IRS Notices

CP504: How Long Before Levy? The Real 2026 Timeline

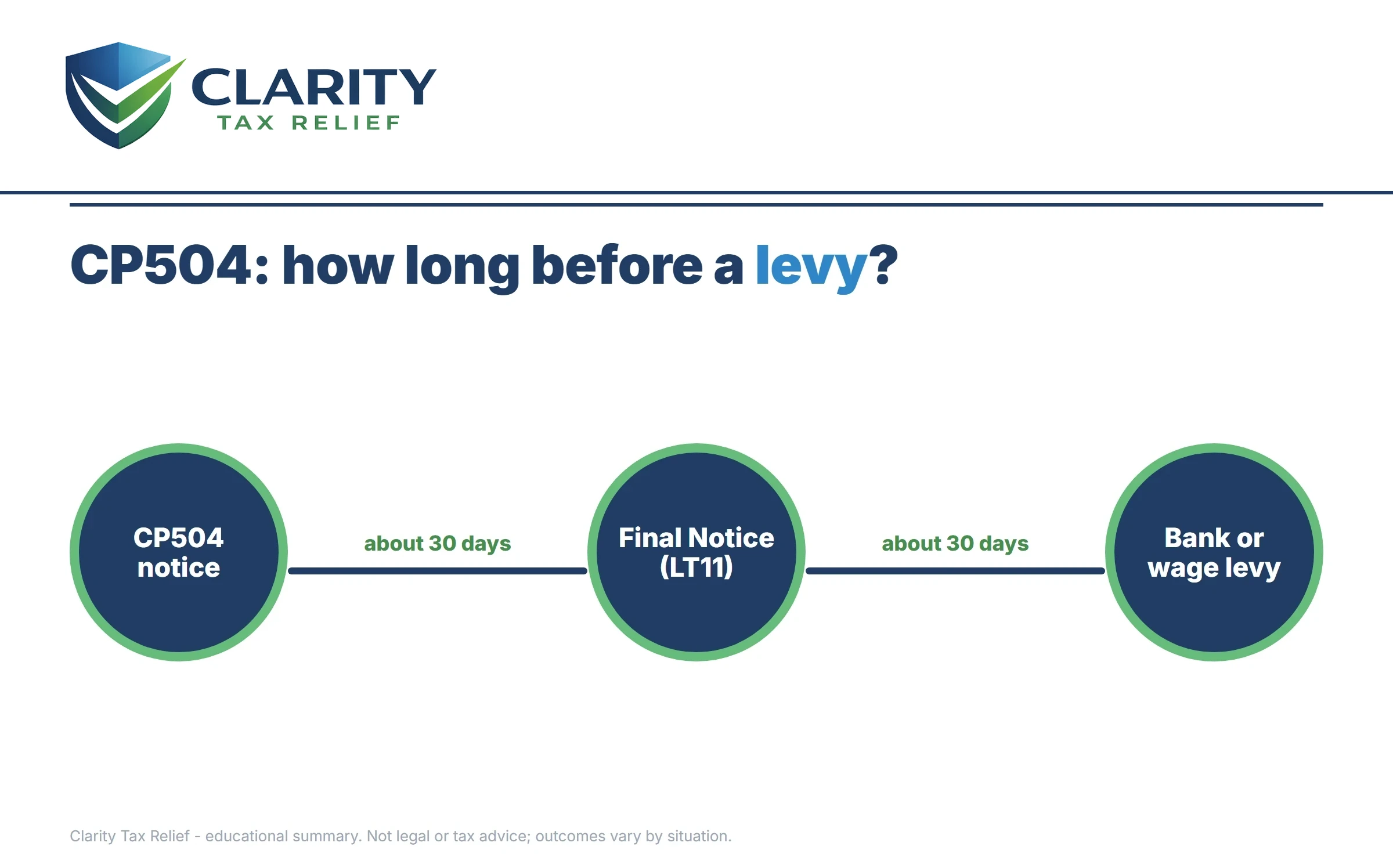

CP504 — how long before levy? After the deadline printed on the notice (typically 30 days), the IRS can seize your state tax refund — but it cannot levy your wages, bank account, or 1099 pay until it sends a final notice (LT11 or Letter 1058) and another 30 days pass.

You've read the CP504 twice looking for the line that says exactly when the seizing starts, and it never quite tells you. Here's what the notice buries: two separate clocks stand between you and an actual levy on your income, and only one of them has started. This page maps both, stage by stage, along with every move that stops them.

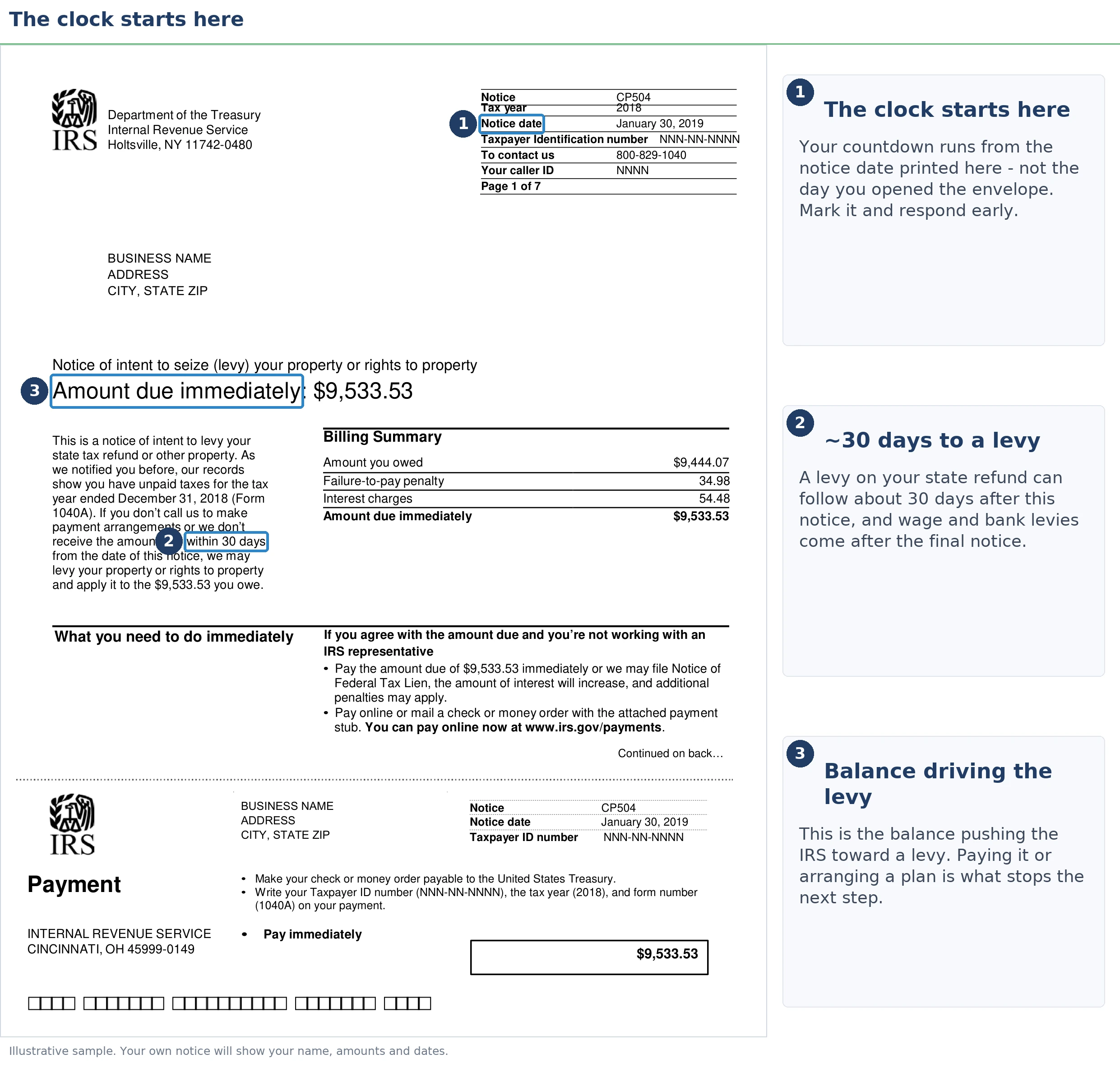

The image below shows exactly what a genuine CP504 looks like and where to find the two things that control everything else on this page — the notice date and the total amount due.

⏱ The clock that has started: You have until the deadline printed on your CP504 — typically 30 days from the notice date — before the IRS can seize your state tax refund and may file a federal tax lien. Wage and bank levies require a second letter (LT11 or Letter 1058) plus 30 more days — and there is no published schedule for when that letter goes out.

CP504: How Long Before Levy Actually Happens?

A CP504 lets the IRS seize your state tax refund after the 30-day deadline printed on the notice, but it cannot levy wages or bank accounts until it sends an LT11 or Letter 1058 and waits 30 more days, unless the IRS already sent you a final notice (LT11/Letter 1058) for those same tax periods in the past, or in rare cases like jeopardy levies.

That's the two-clock structure the notice's scary header hides. The CP504 satisfies the "notice and demand" requirement of IRC §6331(d). Legally, that unlocks exactly one seizure target once the printed deadline passes: money a state owes you, chiefly your state income tax refund. It also opens the door to a Notice of Federal Tax Lien.

Everything people actually fear — the paycheck garnishment, the drained checking account — requires a different letter. The LT11 notice (or its revenue-officer equivalent, Letter 1058) is the true final notice of intent to levy. Its date starts a fresh 30-day window during which you can demand a Collection Due Process hearing, and the IRS generally cannot levy your wages or accounts until that window closes.

How long between the CP504 and the LT11?

There is no published gap. In practice it can be a few weeks or a few months, because the LT11 is generated by the IRS's automated collection system in batches, not by a person reviewing your file. Two things make guessing dangerous in 2026: the system was never paused during the staffing cuts, and once the LT11 mails, your remaining time is fixed at 30 days no matter how long the gap before it was.

So the honest answer to "how long before levy" is: a minimum of roughly 60 days from your CP504 date for wages and bank accounts (30 on the CP504 plus 30 on the LT11 that follows), with your state refund exposed after the first 30 — and no guarantee the gap between the two letters gives you anything extra.

| Stage | What the IRS can legally do | Your move |

|---|---|---|

| CP504 arrives (day 0) | Nothing is seized yet — the notice demands payment and warns of what's next | Verify the balance; start a resolution now, at the cheapest point |

| Printed deadline passes (typically day 30) | State tax refund can be seized; federal tax lien may be filed; federal payments flagged for FPLP | Get a plan, hardship status, or offer in motion before this date |

| LT11 / Letter 1058 arrives (weeks to months later — no fixed schedule) | Final notice issued; your 30-day Collection Due Process window opens | File Form 12153 within 30 days to pause levy action |

| 30 days after the LT11 (if you did nothing) | Bank levy (21-day hold on funds), continuous wage levy, one-time levies on 1099 payments | Emergency release paths only — hardship, plan, or appeal |

Why you got a CP504 — and why "levy" is in the header

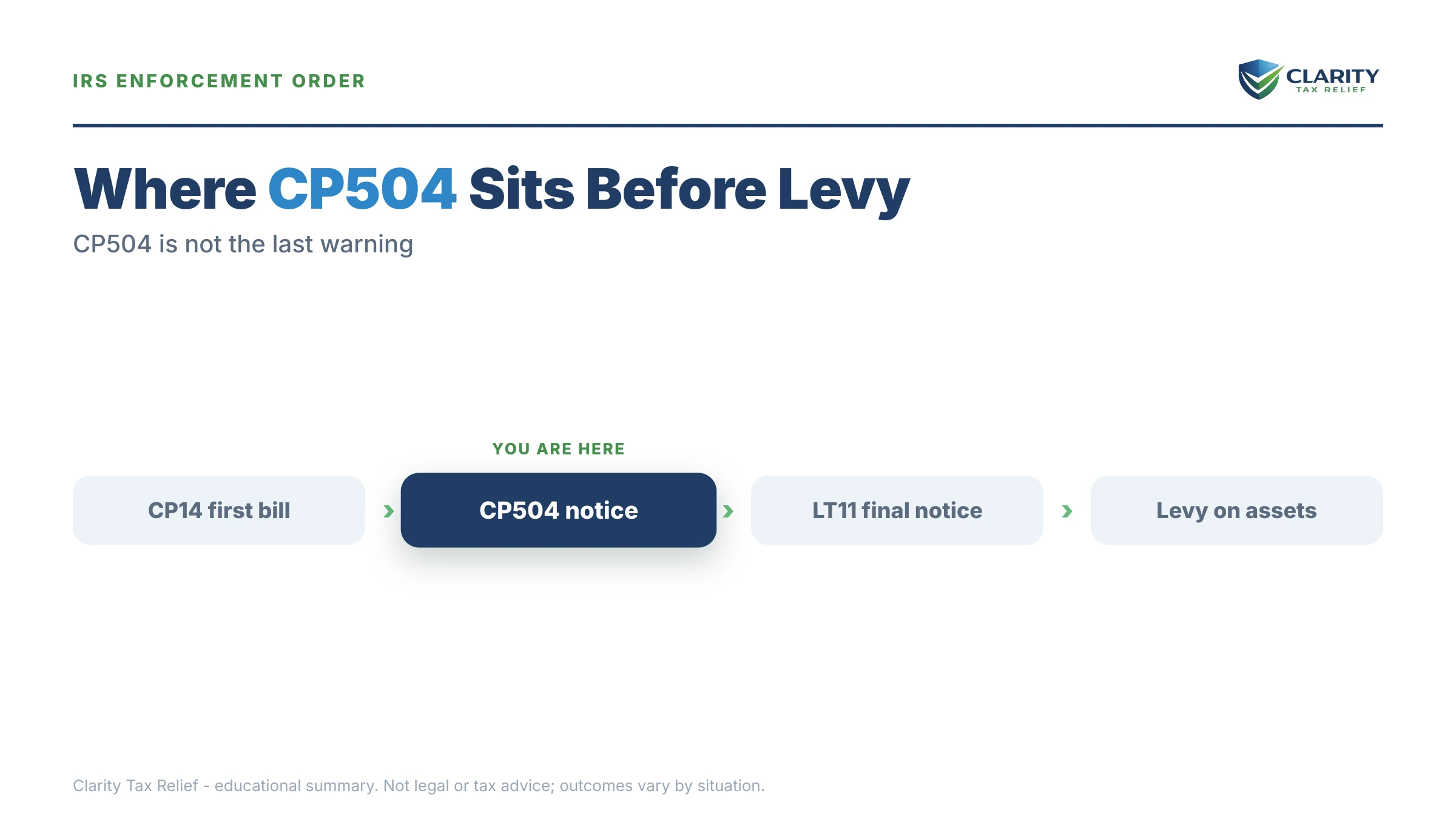

A CP504 means at least three earlier bills went unanswered — it is the fourth notice in the IRS collection sequence, not a first warning. The typical trail is CP14 (first bill), then CP501 and CP503 (reminders), then this. If you never saw the earlier ones, they likely went to an old address; the IRS mails to the last address on file and the clock runs either way. (For the general anatomy of IRS mail, see why did I get a letter from the IRS.)

The header — "Notice of intent to seize (levy) your property or rights to property" — is legally accurate but narrower than it reads. This letter is the statutory demand that must exist before any levy, which is why the intimidating language appears now. What it actually authorizes immediately is the state-refund seizure described above. Our full CP504 notice guide breaks down every box on the letter itself; this page stays focused on the question you asked — the timeline.

One detail that changes everything downstream: where the balance came from. If you filed and simply couldn't pay, the number is probably right. If you have unfiled years, the IRS may have created the balance itself through substitute-for-return (SFR) assessments — returns the IRS files for you using only the income reported by payers, with zero deductions. For self-employed and gig readers, an SFR balance is almost always inflated, and that matters enormously in the worked example below.

What happens if you ignore a CP504

Ignoring a CP504 doesn't pause anything — it hands the sequence to an automated system that escalates in a fixed order. Here is what follows, stage by stage:

- The printed deadline passes. The IRS can now take your state income tax refund; if it does, a CP92 notice arrives confirming the seizure. A Notice of Federal Tax Lien may be filed, becoming a public claim against everything you own.

- Federal payments get flagged. If you receive Social Security, up to 15% of each benefit payment can be taken through the Federal Payment Levy Program — the CP91 Social Security levy notice is the warning shot for that specific action.

- The LT11 or Letter 1058 mails. This is the real final notice. Its date starts a 30-day clock, and it carries your Collection Due Process rights — the strongest appeal right in the entire collection sequence, and one you lose if you let the window lapse.

- 30 days after the LT11: levies begin. A bank levy freezes what's in the account that day, with a 21-day hold before the money leaves. A wage levy is continuous — it repeats every payday until released. For contractors, the IRS can send one-time levies to companies that pay you, and a 1099 levy can capture an entire contract payment.

- Above $66,000, your passport enters the picture. Once the debt is certified as seriously delinquent — which generally requires the case to reach the lien or levy stage — the State Department can deny or revoke your passport for tax debt. The certification threshold is $66,000 in 2026.

If you're trying to picture the endpoint concretely: a continuous wage levy leaves you only an exempt amount based on your filing status and dependents — often far less than rent. You can estimate what a levy would leave you with using our IRS Wage Garnishment Calculator.

And a 2026-specific warning: the IRS workforce shrank roughly 27% in 2025, but none of the steps above involve a human. The notices, the refund seizure, the lien filing, and the levies are all machine-issued. Understaffing makes the IRS harder to call after a levy hits — it does not make the levy later.

Holding a CP504 with the deadline counting down?

Get your CP504 reviewed free before the 30-day deadline printed on it passes. An experienced tax professional will tell you exactly which clock you're on and which resolution fits your numbers — no pressure, no obligation.

Your options before the levy clock runs out

Every IRS resolution program is still fully available at the CP504 stage — the notice narrows your time, not your options. What actually limits you is your balance, your filing compliance, and your finances:

| Option | Eligibility & cost | Effect on the levy clock |

|---|---|---|

| Pay in full | Anyone; no fee at IRS.gov | Ends the sequence immediately |

| Short-term plan (up to 180 days) | Balance you can clear within 180 days; $0 setup | Stops escalation while active; interest and penalties continue |

| Streamlined installment agreement | $50,000 or less (with direct debit); up to 72 months; setup fee applies, reduced for direct debit | No levy while the agreement is pending or current |

| Non-streamlined installment agreement | Over $50,000; requires Form 433-F financial disclosure | Same protection, but approval takes negotiation and documentation |

| Currently Not Collectible | Paying would leave you unable to cover allowable living expenses; proven on Form 433-F | Collection paused; debt remains and interest accrues; lien still possible |

| Offer in Compromise | Means-tested; $205 fee and 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 | Levy action generally on hold while a processable offer is pending |

| Penalty relief (FTA / AEP) | Clean compliance in the prior 3 years for first-time abatement; the new Automatic Exemption from Penalty begins applying automatically in summer 2026 | Shrinks the balance; doesn't stop the clock by itself |

Three notes that matter more at the CP504 stage than the table can show. First, compliance comes before everything: the IRS will not approve a plan, hardship status, or offer while required returns are unfiled. Second, if your balance sits just above $50,000, an IRS payment plan over $50,000 is a different, slower animal than the streamlined version — sometimes paying the balance below the line (or reducing it by filing accurate returns) is the faster path. Third, be skeptical of anyone promising settlement: an offer in compromise is real but strictly means-tested, and Currently Not Collectible status pauses collection only for people who genuinely can't pay — neither is a discount program you simply sign up for.

A worked example: $68,500, gig income, three years unfiled

Say you owe $68,500 — a gig worker's CP504 total after three unfiled years, where the IRS built the balance through substitute-for-return assessments on the gross 1099 amounts. Every number below is hypothetical, but the mechanics are exactly how these cases work.

An SFR allows zero business deductions — no mileage, no phone, no supplies, no platform fees. For a driver or delivery worker whose mileage alone often erases a third of gross income, the SFR balance is almost always overstated. Suppose the real Schedule C returns, built from reconstructed mileage logs and bank records, support $21,700 less in tax, penalties, and interest across the three years:

$68,500 − $21,700 = $46,800 actual balance

That single move — filing the real returns — changes three things at once:

- Passport exposure disappears. $68,500 is above the 2026 certification threshold of $66,000; $46,800 is comfortably below it.

- The streamlined door opens. $46,800 is under $50,000, so a direct-debit installment agreement over up to 72 months becomes available without full financial disclosure: $46,800 ÷ 72 ≈ $650 per month, with interest and the failure-to-pay penalty continuing to accrue on the shrinking balance — so paying more than the minimum shortens the real cost.

- Compliance is restored, which is required before the IRS will approve any agreement in the first place.

Now compare doing nothing. At $68,500, the failure-to-pay penalty of 0.5% per month adds roughly $342 every month (0.005 × $68,500 = $342.50) on top of daily-compounding interest — and the levy that eventually lands on a contractor doesn't take a percentage of a paycheck; a 1099 levy can capture 100% of a contract payment owed to you on the day it hits. If your situation looks like this reader's, start with the returns: our guide to what happens when you haven't filed taxes in 3 years walks through reconstructing income records year by year.

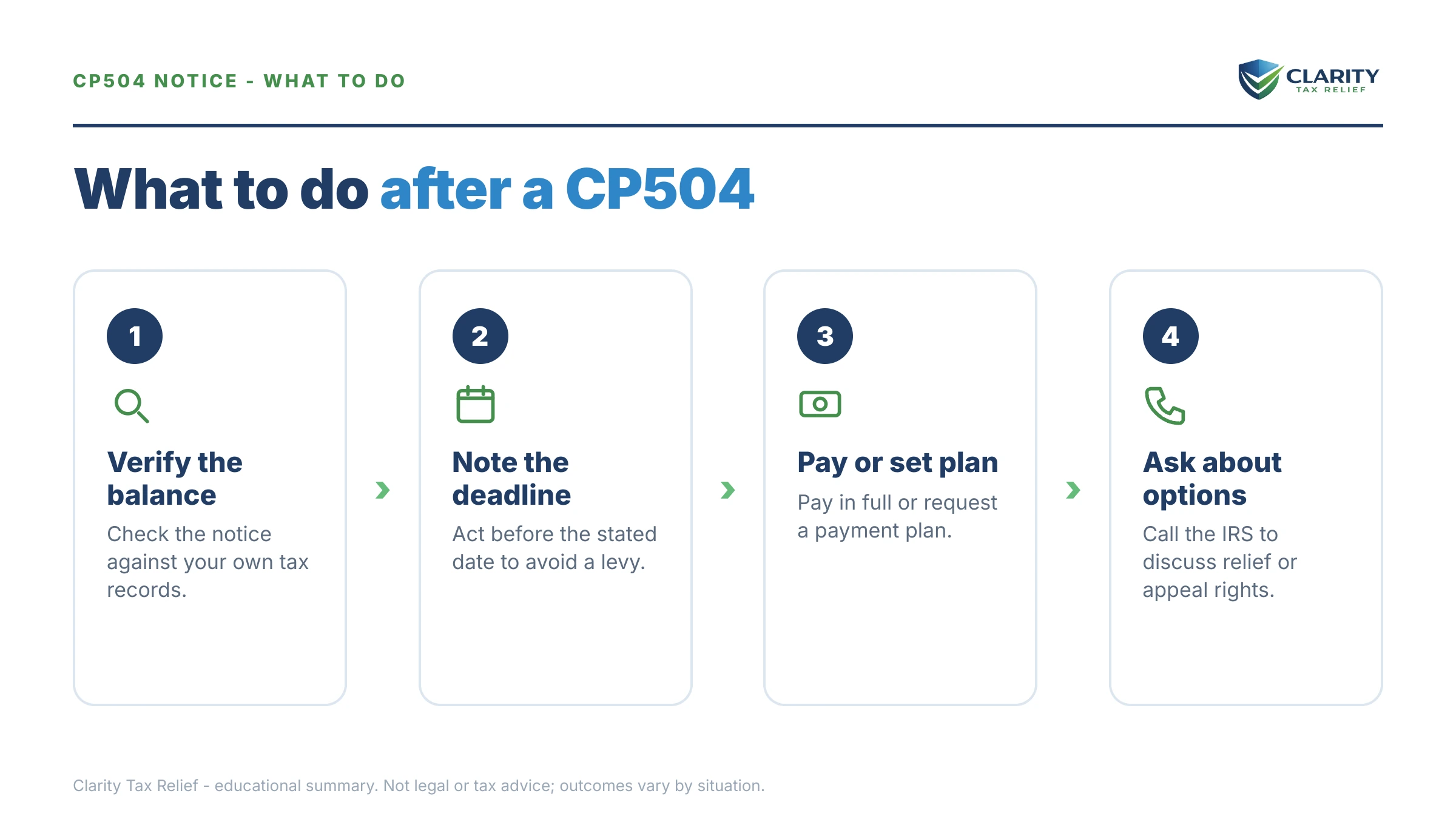

How to respond to a CP504, step by step

- Find the notice date and deadline. Locate the date in the top corner of your CP504 and the pay-by date, then verify the balance against your IRS online account before you pay anything.

- File every unfiled return. The IRS will not approve a payment plan, hardship status, or offer while required returns are missing — and filing real returns can shrink a balance built from substitute assessments.

- Start a resolution before the deadline passes. Set up a payment plan, submit hardship financials, or begin an offer — a resolution in place stops the automated march toward levy.

- Watch the mail for an LT11 or Letter 1058. That letter — not the CP504 — is the true final notice, and the date printed on it starts the 30-day clock that ends in wage and bank levies.

- Request a CDP hearing within 30 days if the LT11 arrives. File Form 12153 before that deadline to pause levy action and put your case in front of the IRS Independent Office of Appeals.

Step 5 deserves emphasis because it is the one right people forfeit without knowing it existed. A timely Form 12153 CDP hearing request generally suspends levy action on those periods while Appeals considers your case — and it preserves your right to take a disputed decision to Tax Court.

How close is the levy really? Check your transcript

Your IRS account transcript shows collection status in coded entries — and it often reveals where you are in the sequence more precisely than the mail does. Pull it free through your IRS online account, then scan the transaction codes on the account transcript for the years on your CP504:

| Code | What it means | What to do |

|---|---|---|

| 971 | A notice was issued — the CP504 and any LT11 each leave a 971 entry with a date | Match the dates to your mail; a recent 971 you never received may be the LT11 clock already running |

| 582 | A federal tax lien has been filed against you | The case has escalated past warnings — get a resolution in place before levy follows |

| 530 | Account placed in Currently Not Collectible (hardship) status | Collection is paused; keep filing on time so the status holds |

| 480 | An offer in compromise is pending | Levy action is generally on hold while the IRS reviews the offer |

| 520 | Bankruptcy or litigation freeze on the account | Collection is legally stayed — but the freeze also pauses the 10-year collection clock |

The single most useful check: a 971 entry dated after your CP504 that doesn't match any letter you've seen. If you moved and the LT11 went to an old address, the 30-day window runs anyway — the transcript is how you catch it in time.

When you can handle a CP504 yourself — and when help changes the outcome

Plenty of CP504 cases need no professional at all. If you agree with the balance, every return is filed, and the amount is under $50,000, you can set up a streamlined payment plan online in an afternoon and the levy sequence ends there. If you can pay in full within 180 days, the short-term plan costs nothing to set up. Those readers should simply act before the printed deadline and keep the confirmation.

Experienced help earns its cost in a narrower set of situations: a balance over $50,000 (where financial disclosure gets negotiated, not just submitted), multiple unfiled years with SFR assessments (where the balance itself is probably wrong), an LT11 that has already arrived (where the CDP request must be done right the first time), a levy already in motion, business or payroll tax debt, offer-in-compromise math, or passport-certification exposure above $66,000. In those cases, the difference between an average outcome and a good one is usually the order of operations — returns first, penalties second, balance last — and the deadlines don't wait while you learn the sequence.

If your CP504 sits on top of unfiled years or a balance above $50,000, a free case review before the printed deadline is the cheapest step in the whole process.

Terms on your CP504, decoded

- Levy — the actual seizure of money or property: a bank account, a paycheck, a state refund.

- Lien — a public legal claim securing the debt against everything you own; it takes nothing directly but attaches to your property.

- Notice of intent to levy (IRC §6331(d)) — the statutory demand the CP504 satisfies; on its own it unlocks state-refund seizure, not wage or bank levies.

- Final notice / CDP rights — the LT11 or Letter 1058, which starts a 30-day window to request a Collection Due Process hearing before broader levies begin.

- FPLP — the Federal Payment Levy Program, an automated levy of up to 15% of federal payments such as Social Security benefits.

- CSED — the Collection Statute Expiration Date: the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

CP504 levy timeline questions, answered

How long after a CP504 does the IRS actually levy?

Two clocks control it. Thirty days after the CP504 date, the IRS can seize your state tax refund and may file a federal tax lien. Wages and bank accounts can only be levied after the IRS also sends an LT11 or Letter 1058 and another 30 days pass — a gap with no published schedule that can run from weeks to months. Never plan around the gap running long.

Can the IRS take money from my bank account after a CP504?

Not yet. A bank levy requires the true final notice — LT11 or Letter 1058 — plus a 30-day waiting period that comes with Collection Due Process appeal rights. If a bank levy does eventually land, the bank holds the funds for 21 days before sending them to the IRS, and that hold is your last realistic window to get the levy released.

Is a CP504 a final notice of intent to levy?

No, despite the alarming header. A CP504 satisfies the notice-and-demand requirement of IRC Section 6331(d) and authorizes seizure of your state tax refund, but the actual final notice is the LT11 or Letter 1058, which starts your 30-day right to a Collection Due Process hearing. Treat the CP504 as your last inexpensive chance to resolve the balance voluntarily.

What can the IRS take right after the CP504 deadline passes?

Your state tax refund is the main target — if it is taken, a CP92 confirms the seizure. The IRS may also file a Notice of Federal Tax Lien, and Social Security recipients can see up to 15% of benefits taken through the Federal Payment Levy Program after a CP91. Wages, bank accounts, and 1099 pay still require the LT11 or Letter 1058 first.

Can I still set up a payment plan after getting a CP504?

Yes — a CP504 does not disqualify you from any resolution program. Balances of $50,000 or less can generally be set up online over as many as 72 months; above $50,000 you will need to disclose finances on Form 433-F or pay the balance below that line first. The catch most people miss: every required return must be filed before the IRS will approve any agreement.

Will a CP504 lead to a tax lien?

It can. The CP504 warns that the IRS may file a Notice of Federal Tax Lien, and once the printed deadline passes a lien filing becomes a real possibility. A lien is a public legal claim against everything you own — it no longer appears on consumer credit reports, but it attaches to your property and can complicate selling or refinancing a home.

What if my CP504 balance came from returns I never filed?

Then the IRS likely built the balance through substitute-for-return assessments, which allow zero business deductions — no mileage, no expenses, no platform fees. Filing your real returns can legitimately shrink the assessed balance, sometimes dramatically for self-employed taxpayers, and filing is required before the IRS will approve any payment plan or hardship status anyway. Start there.

Does a CP504 affect my passport?

Not by itself, but the danger is close. Passport certification applies to seriously delinquent tax debt over $66,000 in 2026, and it generally requires the case to reach the lien or levy stage — you would receive a CP508C when it happens. If your balance is above that threshold at the CP504 stage, resolving or reducing it now can keep certification from ever occurring.

Does the IRS being understaffed in 2026 mean the levy will take longer?

Do not count on it. The IRS workforce shrank roughly 27% in 2025, but CP504s, LT11s, refund seizures, and levies are generated by automated systems that never stopped running. The staffing cuts mostly mean it is harder to reach a human to fix a problem after a levy hits — which is a reason to act earlier, not later.

Your next 24 hours

- Find the two dates. Pull out the CP504 and write down the notice date (top corner) and the pay-by deadline, then count how many days you have left on the first clock.

- Gather your file. The CP504 itself, your last filed return, and income records for any unfiled years (1099-NEC and 1099-K forms, bank statements) — then log into your IRS online account and confirm the balance and any 971 entries.

- Get the free review before the deadline passes. Send a photo of your CP504 through the 2-minute form or call (888) 825-7779 — an experienced tax professional will map which clock you're on and the cheapest way off it.

Primary sources for this guide: the IRS's own Understanding your CP504 notice page, the IRS payment plans and installment agreements page, and the Taxpayer Advocate Service, which can intervene when a levy would cause immediate hardship.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.