California / FTB

Owe California State Taxes and Can't Pay? Your Options (2026)

The short answer: if you owe California state taxes and can't pay, you still have real options. The Franchise Tax Board (FTB) offers monthly payment plans, hardship status that pauses collection, penalty relief, and — for those who qualify — a settlement for less than the full balance. Acting before the FTB levies or garnishes is the key.

Owe California and feeling stuck?

Send us a photo of your FTB notice. An experienced tax professional will explain exactly where you stand and which options you actually qualify for — free, confidential, no pressure.

⏱ Why timing matters: the FTB adds a late-payment penalty plus interest, and after a few unanswered notices it can issue an Order to Withhold (bank levy) or an Earnings Withholding Order (wage garnishment) — often within 30 to 60 days of a final notice. Setting up an arrangement before that point keeps the money in your account.

Why you owe and why it grows so fast

If you owe California state taxes and can't pay, the balance on your notice is usually some mix of three things: tax you reported but didn't fully pay, an estimated-tax shortfall, and the penalties and interest the FTB stacks on top. California's late-payment penalty and ongoing interest mean the number you see today is not the number you'll see in six months.

Not sure what your letter even means? Start with our FTB notice decoder to identify exactly which notice you're holding and where it falls in the collection process. Knowing the notice tells you how much time you have.

What happens if you ignore the FTB

California's collection system, like the IRS's, runs largely on automation. Skip the early notices and the FTB escalates in a predictable order — each step with more teeth than the last:

- Notice of Tax Due / Statement of Balance — the first bills. Penalties and interest are already running.

- Demand for payment — reminder notices, plus a cost-recovery and collection fee added to your balance.

- Final notice before collection action — your warning that levies and garnishments are next.

- Order to Withhold — a bank levy that can sweep funds from your account.

- Earnings Withholding Order — wage garnishment taken straight from your paycheck.

- State Tax Lien & refund intercept — a public lien against your property, plus seizure of state refunds and even lottery winnings.

Two California-specific facts make ignoring the bill especially risky. First, the FTB generally has 20 years to collect — double the IRS's 10-year window. Second, the FTB can intercept your refunds and tack on collection and cost-recovery fees that quietly inflate the debt. Waiting almost never helps.

If you can't pay in full: your real options

The notice makes it sound like "pay now or face collection." In reality, the FTB has several programs, and the right one depends on your numbers:

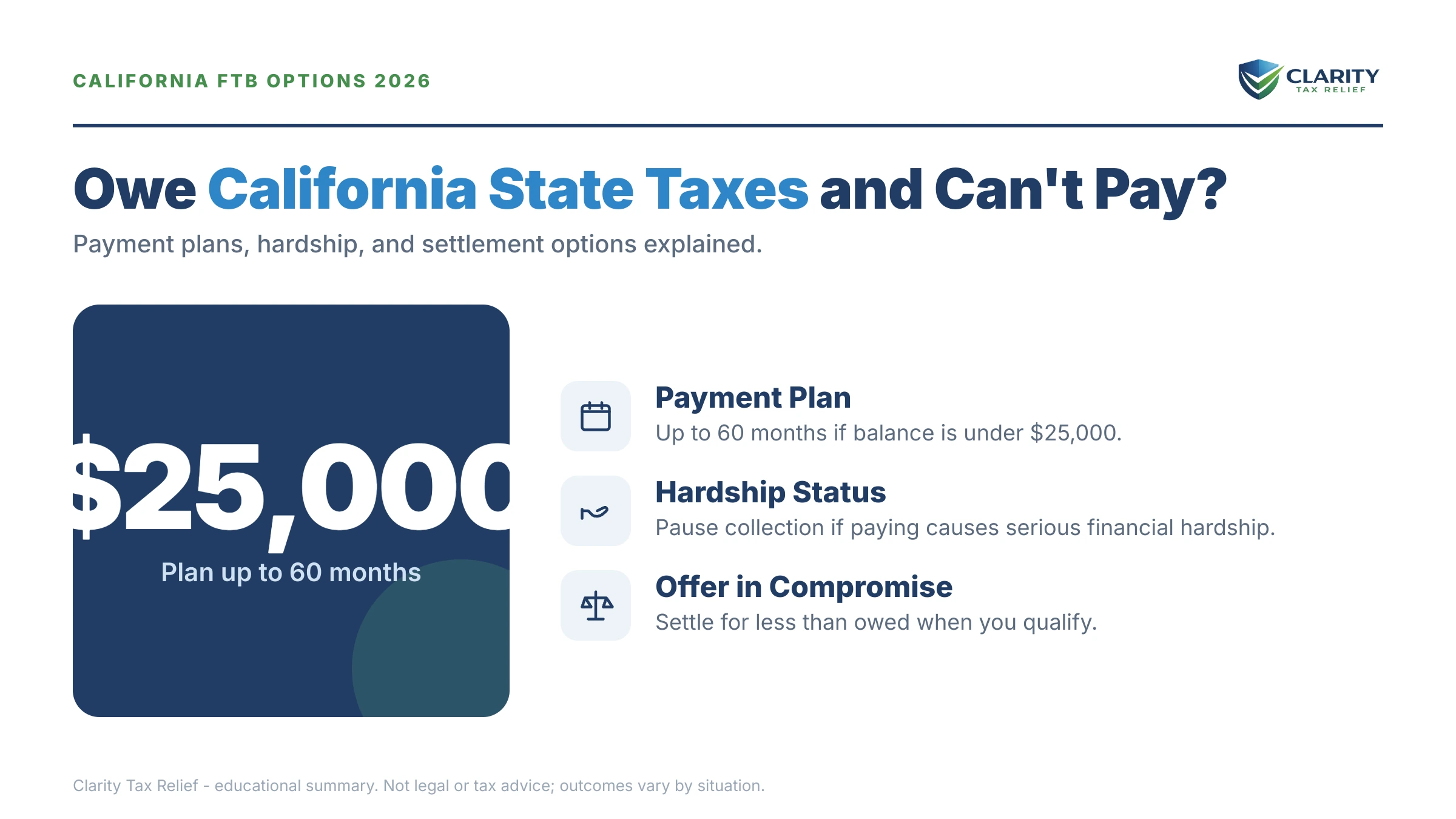

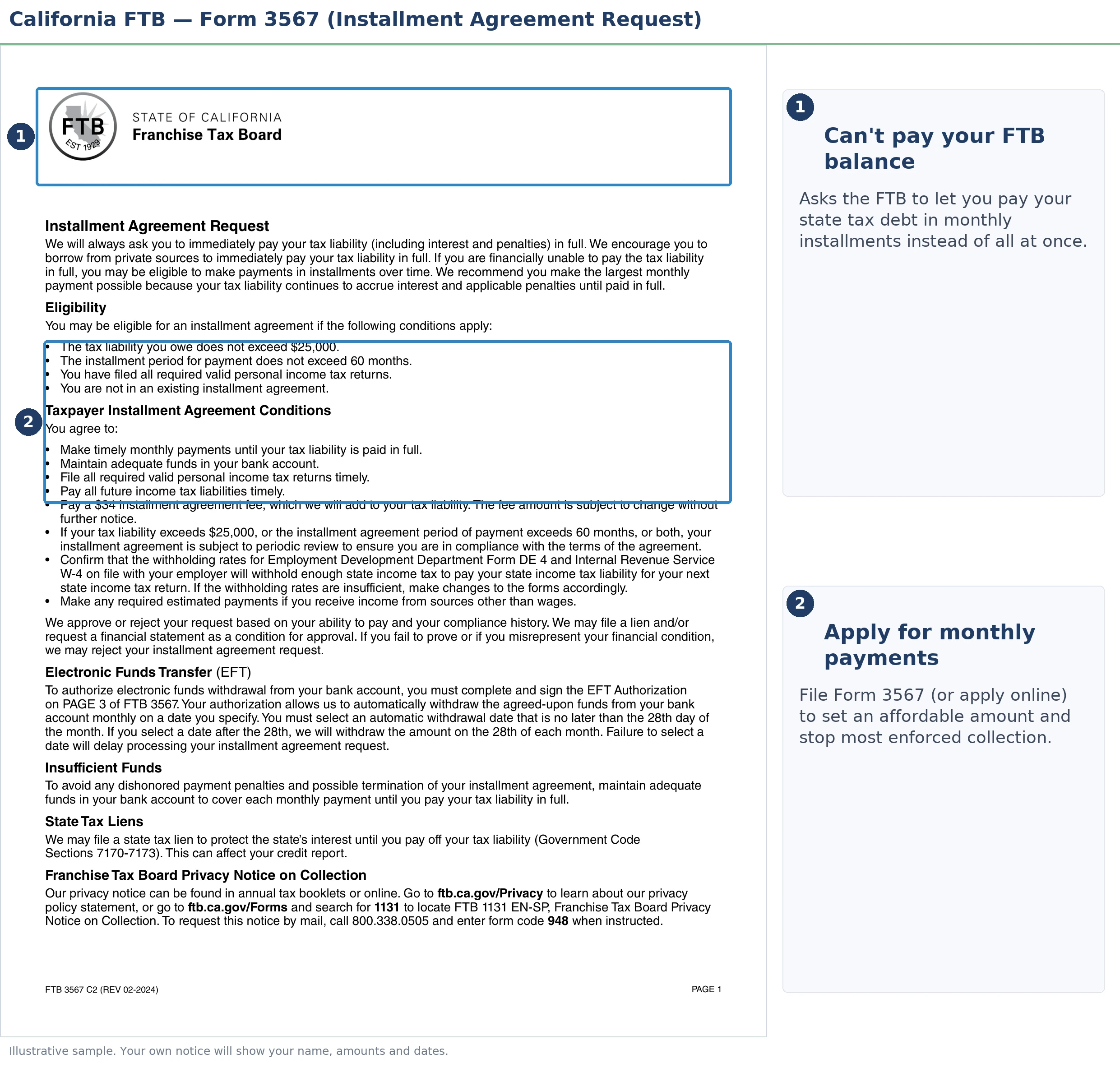

- Installment agreement (payment plan) — a monthly plan. Individuals who owe $25,000 or less and can pay within 60 months can often set one up online without detailed financials. The FTB's own page on payment plans walks through eligibility.

- Financial hardship / Currently Not Collectible — if paying anything would leave you unable to cover basic living costs, the FTB can pause active collection. The debt stays, but levies and garnishments stop. See our guide to FTB financial hardship status.

- Offer in Compromise (settlement) — the FTB can accept less than the full balance when you genuinely can't pay it now or in the foreseeable future. This is real, but it is not automatic and it is not "pennies on the dollar" for everyone — anyone promising a guaranteed settlement before reviewing your finances is selling you something. The FTB runs the math on your income, assets, and expenses first.

- Penalty abatement — if illness, a disaster, or another circumstance beyond your control caused the late payment, you may qualify for FTB penalty abatement and reasonable-cause relief, which can shrink the balance.

For most payment plans and hardship requests above the simple threshold, the FTB asks for a financial statement. That's FTB Form 3561, where you lay out income, expenses, and assets. How you complete it directly shapes the monthly payment the FTB asks for — so accuracy matters.

How to respond, step by step

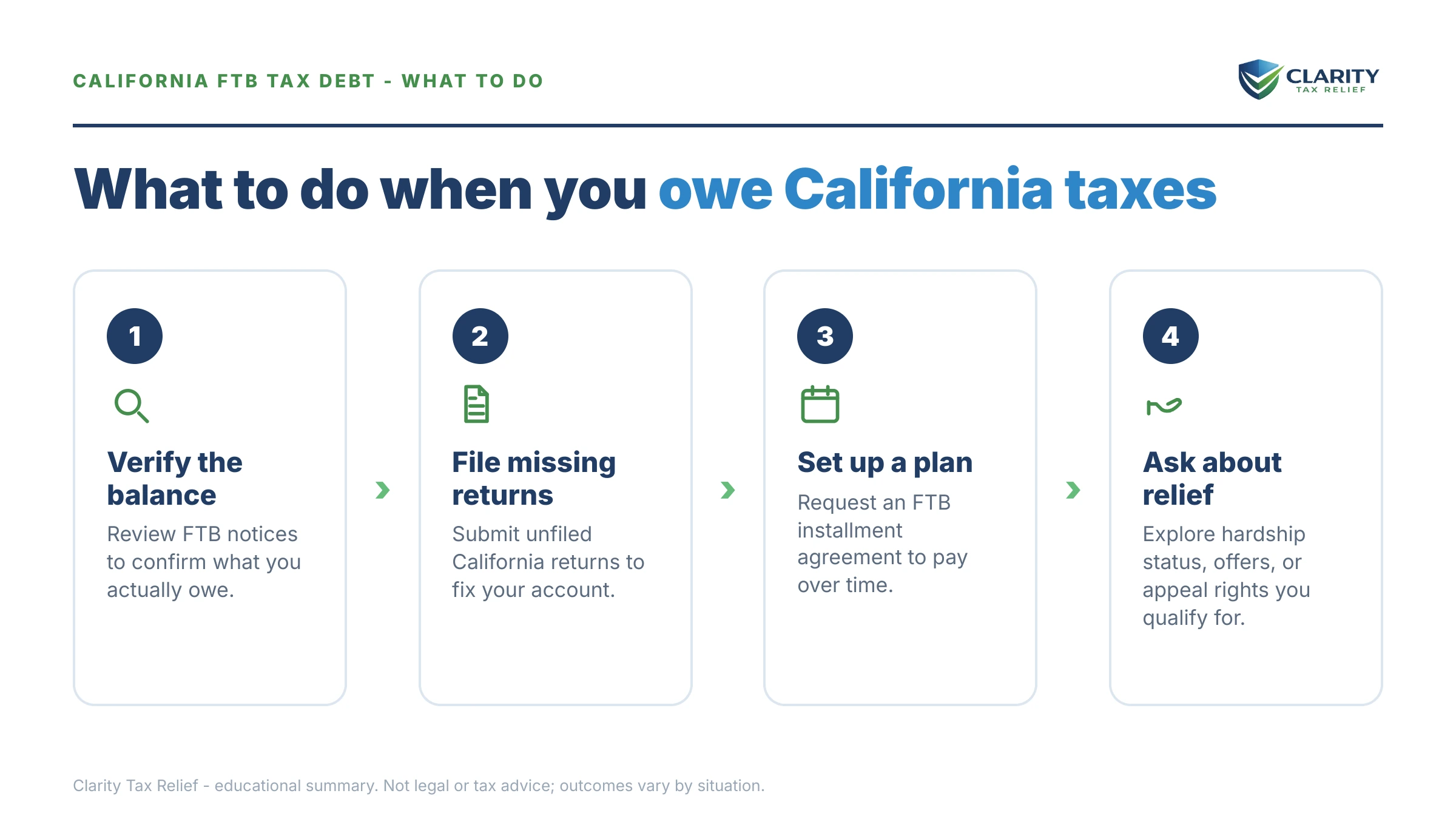

- Confirm the balance is right. Log into your MyFTB account and compare it to your return. Notices and recent payments sometimes cross in the mail.

- File any missing returns first. If the FTB sent a Demand to File, it may estimate your income high. Filing the real return usually lowers the number — fix this before negotiating anything.

- Pick the option that fits. Can pay over time? Request a payment plan. Can't cover basics? Pursue hardship status. Think you qualify for less? Explore a settlement.

- Set it up before the deadline on your notice. Even a plan you start today stops the bank levy and wage garnishment that would otherwise follow.

- Coordinate with any IRS debt. If you owe both, read FTB vs IRS: which back taxes to pay first so you don't solve one problem while the other one explodes.

A quick worked example

Say you filed your California return showing $9,000 due but couldn't pay. Add the late-payment penalty and a few months of interest, plus a collection fee once the bill goes unanswered, and you might owe closer to $10,500 before long. Set up a 60-month installment agreement and you'd pay a manageable fixed amount each month while the levy threat disappears. Ignore it instead, and that same balance could trigger a bank levy or wage garnishment — and keep climbing for up to 20 years. The math almost always favors acting early.

Owe California state taxes you can't pay? Questions, answered

What happens if I owe California state taxes and can't pay?

Interest and penalties keep growing, and the Franchise Tax Board can eventually garnish wages, levy your bank account, and file a state tax lien. But you have options before that: a monthly installment agreement, hardship status that pauses collection, penalty relief, or in some cases a settlement for less than the full balance.

Does the California Franchise Tax Board offer payment plans?

Yes. The FTB offers installment agreements. Individuals who owe $25,000 or less and can pay it off within 60 months can often set one up online without detailed financial paperwork. Larger balances and business debts require a financial statement on Form 3561 and usually a closer review.

Can California reduce or settle my tax debt?

The FTB has an Offer in Compromise program for taxpayers who genuinely cannot pay the full balance now or in the foreseeable future. It is not pennies on the dollar for everyone — the FTB reviews your income, assets, and expenses first. Anyone promising a guaranteed settlement before reviewing your finances is selling you something.

How long does California have to collect a tax debt?

The FTB generally has 20 years from the date the assessment becomes final to collect a tax debt — far longer than the IRS's 10-year window. That long timeline is one reason ignoring an FTB balance rarely works and why acting early matters.

Should I pay the FTB or the IRS first?

It depends on which agency is closer to enforcing collection and how each debt affects your finances. Because California's collection powers and timeline differ from the IRS, the right order isn't automatic. An experienced tax professional can map both debts and tell you which to prioritize.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS and FTB programs depends on individual facts and circumstances; no outcome is guaranteed.