State Tax Debt

NYS Tax Warrant: What It Means, What New York Can Do Next, and How to Resolve It (2026)

The short answer: a NYS tax warrant is a public civil judgment the New York State Department of Taxation and Finance files against you for unpaid state taxes. It creates a lien on your property and lets the state garnish wages and levy bank accounts — no court hearing required — and it stays enforceable for roughly 20 years.

Maybe you found the docket entry after a mortgage lender ran a title search. Maybe your employer's payroll department got the paperwork before you did. However a NYS tax warrant surfaced, New York has already converted a tax balance into a judgment against your name — and if a divorce recently split your finances in two, this may be the first time you're learning that a joint balance was still open. The problem is real, but every open warrant has a resolution path, and most of them start with a single phone call or online account.

Two details on the filing control everything that follows: the county where the warrant is docketed and the docket date. The image below shows exactly what a docketed New York tax warrant looks like and where those details appear, so you can read yours before you act.

⏱ The clock on a NYS tax warrant: there is no response window printed on a warrant — once it's docketed, New York can begin an income execution or bank levy at any time. The warrant is generally enforceable for 20 years, and penalties and interest keep accruing every month until the balance is resolved.

Why New York filed a tax warrant against you

New York files a tax warrant only after a tax has been assessed, billed, and left unpaid — it is the Tax Department's judgment step, not its first letter. Before the warrant, the state assessed the tax (from a return you filed, an audit, or its own estimate), sent a bill, and sent collection notices. When the balance stayed open, the Tax Department filed the warrant with the county clerk and the New York Department of State.

That filing does two things at once. First, it docketed a money judgment against you — legally equivalent to losing a lawsuit, except no lawsuit was needed. Second, it created a lien against your real and personal property in any county where it's docketed, and it entered the public record where lenders, landlords, and background checks can find it.

Divorced filers hit this in a specific way: a warrant on a jointly filed year attaches to each spouse named on the return, no matter what the divorce decree says about who pays. New York collects from whoever it can reach — the same principle behind why the IRS ignores the decree applies to Albany too.

One more thing worth checking early: if the assessment itself is wrong — the state estimated a year you never filed, or disallowed something you can document — amending a return to lower a tax debt or filing the missing return can shrink the number behind the warrant before you negotiate the rest.

What happens if you ignore a NYS tax warrant

A docketed NYS tax warrant lets New York garnish wages and drain bank accounts without any further court proceeding. Because the judgment already exists, enforcement is administrative — the state doesn't ask a judge, it sends paperwork. Ignored, the sequence typically unfolds like this:

- Warrant docketed. You are here. The lien attaches, the filing goes public in the Department of State's tax warrant system, and the collection case moves to active enforcement.

- Income execution. New York's version of wage garnishment — typically 10% of your gross wages. It's usually served on you first with a demand to pay voluntarily; if you don't, it goes to your employer, who must comply.

- Bank levy. The state can seize funds from your accounts. Don't assume New York follows the IRS's 21-day bank-hold rule — its procedures are its own, and money can move faster than you expect.

- Driver's license suspension. New York can suspend the licenses of taxpayers owing $10,000 or more — a state weapon the IRS doesn't have. See our full guide to NYS driver's-license suspension for tax debt.

- Refund offsets and property seizure. State refunds get applied to the balance automatically, and as a judgment creditor the state can move against other property. Seizure and sale is the rare last resort, but the warrant is what makes it legally possible.

None of these steps requires a new notice period the way federal levies do. That's the core difference between a warrant and an IRS letter: the due-process stage already happened. The warrant is the end of the warning phase, not part of it.

A tax warrant is already filed against you?

Once docketed, New York can serve an income execution or bank levy at any time — there's no waiting period left. Send us your warrant details and an experienced tax professional will map exactly what the state can take and which resolution stops it — free and confidential.

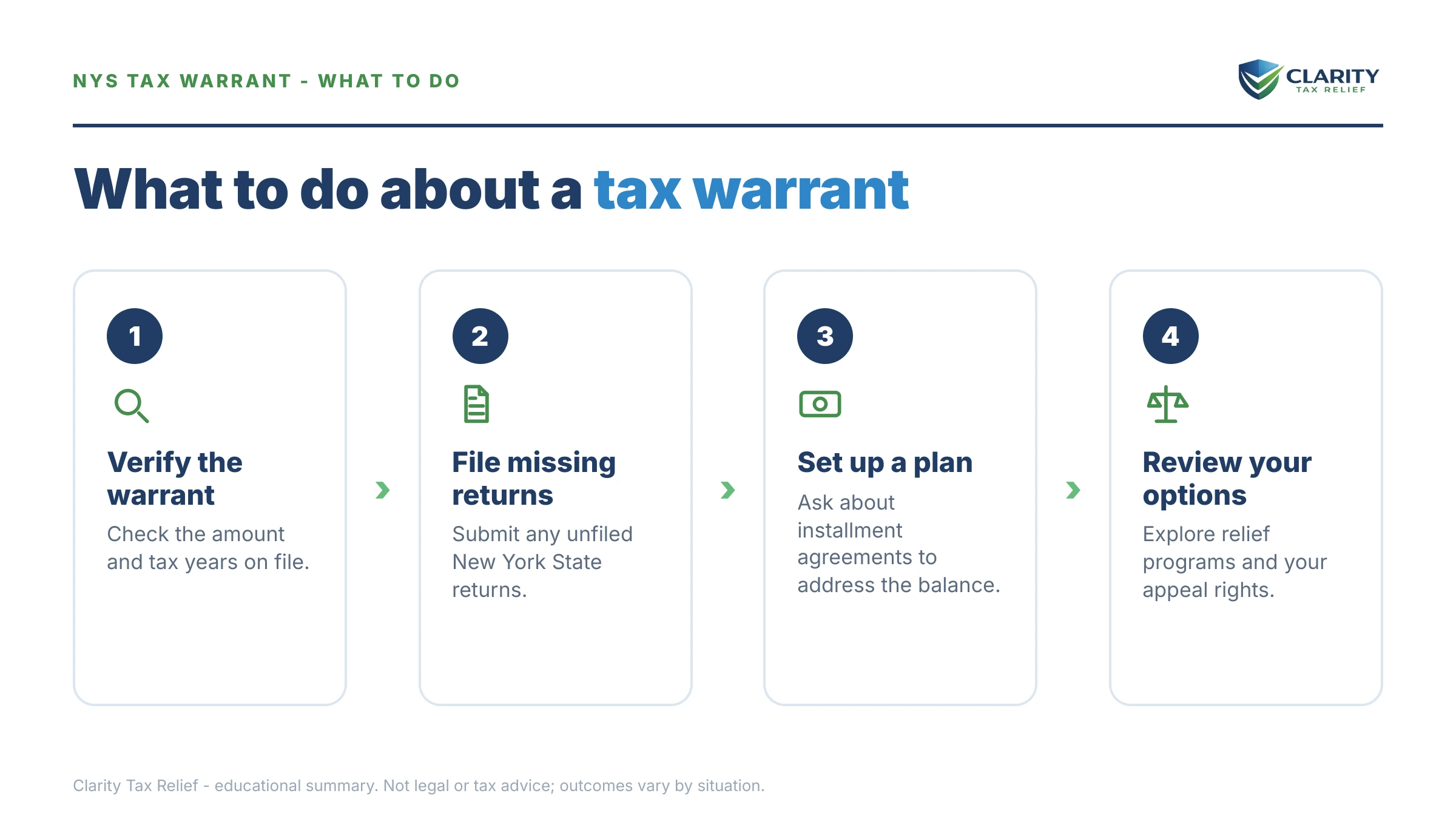

Your options to resolve a New York tax warrant

Every open NYS tax warrant resolves through one of four paths: full payment, an installment payment agreement, a New York offer in compromise, or hardship review. The general mechanics of choosing between paying, settling, and pausing are covered in our guide on how to settle tax debt yourself — here's how New York's versions work once a warrant exists. Note that New York runs its own programs with its own thresholds; nothing about IRS payment-plan limits or the federal Fresh Start framework applies to the Tax Department.

| Option | Who it generally fits | What happens to the warrant |

|---|---|---|

| Pay in full | Anyone who can raise the funds — including from a sale or refinance closing | State files a satisfaction with the county clerk; the record shows the judgment resolved |

| Installment Payment Agreement (IPA) | Steady income and the ability to pay monthly; smaller balances can often be set up through your online account | Warrant usually stays filed as security until paid, but active enforcement generally stops while you're current |

| NYS Offer in Compromise | Insolvent taxpayers, or those for whom full payment would create undue economic hardship — strictly means-tested | Satisfied once the accepted offer amount is paid in full |

| Hardship / uncollectible review | Little or no ability to pay anything right now | Enforcement can pause; the warrant remains and interest keeps accruing |

| Challenge the underlying tax | The assessed amount is wrong — an estimated assessment, a missing return, or a documented error | Warrant is reduced or vacated if the corrected liability is lower; hardest path after docketing, so act on it fast |

Which door is realistic depends on the same math the state will run: your income, your necessary expenses, and your equity in property. The offer in compromise, in particular, is a genuine program — but it's granted on documented inability to pay, not on asking. New York examines your finances at least as closely as the IRS does, and a warrant on file means the state already holds the stronger legal position.

What each option costs and how long it takes

Interest never pauses while you decide — every option below runs against an accruing balance. The exact fees and online-setup thresholds change, so confirm current figures with the Tax Department before committing; what follows is the shape of each path.

| Path | Cost while it runs | Realistic timeline |

|---|---|---|

| Pay in full | Stops new penalties and interest immediately | Satisfaction typically recorded after payment posts — allow weeks for filings and databases to update |

| Installment Payment Agreement | Interest and penalties continue on the unpaid balance for the life of the plan | Days to a few weeks to establish; runs months to years depending on terms |

| NYS Offer in Compromise | Documentation-heavy application; interest accrues during review | Often many months from submission to decision |

| Hardship review | Nothing paid now, but interest compounds and the state re-reviews your finances | Temporary by design; revisited when your situation changes |

| Corrected or amended return | Preparation cost only; can eliminate part of the balance outright | Weeks to months for the state to process and adjust |

How a NYS tax warrant differs from an IRS tax lien

A New York tax warrant is stronger than its federal cousin in two ways. First, the warrant is a judgment — the IRS's lien secures the debt but the IRS must still issue separate levy notices with appeal rights before seizing anything, while New York's due process is already complete when the warrant dockets. Second, the timelines diverge sharply: the IRS generally has 10 years to collect, while a docketed New York warrant is enforceable for roughly twice that. If you owe both Albany and the IRS, sequencing matters — our guide on state tax debt vs irs walks through which to resolve first and why the answer is usually the one with the warrant.

A worked example: a $27,500 warrant after a divorce

Say you owe $27,500 — a hypothetical, but a common shape: two jointly filed years that went unpaid during a separation, assessed against both ex-spouses, with the warrant now docketed against you because you're the one with W-2 wages New York can find. Here's how the realistic paths compare:

- Do nothing: on a $72,000 salary ($6,000/month gross), an income execution at the typical 10% takes about $600 every month — an amount the state picked, on the state's schedule, while the warrant stays enforced and interest keeps compounding on the balance.

- Installment Payment Agreement: $27,500 spread over five years is roughly $458/month before the interest that continues to accrue — so the true monthly figure lands somewhat higher, but you chose the number, enforcement stops, and your employer never sees paperwork.

- Offer in compromise: only in play if your documented assets and future income genuinely can't cover $27,500 — say the divorce left you with no home equity and child-support obligations that consume your margin. The state runs that math from your financials; nobody can promise a settlement figure in advance.

- The tempting shortcut to avoid: cashing out a retirement account from the divorce settlement to pay Albany can create a brand-new federal bill next April — read about the early-401(k)-withdrawal tax bill before you touch that money.

The pattern to notice: the involuntary path (income execution) costs more per month than the voluntary five-year plan, with none of the control. That's the practical argument for acting before the state does.

How to respond to a NYS tax warrant, step by step

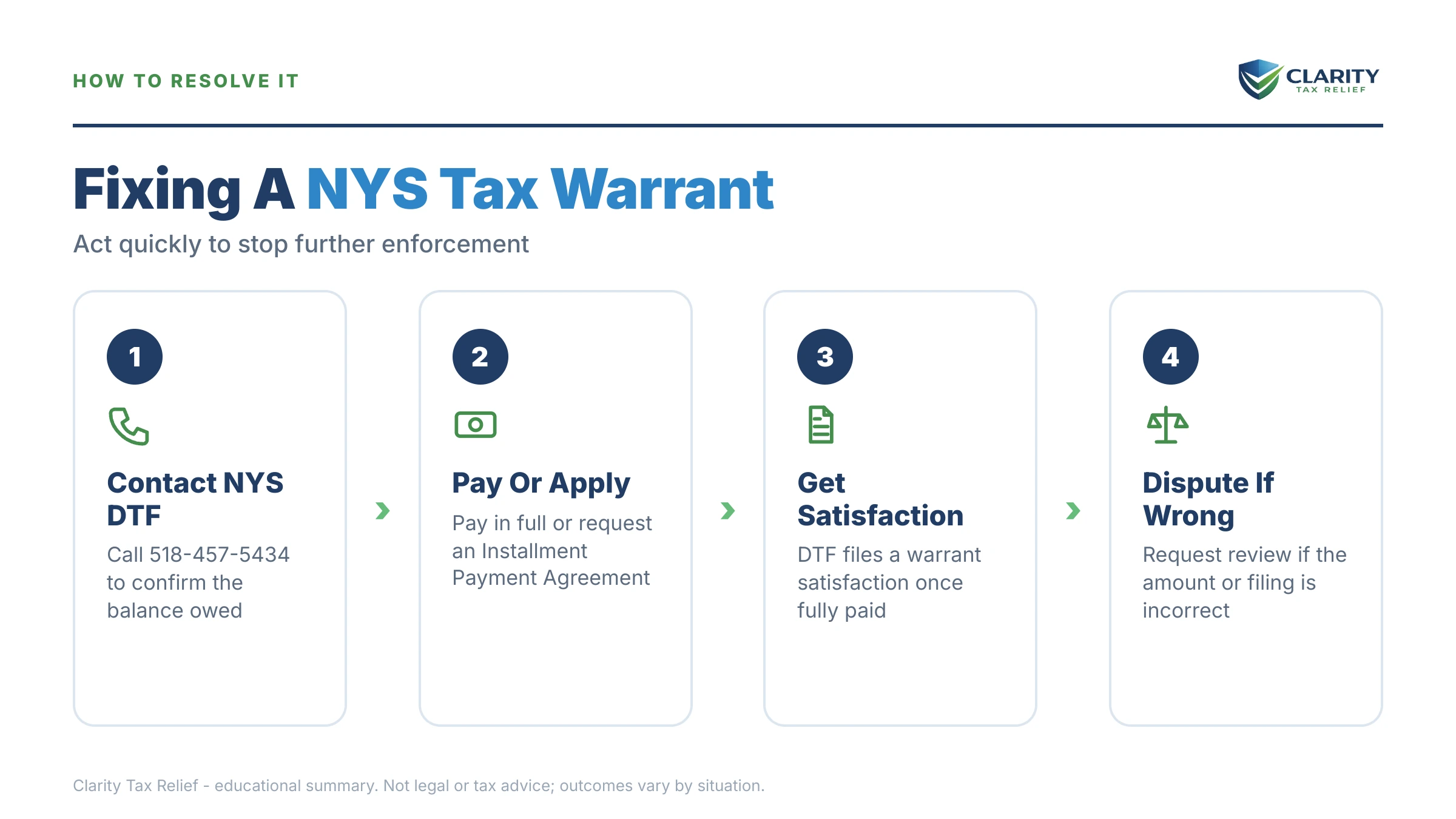

- Pull the warrant details. Search the New York Department of State's tax warrant system or the county clerk's docket for the docket number, date, county, and amount — and log into your NYS Tax Department online account to confirm the balance and the tax years behind it.

- Ask for a collection hold. Call the Tax Department — or have a representative call — and ask that enforcement pause while you set up a resolution, especially if an income execution notice has already arrived.

- File any missing returns. New York will not approve a payment agreement or an offer in compromise while returns are unfiled. File them first, even if you can't pay what they show.

- Set up your resolution. Choose the option that fits your finances — pay in full, an installment payment agreement, a New York offer in compromise, or hardship review — and get the terms in writing before the first due date.

- Get the satisfaction on record. When the balance is resolved, confirm the county clerk's record shows the warrant satisfied and keep the documentation — lenders will ask for it before public databases update.

After you pay: satisfaction, and what stays on the record

Paying a NYS tax warrant doesn't erase it — it converts it to "satisfied," which is the status that matters. The Tax Department files a satisfaction with the county clerk once the balance clears, and the public record then shows the judgment resolved. Two practical notes: the filing takes time to post, so keep your proof of payment and the satisfaction document for any lender who checks before the databases catch up; and if you're mid-closing on a house, ask about how the payoff and satisfaction will be coordinated at the table so the sale isn't held hostage by paperwork timing.

When you can handle a NYS tax warrant yourself

You can usually resolve a warrant on your own when the balance is modest, every return is filed, and a straightforward monthly payment fits your budget — the Tax Department's online account handles simple installment agreements, and step one through five above is genuinely doable solo. If the state's numbers match yours and you just need time, don't pay anyone to make that phone call for you.

Experienced help changes outcomes in the harder scenarios: an income execution or bank levy already in motion, multiple unfiled years New York estimated for you, a joint-liability fight after divorce, a warrant surfacing mid-closing on a property sale, or an offer in compromise where the financial presentation decides everything. In those cases, the difference between an adequate submission and a well-built one is measured in real dollars — and in whether your employer ever receives garnishment paperwork.

Terms on your warrant, decoded

- Tax warrant: New York's civil judgment for unpaid tax — a lien and collection tool, not a criminal charge.

- Docketing: the act of recording the warrant with the county clerk, which makes the judgment official and the lien effective in that county.

- Income execution: New York's wage garnishment under a warrant — typically 10% of gross wages, served on you first and then on your employer.

- Levy: the actual seizure of money or property, most often from a bank account, under the warrant's authority.

- Satisfaction: the filing that marks the warrant paid and the judgment resolved in the public record.

- Judgment debtor: what the warrant makes you — the person against whom the judgment can be enforced, in New York's case for roughly 20 years.

NYS tax warrant questions, answered

Is a NYS tax warrant a criminal warrant or arrest warrant?

No — a NYS tax warrant is a civil money judgment, not a criminal charge, and no one is coming to arrest you. What it does is give the New York State Tax Department the legal power of a judgment creditor: it can garnish wages, levy bank accounts, and place a lien on your property. Criminal tax cases are a separate, rare process that starts very differently.

How do I find out if I have a NYS tax warrant?

Search the New York Department of State's public tax warrant notice system, which lists open warrants by name, or check the county clerk's records where you live or own property. Your Tax Department online account will also show your balance and collection status. If a lender or employer flagged it, ask them for the docket number so you can pull the exact filing.

Does a NYS tax warrant show up on my credit report?

Not directly — the three major credit bureaus stopped reporting tax liens and civil judgments back in 2017–2018, so the warrant itself won't appear on your credit file. But it remains a public record, and mortgage lenders, landlords, and employers who run public-records or title searches will find it. That's why warrants most often surface during a home purchase or refinance.

How long does a NYS tax warrant last?

A docketed New York tax warrant is generally enforceable for 20 years, the same as other New York money judgments — twice as long as the IRS's 10-year collection statute. New York does not simply let the balance age out on any practical timeline, so waiting is not a strategy. Resolution — payment, a payment plan, an offer in compromise, or hardship review — is the realistic way out.

Can I sell or refinance my house with a NYS tax warrant filed?

Yes, but the warrant has to be dealt with at or before closing, because it operates as a lien against your real property in any county where it's docketed. Most commonly the balance is paid from sale or refinance proceeds and the state issues a satisfaction. If the numbers are tight, resolving the balance first — or negotiating how the lien is handled at closing — is where an experienced tax professional earns their fee.

Will New York remove the tax warrant after I pay?

After you pay in full, the Tax Department files a satisfaction of the warrant with the county clerk, which marks the judgment as resolved in the public record. Allow time for that filing to post, and keep your proof of payment and the satisfaction document — you may need to show them to a lender before the public databases catch up. The filing history remains visible; 'satisfied' is the status lenders want to see.

Can NYS garnish my wages without going back to court?

Yes. The warrant itself is the judgment, so no further court action is needed — the Tax Department can serve an income execution that typically takes 10% of your gross wages, first asking you to pay voluntarily and then going to your employer if you don't. It can also levy bank accounts. Setting up a payment agreement before the income execution is served is almost always the cheaper path.

Does a payment plan make the tax warrant go away?

Usually not immediately — New York generally keeps the warrant filed as security until the balance is paid in full, even while you're current on an installment payment agreement. What the agreement does do is stop active enforcement: no income execution, no bank levy, no seizure while you keep the terms. Once the final payment posts, the state files the satisfaction.

Your next 24 hours

- Find the docket details. Pull the county, docket date, docket number, and warrant amount — from the copy the state mailed you, the New York Department of State's tax warrant search, or the county clerk's records.

- Gather three things: your most recent New York return, proof of your current income, and any income-execution or levy paperwork that has arrived — plus your divorce decree if a joint year is involved, so the liability picture is clear. Your online account at the New York State Department of Taxation and Finance fills in whatever's missing.

- Get the warrant reviewed free. There's no waiting period protecting you once a warrant is docketed, and interest compounds monthly either way — so have an experienced tax professional map your resolution options now, before the state picks one for you. Use the 2-minute form or call (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.