California / FTB

California Residency Audit: Are You Still a CA Resident? (2026)

The short answer: a California residency audit is the Franchise Tax Board (FTB) checking whether you really moved away — or whether you still owe California income tax as a resident. There's no magic day count. The FTB weighs where the center of your life is, so your job is to prove your closest connections moved out of state.

Got an FTB residency audit letter?

Send us a copy. An experienced tax professional will read it, explain exactly what the FTB is testing, and map out how to prove your move — free, confidential, no pressure.

⏱ Watch your deadlines: an FTB audit letter usually gives you about 30 days to respond before the auditor draws conclusions from missing information. If the audit ends in a Notice of Proposed Assessment, you generally have 60 days to file a protest. Miss these windows and your options shrink fast.

Why the FTB opened a residency audit

California has one of the highest income tax rates in the country, so when someone with real income claims they left, the FTB pays attention. A California residency audit usually starts because something in the data looks like you may still be a resident on paper even after a move.

Common triggers include:

- Filing a part-year or nonresident return after years of full-year California returns.

- A large one-time income event — selling a business, exercising stock options, a big capital gain — in the year you claim you left.

- Keeping a California home, even a second home or one you rent out.

- A mismatch between the address on your federal return and your California filing.

- Data the FTB pulls from the IRS, other state agencies, and even property and DMV records.

The system is automated and unforgiving of loose ends. The FTB isn't accusing you of fraud — it's asking you to back up where you actually live. Your job is to answer with records, not arguments.

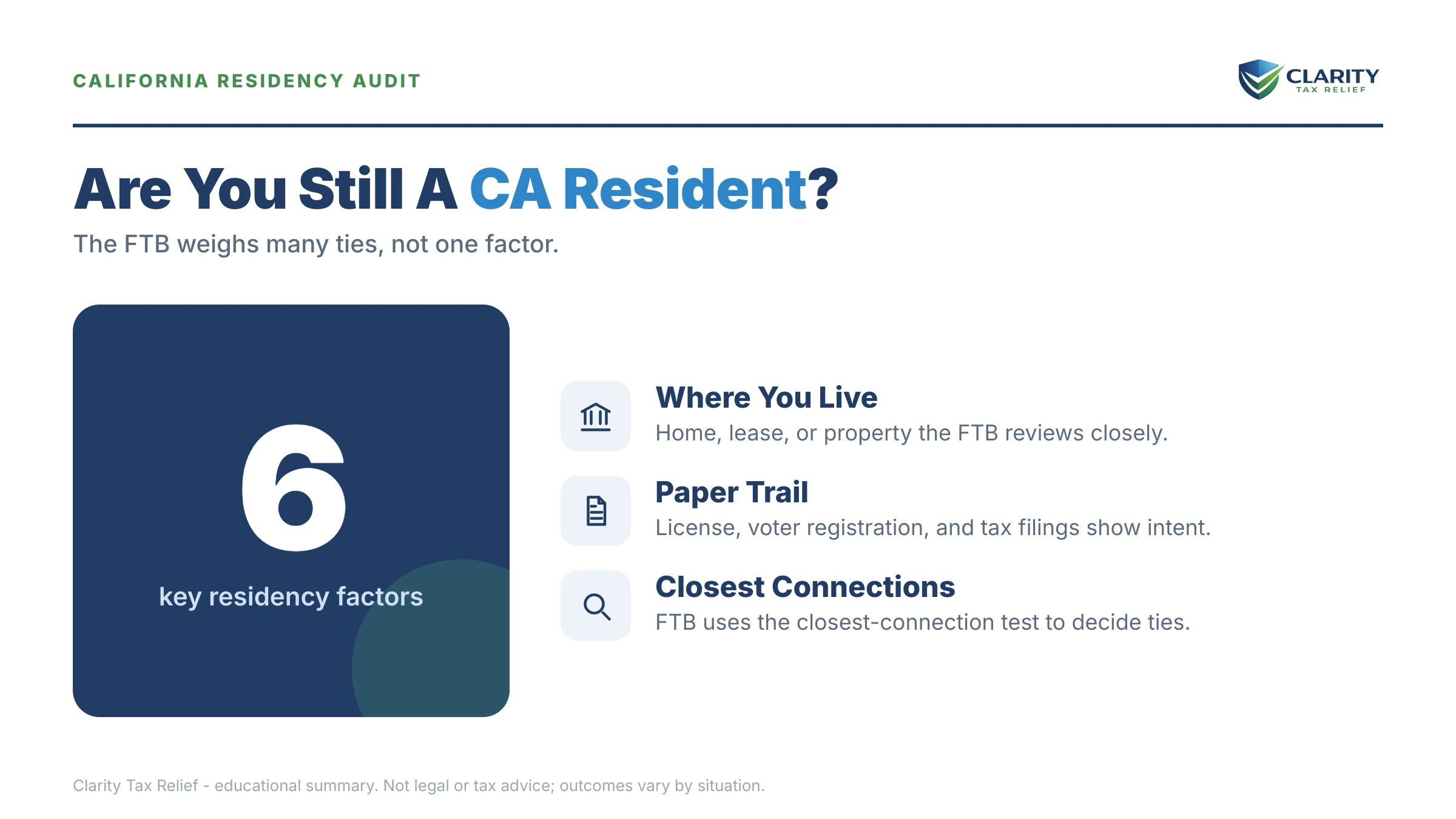

How California decides if you're still a resident

This is the part most people get wrong. California does not use a single 183-day rule to decide general residency. Spending fewer than half the year in the state does not automatically make you a nonresident.

Instead, the FTB applies a "closest connections" test. It asks where the center of your life is by weighing dozens of factors. No single one decides it — but together they paint a picture. The FTB's own guidance lives in FTB Publication 1031, Guidelines for Determining Resident Status.

Factors the auditor looks at include:

- Where your main home is, and how much time you spend in each location.

- Where your spouse and children live and go to school.

- Where your cars are registered and where you hold a driver's license.

- Where you're registered to vote.

- Where your doctors, dentists, accountants, and attorneys are.

- Where your bank accounts and main business ties are.

- Where your professional licenses and memberships are held.

The lesson: leaving California isn't just buying a plane ticket. It's moving the proof of your life. A "safe harbor" exists for certain employees on long-term work contracts abroad, but it has strict rules and doesn't cover most movers.

What happens if you ignore the audit

An FTB residency audit doesn't go away if you stop replying. It escalates on a track, and each step gives you fewer good choices:

- Audit letter / information request — the FTB asks for documents. You are here. Cooperate and you control the story.

- Notice of Proposed Assessment (NPA) — if the auditor concludes you were a resident, the FTB bills the tax plus penalties and interest. You generally have 60 days to protest.

- Final assessment — if you don't protest in time, the amount becomes legally owed.

- Collections — once final and unpaid, the FTB can file a California state tax lien, levy bank accounts, and garnish wages. If you don't respond at all, the FTB can also issue an estimated assessment under its nonfiler enforcement process.

The faster you engage, the more likely the audit ends with no change — or a far smaller bill than an auditor would assume from silence.

A simple worked example

Say you sold a business in 2024 for a $2,000,000 gain and claimed you became a Texas resident that January. California's top marginal rate is over 13%. If the FTB decides you were still a California resident when the sale closed, the tax on that gain alone could exceed $260,000 — before penalties and interest.

Now flip it. If you can show your home, family, driver's license, voter registration, and day-by-day calendar all moved to Texas before the sale, that same gain may be entirely outside California's reach. The records you kept at move-out — not the arguments you make later — decide which version wins.

What records win a California residency audit

Residency audits are won with contemporaneous, consistent paperwork. Build a file that shows your life genuinely relocated:

- New state driver's license and vehicle registration, dated as early as possible after the move.

- Voter registration in your new state (and cancellation of California registration).

- A lease or deed for your new primary home, plus utility bills in your name.

- A day-count calendar backed by cell phone location data, credit card charges, and travel records showing where you actually were.

- Moving company receipts and shipment records.

- New doctors, dentists, and other professionals in your new state.

- Updated estate documents — will, trust, and powers of attorney — naming your new state.

If you kept a California home, be ready to explain why and to show it's not your main residence. Gaps and contradictions are what auditors seize on, so consistency across every document matters more than any single item.

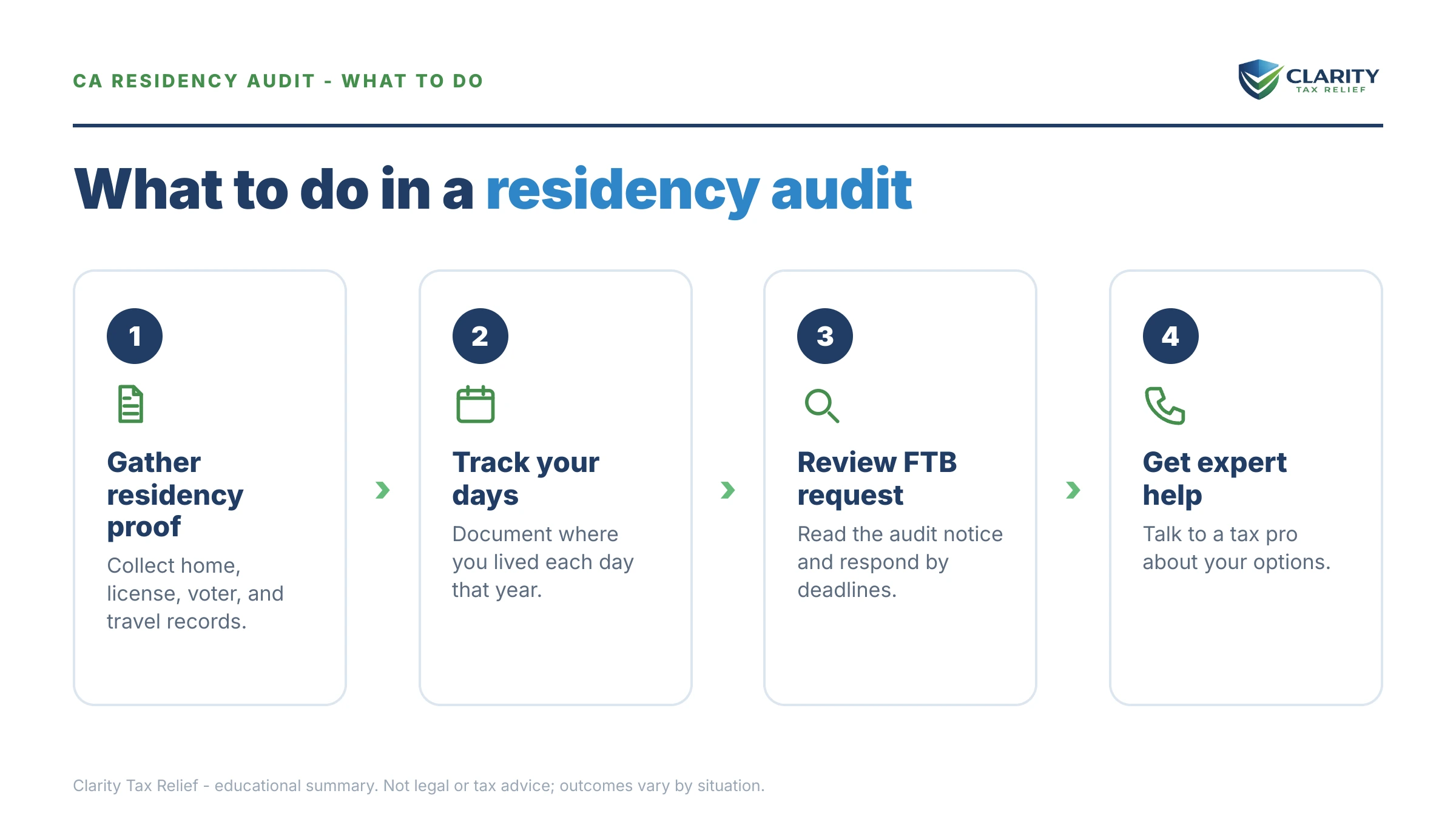

How to respond, step by step

- Read the letter and note every deadline. Calendar the response date and the protest date if an assessment follows.

- Don't volunteer extra information. Answer what's asked, accurately and completely — but don't hand over unrelated years or hand the auditor open-ended narratives.

- Build your records file using the checklist above. Organize it by factor, not by date pile.

- Request more time in writing if you need it. The FTB often grants reasonable extensions when you ask before the deadline.

- If you get a Notice of Proposed Assessment you disagree with, protest in time. You can later appeal to the California Office of Tax Appeals.

- If the audit ties to a broader move, plan the whole picture. Coordinating with the rules on handling your final California taxes after a move keeps your filings consistent.

- Get representation for high-dollar audits. When six figures are on the line, an experienced tax professional who handles FTB matters can manage the auditor and present your records the way the FTB expects.

Residency audit vs. the "exit tax" myth

People often confuse a residency audit with a so-called California exit tax. There's no toll charged simply for leaving. What's real is that California taxes the income you earned while a resident — and a residency audit is how the FTB tests when your residency actually ended. If you're worried about the cost of leaving, our guide to the California exit tax myth and the real cost of moving separates fact from headline.

And if an audit ends in a balance you can't pay, you still have options — from a payment plan to hardship status. Start with our overview of California tax debt relief for FTB and IRS debt to see what may fit.

California residency audit questions, answered

What triggers a California residency audit?

Common triggers include filing a part-year or nonresident return after years as a full-year resident, a large one-time income event like selling a business or stock, keeping a California home after a move, and a mismatch between the address on your federal return and your California filing. The FTB also cross-checks data from other states and the IRS.

How does the FTB decide if I'm still a California resident?

California uses a 'closest connections' test, not a single day count. The FTB weighs where your home, family, vehicles, doctors, bank accounts, business ties, and voter registration are. There's no magic number of days that makes you a nonresident — the question is where the center of your life actually is.

Does living outside California for 183 days make me a nonresident?

No. The 183-day rule is a myth for general residency. Spending fewer than half the year in California does not automatically make you a nonresident. The FTB looks at your overall connections to the state. There is a separate 'safe harbor' for some employees working abroad under a long-term contract, but it has strict rules.

What records do I need for a California residency audit?

Gather proof that ties your life to your new state: a new driver's license, voter registration, lease or deed, utility bills, cell phone and credit card records showing where you spent your days, moving receipts, new doctors and dentists, and updated estate documents. The more contemporaneous and consistent the records, the stronger your case.

What happens if I lose a California residency audit?

The FTB issues a Notice of Proposed Assessment for the tax it says you owe, plus penalties and interest. You can protest within the deadline on the notice, then appeal to the Office of Tax Appeals. If the assessment becomes final and unpaid, the FTB can lien, levy, and garnish — so responding on time matters.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.