California / FTB Collections

How Much Can the FTB Garnish From Your Paycheck?

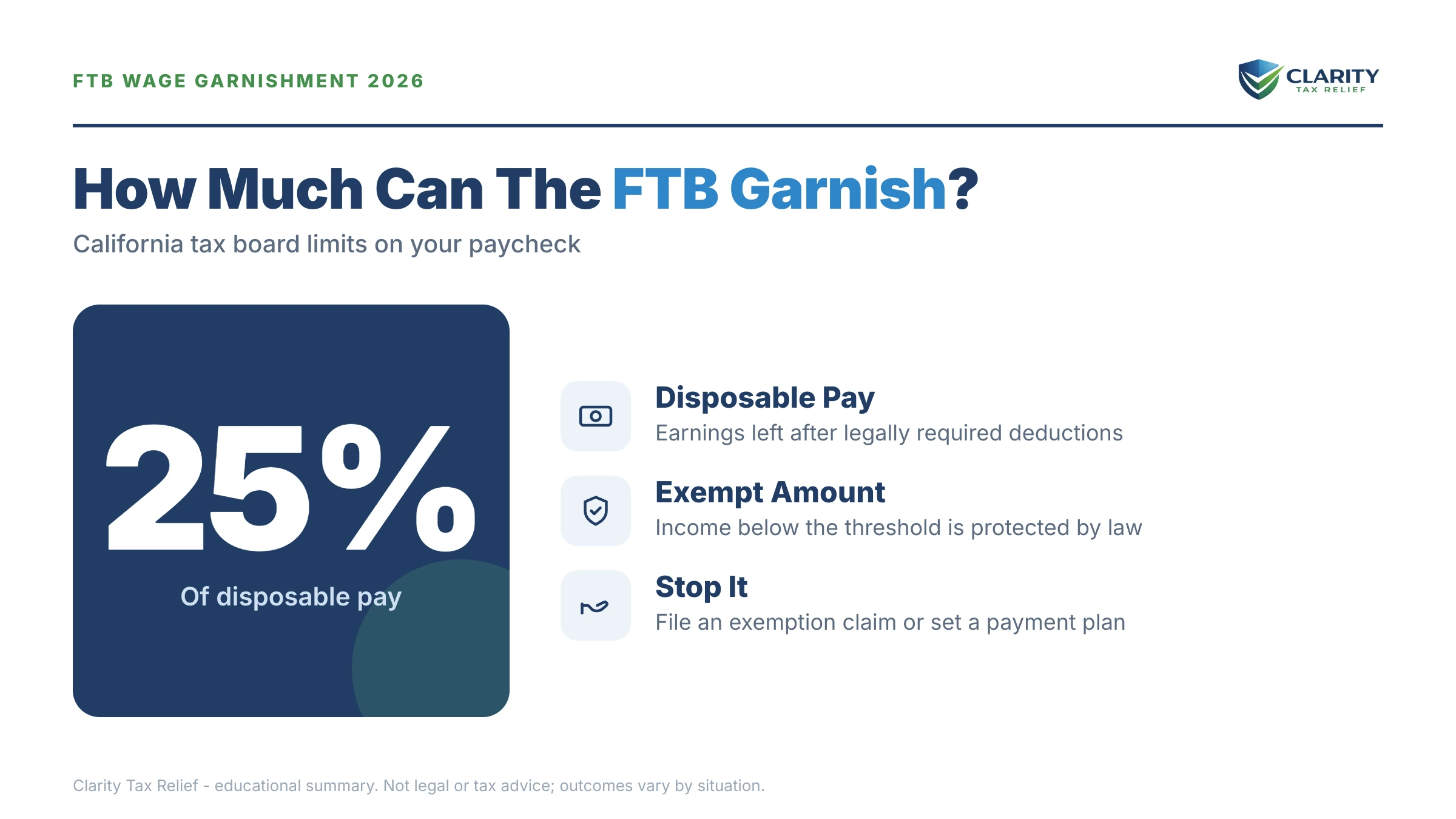

The short answer: the California Franchise Tax Board (FTB) can generally garnish up to 25% of your disposable earnings — your pay after legally required deductions. That is the legal maximum. If taking 25% would leave you unable to cover basic living expenses, you can ask the FTB to reduce it based on financial hardship.

Is the FTB taking part of your paycheck?

Send us the order or notice. An experienced tax professional will explain exactly how much the FTB can take, whether you qualify for a reduction or release, and the fastest way to protect your next check — free, confidential, no pressure.

⏱ Why timing matters: once the FTB sends an Earnings Withholding Order for Taxes (EWOT) to your employer, payroll must usually begin withholding within about 10 days — and the order keeps pulling from every paycheck until the debt is paid or the order is released. The time to act is before your next payday.

How much can the FTB garnish, exactly?

When the FTB garnishes wages, it uses a tool called an Earnings Withholding Order for Taxes (EWOT). The cap is the same one that applies to most wage garnishments in California: up to 25% of your disposable earnings.

"Disposable earnings" is not your gross paycheck. It's what's left after the deductions the law requires — federal and state income tax withholding, Social Security, Medicare, and California State Disability Insurance (SDI). Voluntary deductions like a 401(k) contribution or extra health coverage usually don't lower the number.

So the math runs in two steps: first your employer figures your disposable earnings, then it withholds up to a quarter of that amount and sends it to the FTB. California protects a floor of income tied to the minimum wage, so very low earners may have less than 25% taken — but for most working people, 25% is the figure to plan around.

A worked example

Say you're paid weekly and your gross pay is $1,200. After required deductions, your disposable earnings are $960.

- Maximum garnishment: 25% × $960 = $240 per week

- What you keep: $720 of your disposable pay

- Over a month: roughly $960 withheld — month after month, until the balance is cleared

Now remember that an FTB balance isn't just the original tax. It grows with penalties, interest, and FTB collection and cost-recovery fees. A debt you remember as $6,000 can be noticeably larger by the time a garnishment starts — which means the order runs longer than you'd expect.

How an FTB garnishment is different from a one-time levy

People often confuse a wage garnishment with a bank levy. They're not the same:

- A bank levy is a one-time grab of money sitting in your account on a specific day.

- An EWOT is continuous. It attaches to your wages and keeps withholding from every check until the full balance is paid or the order is modified or released.

That "keeps going" feature is what makes a garnishment so painful — and why ignoring it is the worst option.

What happens before the FTB garnishes — and if you ignore it

The FTB doesn't garnish out of the blue. There's a paper trail, and each step is a chance to stop the next one. If you've moved or stopped opening the mail, the first sign may be a smaller paycheck — so it pays to know the sequence:

- Tax bill / Notice of Tax Due — the FTB says you owe. Decode yours with our FTB notice decoder.

- Final demand / collection notices — penalties, interest, and fees are stacking up while collection ramps up.

- State tax lien — a recorded claim against your property and credit. See how to handle a California state tax lien.

- Earnings Withholding Order for Taxes (EWOT) — sent to your employer. Up to 25% of disposable pay is withheld until the debt is gone.

- Other enforced collection — bank levies, refund and lottery intercepts, and (for some professionals) license issues can run alongside the garnishment.

The FTB's automated collection system doesn't forget. You can read more about how California enforces these debts on the FTB collections page and the FTB's withholding orders overview.

How to stop or reduce an FTB wage garnishment

You have real options — and several can cut the 25% bite or end it entirely. Which one fits depends on your finances:

- Pay the balance in full. The order releases once the debt — including fees — is satisfied.

- Set up an installment agreement. A monthly payment plan can replace the garnishment with a more manageable amount, and the FTB will typically release the EWOT once the plan is in place.

- Prove financial hardship. If 25% leaves you unable to pay rent, food, and utilities, the FTB can lower the withholding or place you in FTB financial hardship / Currently Not Collectible status, which pauses collection. You'll usually document your budget on FTB Form 3561, the California financial statement.

- Challenge a wrong debt. If the balance is based on a return you never filed or an estimate that's too high, fixing the underlying issue can shrink or erase the garnishment.

- Get professional representation. An experienced tax professional can contact the FTB on your behalf and negotiate a release or reduction.

One honest warning: anyone promising to "settle for pennies on the dollar" or stop your garnishment overnight before reviewing your finances is selling you something. Real relief follows your actual numbers, and no outcome is guaranteed.

How to respond, step by step

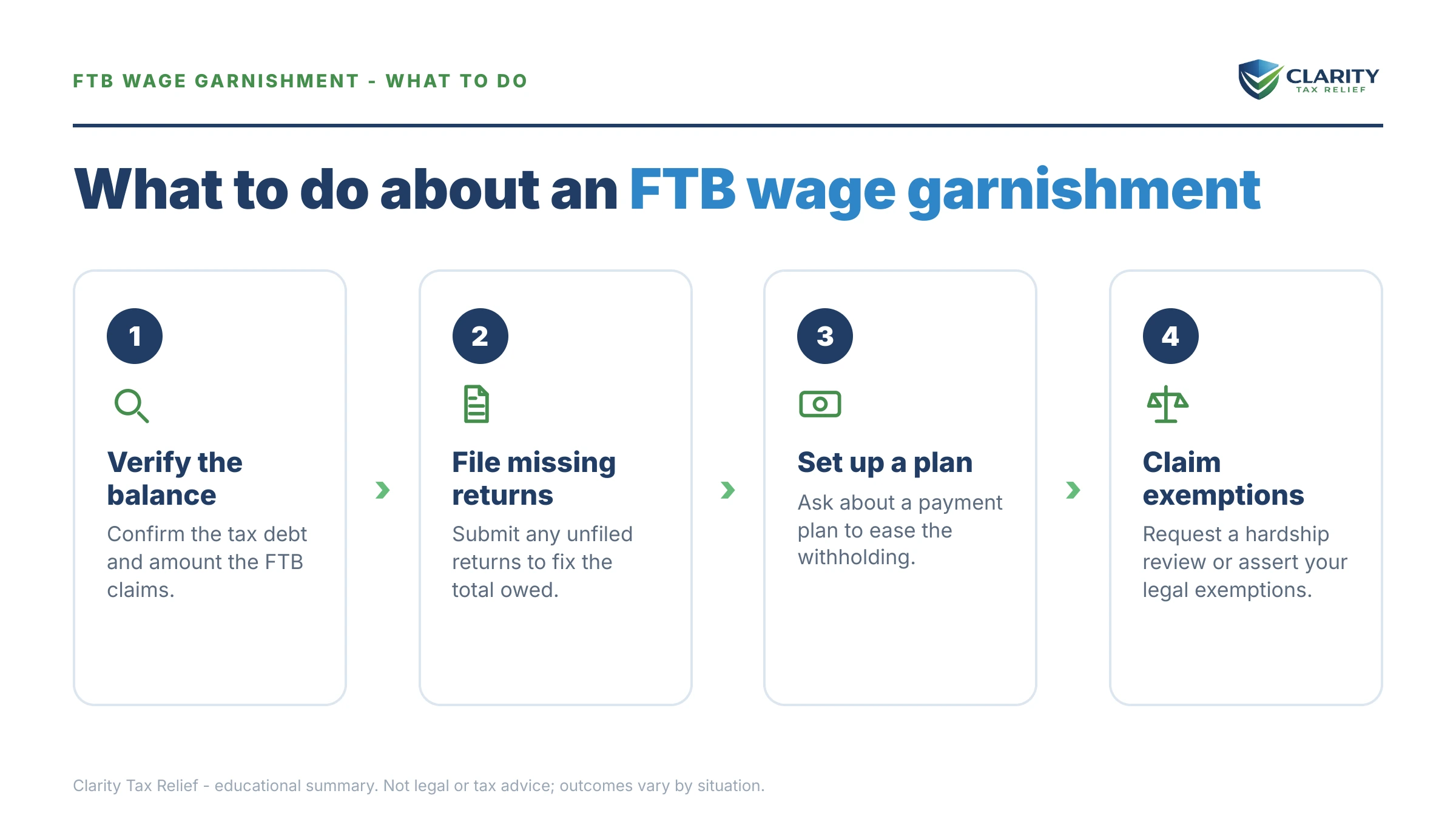

- Confirm it's really the FTB. Match the order to your tax years and balance. The FTB contacts you by mail — not by text demanding gift cards.

- Find out what you owe and why. Log into your MyFTB account or call the FTB. Verify the tax, penalties, interest, and fees.

- Pick your path. Pay in full, request an installment agreement, or gather proof of hardship — whichever your budget supports.

- Contact the FTB before your next payday. The order keeps withholding until it's released, so speed protects your paycheck.

- If you owe the IRS too, decide the order of attack. See FTB vs. IRS: which back taxes to pay first — both can garnish at once, and sequence matters.

- Get help if it's complex. Multiple years, a lien, or both agencies involved? A professional review can save you money and stress.

FTB garnishment questions, answered

How much can the FTB take from my paycheck?

The California Franchise Tax Board can generally garnish up to 25% of your disposable earnings — what's left after legally required deductions like taxes. That is the maximum the law allows. If 25% would leave you unable to cover basic living costs, you can request a reduced amount based on financial hardship.

How long does an FTB wage garnishment last?

An FTB Earnings Withholding Order for Taxes stays in effect until the full balance — tax, penalties, interest, and collection fees — is paid, or until you set up an approved arrangement that replaces it. Unlike a one-time bank levy, the order keeps pulling from every paycheck until you resolve the debt or get the order modified or released.

Can I stop an FTB garnishment once it starts?

Yes. You can pay the balance in full, set up an FTB installment agreement, prove financial hardship to qualify for a reduced amount or Currently Not Collectible status, or show the debt is wrong. The fastest path is contacting the FTB before your next payday, because the order keeps withholding until it's released.

Does the FTB have to warn me before garnishing my wages?

Yes. The FTB sends notices and a final demand before issuing an Earnings Withholding Order for Taxes. If you've moved or ignored the mail, the first you may hear of it is a smaller paycheck. The notices give you a window to set up an arrangement before the garnishment ever reaches your employer.

Can the FTB and the IRS both garnish my wages at the same time?

Yes, both can issue separate wage garnishments. Federal and state limits interact, so your total take-home can drop sharply if both hit at once. If you owe both agencies, the order you address them in matters — an experienced tax professional can help you decide which to resolve first.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS and FTB programs depends on individual facts and circumstances; no outcome is guaranteed.