California State Taxes

FTB Financial Hardship & Currently Not Collectible Status in California (2026)

The short answer: if paying the California Franchise Tax Board (FTB) would leave you unable to cover basic living costs, you can request FTB financial hardship — also called Currently Not Collectible (CNC) status. It pauses garnishments and levies. The debt and interest remain, and the FTB reviews your finances over time.

Can't pay the FTB without going without?

Send us your notice and a quick picture of your monthly budget. An experienced tax professional will tell you whether you qualify for hardship status — and which California option saves you the most — free, confidential, no pressure.

⏱ Why timing matters: there is no single deadline to ask for hardship status, but if you've received a wage garnishment order or a bank levy, your bank funds can be held and sent to the FTB quickly. Request hardship before the next collection action posts — once money leaves your account, it's far harder to get back.

What FTB financial hardship status actually is

FTB financial hardship — the FTB's version of Currently Not Collectible status — is a determination that you genuinely can't pay your state tax debt right now without going without food, rent, utilities, or other necessities. When the FTB agrees, it stops active collection: no new wage garnishments, no new bank levies.

Be clear on one thing: hardship status is a pause, not an eraser. The balance stays. Penalties and interest keep growing in the background. The FTB can still file a state tax lien and keep any state refund or lottery winnings. The relief is breathing room, not forgiveness — but when you're choosing between rent and the FTB, breathing room is exactly what you need.

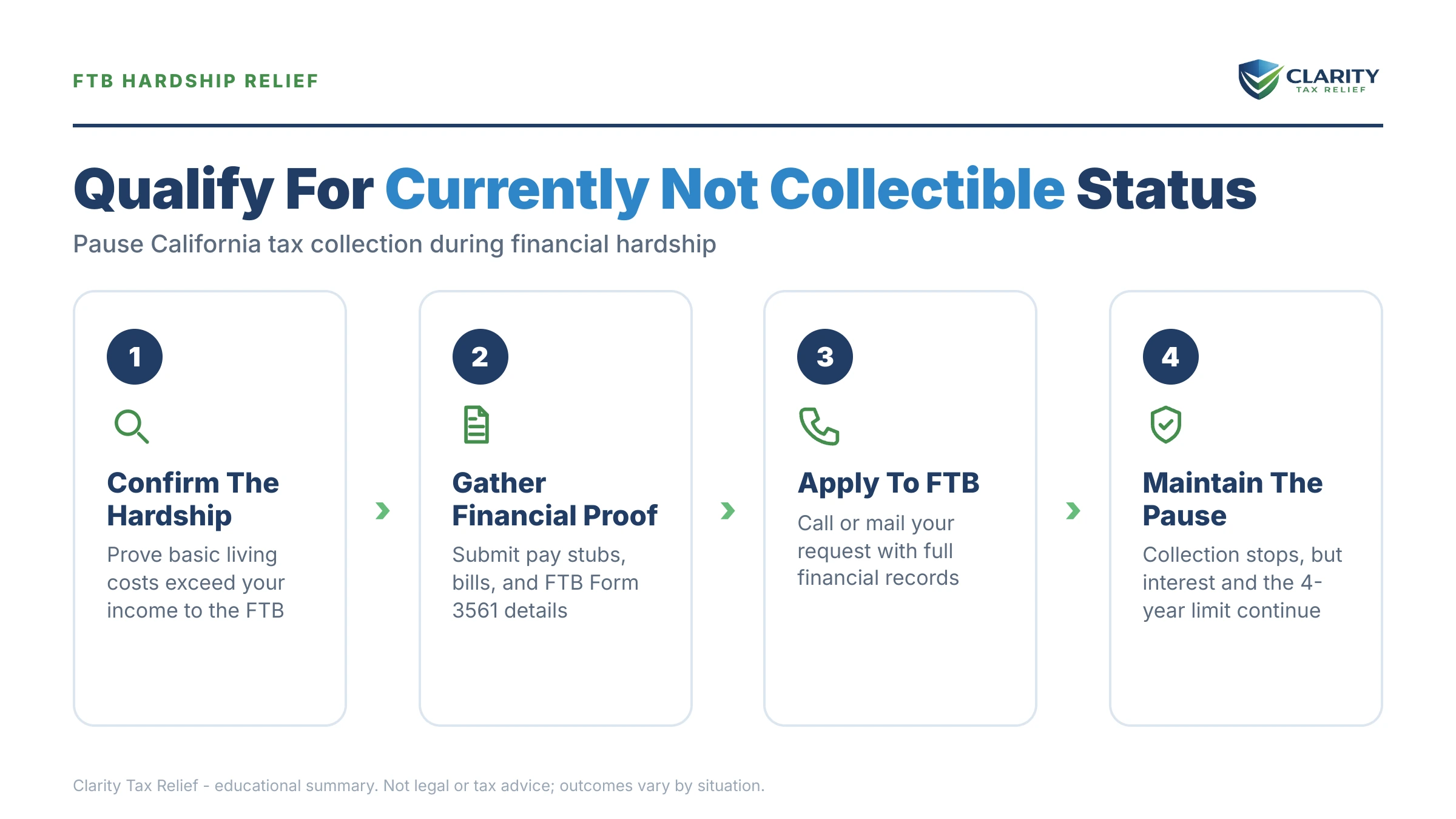

How the FTB decides if you qualify

The FTB looks at one basic question: after your necessary monthly living expenses, do you have money left over to pay the state? If the honest answer is little or nothing, you likely qualify for hardship.

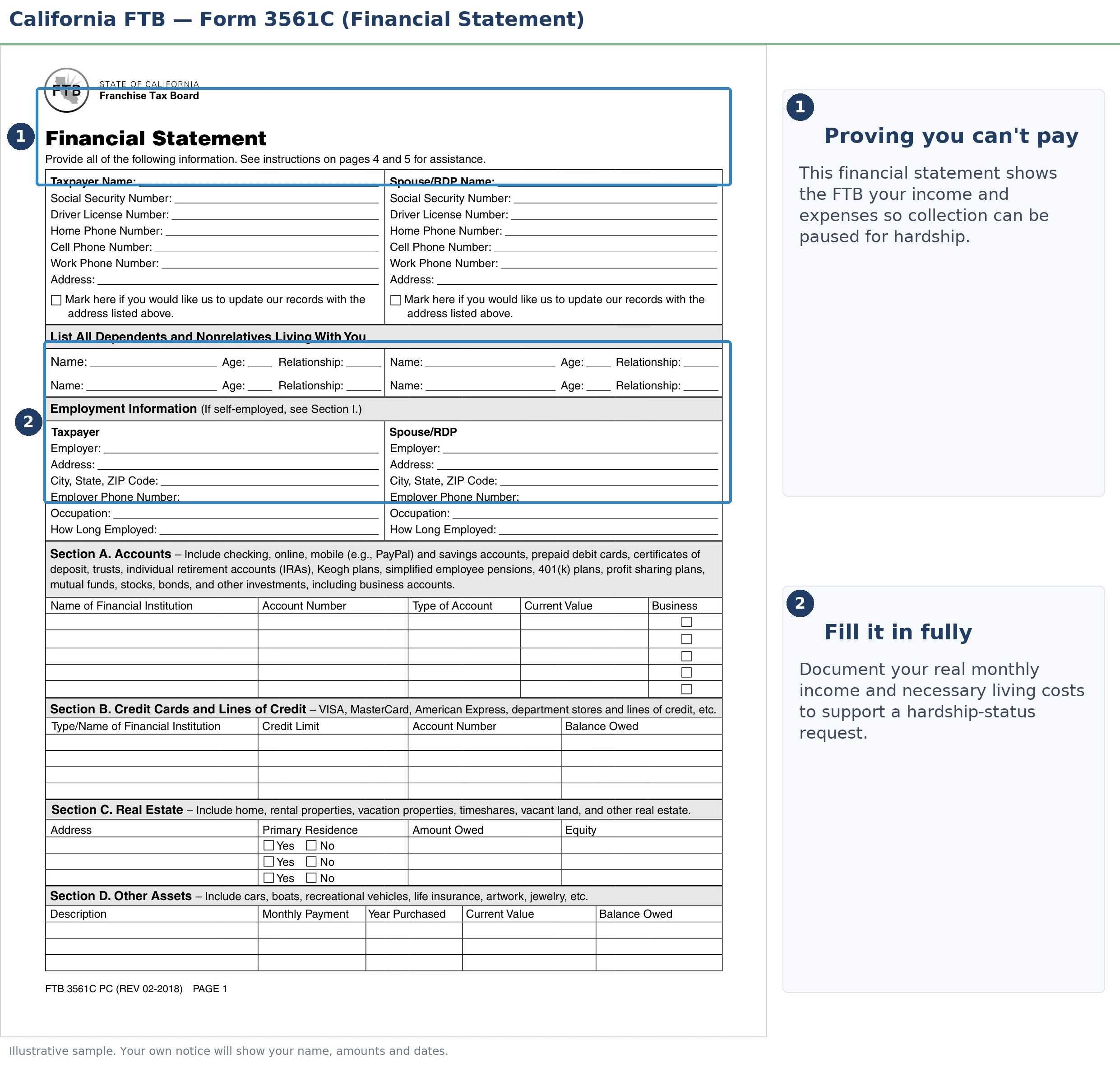

You prove this with a financial statement — FTB Form 3561, the California financial statement — backed by documents like pay stubs, recent bank statements, rent or mortgage records, and utility bills. The FTB compares your income against allowable living expenses (housing, food, utilities, transportation, health care, and similar basics) to see what, if anything, you could realistically pay.

Things that strengthen a hardship case:

- Income that barely covers — or falls short of — your basic monthly bills.

- Job loss, reduced hours, disability, or serious illness in the household.

- Fixed income from Social Security, disability, or a pension.

- No equity in assets the FTB could reach (or assets you genuinely need to live and work).

What happens if you do nothing

The FTB's collection system is automated and persistent. If you ignore the bills, the sequence keeps moving:

- Notices and demands — billing letters and, for nonfilers, a Demand to File. The balance grows each month.

- State tax lien — the FTB can record a lien that attaches to your property and damages your credit.

- Order to Withhold / wage garnishment — the FTB can take a large share of your paycheck. See how much the FTB can garnish from your paycheck before this hits.

- Bank levy and refund intercept — the FTB can pull funds from your bank account and seize your state tax refund.

Hardship status is the tool that stops this machine when you truly can't pay. The earlier you act, the more of your money stays where it belongs — with you.

FTB hardship vs. your other California options

Hardship isn't your only path. It's the right fit when you can't pay anything right now. Other options fit different situations:

- Installment agreement — a monthly payment plan when you can afford something each month. Details are on the FTB's payment plans page.

- Penalty abatement — if a reasonable cause like illness or disaster led to the debt, FTB penalty abatement may remove some charges.

- Offer in Compromise — settling for less than the full balance when your finances genuinely can't cover it. The FTB runs the numbers; anyone promising to settle your debt "for pennies on the dollar" before reviewing your finances is selling you something.

- Currently Not Collectible (hardship) — the focus of this guide, for when paying anything would cause real hardship.

Not sure which one is right? Our overview of what to do when you owe California state taxes and can't pay walks through each path in plain English.

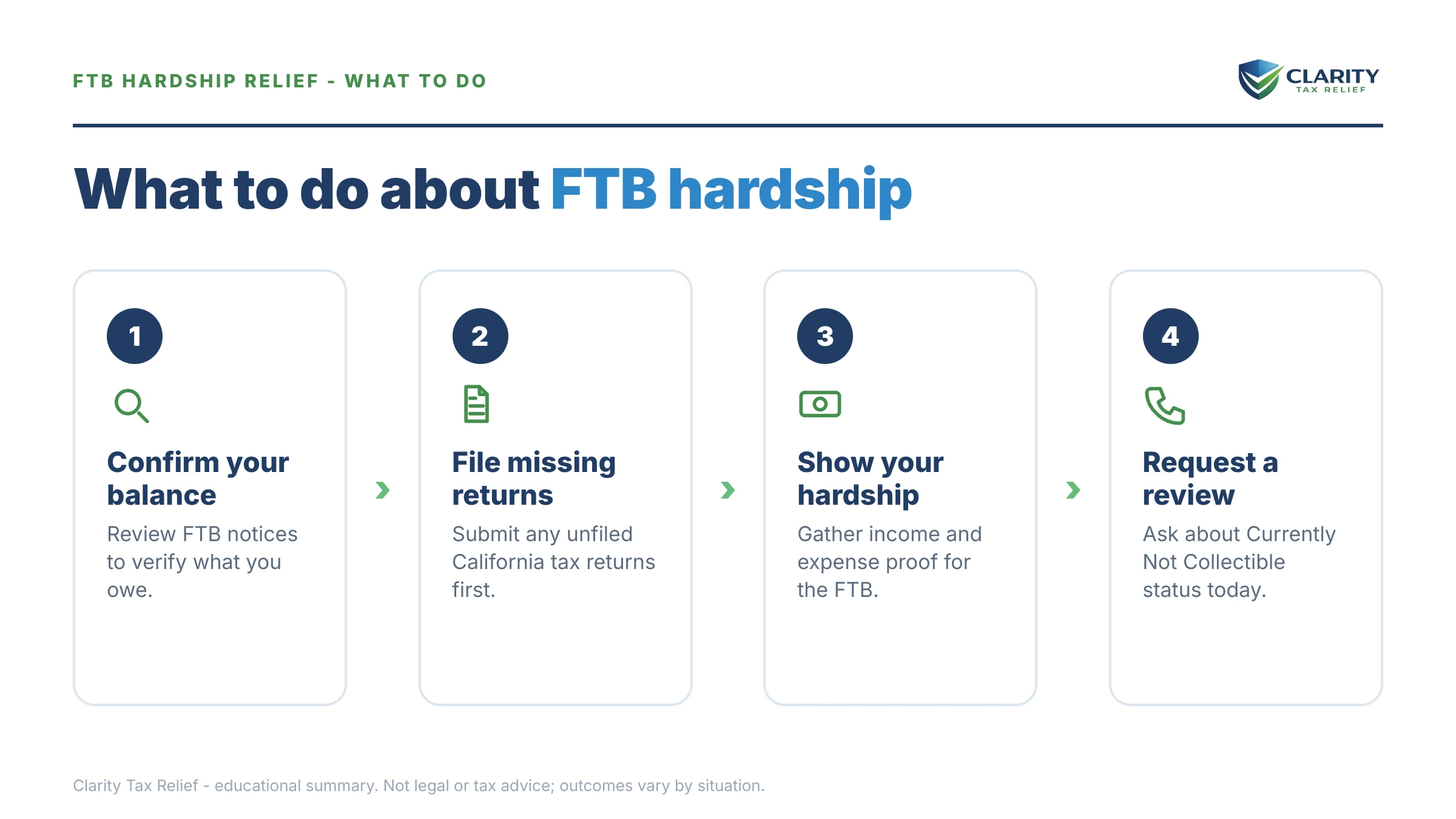

How to request FTB hardship status, step by step

- File any missing returns first. The FTB usually won't grant relief while you have unfiled years. Get current before you ask.

- Gather your numbers. Collect pay stubs, bank statements, and a list of your monthly living expenses with proof.

- Complete FTB Form 3561. This financial statement is how you show that paying would create hardship. Be accurate and complete — gaps slow everything down.

- Submit and contact the FTB. Send the form and ask for your account to be placed in hardship/Currently Not Collectible status. You can reach the FTB through the contact options on ftb.ca.gov.

- Ask to release any active garnishment or levy. If money is already being taken, request a release based on hardship as part of your application.

- Keep filing and stay reachable. The FTB reviews hardship accounts periodically — often yearly. File future returns on time and respond to review letters so the pause stays in place.

One reminder for California: the FTB's collection statute runs up to 20 years — much longer than the IRS's 10-year clock. Hardship status can keep you protected for a long stretch, but the debt doesn't quietly disappear. Plan for the day your finances improve.

FTB financial hardship questions, answered

Does FTB financial hardship status erase my tax debt?

No. Hardship status (Currently Not Collectible) pauses active collection — it does not cancel what you owe. Penalties and interest keep adding up, and the FTB can still file a lien or keep your state tax refund. The balance only goes away if you pay it or California's 20-year collection clock runs out.

How do I qualify for FTB financial hardship?

You qualify when your monthly income barely covers — or doesn't cover — your basic living expenses like rent, food, utilities, and transportation. You show this by filing FTB Form 3561, the California financial statement, with proof such as pay stubs, bank statements, and monthly bills. The FTB compares your income to allowable expenses to decide.

Can the FTB still garnish my wages if I'm in hardship status?

Once your account is approved as Currently Not Collectible, the FTB should stop new wage garnishments and bank levies while the status is active. If a garnishment is already running and paying it would create real hardship, ask the FTB to release or reduce it as part of your hardship request.

How long does FTB Currently Not Collectible status last?

There is no fixed end date, but the FTB reviews hardship accounts periodically — often once a year. If your income rises or your situation improves, the FTB can lift the status and restart collection. As long as your finances still qualify, the pause continues until the debt is paid or California's 20-year statute expires.

Is FTB hardship status the same as the IRS Currently Not Collectible status?

They work the same way — both pause collection when paying would create financial hardship — but they are separate programs run by separate agencies. Getting IRS Currently Not Collectible status does not put your California debt on hold. You must apply to the FTB separately for state relief.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS and FTB programs depends on individual facts and circumstances; no outcome is guaranteed.