California Tax Debt

FTB vs IRS: Which Back Taxes Should You Pay First? (2026)

The short answer: when you weigh FTB vs IRS, deal first with whichever agency is closest to enforcing — sending a final notice, garnishing wages, or levying a bank account. That's often the FTB (California's Franchise Tax Board), which collects faster than the IRS. But you can usually set up plans with both at once, so don't ignore either.

Owe both the FTB and the IRS?

Send us your notices. An experienced tax professional will map out which agency to handle first and what relief you may qualify for — free, confidential, no pressure.

⏱ Why timing matters: the IRS generally has 10 years to collect a tax debt. California's FTB has 20 years. Whichever you owe, every month of delay adds penalties and interest — and the FTB can move to a wage garnishment or bank levy on a shorter timeline than the IRS.

Why you owe both the FTB and the IRS

If you live or earn money in California, you file two income tax returns: a federal one with the IRS and a state one with the Franchise Tax Board, or FTB. When you can't pay in full, you usually end up owing both at the same time. The same missed paycheck, business loss, or skipped estimated payment hits your federal and state balance together.

That's why the FTB vs IRS question comes up so often. People assume one debt is "the big one" and pour everything into it — only to get blindsided by the agency they ignored. The truth is the two agencies are completely separate. Paying one does not lower the other, and each can collect on its own.

FTB vs IRS: how the two agencies differ

Understanding who you're dealing with changes how you prioritize. Here's how California and the federal government compare on the things that matter most when you owe back taxes:

- How long they can collect. The IRS has roughly 10 years from the date a tax is assessed — the Collection Statute Expiration Date, or CSED. The FTB has 20 years from when the debt became due. California's clock runs twice as long.

- Speed of enforcement. The IRS sends a long sequence of notices before it levies. The FTB often moves faster — its demand and final notices can lead to a garnishment or bank levy on a shorter timeline.

- Extra fees. The FTB tacks on collection and cost-recovery fees that the IRS doesn't charge. You can read how those add up in our guide to FTB collection and cost-recovery fees.

- How much they can take. Both can garnish wages, but the rules differ. California uses an Earnings Withholding Order for Taxes; see our breakdown of how much the FTB can garnish from your paycheck.

- Refund intercepts. The FTB can grab your California refund and even lottery winnings to cover a balance, and federal refunds can be offset toward state debt through the Treasury Offset Program.

You can verify the federal collection timeline on the IRS page about how long the IRS can collect tax, and review California's collection authority on the FTB collections page.

What happens if you ignore one of them

Both agencies use automated collection systems. Ignore the notices and the sequence keeps escalating whether or not a human ever looks at your file. A typical path looks like this:

- Balance-due notice — the first bill from either agency. No enforcement yet, but penalties and interest start growing.

- Reminder and demand notices — the balance keeps climbing. The FTB may add a collection fee here.

- Final notice / intent to levy — the IRS issues an LT11 or Letter 1058; the FTB issues its own final demand. Appeal rights apply, but the window is short.

- Enforcement — wage garnishment, bank levy, refund intercept, and tax liens. The FTB can reach this stage faster, and a California state tax lien can damage your credit and tie up property.

The lesson isn't "pick one and forget the other." It's that the agency you ignore is the one that levies you. Your job is to stop enforcement on both.

Which back taxes should you pay first?

There's no single right answer, because it depends on your numbers and which agency is moving. Use this order of thinking:

- Stop the closest threat first. If one agency has sent a final notice or already garnished you, that's your emergency. Often that's the FTB because of its faster timeline.

- File every missing return before you pay a dime. Neither agency will set up a real resolution while returns are unfiled, and an estimated "substitute" assessment is almost always higher than your true tax.

- Compare the cost of waiting. The IRS failure-to-pay penalty runs 0.5% of the unpaid tax per month, plus interest. California adds its own penalties and collection fees. Whichever debt is growing fastest deserves attention sooner.

- Protect what can be taken. If your paycheck or bank account is exposed to one agency more than the other, prioritize stopping that levy.

For most people the smartest move isn't choosing one debt and ignoring the other — it's setting up a plan or hardship status with both so no levy ever lands. If California is your bigger worry, start with your options when you owe California state taxes and can't pay.

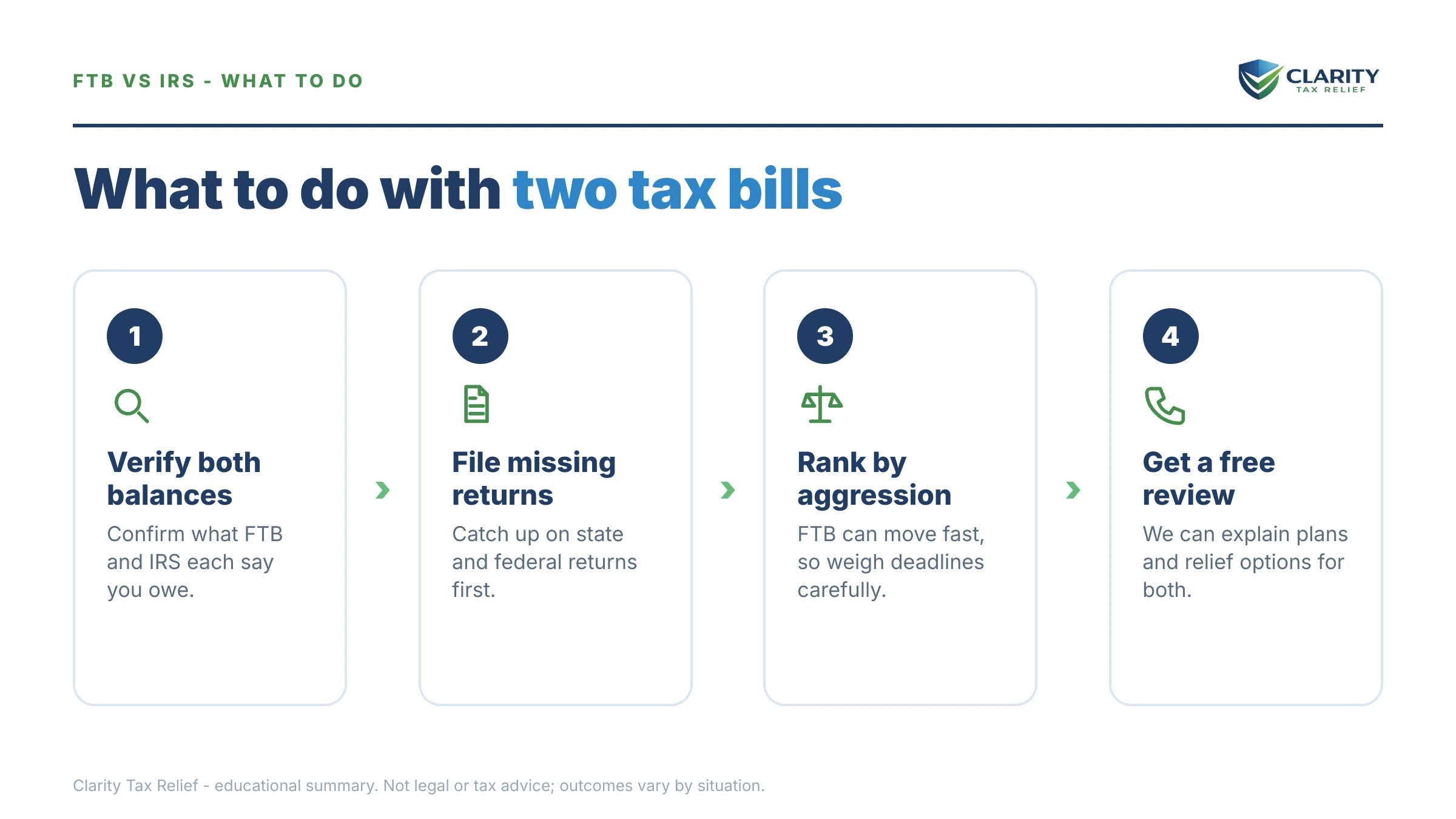

How to handle both debts, step by step

- Pull your records from both agencies. Check your IRS online account and your FTB MyFTB account so you know the real balances, tax years, and any final-notice deadlines.

- File any missing returns. Fixing an unfiled federal year often changes your California income too, so get both returns right before you negotiate.

- Identify the closest threat. Look for the agency with a final notice, garnishment, or levy in motion — that one gets handled first.

- Set up relief with each agency. You can run a payment plan, hardship status, or other resolution with the FTB and the IRS at the same time. Each only counts your allowable expenses, including the payment you owe the other agency, so tell each one about the other debt.

- Watch for penalty relief. First-time abatement may remove an IRS penalty, and California offers reasonable-cause relief. See FTB penalty abatement and reasonable cause for what California allows.

- Get a professional review if the totals are large or messy. The order you fix things in — returns, penalties, then balances — changes what you end up paying both agencies.

A quick worked example

Say you owe $18,000 to the IRS and $7,000 to the FTB, and you can afford about $400 a month total. Pouring all $400 at the IRS feels productive — until the FTB, which moves faster, garnishes your wages for the $7,000 you left untouched. A better plan: split the payment across two installment agreements so both clocks are satisfied and no levy lands. The federal debt is larger, but the state debt was the one about to hurt you. That's the FTB vs IRS trap in one picture — the urgent debt isn't always the biggest one.

FTB vs IRS: your questions, answered

Is the FTB or the IRS more aggressive about collecting back taxes?

The FTB often moves faster than the IRS. California's collection notices can lead to wage garnishments, bank levies, and refund intercepts on a shorter timeline than the federal system, and the FTB also adds collection cost-recovery fees. The IRS hits harder over time and has a 10-year collection limit, while California's clock runs 20 years.

Should I pay the FTB or the IRS first if I owe both?

There is no one-size answer. Generally, deal first with whichever agency is closest to enforcing — sending a final notice, garnishing wages, or levying a bank account. Often that is the FTB because of its faster timeline. But you can usually set up a payment plan or hardship status with both at the same time, so the goal is to stop enforcement on each, not to ignore one.

Can I set up payment plans with the FTB and the IRS at the same time?

Yes. The FTB and the IRS are separate agencies with separate programs, so you can have an installment agreement with each at once. When you build the plans, each agency only counts your real, allowable monthly expenses — including the payment you owe the other agency — so be sure both know about the other debt.

Does paying the IRS reduce what I owe the FTB?

No. They are completely separate debts. Paying one does not lower the other. However, your federal and state returns are linked — fixing an error or filing a missing federal return often changes your California income, which can raise or lower the FTB balance. Getting both returns right is the first step.

How long can the FTB and the IRS collect back taxes?

The IRS generally has 10 years from assessment to collect a tax debt — the Collection Statute Expiration Date. California's Franchise Tax Board has 20 years from the date the debt became due and payable. So even after a federal debt expires, the state balance can still be collectible, which is one reason California debt deserves close attention.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. Anyone promising to settle your debt for "pennies on the dollar" before reviewing your finances is selling you something.