version of the same thing. Either one starts a 30-day clock, after which the IRS can levy wages and bank accounts. This notice also triggers your Collection Due Process rights (defined below).

- Levy — the taking. A bank levy freezes funds for 21 days before they're sent to the Treasury; a wage levy repeats every payday until released.

Two more terms live inside this sequence. ACS (Automated Collection System) is the computer-and-call-center machinery that runs most cases — nobody at the IRS is personally "handling" your file at this stage. A revenue officer is the opposite: a human field collector assigned to larger or business cases, who can show up in person and demands direct answers. In 2026, with the IRS workforce down roughly 27% after the 2025 cuts, humans are scarcer than ever — but ACS keeps issuing levies on schedule, because the automation was never laid off.

Drowning in terms on a notice you're holding right now?

Skip the dictionary work. Send us the notice and an experienced tax professional will decode exactly which stage you're at and which program fits your numbers — free and confidential, before the next automated notice adds another month of penalties and interest.

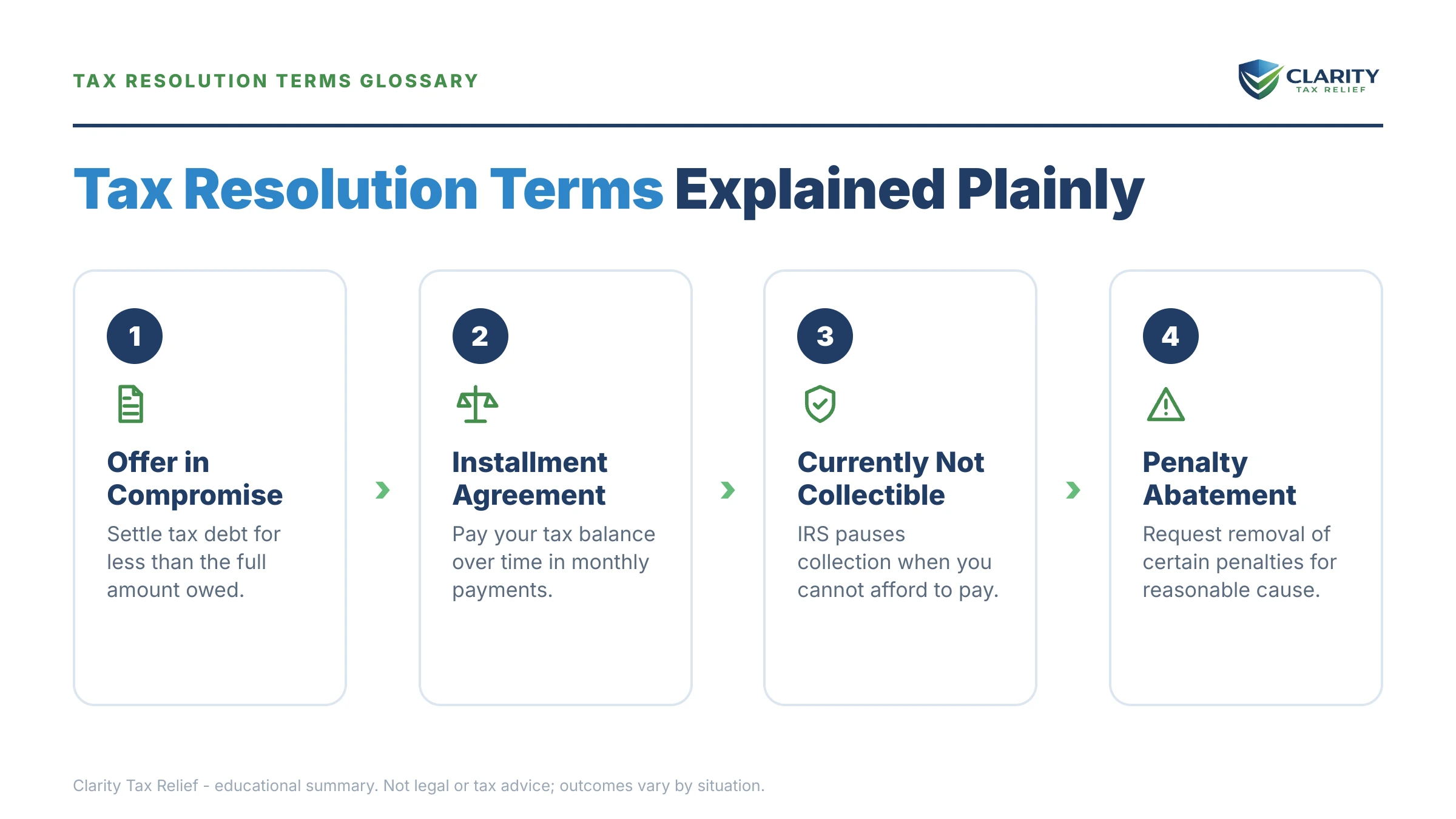

Resolution program terms — and who qualifies for each

Every legitimate tax resolution outcome is one of five things: pay in full, pay over time, settle for less, pause collection, or reduce penalties. The terms below are the official names for those five paths.

Installment agreement (IA)

The formal name for an IRS monthly payment plan. Interest and the failure-to-pay penalty keep accruing during the plan (the penalty rate drops while an IA is in effect), so a plan costs more than paying today — but it stops levies. Sub-types matter, because each has its own threshold:

- Short-term payment plan: full payment within 180 days, $0 setup fee, no monthly commitment.

- Guaranteed installment agreement: the IRS must accept it if you owe $10,000 or less in tax, are filing-compliant, and can full-pay within three years. (This is the official program name — the only place "guaranteed" honestly appears in tax resolution.)

- Streamlined installment agreement: balances up to $50,000, up to 72 months, set up online with no financial disclosure.

- Non-streamlined IA: above $50,000 — the IRS requires a financial statement (Form 433 series) before agreeing to terms.

- Partial-pay installment agreement (PPIA): monthly payments that won't full-pay the debt before the collection statute expires; the IRS accepts what your finances allow and reviews you periodically.

Offer in Compromise (OIC)

The program that lets you settle a tax debt for less than the full balance — real, but strictly means-tested. The application (Form 656) costs $205 plus a 20% down payment on lump-sum offers, both waived if your AGI is at or below 250% of the federal poverty level (called low-income certification). The IRS accepted roughly 1 in 5 offers in FY2024, so treat any pitch that makes an offer sound routine as a red flag. How the whole process runs is covered in how an offer in compromise actually works.

Reasonable Collection Potential (RCP) is the term that decides everything: your net asset equity plus 12 months of monthly disposable income (24 for periodic offers). If RCP is below your balance, an offer is viable; if not, it will be rejected regardless of wording — the full math is in our guide to reasonable collection potential, and you can estimate your own figure with our Offer in Compromise Calculator.

Three offer grounds have their own names: doubt as to collectibility (you can't pay — the common one), doubt as to liability (you don't actually owe it — sometimes better handled by amending a return to lower a tax debt), and effective tax administration (you could technically pay, but collection would be unfair or create hardship). One quiet rule worth knowing: if the IRS doesn't decide your offer within 2 years, it's automatically accepted — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count.

Currently Not Collectible (CNC)

A hardship status — the IRS marks your account uncollectible (transcript code 530) and stops levies because your allowable expenses meet or exceed your income. The debt remains, interest accrues, and refunds get kept, but garnishment stops and the 10-year collection clock keeps running toward expiration. Details and the qualification test are in our guide to Currently Not Collectible status.

Penalty abatement, FTA, and AEP

Abatement means removal — of penalties, not tax. First-Time Abatement (FTA) wipes failure-to-file and failure-to-pay penalties for one year if your prior three years were clean; the request path is in our first-time penalty abatement guide. Starting summer 2026, FTA is being replaced by the Automatic Exemption from Penalty (AEP) — the same relief applied automatically, with no request needed (see automatic exemption from penalty AEP 2026). Reasonable cause is the other relief path: penalties removed because circumstances beyond your control — serious illness, disaster, records destroyed — caused the noncompliance. The refund-or-abatement request form is Form 843.

| Program term | Key 2026 threshold | Cost / catch |

|---|---|---|

| Short-term payment plan | Full pay within 180 days | $0 setup; interest and penalties continue |

| Guaranteed installment agreement | ≤ $10,000 in tax; full pay in 3 years | IRS must accept if you're filing-compliant |

| Streamlined installment agreement | ≤ $50,000 total | Up to 72 months, online, no financial statement |

| Non-streamlined IA / PPIA | Above $50,000, or can't full-pay by CSED | Form 433 financials required; periodic review |

| Offer in Compromise | RCP below your balance | $205 fee + 20% down (both waived if AGI ≤ 250% of poverty); ~1 in 5 accepted FY2024 |

| Currently Not Collectible | Allowable expenses ≥ income | Collection pauses; debt and interest remain |

| First-Time Abatement / AEP | Clean prior 3 years | Removes penalties only, not tax; AEP is automatic from summer 2026 |

Enforcement terms: lien, levy, garnishment, and the passport rule

A lien is a claim; a levy is a taking — that one distinction resolves most of the confusion on IRS collection letters.

- Federal tax lien: the government's automatic legal claim on everything you own once a debt is assessed and unpaid. A Notice of Federal Tax Lien (NFTL) is the public recording of that claim, which complicates selling or refinancing property. The side-by-side comparison lives in lien vs. levy: the difference.

- Levy: the actual seizure of money or property. A bank levy freezes the account balance for 21 days — your one window to get it released — before funds transfer. A wage levy (garnishment) is continuous: it repeats every payday until released or the debt is resolved.

- Federal Payment Levy Program (FPLP): the automated system that takes up to 15% of Social Security benefits and other federal payments, continuously.

- Seriously delinquent tax debt: the legal label that triggers passport certification. In 2026 the threshold is $66,000; once certified (notice CP508C), the State Department can deny or revoke your passport until you resolve the debt or enter an agreement.

- Seizure: the physical taking of property — vehicles, equipment, real estate. Rare, procedurally heavy, and reserved for the far end of enforcement.

Deadline and rights terms: CSED, CDP, and the 90-day letter

The IRS's power to collect a tax debt generally expires 10 years after assessment — a date called the CSED.

- Assessment: the official recording of a tax debt on the IRS's books. Nothing in collections — not the notices, not the 10-year clock — starts until assessment happens.

- CSED (Collection Statute Expiration Date): the day collection authority ends, 10 years from assessment, one date per tax year. The full rules are in the 10-year collection statute (CSED).

- Tolling: pausing that clock. An OIC under review, a bankruptcy, or a CDP hearing all stop the CSED from running — which is why "the debt disappears in 10 years" is only half true. See what pauses the 10-year clock.

- CDP (Collection Due Process) hearing: your statutory right to an independent Appeals review after a final levy notice or a lien filing — requested on Form 12153 within 30 days. A timely request generally stops levy action while pending and preserves Tax Court review; the walkthrough is in our CDP hearing / Form 12153 guide. Note the tradeoff: a CDP request tolls your CSED.

- Equivalent hearing: the consolation version — request Appeals review after the 30-day CDP window closes (within one year), but without levy protection or Tax Court rights.

- CAP (Collection Appeals Program): a faster, narrower appeal of a specific collection action (a levy, a lien filing, an IA rejection). Quick decisions, but no court review afterward.

- Statutory Notice of Deficiency (the "90-day letter"): the letter that proposes additional tax and gives you 90 days to petition Tax Court before the tax is assessed — the last stop where you can dispute without paying first. See the 90-day letter & Tax Court petition basics.

- Taxpayer Advocate Service (TAS): the independent organization inside the IRS that intervenes when normal channels fail or enforcement causes hardship — reachable through taxpayeradvocate.irs.gov.

The forms behind the acronyms

Six form numbers cover almost every resolution filing, and knowing which is which saves real time on the phone.

- Form 9465 — Installment Agreement Request: the paper route to a payment plan (most people now apply online instead).

- Form 433-F — Collection Information Statement: the short financial disclosure ACS uses for payment plans above the streamlined threshold and for CNC. Line-by-line help: Form 433-F walkthrough.

- Form 433-A / 433-A(OIC) — the long-form financial statement used by revenue officers and required with every Offer in Compromise.

- Form 656 — the Offer in Compromise application itself, where you state your offer amount and grounds.

- Form 12153 — the CDP hearing request, due within 30 days of a final levy notice or lien filing.

- Form 843 — Claim for Refund and Request for Abatement: the penalty-relief and interest-abatement request form.

- Form 2848 — Power of Attorney: the form that lets an experienced tax professional speak to the IRS for you, so you never have to sit on hold again.

Penalty terms and the percentages behind them

The failure-to-file penalty runs 5% per month — ten times the 0.5% monthly failure-to-pay penalty — which is why filing on time matters even when you can't pay a dollar.

- Failure-to-file (FTF): 5% of the unpaid tax per month, capped at 25%.

- Failure-to-pay (FTP): 0.5% per month, also capped at 25% — smaller, but it runs for years and compounds with interest.

- Accuracy-related penalty: a flat 20% added when the IRS decides an understatement was negligent or substantial.

- Trust Fund Recovery Penalty (TFRP): the business-world heavyweight — when withheld payroll taxes go unpaid, the IRS can assess the "trust fund" portion personally against every responsible person. Full guide: Trust Fund Recovery Penalty.

- Statutory additions: the umbrella phrase on notices for penalties plus interest — everything stacked on top of the original tax.

- Underpayment penalty: the estimated-tax penalty charged when a self-employed filer doesn't pay quarterly — the reason so many 1099 earners meet this glossary in the first place.

The glossary in action: a 1099 contractor who owes $83,100

Say you're a self-employed contractor who under-withheld for three years and now owes $83,100 across those years. Watch how many of these terms immediately go to work — every figure here is hypothetical:

- Streamlined threshold: $83,100 is above the $50,000 ceiling, so no online 72-month plan on the full balance. Two paths: pay down $33,101 to get under $50,000 (then roughly $49,999 ÷ 72 ≈ $695/month before accruals), or file a Form 433-F for a non-streamlined agreement — full balance over 72 months is $83,100 ÷ 72 ≈ $1,154/month before interest.

- Passport certification: $83,100 exceeds the 2026 threshold of $66,000, so this debt qualifies as seriously delinquent — entering an installment agreement is what blocks the CP508C certification.

- RCP math: suppose net equity in a work truck and tools is $9,000 and disposable income after IRS allowable expenses is $500/month. Lump-sum RCP = $9,000 + ($500 × 12) = $15,000 — well below $83,100, so an Offer in Compromise is worth pricing. If disposable income were $2,000/month instead, RCP jumps to $9,000 + $24,000 = $33,000, and the analysis changes.

- Compliance: none of it sticks unless current-year quarterly estimated payments are being made — the IRS defaults agreements and returns offers when a new balance accrues mid-program.

Which terms matter at your balance: options by amount band

Your total balance — across all years, not one notice — is the single fact that filters this entire glossary down to the handful of terms that apply to you.

| Total balance | Realistic options | The term that matters most |

|---|---|---|

| Under $10,000 | Short-term plan; guaranteed installment agreement; FTA/AEP on penalties | Guaranteed installment agreement |

| $10,000–$25,000 | Streamlined IA online; penalty abatement; OIC only if genuine hardship | Streamlined installment agreement |

| $25,000–$50,000 | Streamlined IA (direct debit often required at the upper end); OIC or CNC if the math fits | Direct debit |

| $50,000–$100,000 | Non-streamlined IA with Form 433-F; PPIA; OIC; CNC — and passport risk above $66,000 | Seriously delinquent tax debt |

| Over $100,000 | Likely revenue-officer assignment; full 433-A financials; PPIA, OIC, lien management | Revenue officer |

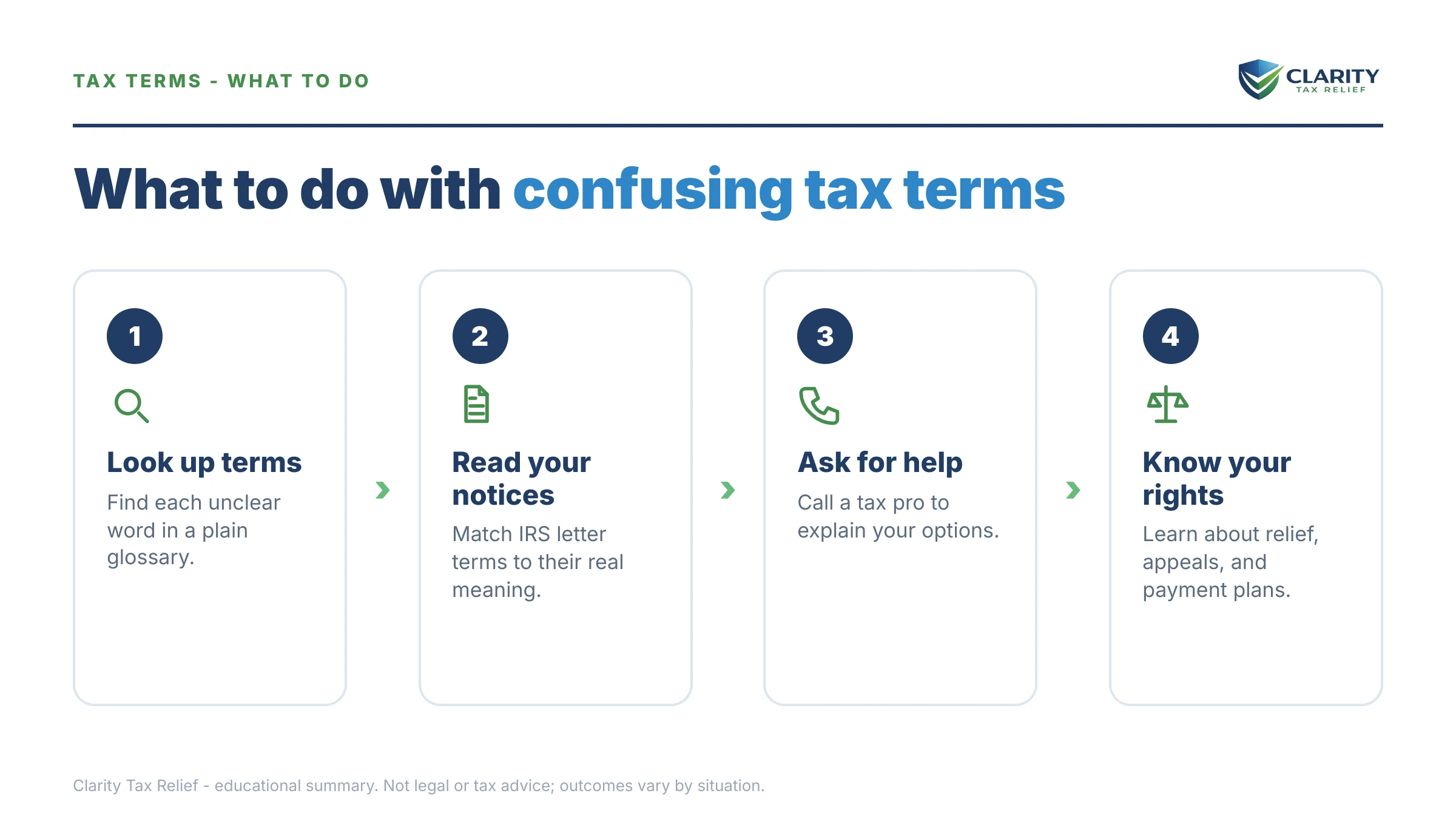

How to use this tax resolution terms glossary, step by step

- Find your notice number. Look at the top-right corner of your IRS letter — the code printed there (CP14, CP504, LT11) tells you exactly where you sit in the collection sequence above and how much time you realistically have.

- Pull your total balance. Log into your IRS online account or request account transcripts to see what you owe across all years — your total balance, not one notice's figure, determines which programs you can use.

- Match your balance to a program. Use the amount-band table above to shortlist the two or three programs your balance realistically fits, then check each program's eligibility threshold in the options table.

- Confirm you're filing-compliant. Every program requires all required returns filed — and for 1099 earners, current-year estimated payments made — so fix compliance before applying for anything.

- Set up your resolution or get a free review. Apply online for a payment plan if your numbers clearly fit, or have an experienced tax professional check your OIC or CNC math first — free at (888) 825-7779.

When you can handle this yourself — and when the vocabulary isn't the hard part

If you owe under $50,000, agree with the balance, and just need time, you don't need help — you need the streamlined installment agreement, and the IRS's own payment plans page can have it set up in an afternoon. Same for a first-time penalty on an otherwise clean record: FTA (or AEP from summer 2026) is yours to claim without paying anyone.

Experienced help changes outcomes when the terms start stacking: a levy already in motion against 1099 income, multiple unfiled years plus a balance, payroll or trust-fund exposure, or an Offer in Compromise where the RCP math decides between a $15,000 settlement and a rejection. The IRS publishes the OIC rules itself at irs.gov's Offer in Compromise page — the program is real; the judgment call is whether your numbers fit it before you spend a year finding out.

Tax resolution glossary questions, answered

What does tax resolution actually mean?

Tax resolution is the process of formally settling a tax debt through one of the government's established programs — a payment plan, an Offer in Compromise, Currently Not Collectible status, or penalty abatement. It is not a single program you apply for; it's the umbrella term for choosing and securing the option your finances qualify for. Marketing phrases like "tax forgiveness" and "Fresh Start" all describe these same underlying programs.

What is the difference between a tax lien and a tax levy?

A lien is a legal claim on what you own; a levy is the actual taking. A Notice of Federal Tax Lien attaches to your property and complicates selling or refinancing, but it doesn't move money. A levy does: a bank levy freezes funds for 21 days before they're sent to the IRS, and a wage levy takes part of every paycheck continuously until it's released.

What does CSED mean on my IRS account?

CSED stands for Collection Statute Expiration Date — the day the IRS legally loses the right to collect a tax debt, generally 10 years after the tax was assessed. The catch is tolling: an Offer in Compromise, a bankruptcy, or a Collection Due Process hearing pauses the clock while it's pending, so the real date is often later than year ten. Each tax year has its own CSED.

Is the IRS Fresh Start Program a real program?

Fresh Start was a real 2011–2012 IRS policy change that raised lien-filing thresholds and loosened payment plan rules — but it is not an application you can file today. Companies advertising "Fresh Start" enrollment are describing the standard programs in this glossary: installment agreements, Offers in Compromise, and Currently Not Collectible status. The programs are real; the branded shortcut is marketing.

What is Currently Not Collectible status?

Currently Not Collectible (CNC) is a hardship designation the IRS applies when your allowable living expenses meet or exceed your income, meaning any payment would leave you unable to cover basics. Levies and garnishments stop while you're in CNC. The debt doesn't disappear, though — interest keeps accruing, refunds are kept and applied to the balance, and the IRS periodically reviews your income. The 10-year collection clock keeps running.

What is Reasonable Collection Potential in an Offer in Compromise?

Reasonable Collection Potential (RCP) is the number the IRS calculates to decide your offer: your net equity in assets plus a multiple of your monthly disposable income — 12 months' worth for a lump-sum offer, 24 for a periodic-payment offer. If your RCP is below what you owe, an offer is viable; if it's above, the IRS will reject the offer no matter how it's written.

What is a CDP hearing and when can I request one?

A Collection Due Process (CDP) hearing is your right to an independent Appeals review after the IRS sends a final levy notice (LT11 or Letter 1058) or files a lien. You request it on Form 12153 within 30 days of the notice date. A timely request generally stops levy action while the hearing is pending and preserves your right to Tax Court review — but it also pauses the 10-year collection clock.

Your next 24 hours

- Find two things on your latest IRS letter: the notice number in the top-right corner and the total amount due — those two facts locate you in the collection sequence and the amount-band table above.

- Gather your paper: your most recent tax return, every IRS letter you've received, and — if you're a 1099 earner — the last three months of income deposits, so any program's math can be run immediately.

- Get the free case review: use the 2-minute form or call (888) 825-7779. There's no notice deadline on a glossary, but the failure-to-pay penalty and daily interest are compounding on your balance either way — decoding the terms today costs nothing; waiting does.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.