California Payroll Taxes

EDD Payment Plan for California Payroll Tax Debt (2026)

The short answer: an EDD payment plan is an installment agreement that lets you pay California payroll tax debt to the Employment Development Department (EDD) over time. Short plans need little paperwork; longer plans require a financial statement. Interest and penalties keep accruing, but an active, current plan generally stops new liens and levies.

Behind on EDD payroll taxes?

Send us your latest EDD notice. An experienced tax professional will review where you stand — including any personal liability exposure — and lay out your payment-plan and relief options. Free, confidential, no pressure.

⏱ Your deadline: if you received a Notice of Assessment, you generally have 30 days to file a petition disputing it before it becomes final. Once a bill is final, the EDD can lien and levy. Don't wait — set up a payment plan or respond before that 30-day window closes.

Why you owe the EDD

The EDD collects California's payroll taxes. There are four of them: Unemployment Insurance (UI), Employment Training Tax (ETT), State Disability Insurance (SDI), and the California Personal Income Tax (PIT) you withhold from employee paychecks. You can read the basics on the EDD's payroll taxes page.

Two of those — SDI and the PIT you withhold — are "trust fund" taxes. That money was your employees' money. You held it in trust and were supposed to pay it over to the state. When it isn't paid, the EDD treats it as the most serious kind of debt, because it was never yours to keep.

Most EDD payroll tax debt starts one of three ways: you filed your DE 9 quarterly returns but couldn't pay, an EDD payroll tax audit reclassified workers and created a back bill, or you fell behind during a slow stretch and the balance snowballed with penalties. However it started, a payment plan is usually the fastest way to stop the bleeding.

What happens if you ignore an EDD bill

The EDD's collection process is automated and steady. Each step adds cost and removes options:

- Statement of Account / billing notice — your balance with penalties and interest. Still just a bill.

- Notice of Assessment — the formal assessment. You have 30 days to petition before it becomes final and collectible. See our EDD Notice of Assessment guide.

- State tax lien — recorded against you or your business, damaging credit and clouding any property you own.

- Bank levy & wage garnishment — the EDD can take funds from business and personal accounts and garnish wages once a debt is final.

- Section 1735 personal assessment — the EDD can pursue owners and responsible officers personally for unpaid withholdings, even after the company closes.

The point isn't to scare you. It's that every one of these steps is avoidable if you act while you still have a choice. An EDD payment plan started today stops most of what comes after.

How an EDD payment plan works

An EDD installment agreement spreads your payroll tax debt over monthly payments you can afford. There's no single fixed term — the EDD wants the balance paid as quickly as your finances reasonably allow.

- Shorter plans (often around 12 months) are easier to approve and may need little documentation.

- Longer plans usually require a completed financial statement and proof — bank statements, income, expenses, and assets — so the EDD can see what you can genuinely pay.

- Interest and penalties continue while you pay. A plan stops new enforcement; it doesn't freeze the meter.

- You must stay current on new payroll tax returns and deposits. A new unpaid quarter can default the whole agreement.

If the business is still operating, the EDD will want to see that you can both pay the old debt and keep up with current taxes. If the business has closed, the conversation often shifts to your personal liability under Section 1735 and what a personal payment plan looks like.

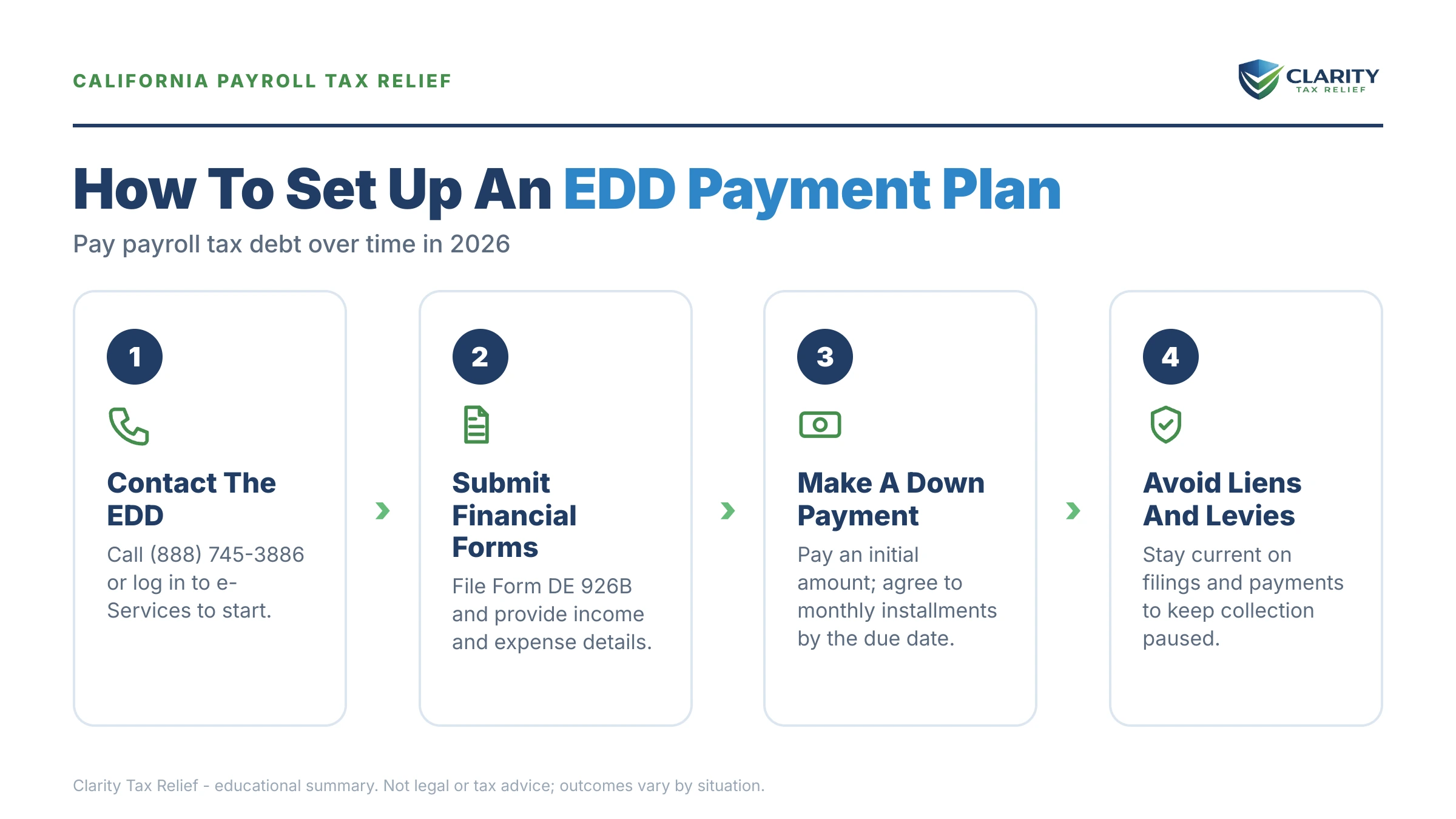

Setting up your EDD installment agreement, step by step

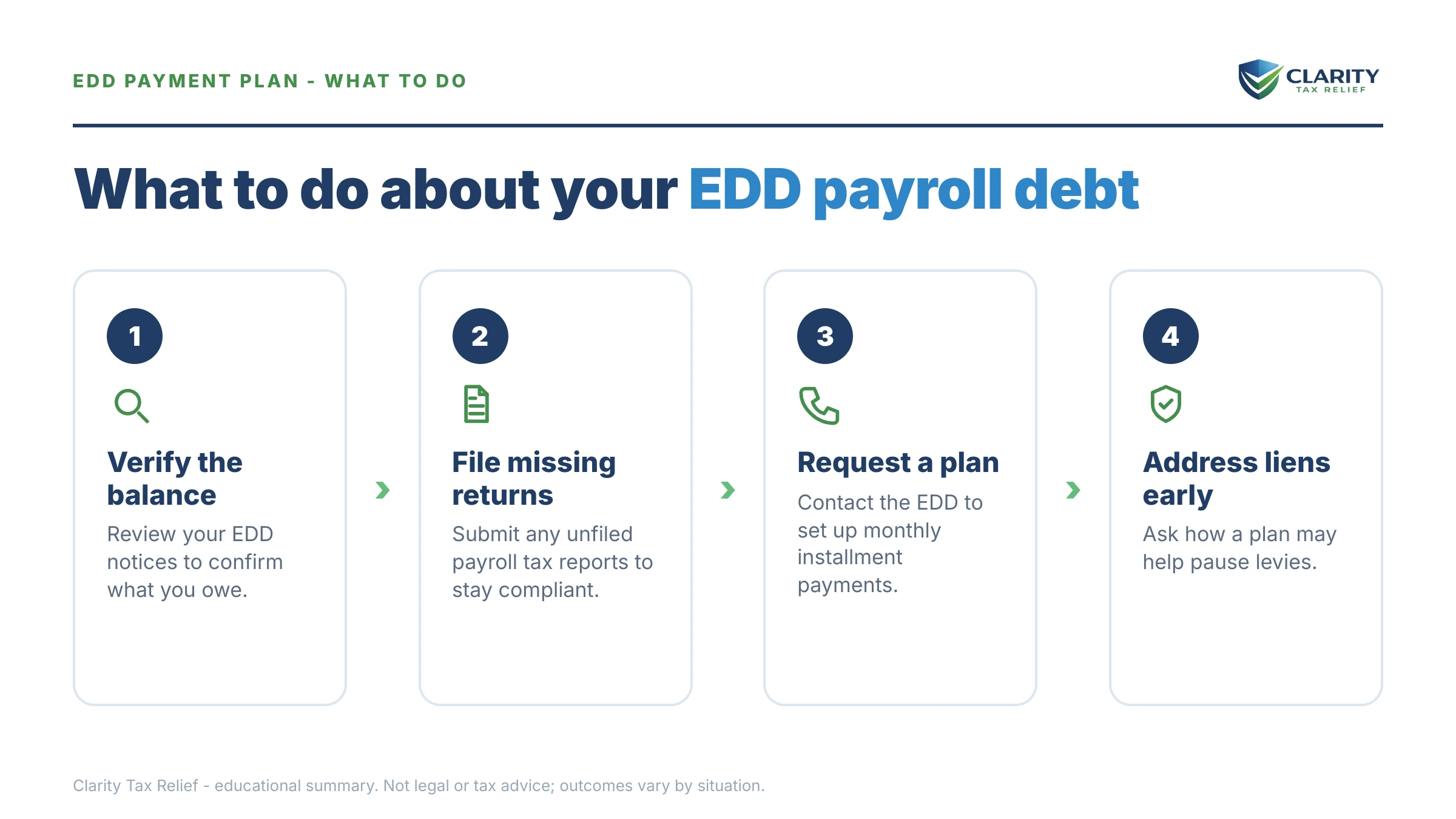

- Confirm the balance. Pull your account through the EDD's e-Services for Business and match it against your DE 9 filings. Make sure the assessment is correct before you agree to pay it.

- File any missing returns. The EDD won't finalize a plan while quarterly returns are unfiled. Get current first.

- Gather your financials. For a longer plan, prepare income, expenses, bank statements, and a list of assets. This is the EDD's version of the California financial statement process the FTB uses.

- Propose a realistic monthly amount. Offer what you can actually sustain. A plan you default on is worse than a smaller plan you keep.

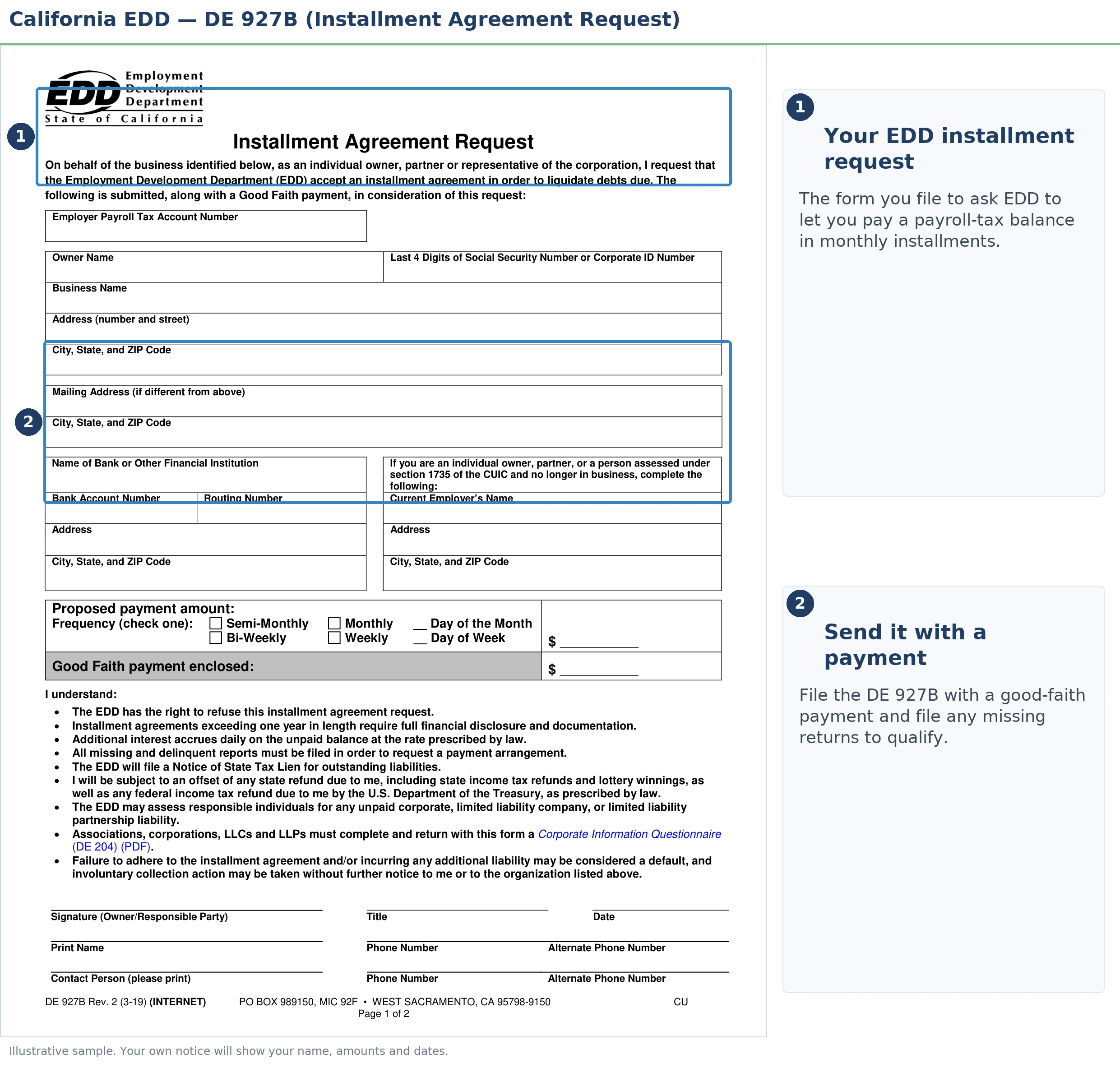

- Contact EDD collections to request the agreement, or have an experienced tax professional do it for you. Get the terms in writing.

- Stay current going forward. Pay each new quarter on time so the agreement holds.

Other options if a payment plan isn't enough

A monthly plan is the most common fix, but it isn't the only one. Depending on your situation you may also consider:

- Penalty review. If you had reasonable cause — serious illness, disaster, or circumstances beyond your control — some EDD penalties may be reduced. Always ask before assuming penalties are fixed.

- Hardship or temporary delay. If you truly can't pay anything right now, the EDD may pause active collection while your situation improves, similar to how the FTB handles financial hardship status on state income tax debt.

- Settlement programs. California's tax agencies have limited settlement avenues, but they're fact-specific and never automatic. Be skeptical of anyone promising to wipe out your debt "for pennies on the dollar" before they've reviewed your finances — that's a sales pitch, not a plan.

- Sequencing your debts. If you also owe the IRS or the Franchise Tax Board, the order you tackle them matters. Our overview of California tax debt relief options can help you build a plan that covers everything.

Whatever path fits, document it and get terms in writing. The EDD, like the IRS, runs on records — yours protect you.

Know your rights

You have the right to fair treatment and to dispute an assessment you believe is wrong. California's Office of the Taxpayer Rights Advocate exists to help when normal channels stall. If your debt also involves federal payroll taxes, the same trust-fund rules apply on the IRS side, and a coordinated approach usually saves money.

EDD payment plan questions, answered

Can I set up an EDD payment plan if I'm behind on California payroll taxes?

Yes. The EDD can set up an installment agreement that lets you pay your payroll tax debt monthly. Short plans may be approved with little paperwork; longer plans usually require a financial statement showing what you can afford. Interest and penalties continue, but an active plan generally stops new liens and levies.

How long can an EDD payment plan last?

There's no single fixed term. The EDD wants the debt paid as quickly as your finances allow. Shorter plans of around 12 months are easier to approve, while longer terms usually require a completed financial statement and supporting documents. The exact length depends on the balance and what you can genuinely afford each month.

Can I be held personally liable for my company's EDD payroll taxes?

Yes. Under California Unemployment Insurance Code Section 1735, the EDD can assess responsible individuals personally for unpaid withholdings the business collected from employees but never paid over — the state disability insurance and personal income tax that were withheld. That liability can follow you even after the business closes, so address it early.

Will the EDD file a lien or levy if I'm on a payment plan?

While a payment plan is active and you stay current, the EDD generally holds off on new bank levies and wage garnishments. The EDD may still record a state tax lien to protect its interest in some cases. If you miss a payment or a new return goes unpaid, the agreement can default and collection resumes.

What happens if I ignore an EDD payroll tax bill?

The balance keeps growing with interest and penalties, and the EDD's collection process escalates: a Statement of Account, then a state tax lien, then bank levies, wage garnishments, and intercepts of state payments. Acting before the bill becomes final gives you more options and lower cost than waiting.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.