California State Tax

CDTFA Sales Tax Audit: What to Expect and How to Survive It (2026)

The short answer: a CDTFA sales tax audit is a review by the California Department of Tax and Fee Administration to confirm you reported and paid the right amount of sales and use tax. The auditor compares your sales tax returns to your books and outside data. You can survive it by responding on time, organizing your records, and not guessing at answers.

Just opened a CDTFA audit letter?

Send us the notice. An experienced tax professional will explain exactly what the auditor is looking for, what records to pull, and how to keep the assessment as small as the facts allow — free, confidential, no pressure.

⏱ Your deadlines: respond to the audit engagement letter by the date it gives you — usually 30 days to schedule and gather records. If the audit ends in a Notice of Determination you disagree with, you generally have 30 days from that notice to file a petition for redetermination, or the bill becomes final.

Why you got a CDTFA sales tax audit notice

If you opened a letter from the California Department of Tax and Fee Administration scheduling a CDTFA sales tax audit, take a breath. An audit is not an accusation — it's a verification. The CDTFA wants to confirm the numbers on your sales tax returns match what actually happened in your business.

Audits get triggered for ordinary reasons. The most common is a mismatch: your reported taxable sales don't line up with your income tax returns, your bank deposits, or the 1099-K totals card processors send the state. Cash-heavy businesses, large amounts of claimed exempt or resale sales, and certain targeted industries (restaurants, bars, auto sales, convenience stores, online sellers) draw extra attention. Some audits are simply random. You can read the agency's own overview in the CDTFA's audit publication (Publication 76).

What the auditor actually does

A sales tax auditor's job is to test whether the tax you collected and the tax you reported are the same number. To do that, they reconcile your records against each other. Expect them to ask for:

- Your sales and use tax returns for the audit period

- Federal and California income tax returns

- Profit-and-loss statements and your general ledger

- Bank statements and merchant card statements

- Point-of-sale and cash register (Z-tape) records

- Purchase invoices for resale and for items used in the business

- Resale certificates and exemption certificates for non-taxed sales

If your records are incomplete, the auditor doesn't just give up — they estimate. They may use a "markup" test (comparing your purchases to your sales) or sample a few months and project the result across the whole period. Estimates rarely favor the taxpayer, which is exactly why clean records matter so much.

What happens if you ignore it

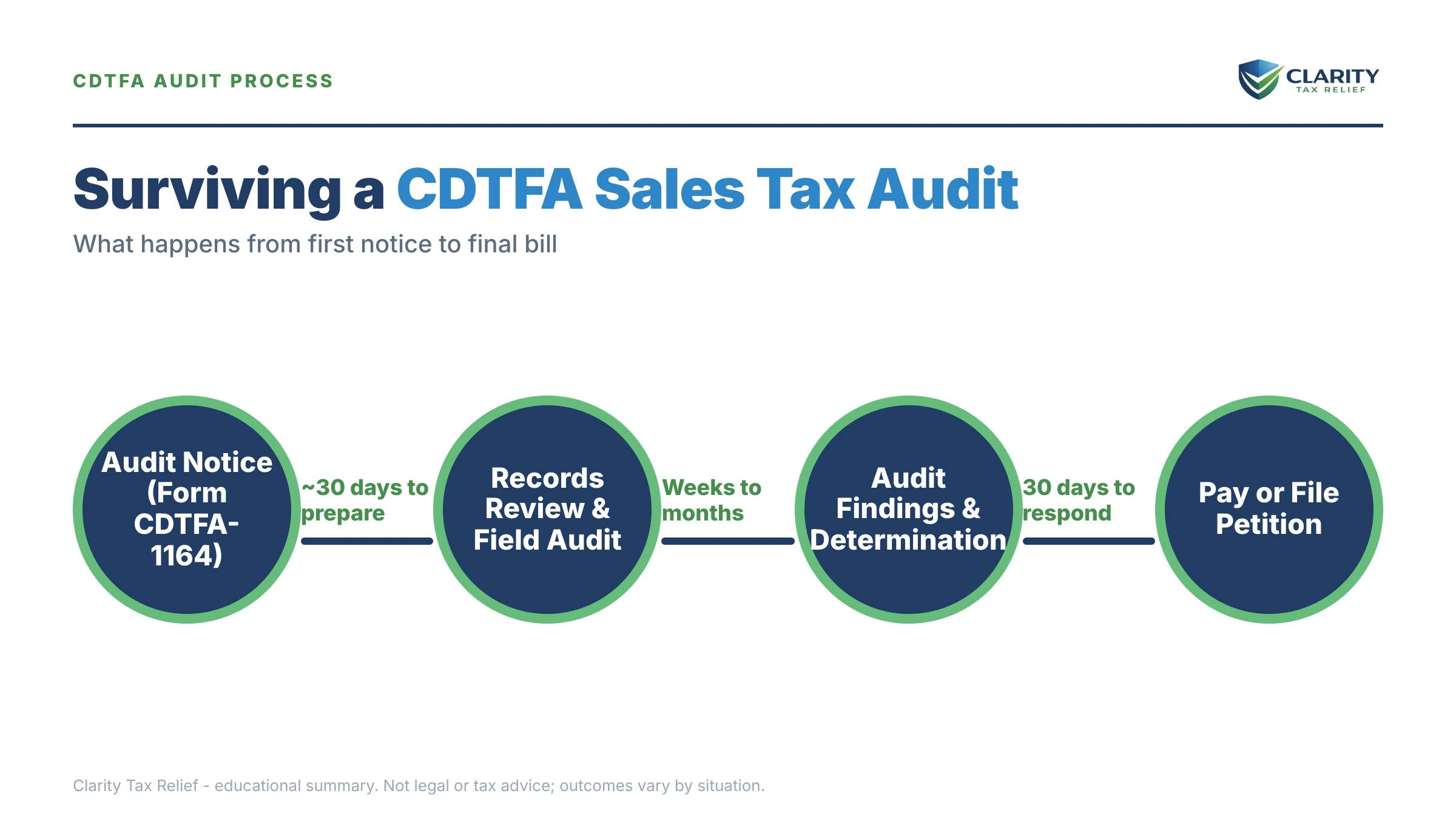

A CDTFA audit doesn't go away if you stop answering the phone. The process is structured, and missing each step makes the outcome worse:

- Engagement letter — the audit is opened and records are requested. You are here. Cooperation now keeps you in control.

- Estimated assessment — if you don't provide records, the auditor builds the bill from estimates and outside data, almost always higher than reality.

- Notice of Determination — the formal tax bill, with penalties and interest. You have 30 days to petition before it's final.

- Collections — once final and unpaid, the CDTFA can record a lien, levy bank accounts, and pursue responsible owners personally for tax that was collected in trust.

That last step is the one people underestimate. Sales tax is money you collected from customers on the state's behalf. If the business can't pay, California can hold a "responsible person" — an owner or officer who controlled the funds — personally liable. To see what the final bill looks like, read our guide to the CDTFA Notice of Determination.

A worked example: how an estimate inflates the bill

Say you ran a small café and reported $600,000 in taxable sales over a three-year period. Your register tapes are missing for several months. The auditor pulls your food and beverage purchase invoices, applies a typical industry markup, and concludes your sales "should" have been $720,000. The $120,000 gap becomes taxable. At a combined rate of roughly 9%, that's about $10,800 in additional tax — before penalties and interest.

Now flip it. If you'd produced complete register records showing the $600,000 was accurate — and documented the comps, spoilage, and employee meals that explained the lower sales — that $120,000 estimate may never appear. The difference between those two outcomes is paperwork, not luck.

How to survive a CDTFA sales tax audit, step by step

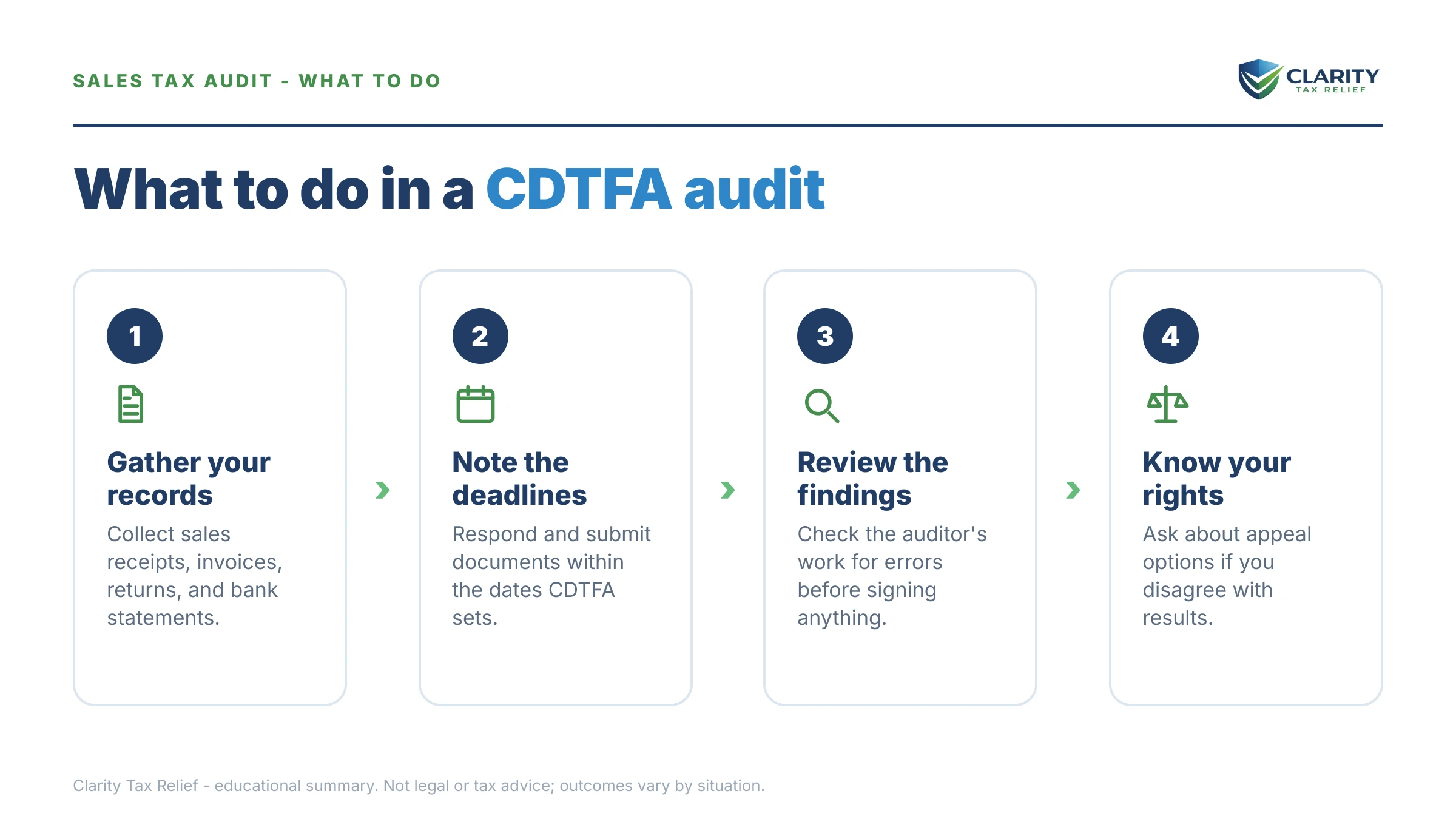

- Respond by the deadline. Acknowledge the engagement letter and schedule the audit. Asking for a reasonable extension to gather records is normal and usually granted — going silent is not.

- Gather and organize your records before the auditor arrives. Reconcile your sales tax returns to your income tax returns and bank deposits yourself first, so you find the gaps before they do.

- Fix your exemption paperwork. Every resale or exempt sale needs a valid certificate. Missing certificates are one of the biggest sources of assessments — and many can still be collected from customers.

- Answer only what's asked. Be polite and honest, but don't volunteer extra years, extra entities, or guesses. "I'll get back to you with the records" is a complete answer.

- Review the audit findings carefully. Auditors make mistakes in sampling and markup math. Discuss disagreements with the auditor, then the supervisor, before anything is finalized.

- Protect your appeal rights. If the Notice of Determination is wrong, file a petition for redetermination within 30 days. If you owe but can't pay it all at once, look into a CDTFA payment plan to keep collections off your back.

Options after the audit ends

If the audit produces a balance you genuinely owe, you still have choices. You can pay in full, set up an installment agreement, or — if paying would create real hardship — ask about hardship relief similar to the FTB financial hardship framework California's other tax agency uses. Penalties for things like late filing or negligence can sometimes be reduced for reasonable cause. And if the underlying numbers are wrong, your strongest move is the petition, not the checkbook. Our broader guide to resolving California back sales tax walks through each path.

Remember that the CDTFA is one of three tax agencies a California business deals with — alongside the Franchise Tax Board (FTB) and the Employment Development Department (EDD). If you're juggling more than one, the order you resolve them in matters; start with our overview of which back taxes to pay first.

CDTFA sales tax audit questions, answered

What triggers a CDTFA sales tax audit?

Common triggers include sales tax returns that don't match your income tax returns or 1099-K totals, large amounts of exempt or resale sales, cash-heavy businesses, an industry the CDTFA targets, a tip, or simply random selection. A mismatch between what you reported and outside data is the most frequent reason.

How far back can a CDTFA audit go?

The standard look-back period is three years from the due date of the return. If you didn't file or the CDTFA suspects fraud, that window can extend to eight years or more. The auditor will tell you the exact periods under review early in the process.

What records do I need for a CDTFA audit?

Plan to provide sales tax returns, federal and state income tax returns, profit-and-loss statements, bank statements, point-of-sale and register records, purchase invoices, and resale and exemption certificates. The auditor uses these to test whether your reported taxable sales match your actual sales.

What happens if I disagree with the CDTFA audit results?

You don't have to accept the findings. You can discuss them with the auditor and the auditor's supervisor, and if you still disagree you can file a petition for redetermination after the Notice of Determination is issued — generally within 30 days. That preserves your appeal rights before the bill becomes final.

Can a CDTFA audit make me personally liable?

Yes. Sales tax is considered money you collected in trust for the state. If a business closes or can't pay, the CDTFA can pursue responsible persons — owners, officers, or others who controlled the funds — personally for the unpaid tax. That's why a sales tax audit should never be ignored.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.