California State Tax

CDTFA Payment Plan: California Sales Tax Installment Agreements (2026)

The short answer: a CDTFA payment plan lets you pay California sales and use tax debt to the California Department of Tax and Fee Administration (CDTFA) in monthly installments instead of all at once. Most plans run up to 12 months. You can request one online, and setting it up stops most collection action like bank levies and wage garnishment.

Owe the CDTFA and not sure where to start?

Send us your notice. An experienced tax professional will review where you stand, whether the bill is even correct, and which option fits your situation — free, confidential, no pressure.

⏱ Time matters: if you received a CDTFA Notice of Determination, you have 30 days to file a petition for redetermination before the bill becomes final. Once a balance is final and past due, the CDTFA can record a lien and levy your accounts. Request a payment plan before enforcement begins, not after.

What a CDTFA payment plan is

The CDTFA collects California sales tax, use tax, and many special excise taxes and fees. When you owe back sales tax and can't pay the full amount, a CDTFA payment plan — also called an installment agreement — breaks the balance into monthly payments you can actually manage.

It works a lot like an IRS or Franchise Tax Board (FTB) plan, but with shorter terms. The CDTFA generally wants the debt cleared quickly, so most plans last 12 months or less. You agree to a fixed monthly amount, you keep current on all new returns and payments, and in exchange the CDTFA holds off on aggressive collection while you pay it down.

You can set most plans up through the CDTFA online services portal or by calling the agency. The official program details live on the CDTFA payment plan page.

Who qualifies for a CDTFA payment plan

The CDTFA looks at three basic things:

- You owe a final, billed balance. If you're still disputing a Notice of Determination, sort that out first — a payment plan isn't the place to argue you don't owe the money.

- You're filing current returns. The CDTFA won't approve a plan for old debt while you keep racking up new unpaid sales tax. Get caught up on filings first.

- You can make a realistic monthly payment. For smaller balances over a short term, approval is often quick with little paperwork. For larger balances or longer terms, expect to provide financial information and possibly a down payment.

Business owners take note: the CDTFA can pursue owners, officers, and other "responsible persons" personally for a corporation's or LLC's unpaid sales tax. That means a payment plan may be set up in your personal name even after the business closes — which is why getting the assessment reviewed first matters.

What happens if you ignore the debt

CDTFA collection is methodical, and the longer you wait, the fewer good options you have. A typical escalation looks like this:

- Notice of Determination or billing notice — the CDTFA states what you owe. You have 30 days to petition if you disagree.

- Demand for payment — reminders that the balance is final and past due, with interest growing each month.

- State Tax Lien — recorded against you or your business, damaging credit and clouding any property you own.

- Bank levy — the CDTFA can seize funds directly from your business or personal accounts.

- Earnings withholding order — wage garnishment, plus seizure of accounts receivable and even your seller's permit in serious cases.

None of this is personal — it's an automated, deadline-driven system. The fix is the same at every stage: get into a plan before the next step triggers.

How much will the monthly payment be?

For short, smaller plans the CDTFA may simply divide the balance over the number of months you request. For larger balances, the monthly amount is based on what your finances show you can pay after reasonable living and business expenses.

Here's a simple worked example. Say you owe $18,000 in back sales tax and the CDTFA approves a 12-month plan. Your base payment is roughly $1,500 a month — plus interest, which keeps accruing on the unpaid balance until it's gone. A payment plan stops most enforcement, but it does not freeze interest, so paying faster always costs less in the end.

If $1,500 a month isn't realistic, that's a signal to look at other options below — not to skip payments once a plan is in place. A missed payment can default the whole agreement.

Your options if a payment plan isn't enough

A monthly plan is the most common fix, but it isn't the only one. Depending on your finances, you may have other paths:

- Offer in Compromise (OIC). The CDTFA has its own settlement program for taxpayers who can't realistically pay the full balance. It's real, but it's based on a hard look at your assets and income — anyone promising to settle your debt for "pennies on the dollar" before reviewing your finances is selling you something, not telling you the truth.

- Hardship / collection hold. If paying anything would leave you unable to cover basic living expenses, collection can sometimes be paused. This mirrors how FTB financial hardship status works on the state income tax side.

- Penalty relief. If you have reasonable cause — illness, disaster, or circumstances beyond your control — the CDTFA may waive certain penalties, lowering the balance.

- Disputing the assessment. If the underlying bill is wrong, the smartest move may be to challenge it rather than pay it. See our guide to resolving CDTFA back sales tax for how that fits together.

If you also owe the IRS or the FTB, the order you tackle each one matters — read your options when you owe California taxes and can't pay before committing your cash to one agency.

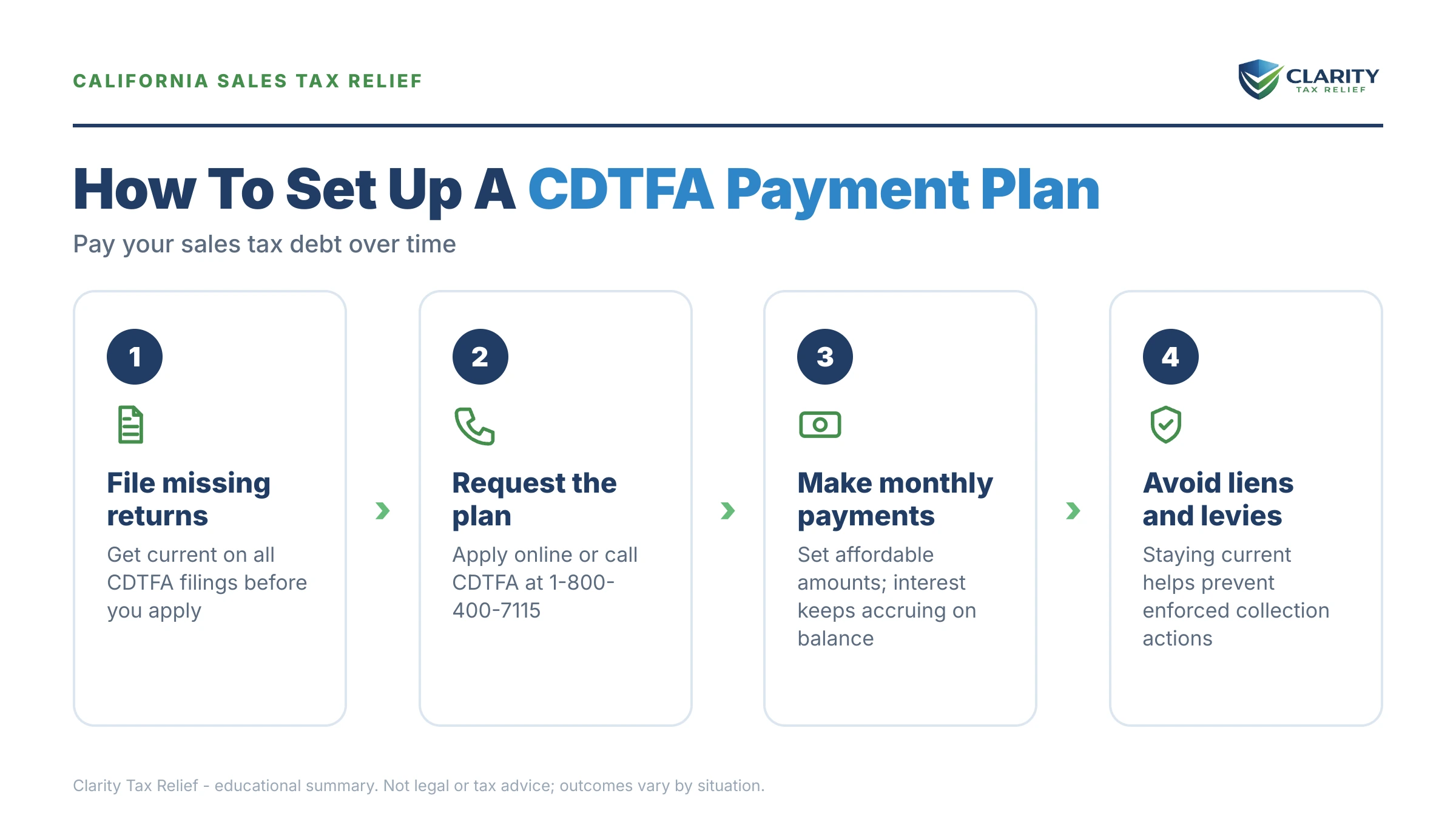

How to set up a CDTFA payment plan, step by step

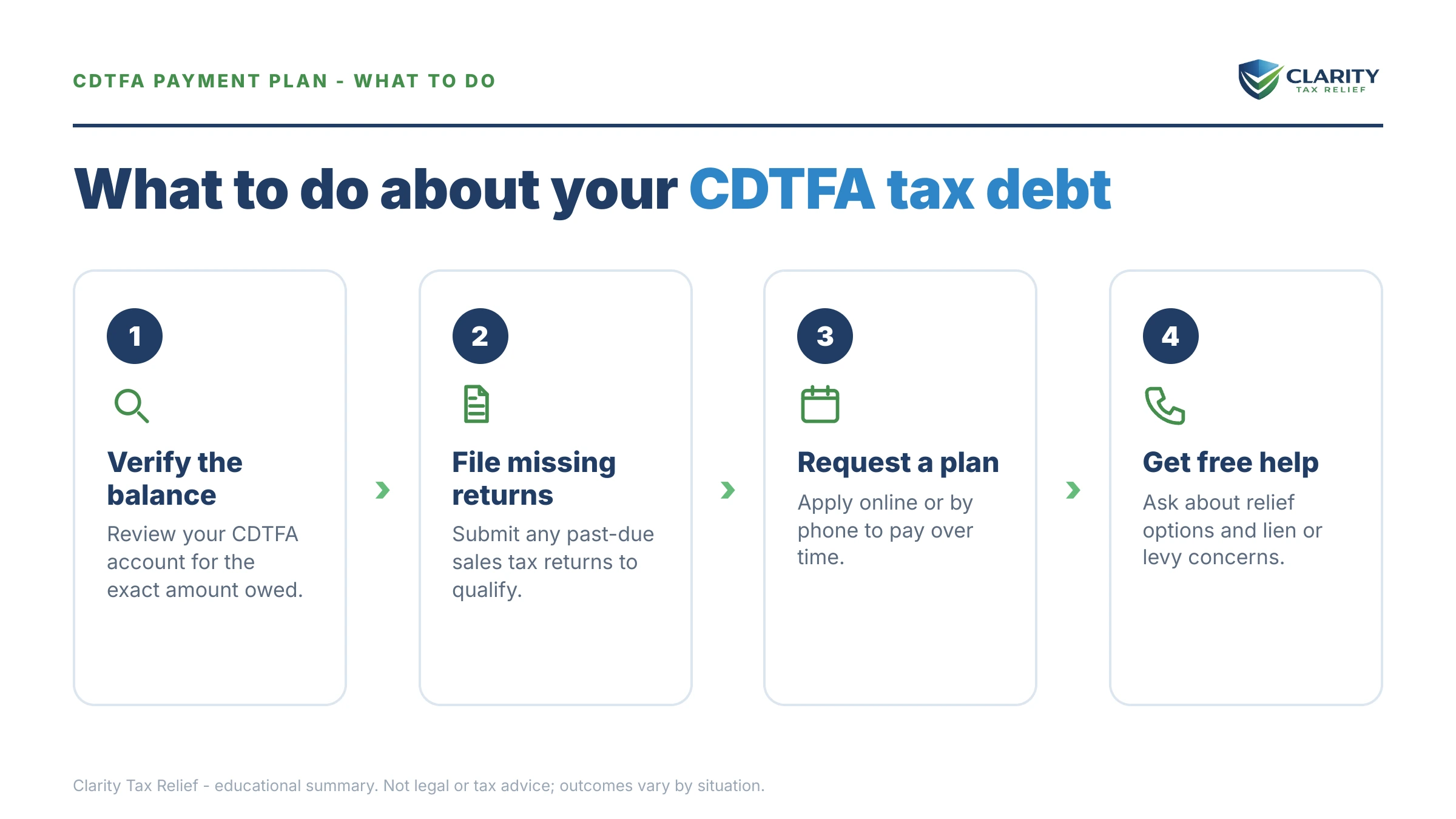

- Confirm the balance is correct. Compare the notice against your returns and records. If a sales tax audit produced the bill, make sure the numbers hold up.

- File any missing returns. The CDTFA won't approve a plan while returns are outstanding, so get current first.

- Gather your numbers. Know your monthly income, expenses, and what you can realistically pay. Larger balances require financial documentation.

- Request the plan. Apply through the CDTFA online services portal or call the agency. Propose a monthly amount you can sustain.

- Get the terms in writing and pay on time. Set up automatic payments if you can. One missed payment can default the agreement and restart collection.

- Stay current going forward. Keep filing and paying new sales tax on time — a new delinquency can void your plan.

If you're unsure whether the bill is right, whether you're personally liable, or which option saves you the most, the California CDTFA Taxpayers' Rights Advocate can help, and an experienced tax professional can review the whole picture before you commit.

CDTFA payment plan questions, answered

How long can a CDTFA payment plan last?

Most CDTFA payment plans run up to 12 months, and shorter is easier to get approved. Larger balances or hardship situations can sometimes be stretched longer, but the CDTFA generally wants the debt paid quickly. The longer the term, the more likely they'll ask for financial documents and a down payment.

Will a CDTFA payment plan stop a lien or levy?

Setting up and keeping an approved payment plan generally stops new levies and bank account seizures. A state tax lien may still be recorded to protect the state's interest, especially on larger balances. The key is to arrange the plan before enforcement starts and to never miss a payment.

Can I get a CDTFA payment plan if my sales tax debt is from a closed business?

Yes. The CDTFA can hold owners, officers, and other responsible persons personally liable for unpaid sales tax even after a business closes. A payment plan is often available on that personal liability. Get the assessment reviewed first, because personal liability is sometimes assessed incorrectly.

Does interest keep adding up on a CDTFA payment plan?

Yes. Interest continues to accrue on the unpaid sales and use tax balance until it is paid in full, even while you make monthly payments. A payment plan stops most enforcement, but it doesn't freeze interest. Paying faster or as a lump sum costs less overall.

What happens if I miss a CDTFA payment plan payment?

Missing a payment can default the agreement. Once defaulted, the CDTFA can resume collection — bank levies, wage garnishment, and liens — without setting up a new plan first. If you can't make a payment, contact the CDTFA before the due date to discuss adjusting the terms.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS and California state tax programs depends on individual facts and circumstances; no outcome is guaranteed.