State Tax Problems

NYS License Suspension for Tax Debt: The $10,000 Rule and Your 60-Day Window (2026)

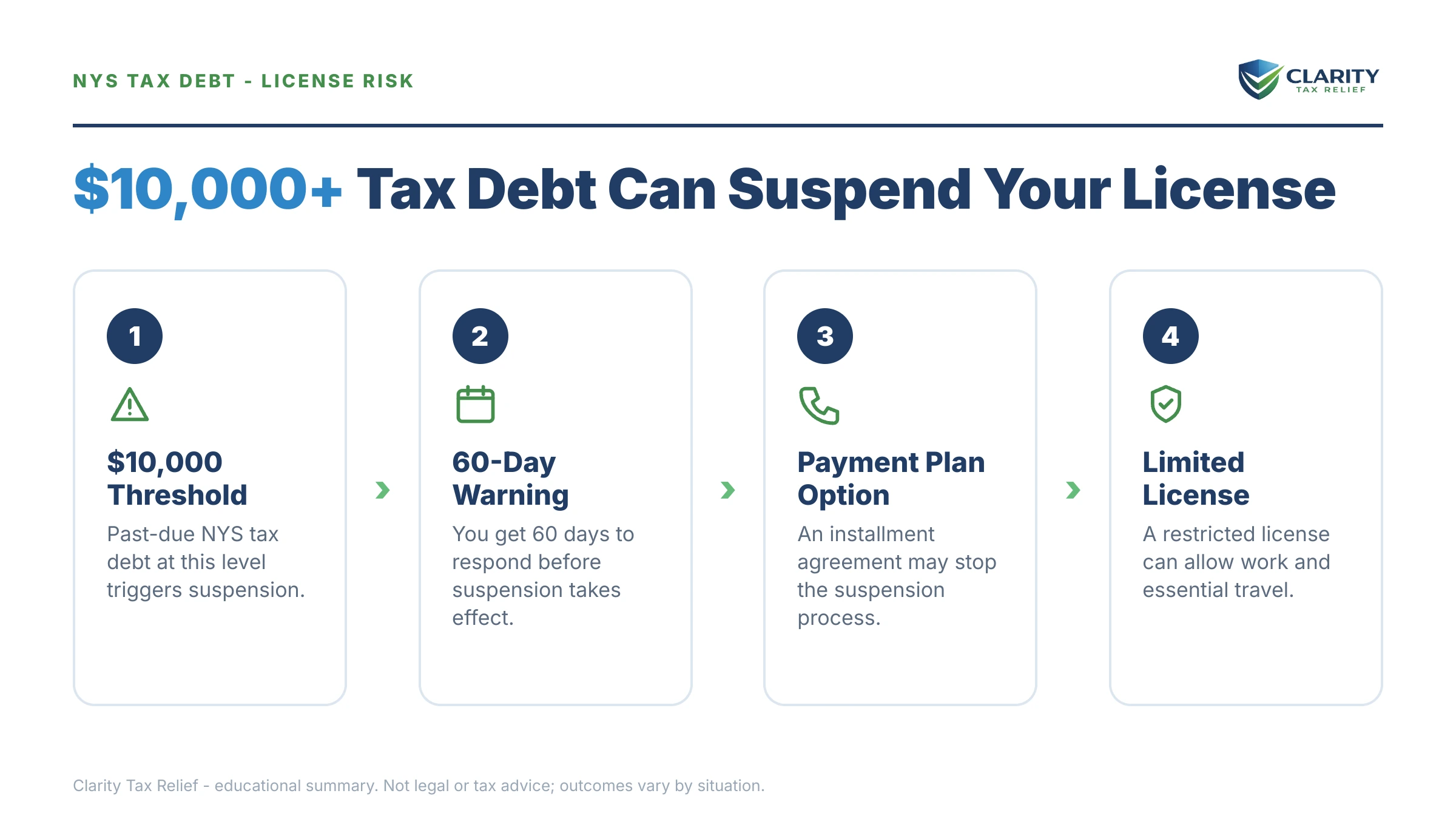

The short answer: NYS license suspension for tax debt starts at $10,000 — New York can suspend your driver's license once your past-due state taxes, penalties, and interest reach that amount. You get a 60-day written notice first. Paying, entering a payment agreement, or proving an exemption inside that window keeps your license.

The letter isn't from the IRS — it's from the New York State Department of Taxation and Finance, and it says the state intends to take your driver's license over an unpaid tax bill. If you're retired and the car is how you reach the pharmacy, the doctor, and everyone you love, that threat cuts deeper than any dollar figure on the page.

Here's the part the notice doesn't emphasize: New York doesn't actually want your license — it wants a response. One action inside the 60-day window, and the suspension never happens. The image below shows what this notice looks like and where to find the two things that control everything: the notice date and the balance being counted toward the $10,000 threshold.

⏱ Your deadline: 60 days from the date printed on your Notice of Proposed Driver License Suspension. Check the exact date on your copy. If the window closes with no payment in full, no payment agreement, and no valid exemption, the Tax Department refers your license to the DMV for suspension.

Why New York can suspend your license over back taxes

New York Tax Law §171-v lets the state suspend your driver's license when you owe $10,000 or more in past-due state tax debt. That threshold counts everything together — tax, penalties, and interest, stacked across every open year. A $7,500 assessment that has grown with penalties, or three smaller years combined, crosses the line just as surely as one big bill.

Two agencies run the program in sequence. The Department of Taxation and Finance (DTF) decides you meet the criteria and sends the Notice of Proposed Driver License Suspension. The Department of Motor Vehicles (DMV) actually suspends — but only after DTF refers you, and DTF can only refer you after your 60 days run out.

Understand what kind of weapon this is. A bank levy takes money; a license suspension takes leverage. It costs the state nothing, touches no protected income, and works on people traditional collection can't reach — which is exactly why it exists. If your income is Social Security, New York can't garnish it, so the license became the pressure point instead. (More on that in the worked example below.)

One point of frequent confusion: this is purely a state program. The IRS cannot take your license — its equivalent pressure tool is passport revocation for tax debt, which triggers at $66,000 of federal debt in 2026. If you owe both New York and the IRS, the two systems run on separate clocks, and it usually matters which one you resolve first.

What happens if you ignore the 60-day notice

If the 60-day window closes with no payment, no agreement, and no exemption claim, the Tax Department refers your license to the DMV for suspension. The sequence from there is mechanical:

- Balance assessed and unpaid. DTF bills you, adds penalties and interest monthly, and may file a NYS tax warrant — a public civil judgment and lien against everything you own.

- Balance reaches $10,000 with no agreement. DTF mails the Notice of Proposed Driver License Suspension. Your 60-day window starts on the notice date.

- Day 60 passes. DTF refers you to the DMV, which sends its own suspension order with a short final window — typically about 15 more days — before the suspension takes effect.

- Your license is suspended, indefinitely. There is no automatic expiration; it lifts only when the tax side is resolved. Driving anyway is aggravated unlicensed operation — a criminal charge, not a ticket.

- Collection continues in parallel. The suspension pays nothing toward the debt. Warrant enforcement — bank levies, liens on property, income executions against any wages — keeps running, and New York can enforce a tax warrant for up to 20 years, twice the IRS's collection window.

Stage 4 is where lives actually break. A suspended license means insurance complications, a criminal record if you drive anyway, and — for anyone outside a city with transit — no independent way to get to a doctor. Every option in the next section is available today; almost none of them get easier after the referral goes to the DMV.

Holding a Notice of Proposed Driver License Suspension?

Get it reviewed free before the 60-day window closes. An experienced tax professional will verify the balance, check the exemptions, and map the payment terms that keep you driving — no pressure, no obligation.

Your options to stop a NYS license suspension for tax debt

A payment agreement entered before the 60-day deadline stops the suspension referral — you do not have to pay the full balance to keep your license. That single fact changes the whole problem: the question isn't "how do I find the money," it's "which resolution can I get in place within 60 days." (For the general playbook on negotiating tax debt on your own, see how to settle tax debt yourself — everything below is what's specific to New York's license program.)

| Option | Who it fits | Effect on your license |

|---|---|---|

| Pay in full | Anyone who can raise the funds (savings, family, asset sale) | Ends the referral entirely; fastest and cheapest long-term |

| Installment Payment Agreement (IPA) | Most taxpayers; online setup typically available at $20,000 or less payable within 36 months, financial disclosure above that | Stops the suspension while you stay current on payments |

| Statutory exemption | Public assistance or SSI recipients; wages already garnished for this tax debt or for child/spousal support; pending innocent spouse claim | Blocks the suspension for as long as the exemption applies |

| Challenge the notice | Wrong person, balance already paid, or liability not actually yours — the grounds are narrow | Cancels the referral if you prove it with documentation |

| NYS Offer in Compromise | Insolvency or documented undue economic hardship (Form DTF-4.1 plus financial statement DTF-5) | Acceptance settles the debt below $10,000 — and with it, the license exposure |

| Bankruptcy | Limited — generally only older income tax years qualify for discharge | The automatic stay pauses state collection while the case is open |

The Installment Payment Agreement is the workhorse. For most people holding this notice, the realistic move is an IPA with the Tax Department — the full mechanics, terms, and setup process are in our guide to NYS installment payment agreements. The key license-specific point: the agreement must be in place before day 60, not merely requested, so don't start on day 55. And the protection is conditional — miss payments and default, and the suspension referral comes back.

Read the exemptions carefully before assuming one covers you. The statute exempts people receiving public assistance or Supplemental Security Income (SSI). Regular Social Security retirement benefits are not SSI — this trips up retirees constantly. SSI is the separate needs-based program; if your check is ordinary retirement or survivor benefits, the exemption doesn't automatically apply, no matter how tight your budget is. The garnishment exemption is similarly specific: it protects you if your wages are already being taken for this tax debt or for child or spousal support obligations.

Challenges are narrow by design. This notice is not the place to argue you shouldn't owe the tax — that fight belonged to the assessment stage. The grounds that work here are identity errors, debts already paid, and exemptions DTF missed. If the underlying assessment itself is inflated (a state return that missed deductions, or an estimated assessment for a year you never filed), fixing the return is sometimes the better lever — see amending a return to lower a tax debt. Dropping the true balance below $10,000 removes the license exposure entirely.

The NYS Offer in Compromise is real but strict. New York settles debts for individuals who are insolvent, discharged in bankruptcy, or who can show that full payment would create undue economic hardship — the application is Form DTF-4.1 with a full financial statement on Form DTF-5. It is a documentation-heavy, means-tested review, not a discount program, and while it's pending you should confirm directly with DTF how the license referral will be handled rather than assume it pauses. On the bankruptcy route, only certain older income taxes are dischargeable — the tests are covered in Chapter 7 vs 13 for tax debt — and it's rarely worth filing over the license alone.

| Balance owed to NYS | License exposure | Realistic path |

|---|---|---|

| Under $10,000 | None under §171-v — but warrants, levies, and refund offsets still apply | Pay in full or set up an IPA online before penalties push you over the threshold |

| $10,000 – $20,000 | Suspension-eligible | Online IPA (up to 36 months) is usually the fastest fix inside the 60-day window |

| $20,000 – $100,000 | Suspension-eligible; tax warrant likely | IPA with financial disclosure (DTF-5); hardship terms or an OIC if the numbers support it |

| Over $100,000 | Suspension plus aggressive warrant enforcement | Negotiated IPA or OIC with full financials — professional representation earns its cost here |

Say you owe NYS $83,100 on a fixed income: a worked example

Here's a hypothetical to make the math concrete. Say you're retired, your income is a Social Security check plus a small pension, and the notice says you owe New York $83,100 — old self-employment years, penalties, and interest that compounded while the letters went unopened.

First, what New York can't do: it can't garnish your Social Security — federal law shields those benefits from state income executions, and if a bank levy hits your account, federal rules require the bank to protect roughly two months of directly deposited benefits. That protection is precisely why the state reaches for your license instead. It's the one thing you have that DTF can take without touching a protected dollar.

Now the payment math. At $83,100 you're far above the online-IPA range, so any agreement goes through financial disclosure on Form DTF-5:

- 36 months: $83,100 ÷ 36 ≈ $2,308/month, plus interest that keeps accruing. On a fixed income, almost certainly impossible.

- 72 months (if DTF agrees to a longer term): $83,100 ÷ 72 ≈ $1,154/month. Still brutal for most retirees.

- Ability-to-pay terms: suppose your Social Security and pension total $3,400/month and documented essential living expenses run $2,900. Your realistic capacity is around $500/month — and an IPA the Tax Department accepts at that level protects your license exactly as well as one at $2,308.

This is the insight the notice never spells out: the license doesn't care about the size of the payment — only that an agreement exists. And if the DTF-5 shows genuinely nothing left after essentials, that same financial statement becomes the backbone of a hardship-based Offer in Compromise on Form DTF-4.1. If you owe the IRS on top of the state balance, the federal side has its own fixed-income playbook — see retired and owing back taxes — and the state's 60-day clock usually means New York goes first.

How to respond, step by step

- Find your deadline. Locate the notice date on the first page. Your 60-day response window runs from that date, not from the day you opened the envelope — write the exact deadline down.

- Verify the balance. Log into your NYS Online Services account at tax.ny.gov and compare the assessed balance with the notice. If the debt is paid, isn't yours, or is overstated, gather proof now.

- Check the exemptions. Confirm whether you receive public assistance or SSI, already have wages garnished for this debt or for child or spousal support, or have an innocent spouse claim — any of these blocks the suspension.

- Set up a payment agreement before day 60. Pay in full if you can; otherwise request an Installment Payment Agreement. Balances of $20,000 or less payable within 36 months can usually be set up online; larger balances require financial disclosure on Form DTF-5.

- Confirm the referral is cleared. Get confirmation from the Tax Department that your resolution stopped the DMV referral. If the suspension already took effect, resolve with DTF first, then clear the DMV side, including any termination fee.

When you can handle this yourself — and when help changes the outcome

Plenty of people resolve this notice on their own, and you may be one of them. Handle it yourself if:

- You can pay in full — pay through your Online Services account, keep the confirmation, and the referral dies.

- You owe $20,000 or less and can manage 36 monthly payments — the online IPA takes minutes and doesn't require financial disclosure.

- The notice is simply wrong and you hold clean proof — a canceled payment, a satisfied warrant, an identity mix-up.

Experienced help earns its cost in the harder patterns: a large balance like $83,100 where the outcome hinges entirely on how the DTF-5 financial statement is documented and presented; a fixed income where a few hundred dollars a month of allowed expenses decides between an affordable agreement and an impossible one; a tax warrant already filed against your home; multiple unfiled years inflating the assessed balance; or a suspension that has already reached the DMV. In those cases, the difference between a well-built submission and a rushed one is measured in years of payments — get the free review before the window closes at the 2-minute form or (888) 825-7779.

Terms on your notice, decoded

- DTF vs. DMV: the Department of Taxation and Finance decides you owe and triggers the process; the Department of Motor Vehicles carries out the actual suspension. You resolve with DTF, then the DMV restores the license.

- Tax warrant: New York's version of a lien — a civil judgment filed publicly against you, attaching to your property and enforceable for up to 20 years.

- Income execution: the state's wage garnishment. It reaches wages, not Social Security benefits.

- Installment Payment Agreement (IPA): New York's monthly payment plan. An active IPA blocks the license suspension while you stay current.

- Fixed and final: a liability you can no longer protest or appeal. The license program targets fixed-and-final debts, which is why the suspension notice isn't the place to relitigate the tax.

- Restricted use license: a limited DMV license available after a tax suspension that allows essential driving, typically to work and medical care — not general driving, and generally not commercial driving.

NYS license suspension questions, answered

How much do you have to owe for NYS to suspend your license?

The threshold is $10,000 in past-due New York State tax liabilities, counting tax, penalties, and interest combined across every open year. A $7,000 balance that grows past $10,000 with penalties can trigger the program. Below $10,000 your license is safe from this specific tool, but the Tax Department can still collect through warrants, bank levies, and income executions.

Does a payment plan stop a NYS license suspension?

Yes. Entering an Installment Payment Agreement with the Tax Department before your 60-day window closes stops the suspension referral, even though the debt is not paid off. You do not need to pay the balance in full to keep your license. The protection lasts only while you stay current — defaulting on the agreement puts the suspension back on the table.

I'm retired on Social Security — can New York still suspend my license?

Yes. The statutory exemption covers people receiving public assistance or Supplemental Security Income (SSI) — regular Social Security retirement benefits are not the same thing and do not automatically exempt you. What a fixed income does give you is strong footing for a low-payment agreement or a hardship-based Offer in Compromise, both of which protect the license once in place.

Can NYS take my Social Security check for the tax debt?

No — Social Security benefits are protected by federal law from state income executions, and federal banking rules require your bank to protect roughly two months of directly deposited benefits if a levy hits the account. That protection is exactly why New York built the license suspension program: it gives the state leverage over people whose income it cannot garnish.

Can I get a restricted license if NYS suspends mine over taxes?

Often, yes. After a tax suspension takes effect, you can apply to the DMV for a restricted use license that allows limited driving — typically to and from work and medical appointments. It is not a full license: it will not cover general errands, and it generally will not authorize commercial driving, so CDL holders have far more at stake and should act before the 60-day window closes.

Does the IRS suspend driver's licenses too?

No. Driver's licenses are issued by states, and the IRS has no authority over them. The federal pressure tool that works the same way is passport certification: at $66,000 or more in seriously delinquent federal tax debt (the 2026 threshold), the IRS can certify you to the State Department, which can deny or revoke your passport. If you owe both, the two clocks run independently.

What happens if I drive while my license is suspended for tax debt?

Driving on a suspended New York license is a criminal offense — aggravated unlicensed operation — not a traffic ticket. A stop can mean arrest, fines, and a criminal record, and your insurer may raise rates or drop you once the suspension surfaces. If your license has already been suspended, resolving the tax side with DTF is the only path back; driving through it compounds the problem.

How do I get my license back after a NYS tax suspension?

Resolve the tax side first — pay in full, enter an Installment Payment Agreement, or document a valid exemption — and the Tax Department notifies the DMV to lift the suspension. The DMV side may involve a suspension termination fee before your driving privilege is fully restored, so confirm with both agencies and keep written proof of the resolution in your car until your record updates.

Your next 24 hours

- Find the notice date on the first page of your Notice of Proposed Driver License Suspension and count 60 days forward — that date is your entire strategy's boundary. Write it somewhere you'll see it.

- Gather three things: the notice itself, your most recent state and federal returns, and a one-page snapshot of your monthly income (Social Security, pension, anything else) and essential expenses. That's everything a payment agreement or hardship case is built from.

- Get the free case review before the 60-day window narrows your options — the 2-minute form at claritytaxrelief.com/#consult or (888) 825-7779. An experienced tax professional will confirm the balance, screen every exemption, and map the agreement that keeps you driving.

Primary sources: the New York State Department of Taxation and Finance administers the suspension program, payment agreements, and the state Offer in Compromise; the New York Department of Motor Vehicles handles the suspension itself and restricted use licenses.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.