California / FTB

FTB Collection & Cost-Recovery Fees Explained (2026)

The short answer: an FTB collection fee is a cost-recovery charge the California Franchise Tax Board adds when it has to take action to collect an unpaid balance. The main ones are the Collection Cost Recovery Fee and the Filing Enforcement Cost Recovery Fee. They're flat, one-time charges set by law — and acting early usually keeps them from attaching at all.

Staring at a fee you don't understand?

Send us a photo of your FTB notice. An experienced tax professional will explain exactly which fees were added, whether any can be challenged, and what your options are — free, confidential, no pressure.

⏱ Why timing matters: the Collection Cost Recovery Fee attaches the moment your account moves into active collections — not the day your tax was due. If you pay or set up an arrangement after the FTB's billing notice but before it starts collecting, you can avoid the fee entirely. Respond to any FTB notice within the timeframe it gives you (usually 30 days).

What the FTB collection fee actually is

When you owe the California Franchise Tax Board (FTB) and don't pay, the state doesn't just charge interest and penalties. It also charges you for the cost of chasing the money. That's the "cost-recovery" fee — and the one most people search for as the FTB collection fee shows up as a separate line item on your balance.

There are a few different cost-recovery fees, and they're charged for different reasons:

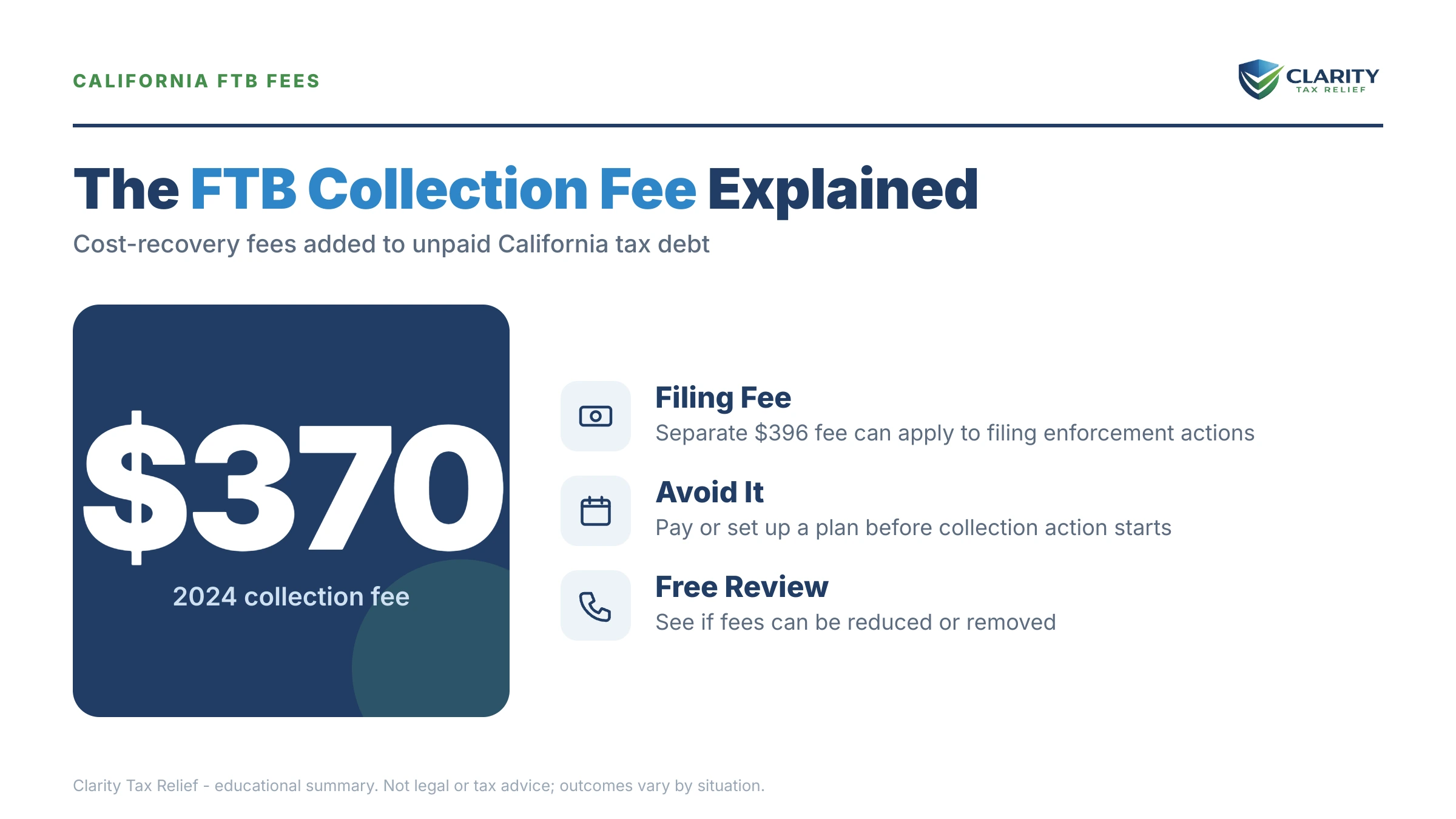

- Collection Cost Recovery Fee (CRF) — added when your account moves into active collections after you failed to pay a final bill. This is the big one most people are asking about.

- Filing Enforcement Cost Recovery Fee — added when the FTB has to force you to file a missing return, usually after a Demand to File goes unanswered.

- Lien and other recording fees — added when the FTB records a state tax lien or takes a similar enforcement step.

The exact dollar amounts are set by statute and updated each year. You can see the current figures on the FTB's own cost-recovery fees page. The key point: these are flat charges, not a percentage of what you owe, and they don't compound the way interest does.

Why you got charged a cost-recovery fee

A cost-recovery fee means the FTB had to do something to collect from you — not just send a routine bill. That usually traces back to one of these:

- You received an earlier FTB bill and didn't pay it or respond.

- The FTB sent a FTB Demand to File notice for a missing return and you didn't file, so it built a return for you and added the filing enforcement fee.

- The account aged past the billing stage and got handed to collections, which triggers the Collection Cost Recovery Fee.

- The FTB recorded a lien to protect the debt, adding a recording fee.

If a notice arrived but you're not sure which stage you're at, our FTB Notice Decoder walks through what each California Franchise Tax Board notice means and how urgent it is.

What happens if you ignore the balance

FTB collection runs on an automated schedule. Each step you skip adds cost and removes options. A typical escalation looks like this:

- Billing notice — your first bill for the unpaid tax, plus penalties and interest. No collection fee yet.

- Final notice / move to collections — the account goes active and the Collection Cost Recovery Fee attaches.

- State tax lien — the FTB can record a lien against your property, adding a recording fee. See how to release or withdraw an FTB tax lien.

- Levy or garnishment — the FTB can take money from your bank account or your paycheck. (Wondering how much? See how much the FTB can garnish from your paycheck.)

Interest on the underlying tax keeps running the whole time. The cost-recovery fees are one-time hits, but they pile on top of a balance that's already growing — so the longer you wait, the bigger the gap between what you owed and what you'll actually pay.

A quick worked example

Say you filed a California return showing $4,000 in tax due and couldn't pay. Here's roughly how the costs stack up if you let it slide:

- Original tax: $4,000

- Late-payment penalty + interest: grows month after month until paid

- Collection Cost Recovery Fee: a flat fee added when the account hits collections

- Lien recording fee: added if the FTB records a lien

None of the fees are huge on their own. But stacked on penalties and accruing interest, they can turn a $4,000 problem into a noticeably larger one — and a lien can follow you onto your credit and into any home sale or refinance. The cheapest version of this debt is always the one you handle before the fees attach.

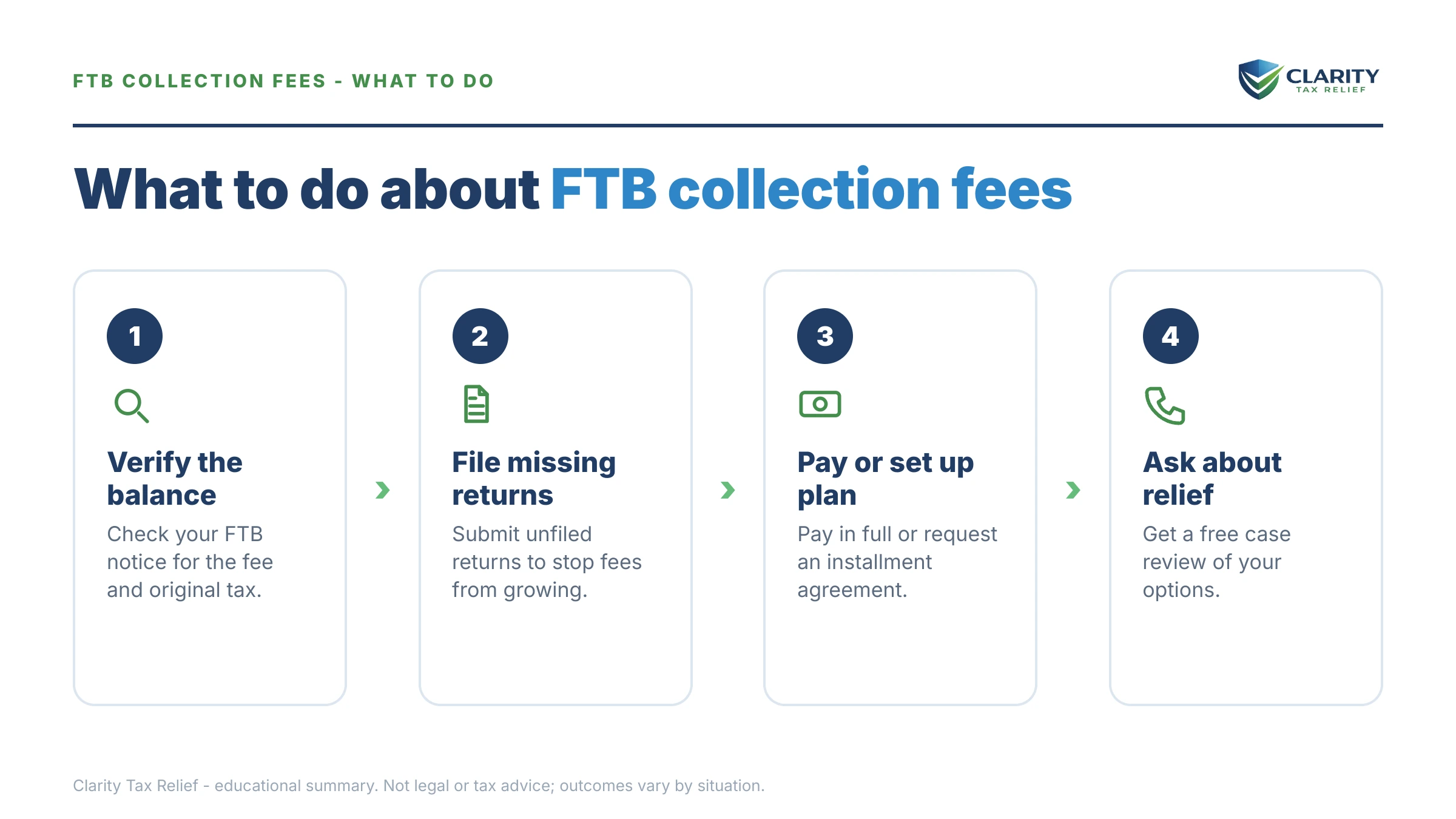

How to avoid or reduce FTB collection fees, step by step

- Confirm the balance. Log into FTB MyAccount and check exactly what you owe and which fees were added. Compare it to your records — fees added in error can be disputed.

- Pay before collections, if you can. Paying the balance at ftb.ca.gov/pay before the account goes active usually keeps the Collection Cost Recovery Fee from attaching.

- Set up a payment plan. If you can't pay in full, an FTB installment agreement stops the escalation. Starting one early can prevent later fees and a lien.

- File any missing returns. If a Demand to File triggered a filing enforcement fee, getting the actual return filed can correct an inflated estimated assessment.

- Dispute fees added in error. If the tax was already paid, or you never received the notice that triggered the fee, respond in writing with documentation. Keep copies of everything.

- Ask about penalty relief. Cost-recovery fees aren't waived for hardship, but the related penalties sometimes can be. See FTB penalty abatement and reasonable cause for what qualifies.

If you can't pay the underlying tax

Fees are only part of the picture — the real issue is the balance behind them. If money is tight, California has options beyond "pay in full":

- Installment agreement — a monthly payment plan that stops new collection actions.

- Currently Not Collectible / hardship status — if paying anything would create genuine hardship, the FTB can pause active collection. Learn more about FTB financial hardship and Currently Not Collectible status.

- Reviewing IRS and FTB together — if you owe both, the order you resolve them in matters. Our guide on California tax debt relief covers every option for FTB and IRS debt.

If your situation is complicated — multiple years, a lien, or money owed to both the FTB and the IRS — a professional review first can save you from fixing things in the wrong order. Be wary of anyone promising to make your fees or balance vanish before they've seen your finances; that's a sales pitch, not a plan.

FTB collection fee questions, answered

What is an FTB collection fee?

It's a cost-recovery fee the California Franchise Tax Board adds when it has to take action to collect an unpaid balance. The most common ones are the Collection Cost Recovery Fee, added when your account moves into active collections, and the Filing Enforcement Cost Recovery Fee, added when the FTB has to force you to file. The amounts are set by law and updated each year.

Can FTB collection fees be removed or waived?

Sometimes. If a fee was added in error — for example, the underlying tax was already paid or the notice never reached you — you can dispute it with documentation. Cost-recovery fees themselves are not automatically waived for hardship, but resolving the underlying debt and showing reasonable cause can support a request to abate related penalties. An experienced tax professional can review whether your fee is reviewable.

How do I avoid the FTB Collection Cost Recovery Fee?

Pay the balance or set up an arrangement before your account moves into active collections. The fee is triggered when the FTB has to start collecting — not the day your tax is due. Responding to the first billing notice, paying in full, or starting a payment plan early usually keeps the collection fee from attaching at all.

Do FTB cost-recovery fees keep growing like interest?

No. Cost-recovery fees are flat, one-time charges added when the FTB takes a specific action, such as opening a collection case or filing a lien. They don't compound. Interest and the underlying penalties do keep accruing on the unpaid tax, which is why the total still grows the longer a balance sits unresolved.

Will paying the tax remove the FTB collection fee?

Paying the tax stops new fees and interest, but a collection fee that already attached generally stays on the account unless it was charged in error. Check your balance on FTB MyAccount to see exactly what remains after your payment posts, and dispute any fee you believe was added incorrectly.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.