IRS News & Enforcement

IRS Layoffs: Will I Still Get Audited in 2026?

The short answer: yes — despite the IRS layoffs, you can still get audited in 2026. The IRS cut roughly 27% of its workforce in 2025, but audit selection is computerized: document matching (CP2000), correspondence audits, and refund holds continue at scale. What slowed is the human work — phone help, appeals, and complex field exams.

You've seen the headlines about tens of thousands of IRS employees walking out the door — and somewhere in the back of your mind is a 1099 you didn't report, or a return you keep meaning to file, and the question: does anyone even check anymore? If you searched "IRS layoffs will I still get audited," you deserve the honest answer, because the wrong assumption here gets expensive. The people left. The computers didn't.

⏱ The real clock: there's no notice deadline attached to this question — but penalties and interest accrue monthly on any unpaid balance regardless of IRS staffing. The failure-to-file penalty runs 5% per month; the failure-to-pay penalty runs 0.5% per month. "Waiting out the layoffs" only makes the eventual letter bigger.

What the IRS layoffs actually changed — and what still runs on autopilot

The IRS lost roughly 27% of its workforce in 2025, but audit selection, notice mailing, refund holds, and many levies are run by computer systems that were never laid off. That single distinction — human work versus automated work — answers almost every question people are asking about the cuts.

The human side shrank hard: phone assistors, revenue agents who run complex exams, appeals officers, and the clerks who process paper mail. That's why hold times ballooned and why paper responses sit for months — we cover the backlog in detail in IRS layoffs 2026 processing delays and what it means for open cases in IRS budget cuts 2026.

The automated side kept humming. Every W-2 and 1099 filed by employers, banks, brokers, and payment platforms still flows into IRS matching systems. The collection notice stream still mails on schedule. Refund-screening filters still freeze suspicious returns. None of those systems needs a human to start acting against you — a human only becomes necessary when you want to argue, appeal, or fix something.

That's the trap in the layoff headlines: enforcement stayed automatic while help became scarce. The machine that bills you is fine. The person who could straighten out its mistake is the one who's gone.

IRS layoffs: will I still get audited — and by what kind of exam?

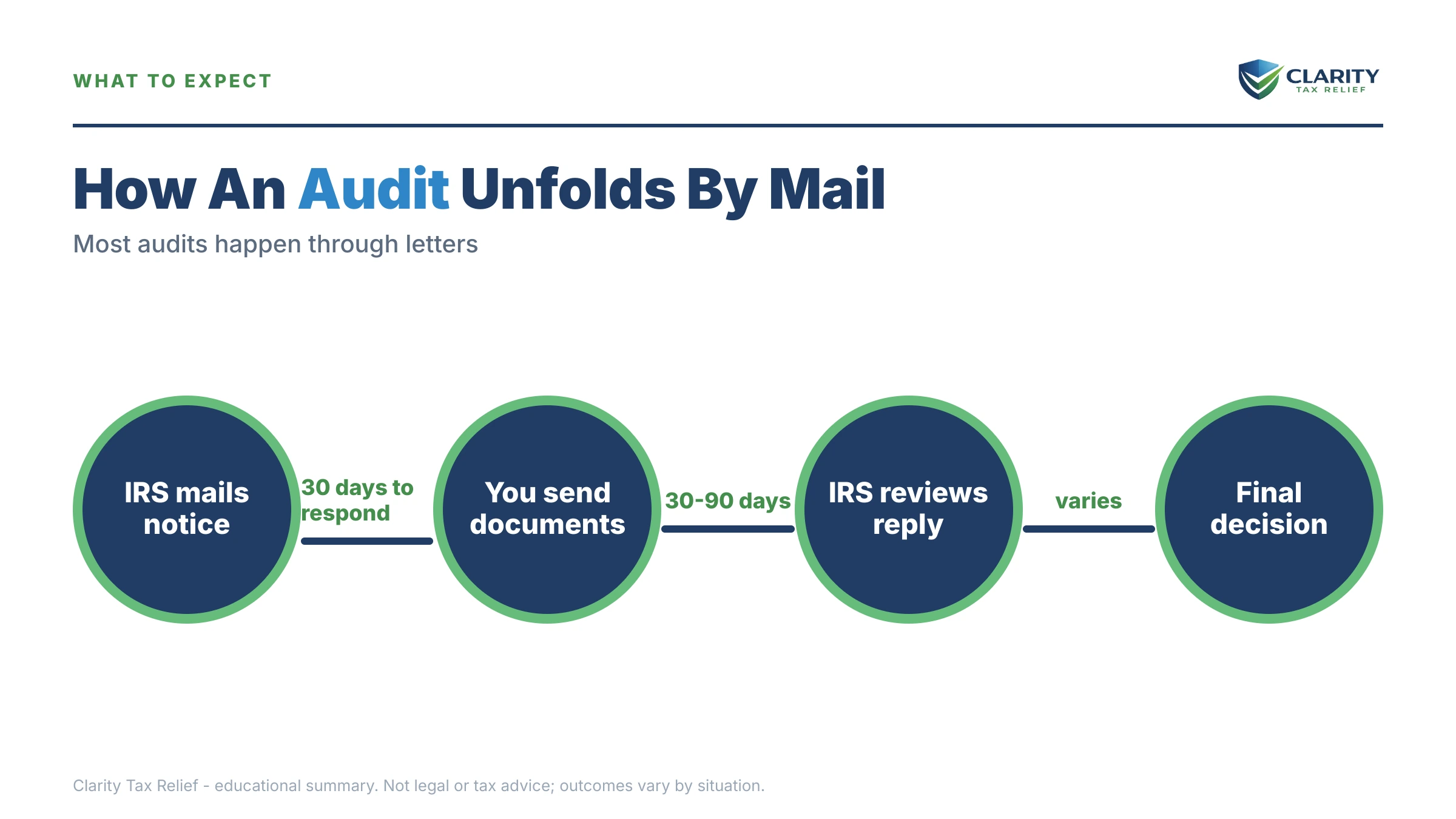

Yes, you can still get audited after the IRS layoffs, because most IRS exams are computer-selected reviews conducted by mail — not agents knocking on doors. The staffing cuts changed which kinds of scrutiny got rarer, not whether scrutiny exists. Here's the breakdown:

| Type of review | How it's run | Effect of the layoffs |

|---|---|---|

| CP2000 document match (Automated Underreporter) | Computer compares W-2s/1099s to your return; letter generated automatically | Largely unaffected — still the most common way a W-2 filer hears from the IRS |

| Correspondence (mail) audit | Computer-selected; conducted entirely by letter with limited staff review | Continuing; IRS responses to your replies are slower |

| Refund review holds (identity/withholding screens) | Automated filters freeze the refund before any human looks | Continuing — and holds take longer to release with fewer staff |

| Office audit (appointment at an IRS office) | Requires a tax compliance officer's time | Slowed; fewer opened, longer to schedule |

| Field audit (agent at your home or business) | Revenue-agent intensive, often months of work | Hit hardest; remaining capacity concentrates on high-income and business returns |

Notice what that table means for you specifically. If you're a W-2 employee, your realistic "audit" risk was never a suit at your door — it was always the automated match against the forms your employer and your broker filed. That risk is intact. Meanwhile, selection is getting more automated, not less: the IRS is leaning on algorithmic scoring to replace lost human screeners, a shift we break down in IRS AI audits. For baseline numbers by income level, see your real odds of being audited.

Two more things the layoffs did not change. First, the clock: the IRS generally has three years from the date you file to assess more tax — six years if you left more than 25% of your income off the return, and forever if you never file. A thin audit year now doesn't protect you; it just delays the letter while interest builds. The full statute rules are in how far back can the IRS audit. Second, the paper trail: third parties keep filing information returns about you every January whether the IRS reads them this year or in two years.

If you're self-employed or run a cash-heavy operation, your calculus is different: field-audit capacity dropped, but when an exam does open, the techniques are aggressive — indirect income reconstruction is standard, as covered in cash business audit and bank deposit method audit. Fewer audits does not mean gentler audits.

What happens if you ignore taxes because the IRS is "too understaffed"

Ignoring a tax balance during the IRS layoffs pauses nothing — penalties and interest accrue monthly, and the automated collection stream keeps mailing on schedule. The sequence below runs without a single human decision, which is exactly why understaffing doesn't slow it down (more on that paradox in IRS understaffed do I still owe):

- A balance posts. Filed and didn't pay, or a CP2000 proposal you never answered became an assessment. Failure-to-pay penalty and daily-compounding interest start.

- CP14 — the first bill. You typically have about 21 days from the notice date before the system queues the next letter.

- CP501 / CP503 — reminders. Still just bills, but the balance grows every month they go unanswered.

- CP504 — intent to levy. The IRS can now take your state tax refund, and a federal tax lien becomes realistic.

- LT11 / Letter 1058 — final notice. A 30-day clock starts on your Collection Due Process rights (Form 12153). After it runs, wage and bank levies are on the table.

- Levy. A bank levy holds your funds for 21 days before they're sent to the IRS; a wage levy is continuous until released. Never file at all, and the IRS can eventually create a substitute return for you — with zero deductions.

| Notice | What it does | Your response window |

|---|---|---|

| CP14 | First bill for the assessed balance | Typically 21 days from the notice date |

| CP501 / CP503 | Reminder bills; balance keeps compounding | The "pay by" date printed on each notice |

| CP504 | Intent to levy — state refund can be seized | The date printed on the notice |

| LT11 / Letter 1058 | Final notice of intent to levy; appeal rights attach | 30 days to request a CDP hearing (Form 12153) |

| Levy | Bank funds or wages taken | Bank funds held 21 days before release to the IRS |

One more number worth burning in: the failure-to-file penalty is ten times the failure-to-pay penalty — 5% per month versus 0.5%. If the layoffs tempted you to skip filing, that's the single costliest way to act on the news. File, even broke.

Hoping the layoffs bought you time on a balance or an unfiled year?

They didn't — interest and penalties accrue every month while the automated notices keep coming, and the humans who could fix errors are harder to reach than ever. Get your situation reviewed free by an experienced tax professional before the machine escalates: call (888) 825-7779 or use the 2-minute form.

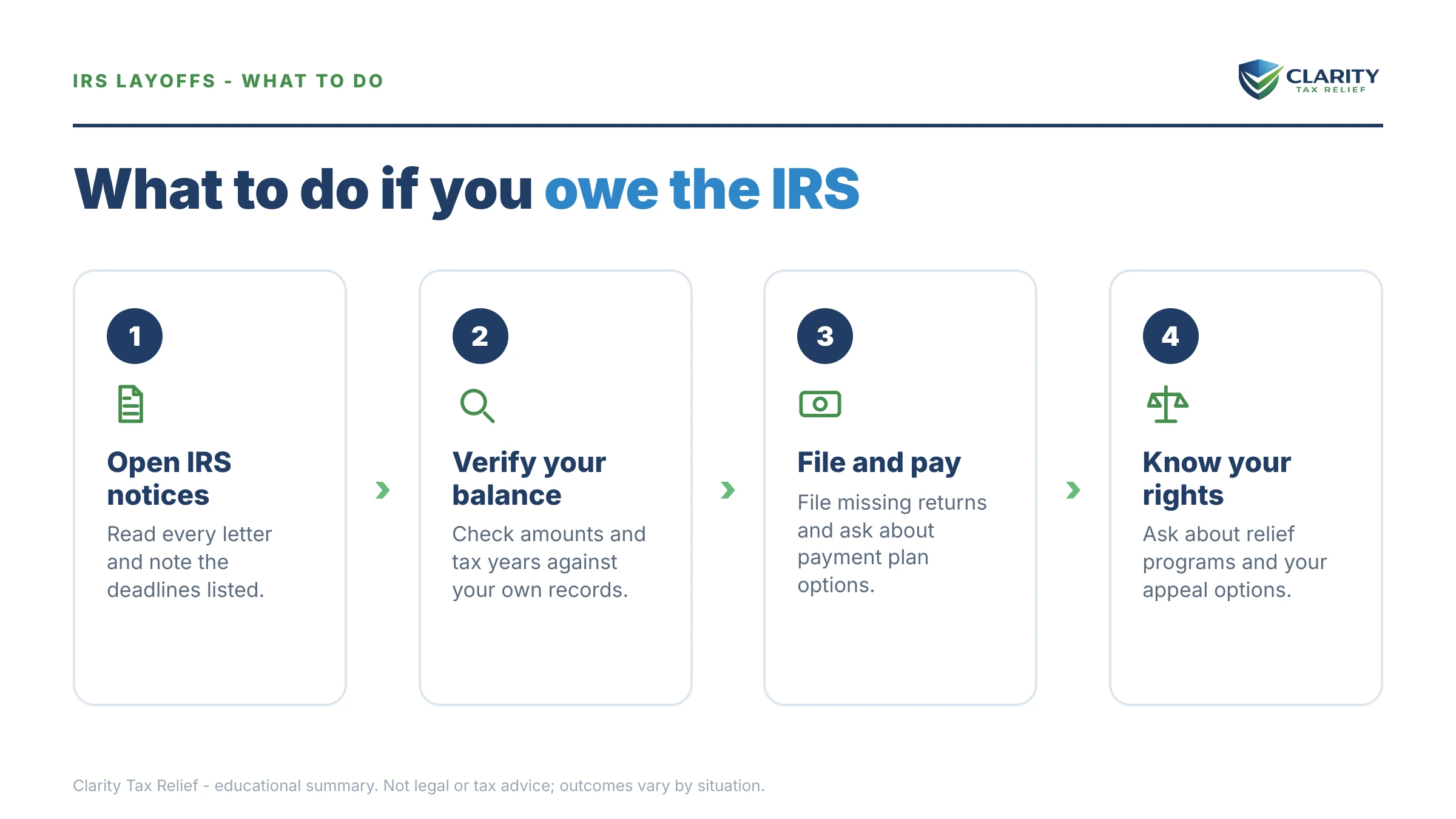

Your options if you owe: the layoffs didn't change the programs

Every IRS resolution program survived the staffing cuts, and most can be set up online without ever waiting on hold. If a matching notice or old balance surfaces, your menu looks like this: a short-term plan gives you up to 180 days with no setup fee; a long-term installment agreement covers balances up to $50,000 over as many as 72 months, set up entirely online (details at the IRS payment plans page); Currently Not Collectible status pauses collection if paying would create genuine hardship; and an Offer in Compromise settles for less than the full balance only when the math shows the IRS could never collect it — the IRS accepted roughly 1 in 5 offers in FY2024, so treat anyone promising approval as a red flag.

Penalty relief also still exists — and it's actually getting easier. First-time penalty abatement can wipe penalties if your prior three years were clean, and starting in summer 2026 the IRS is rolling out the Automatic Exemption from Penalty (AEP), which applies qualifying relief automatically with no request needed.

Say you owe $4,800: what "waiting out the layoffs" actually costs

Here's a clearly hypothetical example. Say you're a W-2 employee filing single, and a brokerage 1099-B you forgot about triggers a CP2000 that becomes a $4,800 balance. If you decide the understaffed IRS won't chase it and wait a year, the failure-to-pay penalty alone adds 0.5% × 12 months = $288, and interest at the IRS's quarterly rate — compounding daily — typically adds several hundred more. You'd owe roughly $5,400+ for the privilege of waiting, and the automated notice stream would be at the intent-to-levy stage.

Act instead, and the same $4,800 is small enough for the easiest tools the IRS offers: a 180-day short-term plan means about $800 a month for six months with a $0 setup fee, or a 72-month agreement runs about $67 a month before accruals (and because the balance is under $10,000, you'd generally fit the guaranteed installment agreement rules). You can estimate your own penalty and interest buildup with our Penalty & Interest Calculator.

How to protect yourself during the IRS layoffs, step by step

- Pull your IRS online account. Log in at IRS.gov to see your balances, notices, and whether any return shows as missing — don't wait for mail that moves slower now.

- File every unfiled return. The failure-to-file penalty (5% per month) is ten times the failure-to-pay penalty; filing stops the worst bleeding even if you can't pay a dollar.

- Verify any IRS letter before you act. Scammers exploit layoff headlines; real IRS contact starts with postal mail, and payments go only to the United States Treasury or through IRS.gov.

- Respond to audit and CP2000 letters by the printed date. Automated deadlines don't flex for staffing; a missed response window converts a proposal into an assessed debt.

- Set up a payment arrangement online if you owe. Balances under $50,000 can usually be put on a plan at IRS.gov without waiting on hold, and an active agreement stops the escalation sequence.

Step 4 deserves emphasis in 2026: because IRS correspondence processing is slow, your response can sit unread while the system's deadline passes. Send replies certified, keep copies, and if you disagree with an exam result, know that appeal rights still exist and still work — see IRS audit appeal for how to preserve them.

When you can handle this yourself — and when help changes the outcome

Most people asking this question can handle their situation alone, and it's worth saying plainly. If you're a W-2 filer with returns filed on time and no letters, do nothing — you're not "flagged," and the layoffs are background noise. If a CP2000 notice arrives and the IRS is simply right about a form you missed, agreeing and paying (or setting up a plan under $50,000 online) needs no professional. If you owe an amount you can clear within 180 days, the free short-term plan is a ten-minute task.

Experienced help changes outcomes in a specific set of situations, and the layoffs made each one harder to solve alone: a levy already in motion when no human answers the phone (the Taxpayer Advocate Service exists for exactly these breakdowns); multiple unfiled years where the filing order affects what you ultimately owe; a correspondence audit that's expanding into more years or issues; business or payroll tax debt, where personal liability rules bite; and any Offer in Compromise, where the math has to be right before you apply. In each of those, the cost of a wrong first move exceeds the cost of getting it reviewed.

Terms in the layoff headlines, decoded

- Automated Underreporter (AUR): the computer program that matches W-2s and 1099s to your return and generates CP2000 notices with no human review.

- Correspondence audit: an examination conducted entirely by mail — the most common audit type, and the one least affected by staffing cuts.

- Revenue agent: the human examiner who runs office and field audits — the role the layoffs actually thinned.

- ACS (Automated Collection System): the computerized collection arm that issues notices, liens, and many levies without a caseworker assigned.

- Assessment statute: the IRS's window to charge more tax — generally 3 years from filing, 6 for large omissions, unlimited if you never file.

- Substitute for Return (SFR): the return the IRS eventually files for a non-filer, using only reported income and none of your deductions.

IRS layoffs and audits: your questions answered

details class="faq-item">No. The IRS lost roughly 27% of its workforce in 2025, but audit selection and document matching are handled by computer systems that kept running. Mail-based correspondence audits and CP2000 underreporter notices continue at scale; the exams that genuinely slowed are labor-intensive field audits of complex businesses and high-income returns. If your issue is a mismatched W-2 or 1099, the layoffs offer no protection at all.

Are my chances of being audited lower in 2026?

For computer-selected issues — unreported 1099s, mismatched withholding, questionable refundable credits — your odds are roughly unchanged, because those reviews need almost no staff. Odds fell mainly for in-person field audits, which concentrate on businesses and high earners. A W-2 employee's most likely 'audit' was always the automated CP2000 match, and that program is still running.

Can I skip filing my taxes because the IRS is understaffed?

No — this is the most expensive conclusion you could draw from the layoff headlines. The failure-to-file penalty is 5% of the unpaid tax per month, ten times the 0.5% failure-to-pay penalty, and it accrues whether or not anyone at the IRS ever contacts you. If you skip filing, the IRS can eventually file a substitute return for you with none of your deductions or credits.

Will the IRS catch a 1099 I didn't report even though it's short-staffed?

Very likely, yes — 1099 matching is fully automated. Every 1099 your payers file goes into the IRS's Automated Underreporter system, which compares it to your return by computer and generates a CP2000 proposal without a human ever opening your file. The notice often arrives a year or more after you file, with interest calculated back to the return's original due date.

Does the IRS still send CP2000 notices during the layoffs?

Yes. CP2000 notices come from the Automated Underreporter program, which is computer-driven and largely unaffected by staffing cuts. What changed is what happens after you respond: with fewer employees processing correspondence, disputes can take longer to resolve. Respond by the deadline printed on the notice and keep proof of everything you send.

How long does the IRS have to audit me?

Generally three years from the date you file, and six years if you omitted more than 25% of your income; there is no time limit at all if you never file or the return is fraudulent. The layoffs don't shorten these windows — a return the IRS doesn't examine this year can still be examined next year, with more interest attached to any balance.

Do IRS collections stop during layoffs or budget cuts?

No. Collection notices, refund offsets, liens, and many levies are issued by the Automated Collection System and continue regardless of staffing. In fact, understaffing can make collections feel harsher, because it's harder to reach a human who can pause enforcement or fix an error while the automated deadlines keep running.

Your next 24 hours

- Log into your IRS online account. Check for balances, holds, missing returns, and notices you haven't seen — it's the only IRS channel the layoffs didn't slow, and payments can be made there directly at IRS.gov/payments.

- Gather your paper trail. Last year's return, every W-2 and 1099 you received, and any IRS letter in the drawer — five minutes of gathering tells you whether anything is actually mismatched.

- Get a free case review if anything is off. An unfiled year, a notice you ignored, or a balance you can't pay won't wait out the layoffs — interest and penalties accrue monthly either way. Call (888) 825-7779 or use the free consultation form and an experienced tax professional will map your exact options.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.