California State Taxes

California Tax Debt Relief: Every Option for FTB & IRS Debt (2026)

The short answer: California tax debt relief means using a real program — a payment plan, hardship status, a settlement, or penalty removal — to handle back taxes you owe the Franchise Tax Board (FTB), the IRS, or both. Each agency has its own options, and the right one depends entirely on your income, assets, and how close collection has gotten.

Not sure which option fits your situation?

Send us a photo of your FTB or IRS notice. An experienced tax professional will tell you exactly where you stand with each agency and which relief options you actually qualify for — free, confidential, and no pressure.

⏱ Why timing matters: the IRS generally has 10 years to collect a debt; the FTB has up to 20 years on California income tax. Both agencies add interest and penalties every month, and the FTB can move on a bank levy in as little as 10 days after a final demand. Acting now is almost always cheaper than waiting.

Why you're dealing with two tax agencies at once

If you live or earn money in California and you owe back taxes, you may be facing two separate collectors. The IRS handles your federal income tax. The California Franchise Tax Board (FTB) handles your state income tax. They are completely different agencies with different rules, different deadlines, and different powers — and they do not coordinate with each other.

That's why "California tax debt relief" isn't one button you press. It's a set of choices on the federal side and a separate set on the state side. The good news: every one of these debts has a real, legal path forward. The bad news: the systems that collect them are automated and don't slow down on their own.

Two other state agencies show up for business owners. The California Department of Tax and Fee Administration (CDTFA) collects sales tax, and the Employment Development Department (EDD) collects payroll tax. If your debt involves those, the resolution paths look similar but the forms differ — start with the agency that sent your most recent notice.

What happens if you ignore California tax debt

Both the IRS and the FTB run automated collection sequences. Each ignored notice triggers the next, with more interest and more enforcement power behind it. Here's the FTB side, which often moves faster than people expect:

- Tax due notice — the first bill. The balance is growing monthly, but no enforcement yet.

- Demand / final notice — your last warning before the FTB can act. Decoding your FTB notice tells you exactly which stage you're at.

- Refund and lottery intercept — the FTB grabs your state refund and any lottery winnings to apply against the debt.

- Bank levy and wage garnishment — the FTB can take money straight from your account and order your employer to withhold part of your paycheck.

- State tax lien — a public claim against your property that damages credit and blocks home sales.

- License suspension and the Top 500 list — California can suspend professional and driver's licenses for large debts and publish the biggest delinquents by name.

The IRS sequence ends in a Final Notice of Intent to Levy (Letter LT11 or Letter 1058), after which it can garnish wages and seize bank funds. The lesson is the same on both sides: the longer you wait, the fewer good options you keep.

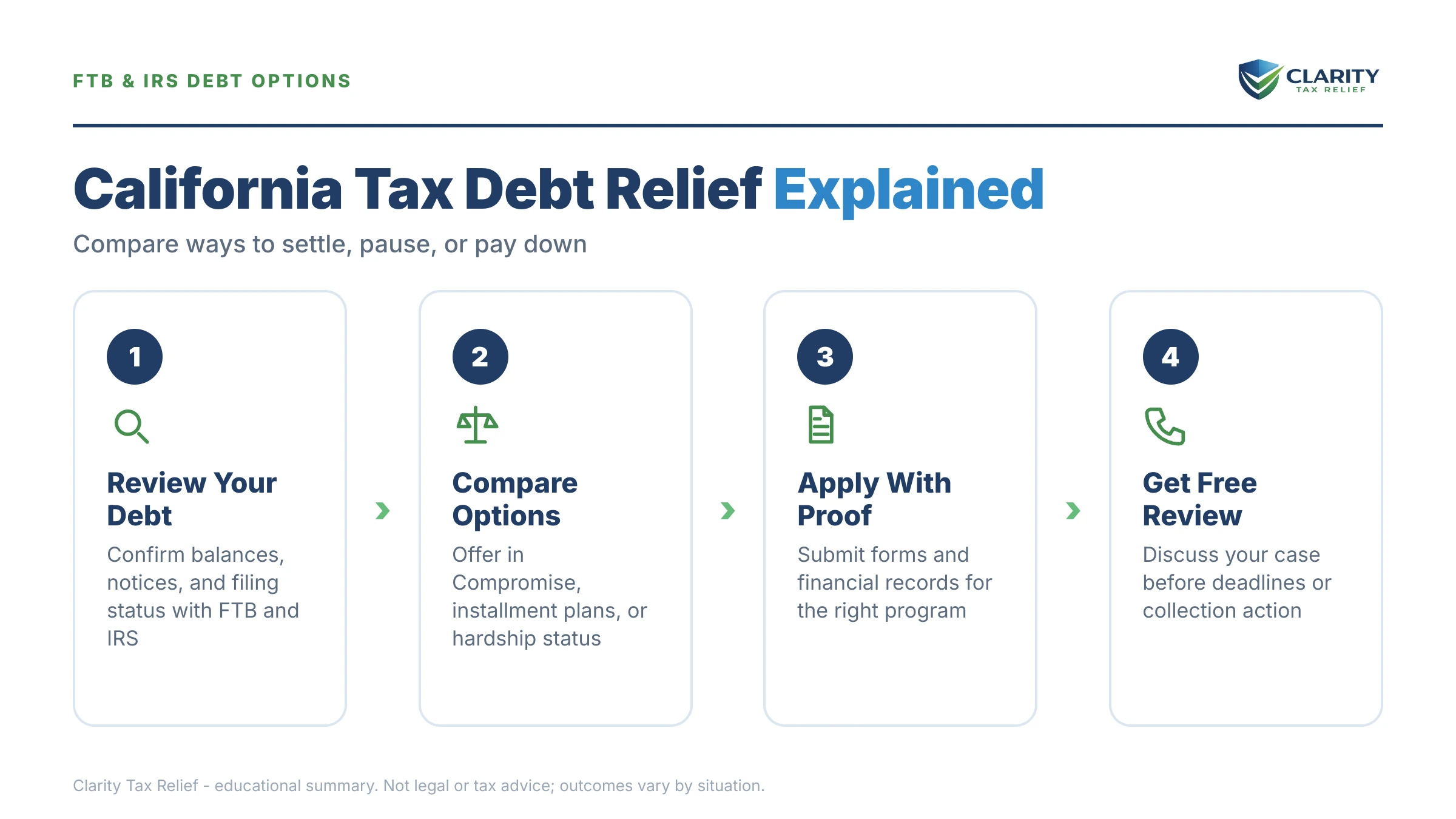

Your California tax debt relief options, agency by agency

Here is every legitimate program, grouped by who you owe. Most people qualify for at least one — often more than one.

If you owe the IRS

- Short-term payment plan — up to 180 extra days to pay in full, with no setup fee.

- Installment agreement — a monthly plan. For balances under about $50,000, "streamlined" agreements can usually be set up over up to 72 months without detailed financial disclosure. See the IRS payment plans page.

- Currently Not Collectible (CNC) status — if paying anything would create genuine hardship, the IRS pauses collection. The debt stays and interest accrues, but levies and garnishments stop.

- Offer in Compromise — settling for less than the full balance, but only when your income and assets genuinely can't cover the debt. The IRS runs the math; the marketing doesn't.

- Penalty relief — first-time abatement can erase the failure-to-pay penalty if you have a clean recent history, and reasonable-cause relief may apply for illness or disaster.

If you owe the FTB

- FTB installment agreement — a monthly payment plan for qualifying California taxpayers. If you owe California state taxes and can't pay, this is usually the first stop.

- FTB financial hardship — the state's version of Currently Not Collectible. The FTB reviews your Form 3561 financial statement and can place your account in FTB hardship status, pausing collection.

- FTB Offer in Compromise — California's own settlement program for less than the full balance, again only when your finances genuinely qualify.

- FTB penalty abatement — reasonable-cause relief may remove penalties tied to circumstances beyond your control.

- Lien release or withdrawal — once the debt is resolved or a plan is in place, you can ask the FTB to release the lien.

You can review the FTB's own collection and payment-plan information at FTB.ca.gov, and the federal versions at IRS.gov/payments. If an agency's collection is creating real hardship, the independent Taxpayer Advocate Service can sometimes step in on the federal side.

If you owe both: which one do you handle first?

When you owe the FTB and the IRS at the same time, the order matters. The FTB often moves faster on levies and garnishments and has that 20-year collection window. The IRS debt is larger for most people but expires after 10 years. The right move depends on which collector is closest to enforcement and which balance is growing fastest. Our deeper guide on FTB vs. IRS and which back taxes to pay first walks through the trade-offs.

How to get California tax debt relief, step by step

- Find out what you actually owe. Pull your IRS account transcript at IRS.gov and your FTB balance at FTB.ca.gov. Separate the two debts and note the tax years.

- File any missing returns first. Neither agency will approve a payment plan or settlement while returns are unfiled. An FTB Demand to File notice is a sign this step is overdue.

- Stop the bleeding. If a levy or garnishment is imminent, contact the agency or get representation immediately — a plan in progress can pause enforcement.

- Match each debt to the right program. Use the lists above. If you can pay over time, request an installment agreement. If you can't pay anything, ask about hardship or CNC status.

- Ask about penalty relief. Penalties often make up a big slice of the balance. First-time and reasonable-cause abatement can shrink what you owe before you settle anything.

- Get a professional review if the numbers are large. If you owe more than $10,000, have multiple years, or face both agencies, the order you fix things in changes the final cost. An experienced tax professional can build the plan before you spend money chasing the wrong option.

One warning about "settle for pennies" promises

You'll see ads promising to wipe out your California tax debt for pennies on the dollar. Settlement programs are real — both the IRS and the FTB have them — but no honest professional can promise a specific result before reviewing your full financial picture. Anyone guaranteeing a settlement amount over the phone, before they've seen your income and assets, is selling you something. The math the agencies use is based on your actual ability to pay, not a sales pitch.

California tax debt questions, answered

Can California tax debt be forgiven or settled?

Both the FTB and the IRS have settlement programs, but neither hands them out freely. The FTB Offer in Compromise and the IRS Offer in Compromise let you pay less than the full balance only when your income and assets genuinely can't cover the debt. Anyone promising to settle for pennies on the dollar before reviewing your finances is selling you something.

Should I pay the FTB or the IRS first if I owe both?

It depends on which agency is closer to enforcement and which debt is growing faster. The FTB often moves faster on bank levies and wage garnishments than the IRS, and it can intercept your state refund and suspend professional licenses. The IRS has a 10-year collection limit the FTB does not. An experienced tax professional can map both timelines before you commit a dollar.

How long can California collect a tax debt?

The IRS generally has 10 years from assessment to collect, after which the debt expires. California's FTB has a 20-year collection statute on most income tax debts — twice as long. That longer window is one reason California tax debt should not be left to sit and grow.

What if I can't pay my California state taxes at all?

If paying anything would leave you unable to cover basic living costs, the FTB can place your account in financial hardship status, which pauses collection. The IRS calls the same thing Currently Not Collectible status. The debt remains and interest keeps adding, but garnishments and levies stop while you qualify.

Will a payment plan stop FTB and IRS collection?

Yes. Once an installment agreement is in place and you keep up the payments, both agencies stop active enforcement such as new levies and garnishments. The IRS offers streamlined plans up to 72 months for balances under about $50,000, and the FTB offers monthly plans for qualifying California taxpayers.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.