Business & Payroll Taxes

Payroll Tax Debt After Your Business Closed: Why the Liability Survives the Dissolved Business (2025)

The short answer: closing your business does not erase payroll tax debt. The "trust fund" part — the income tax and Social Security and Medicare you withheld from employees' paychecks — can be assessed against you personally through the Trust Fund Recovery Penalty, even after the company is gone. That personal liability survives the dissolved business.

Did the IRS just make your closed business personal?

Send us your Letter 1153 or 941 notice. An experienced tax professional will explain exactly where you stand, whether you can fight the responsible-person finding, and what relief you may qualify for — free, confidential, no pressure.

⏱ Your deadline: if you've received Letter 1153 proposing the Trust Fund Recovery Penalty, you generally have 60 days to appeal before it becomes a personal assessment. After that, the IRS can levy your personal accounts and wages. Don't let that window close without responding.

Why payroll tax debt follows you after the business closes

When you ran payroll, you held two kinds of money. The first is your company's own share of Social Security and Medicare — a true business expense. The second is "trust fund" money: the income tax, Social Security, and Medicare you withheld from your workers' paychecks. That money was never yours. You held it in trust for the government and the employees.

When a business falls behind on its Form 941 payroll taxes and then closes, the company's share may die with the company. But the trust-fund money does not. The IRS treats failing to pay over withheld taxes as a serious matter, because that cash belonged to your employees and the U.S. Treasury, not the business. So Congress gave the IRS a tool to reach the people behind the company: the Trust Fund Recovery Penalty.

That's why your payroll tax debt didn't vanish when you dissolved the LLC or corporation. The IRS can move the trust-fund portion off the dead company and onto you personally. You can read the IRS's own overview on the Trust Fund Recovery Penalty page.

The Trust Fund Recovery Penalty, in plain English

Despite the word "penalty," the Trust Fund Recovery Penalty (TFRP) isn't an extra fine. It's the IRS shifting the unpaid trust-fund taxes from your closed business to a person. To assess it, the IRS has to show two things:

- You were a "responsible person." That means you had the authority to decide which bills got paid — an owner, officer, partner, bookkeeper, or anyone who signed checks or controlled the money. More than one person can be responsible at the same time.

- You acted "willfully." This sounds criminal, but it isn't. It simply means you knew the taxes were due and chose to pay other creditors — rent, suppliers, payroll itself — instead of sending the withheld money to the IRS.

If both are true, the IRS can assess 100% of the trust-fund taxes against you as an individual. For a deeper walkthrough of how this works and how to push back, see our full guide on the Trust Fund Recovery Penalty and who is personally liable.

What happens if you ignore it

The IRS doesn't forget a dissolved business. Its systems are automated, and the path from a closed company to a personal levy is well-traveled. Here's the typical sequence:

- Form 4180 interview. A revenue officer interviews you (and others) to decide who was responsible and willful.

- Letter 1153. The IRS formally proposes the TFRP against you. You have 60 days to appeal.

- Personal assessment. If you don't appeal, the penalty becomes a debt in your own name — and a fresh 10-year collection clock starts.

- Liens and levies. The IRS can file a federal tax lien against your home, levy your personal bank account, and garnish your wages from your next job.

Because more than one person can be held responsible, the IRS may pursue you, a former business partner, and your bookkeeper all at once. Each of you can be assessed for the full trust-fund amount, though the IRS only collects the total once.

How long the IRS can collect after the business closed

The IRS generally has 10 years to collect a tax debt from the date it's assessed. The twist with payroll tax debt is timing: the Trust Fund Recovery Penalty gets its own 10-year clock from the date it's assessed against you personally — which can be a year or more after your business shut its doors. So even a company you closed years ago can produce a personal collection clock that runs well into the future. Our guide on how long the IRS can collect back taxes explains the statute in detail.

Your options when payroll tax debt survives a closed business

Once the trust-fund penalty is assessed in your name, it's treated like any other personal tax debt — which means the same relief programs are on the table. Which one fits depends on your finances:

- Fight the assessment first. If you weren't truly a responsible person — say you were a minority owner with no check-signing power, or a bookkeeper following orders — you may be able to defeat the TFRP before it ever sticks. This is why responding to Letter 1153 matters so much.

- Installment agreement. A monthly payment plan on the assessed balance. Details are on the IRS payment plans page.

- Currently Not Collectible status. If paying anything would create real hardship, the IRS can pause collection. The debt stays, but levies and garnishments stop.

- Offer in Compromise. Settling for less than the full balance — real, but only when your personal assets and income genuinely can't cover the debt. Anyone promising to settle for pennies on the dollar before reviewing your finances is selling you something. The IRS runs the math, not the marketing.

A worked example: say your closed S-corp left $42,000 in unpaid 941 taxes. Roughly $30,000 of that is trust-fund money (the withheld income tax plus the employee half of Social Security and Medicare). The IRS can assess that $30,000 against you personally as the TFRP. The remaining $12,000 — the employer's matching share and penalties — generally stays with the dead corporation and is often uncollectible. Knowing which dollars can follow you changes your entire strategy.

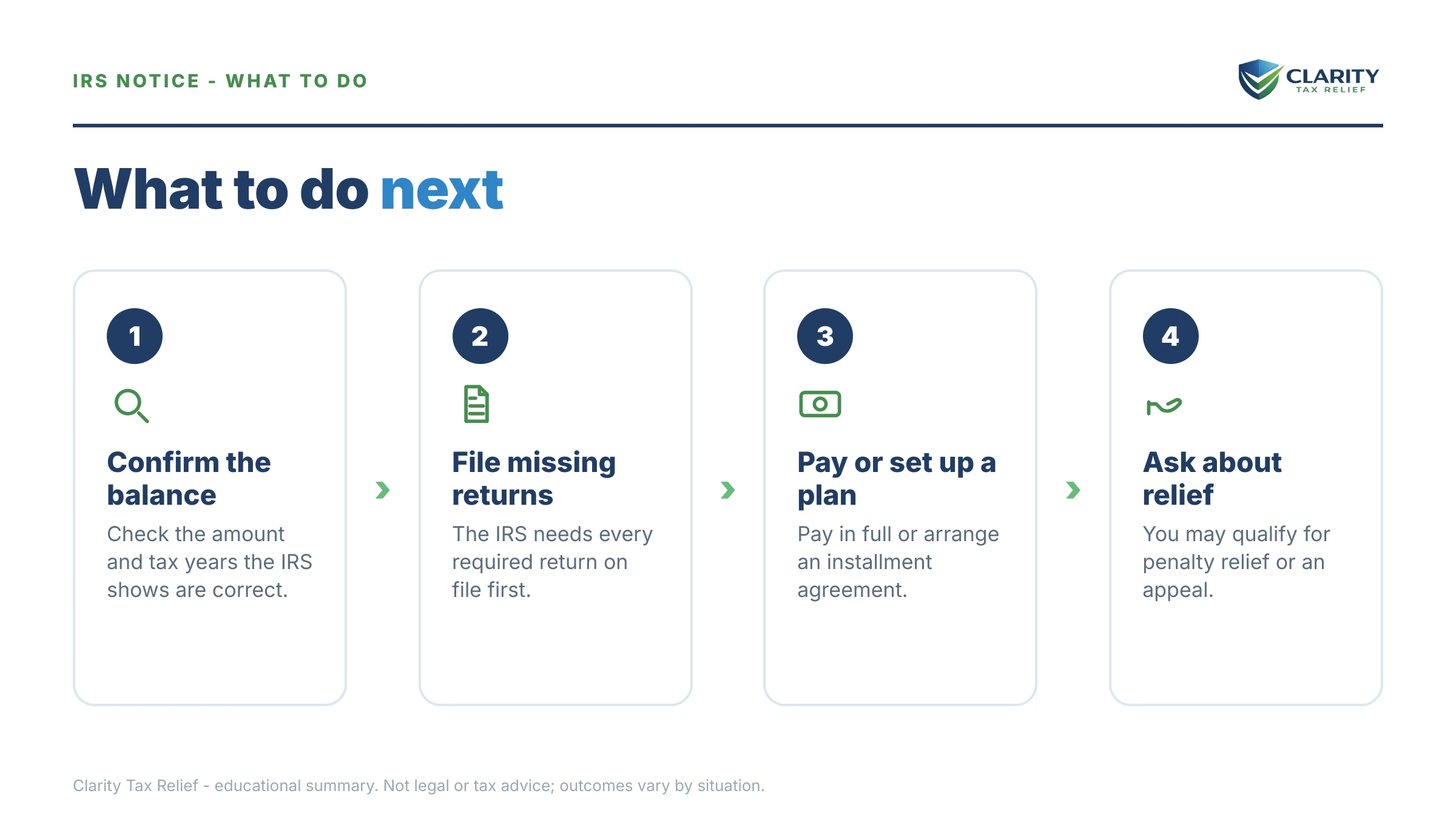

How to respond, step by step

- Read the notice carefully. Is it a business 941 balance, or a personal TFRP proposal (Letter 1153)? They call for different responses. Our guide on 941 back taxes when a business falls behind covers the business side.

- Calendar the 60-day deadline. If you have a Letter 1153 and want to dispute that you were responsible or willful, you must act within that window.

- Gather your records. Bank signature cards, payroll reports, board minutes, and anything showing who actually controlled the money. This evidence wins or loses the responsible-person argument.

- Decide whether to appeal. If you have a real defense, file the appeal before the penalty is assessed — your options narrow sharply afterward. See our walkthrough of Letter 1153 and the 60-day deadline.

- Plan for the balance you'll owe. If the TFRP will stick, line up an installment agreement, hardship status, or an offer based on your personal finances before the IRS starts levying.

- Get a professional review. The order you handle this in — defense first, then resolution — changes what you end up paying. An experienced tax professional can map it out before you commit to anything.

If collection is already causing hardship, the independent Taxpayer Advocate Service can sometimes help. And if you haven't yet formally wrapped up the entity, the IRS closing a business page lists the final payroll filings you still owe.

Payroll tax debt after a closed business: your questions, answered

Does payroll tax debt go away when I close my business?

No. Closing or dissolving a business does not erase its payroll tax debt. The trust-fund portion — the income tax and employee Social Security and Medicare you withheld — can be assessed against you personally through the Trust Fund Recovery Penalty, even after the company no longer exists.

Can the IRS come after me personally for my closed company's 941 taxes?

Yes, for the trust-fund part. If you were a responsible person who willfully failed to pay over withheld taxes, the IRS can assess the Trust Fund Recovery Penalty against you as an individual. It can then levy your personal bank account, garnish your wages, and file a lien against your property.

How long can the IRS collect payroll tax debt after a business closes?

The IRS generally has 10 years to collect from the date each liability is assessed. The Trust Fund Recovery Penalty gets its own separate 10-year clock from the date it is assessed against you personally, which can be years after the business shut down.

I got a Letter 1153 after closing my business. What is it?

Letter 1153 is the IRS's formal proposal to assess the Trust Fund Recovery Penalty against you personally. You generally have 60 days to appeal before the penalty becomes a personal assessment. Do not ignore it — this is the moment your options are widest.

Can I settle payroll tax debt after my business closed?

Possibly. Once the trust-fund penalty is assessed against you as an individual, you may qualify for an installment agreement, Currently Not Collectible status, or an Offer in Compromise — depending on your personal finances. There are no guaranteed outcomes; eligibility depends on your facts.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.