Back Taxes

Inheritance and Back Taxes: What the IRS Can Take — and How to Protect What's Left (2026)

The short answer: when inheritance and back taxes meet, the federal tax lien controls. If you owe the IRS, the lien automatically attaches to money and property you inherit, and the IRS can collect from it. If the person who died owed, the estate pays first — heirs aren't personally liable beyond what they actually received.

The distribution check from your brother's estate finally cleared — $83,100 — and instead of relief, your first thought was the IRS balance you've been quietly carrying on a Social Security budget. You're right that the two are connected. But you get to decide how they meet, and doing it deliberately can leave you thousands of dollars ahead of doing nothing.

⏱ The real clock: there is no letter deadline on an inheritance — the federal tax lien attached to your future property the day the IRS assessed your debt and demanded payment. Every month you wait, the failure-to-pay penalty adds 0.5% and interest compounds daily on the full balance, shrinking what the inheritance can accomplish.

Why the IRS can take an inheritance for back taxes

A federal tax lien attaches automatically to property you acquire after the debt was assessed — including an inheritance, the moment it vests in you. This is called the after-acquired property rule, and it's why "the debt is old and the money is new" offers no protection. The lien arose when the IRS assessed your balance and sent its demand for payment; it has been waiting silently for assets ever since.

It doesn't matter that the money came from a parent, a sibling, or a spouse who never owed anything. Once your interest in the estate vests — typically at the death of the person who left it to you, even before the executor cuts a check — the lien reaches it. Cash, a house, a brokerage account, an inherited IRA: all of it. The can the IRS take my inheritance guide covers the seizure mechanics in more detail; this page covers the full playbook.

One tactic readers ask about immediately: refusing the inheritance. Under most state laws, a "disclaimer" treats you as never having owned the asset — which works against ordinary creditors. It does not work against the IRS. In Drye v. United States (1999), the Supreme Court held that a state-law disclaimer does not defeat the federal tax lien. Sign a disclaimer to dodge back taxes and the IRS can still collect from the share you turned down — and you've given up the money on top of it.

The other direction: when the person who died owed the IRS

Heirs are not personally liable for a decedent's back taxes — but the IRS gets paid from the estate before heirs do. If you're inheriting from someone who owed, the debt belongs to their estate, and the executor must satisfy the IRS out of estate assets before distributing what's left. Your own savings, home, and Social Security are never on the hook for someone else's tax debt.

Two exceptions make this messier in practice:

- Transferee liability (IRC §6901). If the estate distributes assets to you while the IRS goes unpaid, the IRS can come after you — but only up to the value of what you received. Inherit $40,000 from an estate that stiffed the IRS on $100,000, and your maximum exposure is $40,000, not the full debt.

- Executor liability (31 U.S.C. §3713). An executor who pays heirs or other creditors while knowing the estate can't cover its federal tax debt can be personally liable for the shortfall. If you're wearing both hats — heir and executor — read the executor personally liable IRS guide before distributing anything.

The decedent's debt also stays subject to the normal 10-year collection statute; death doesn't extend it, and death doesn't erase it either. For the full sequence of resolving a deceased person's balance, see estate owes IRS and parent died owing taxes; the broader question is answered honestly in does IRS debt die with you.

Do you owe new taxes on the inheritance itself?

There is no federal inheritance tax on the person receiving the money — most bequests arrive income-tax-free. Any federal estate tax is the estate's problem, and in 2026 it only touches multi-million-dollar estates. So the $83,100 itself generally doesn't add a line to your 1040.

Three exceptions create new tax — and for someone already behind, new tax on top of old debt is exactly the trap to avoid:

- Inherited traditional IRAs and 401(k)s. Every dollar you withdraw is ordinary taxable income to you, and most non-spouse beneficiaries must empty the account within 10 years. Big withdrawals can also make more of your Social Security taxable. The inherited IRA taxes owed guide walks through the timing.

- Income in respect of a decedent (IRD) — items like the decedent's final paycheck, unpaid commissions, or accrued savings-bond interest — is taxable to whoever collects it.

- Post-death earnings. Interest, dividends, and rent the inherited assets produce after you receive them are your taxable income going forward.

A few states also charge their own inheritance tax on beneficiaries. State rules vary widely — don't apply federal assumptions to your state; check with its revenue agency directly.

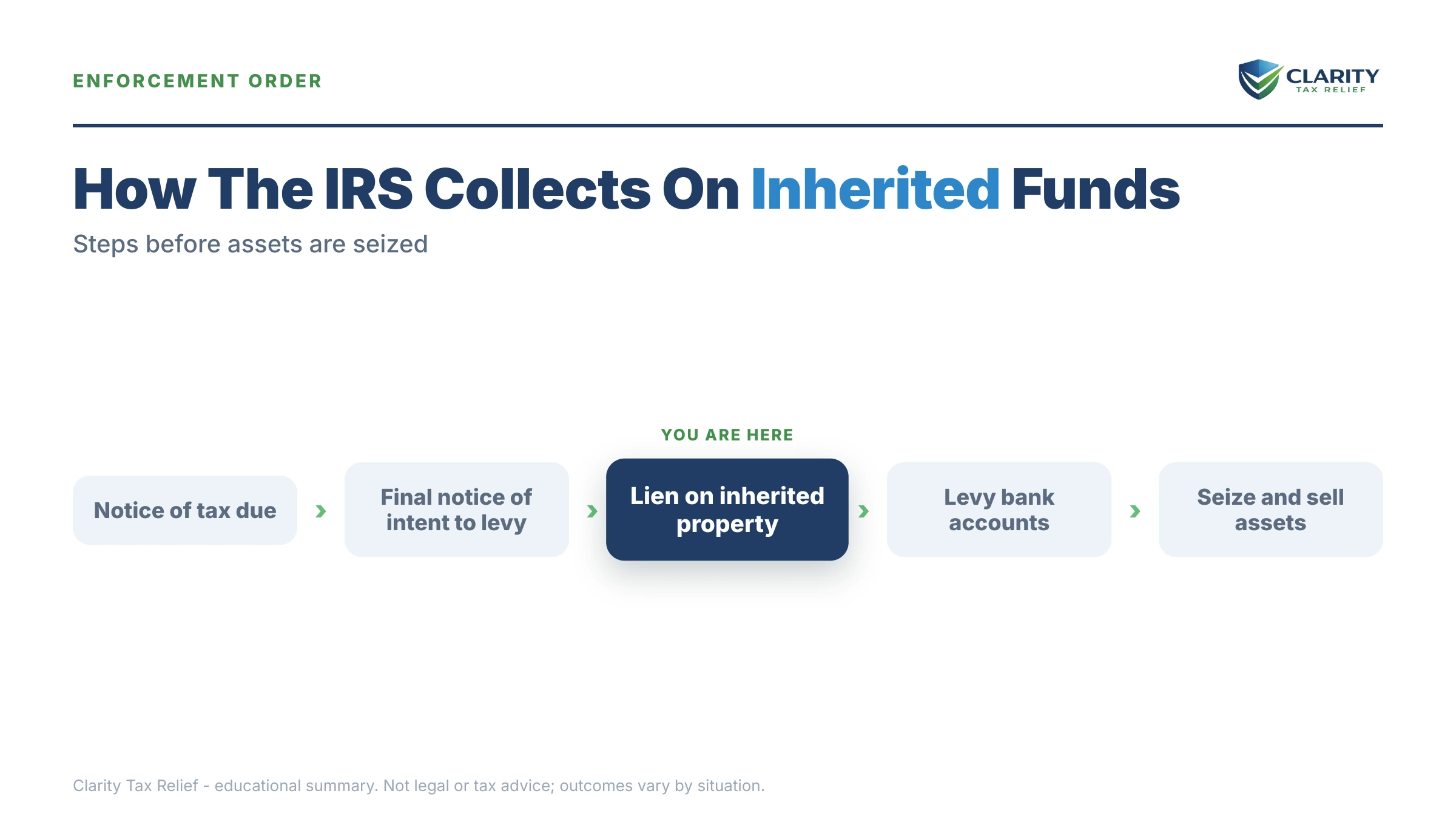

What happens if you ignore back taxes after inheriting

An inheritance sitting in a bank account is the single easiest asset for the IRS to levy — and a bank levy gives you only a 21-day hold before the funds leave. Here is the sequence if you deposit the money and do nothing about the balance:

- The lien is already attached. No new paperwork needed — the existing federal tax lien reached your inherited share the moment it vested, before the check was even cut.

- Collection notices resume or escalate. If your account was quiet, a new asset and new filings can wake it up. The notice ladder runs through a CP504 (the IRS can take your state refund) to an LT11 or Letter 1058 — the final notice that starts a 30-day clock and your Collection Due Process rights.

- Bank levy. Once the final-notice window passes, the IRS can levy the account holding the inheritance. The bank freezes the funds for 21 days, then sends them to the Treasury. On a fixed income, that's your cushion gone in one stroke.

- Your Social Security keeps getting hit too. The Federal Payment Levy Program can take up to 15% of each benefit check, continuously, on top of any bank levy — one doesn't replace the other.

- Passport certification. If penalties and interest push your balance to $66,000 or more (the 2026 threshold), the IRS can certify the debt to the State Department, blocking passport issuance or renewal.

- Spending it first doesn't reset anything. If you later seek an Offer in Compromise, money you spent on non-essentials can be added back into the IRS's math as dissipated assets OIC — you're treated as if you still had it.

In 2026 the IRS workforce is roughly 27% smaller than it was, and reaching a human is genuinely harder. But liens, levies, and notice escalation run on automated systems that never took a layoff. The machine doesn't know you inherited the money for a roof and medical bills — it only sees a collectible balance and a fresh deposit.

Inherited money while owing the IRS?

The window between the estate distribution and IRS enforcement is when your options are widest. Get your balance and your inheritance reviewed free — before the money sits where a levy can reach it. Call (888) 825-7779 or use the 2-minute form.

Your options when inheritance and back taxes collide

With a lump sum in hand, full payment is usually the cheapest resolution — but it is not the only one, and it is not always the smartest first move. An inheritance changes which IRS programs realistically fit, because most relief programs are means-tested and the lump sum now counts against you. Here's the honest map (the general mechanics of each program live in our how to settle tax debt yourself pillar):

| Option | Fit when you're holding an inheritance | Cost / catch |

|---|---|---|

| Pay in full | Best when the inheritance covers the balance — stops all accrual the day it posts | Consumes part of the inheritance; the IRS releases the lien after full payment |

| Short-term plan (up to 180 days) | Good bridge while the estate is still in probate and the distribution hasn't arrived | $0 setup; interest and penalties continue until paid |

| Streamlined installment agreement (balance ≤ $50,000) | Available — up to 72 months, usually no financial disclosure — but rarely cheapest with cash in hand | Setup fee applies; interest plus a monthly late-payment penalty keep accruing the whole term |

| Offer in Compromise | Generally off the table — the inheritance raises your Reasonable Collection Potential, often above the debt | $205 application fee; roughly 1 in 5 offers were accepted in FY2024 |

| Currently Not Collectible | Unlikely while a lump sum sits in your account — it's an available asset, even on a Social Security income | Debt keeps accruing; the IRS reviews hardship accounts and will see the deposit |

| Penalty abatement (FTA / reasonable cause / AEP) | Stacks with every option above — shrinks what the inheritance must cover | Free to request; interest on the underlying tax cannot generally be waived on its own |

The Offer in Compromise row deserves one more sentence, because it's where people get burned. The IRS prices an offer on your Reasonable Collection Potential — your net equity in assets plus a multiple of your monthly disposable income. Before the inheritance, a retiree on Social Security often has an RCP far below the debt. After $83,100 lands, RCP usually exceeds the balance, and the IRS will simply say: pay it. You can estimate your own numbers with our Offer in Compromise Calculator — run it both with and without the inheritance and you'll see exactly why timing and honesty both matter here.

Penalty relief is the quiet winner. If your filing and payment history was clean for the three years before the problem year, first-time abatement can strip the failure-to-pay penalties — and beginning summer 2026, the IRS's Automatic Exemption from Penalty (AEP) applies qualifying relief automatically, with no request needed. Read first-time penalty abatement before you send a payment, because a granted abatement means the inheritance covers less debt and more of your life.

How much you owe changes the play

The right move with $83,100 depends almost entirely on the size of the balance it's meeting. Two thresholds matter more than any others: $50,000 (the streamlined-plan ceiling) and $66,000 (the 2026 passport-certification line).

| Your back-tax balance | Realistic play with $83,100 in hand | Why |

|---|---|---|

| Under $10,000 | Pay in full online, then request penalty relief | Stops the 0.5%/month penalty and daily interest instantly; costs a small slice of the inheritance |

| $10,000 – $50,000 | Full pay is usually cheapest; file the abatement request alongside | A 72-month plan is available but interest makes it thousands more expensive than paying now |

| $50,000 – $83,100 | Full pay if the rest of your budget allows; otherwise pay down below $50,000 and set a streamlined plan | Getting under $66,000 also clears the passport-certification range on the way down |

| More than $83,100 | Strategic lump-sum paydown plus a payment plan — get a professional review before wiring anything | The inheritance can't clear it, so where you land the remaining balance decides which programs open up |

Notice what the last row implies: when the debt is bigger than the inheritance, sending every dollar isn't automatically right. A retiree who owes $110,000 and pays $63,000 lands at $47,000 — under both key thresholds, eligible for a streamlined plan, passport safe — while keeping $20,100 as a cushion the IRS's own living-expense standards would largely allow. That's a materially better position than owing $26,900 with an empty account and a levy-vulnerable final stretch.

What the IRS can reach, asset by asset

Not every inherited asset is equally exposed, and a few carry their own tax time bombs. This is the reference most heirs have to piece together from six different pages:

| What you inherited | Can the IRS reach it for your back taxes? | Key detail |

|---|---|---|

| Cash bequest / bank or brokerage account | Yes — the lien attaches when your share vests | Once deposited, it's the easiest levy target; a bank levy has a 21-day hold before funds leave |

| Inherited traditional IRA or 401(k) | Yes — and withdrawals are also taxable income to you | Most non-spouse heirs must empty it within 10 years; plan withdrawals so they don't create new debt |

| Real estate | Yes — the lien attaches to your interest in the property | Complicates any sale; see sell house with IRS lien for the payoff-at-closing process |

| Life insurance proceeds paid to you as beneficiary | Yes, once paid to you | Generally income-tax-free to receive, but not levy-proof once it's your money |

| A share you disclaimed | Yes — the federal lien still reaches it | Drye v. United States: a state-law disclaimer doesn't defeat the federal tax lien |

| Assets still sitting in the estate or trust | Generally reachable once distributed to you | Timing and trust terms matter enormously — this is a get-advice-first situation, not a DIY one |

A worked example: $83,100 inheritance, $26,400 in back taxes

Say you're retired, living on Social Security plus a small pension, and you owe the IRS $26,400 from the year you cashed out a retirement account — roughly $21,000 in tax, $3,300 in penalties, and $2,100 in accrued interest. Then $83,100 arrives from an estate. This is a hypothetical, but the arithmetic is exactly what you'd face:

- Option 1 — pay in full now. $83,100 − $26,400 = $56,700 kept, and all accrual stops the day the payment posts. Then file Form 843 requesting first-time abatement of the penalties: if your prior three years were clean and it's granted, roughly $3,300 of penalty (plus the interest charged on it) comes back to you. Net cost of the whole episode: about $23,000 or less.

- Option 2 — a 72-month payment plan instead. $26,400 ÷ 72 ≈ $367 a month before accrual — and interest plus a monthly late-payment penalty keep running on the declining balance the entire time, adding thousands to the total. You'd keep the $83,100 liquid, but on a fixed income you'd carry a $367 payment into your mid-80s while the IRS lien sits on everything you own.

- Option 3 — an Offer in Compromise. Your Reasonable Collection Potential now includes most of the $83,100, which is more than triple the $26,400 debt. The offer would be rejected on arithmetic alone, and you'd be out the $205 fee and months of waiting while accrual continued.

The order matters as much as the choice: request penalty relief, pay, keep the paperwork. Paying first and never asking for abatement is the most common — and most expensive — mistake we see heirs make.

Special situations that change the answer

Only your spouse owes. An inheritance is generally your separate property — even in community-property states — which puts it beyond the IRS's reach for a debt that's solely your spouse's. That protection evaporates if you deposit it into a joint account and commingle it. Keep inherited funds in an account titled only to you, and read can the IRS take my spouse's bank account before moving money.

You're in a Chapter 13 bankruptcy. An inheritance received during your case can become property of the bankruptcy estate and may have to be committed to your plan — sometimes changing what unsecured creditors, including the IRS, get paid. Do not spend a dime of it before your attorney weighs in; the chapter 13 IRS back taxes guide explains how tax claims sit inside a plan.

You have a pending OIC or you're in CNC status. Both are built on your financial disclosures, and both come with an ongoing duty of accuracy. An inheritance received mid-offer must be reported and will be priced into the decision; a lump sum discovered during a hardship review can end IRS hardship on Social Security status. Getting ahead of the disclosure — with a plan for the money already in place — always beats being caught.

The debt is old. The IRS has 10 years from assessment to collect, and events like offers and bankruptcies pause that clock. If your 10-year collection statute is nearly expired, paying a nearly-dead debt in full may be the wrong move entirely — but the lien on your inheritance is precisely the leverage the IRS uses in those final years, so this is a verify-the-dates-first decision, never a guess.

How to respond to inheritance and back taxes, step by step

- Pull your exact IRS balance. Log into your IRS online account or request account transcripts for every year you owe. Note each year's balance, how much is penalty versus tax, and where each debt sits on its 10-year collection clock.

- Inventory the inheritance before you spend it. List what you received or will receive — cash, IRA, real estate, life insurance — with dates and the executor's distribution paperwork. What vested, and when, determines what the lien already reaches.

- Request penalty relief before or alongside payment. If your compliance history is clean for the prior three years, ask for first-time abatement; starting summer 2026, the IRS's Automatic Exemption from Penalty applies some relief with no request at all. Form 843 recovers qualifying penalties you already paid.

- Pay or structure the balance deliberately. Full payment at IRS.gov stops penalty and interest accrual immediately. If the debt is bigger than the inheritance, choose your paydown target — under $66,000 or under $50,000 — before you send anything.

- Keep every estate document. Distribution letters, the will or trust, account statements, and 1099-R forms prove what you received and when — the exact facts that decide transferee-liability and levy disputes.

- Get a professional review if the numbers don't line up. If the debt exceeds the inheritance, the estate itself owed the IRS, or a levy is already in motion, an experienced tax professional can sequence the fix before the money is exposed.

When you can handle this yourself

If the inheritance comfortably covers a balance you agree with, you likely don't need anyone's help. Verify the number in your IRS online account, pay at IRS.gov/payments, and mail your own penalty-abatement request — that's a solved problem and a good afternoon's work. The same goes for a small balance you can clear within 180 days on a $0-fee short-term plan while probate finishes.

Experienced help genuinely changes outcomes in five situations: the debt is larger than the inheritance (paydown targeting and program sequencing decide what you pay for years); a levy or final notice is already in motion (the 30-day and 21-day windows are unforgiving); the estate itself owed the IRS (transferee and executor exposure need to be scoped before distributions); you inherited real estate with a lien in play; or you have a pending OIC, CNC status, or an active bankruptcy, where the disclosure itself must be handled correctly. If you can't get a straight answer from the IRS by phone — and in 2026, many people can't — the Taxpayer Advocate Service is a free, independent escalation path for cases the system is mishandling.

Terms in this situation, decoded

- Federal tax lien — the government's automatic legal claim to everything you own and later acquire, arising when a tax debt is assessed and demand for payment goes unpaid (the IRS's own explainer: Understanding a federal tax lien).

- After-acquired property — assets you obtain after the lien arises, like an inheritance, which the existing lien reaches without any new filing.

- Transferee liability — the IRS's power to collect a decedent's unpaid taxes from heirs, capped at the value of what each heir actually received.

- Income in respect of a decedent (IRD) — income the deceased earned but never collected (final wages, accrued bond interest), taxable to whoever receives it.

- Reasonable Collection Potential (RCP) — the IRS's math for pricing an Offer in Compromise: your asset equity plus a multiple of monthly disposable income.

- CSED — the Collection Statute Expiration Date, the end of the IRS's 10-year window to collect an assessed debt, pausable by offers, appeals, and bankruptcy.

If the estate paperwork and the IRS balance are sitting side by side on your kitchen table and the right order of moves still isn't obvious, a free case review with an experienced tax professional at (888) 825-7779 can map it in one call — before the money is anywhere a levy can find it.

Inheritance and back taxes: your questions, answered

Can the IRS take my inheritance for back taxes?

Yes. Once the IRS assesses a tax debt and sends its demand for payment, a federal tax lien attaches to everything you own — including property you acquire later. An inheritance vests in you and the lien reaches it automatically, whether it's cash, a house, or an IRA. The practical risk is a bank levy after the money lands in your account, which comes with a 21-day hold before the funds leave.

Can I refuse (disclaim) an inheritance so the IRS can't take it?

Usually not. In Drye v. United States, the Supreme Court held that disclaiming an inheritance under state law does not defeat a federal tax lien — the IRS can still collect from the share you turned down. A disclaimer may still work against other creditors, but the federal tax lien is the exception. Talk to an experienced tax professional before signing any disclaimer.

Do I owe taxes on the inheritance itself?

Generally no — there is no federal inheritance tax on the person receiving the money, and most bequests arrive income-tax-free. The big exceptions: distributions from an inherited traditional IRA or 401(k) are taxable income to you, and income the inherited assets earn after you receive them — interest, dividends, rent — is taxable going forward. A handful of states charge their own inheritance tax, so check yours.

Am I responsible for a parent's or spouse's back taxes if I inherit from them?

You are not personally liable for a deceased person's back taxes from your own money. The debt belongs to their estate, which must pay the IRS before distributing assets to heirs. But if the estate hands you assets while IRS debt goes unpaid, the IRS can pursue transferee liability — recovering up to the value of what you received, and not a penny more.

Should I use my inheritance to pay off my back taxes?

Often yes, because full payment stops the 0.5% monthly failure-to-pay penalty and daily-compounding interest immediately — but request penalty relief first or alongside payment so you don't overpay. If your balance is larger than the inheritance, a strategic partial payment — for example, getting under $50,000 to unlock a streamlined plan, or under $66,000 to stay clear of passport certification — can beat simply sending everything you have.

What happens if I get an inheritance while my Offer in Compromise is pending?

You must tell the IRS, and it will almost certainly change the outcome. An offer is priced on your Reasonable Collection Potential — assets plus future income — and a lump-sum inheritance raises that number, often above your full balance. Hiding it risks the offer being returned now or revoked later. Sometimes withdrawing the offer and full-paying with a penalty-abatement request is the better ending.

Does an inheritance end Currently Not Collectible status?

It can. CNC status rests on your inability to pay basic living expenses, the IRS periodically reviews accounts in hardship status, and a lump sum sitting in your bank account is an available asset. Expect the IRS to ask for payment from it. If most of the inheritance is already committed to necessary expenses — medical debt, housing repairs — document that before the review, not after.

Will the IRS know I received an inheritance?

Assume yes. Probate filings are public record, inherited IRA distributions generate a Form 1099-R, estates file their own tax returns, and bank activity plus your own future returns leave a trail. IRS systems match this data automatically, even with reduced staffing. Planning around the assumption of disclosure — rather than hoping the IRS misses it — is what actually protects the money.

Can the IRS levy my Social Security and my inheritance at the same time?

Yes — they are separate collection tools. The Federal Payment Levy Program can take up to 15% of each Social Security check on a continuous basis, while a one-time bank levy can reach the inherited funds sitting in your account. Resolving the balance — payment, a plan, or documented hardship status — is what stops both; neither levy releases on its own.

Your next 24 hours

- Find your exact balance. Log into your IRS online account (or pull your most recent CP71 annual reminder) and write down the total, the tax years, and how much of it is penalty.

- Gather the estate paperwork. The distribution letter or check stub, the will or trust page naming you, any 1099-R, and your last filed tax return — everything that shows what you received and when.

- Get the free case review. Call (888) 825-7779 or use the form at the top of this page. Interest and the monthly late-payment penalty are accruing on the balance right now — the sooner the inheritance meets a plan instead of a levy, the more of it you keep.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.