Levies & Seizures

IRS Seized Business Assets: Levy on a Going Concern and Your Alternatives (2025)

The short answer: if the IRS seized business assets, it's because a tax debt — usually unpaid payroll taxes — went unaddressed after several warning notices. You still have options. The IRS must release a levy or seizure if it causes hardship, if you set up a payment agreement, or if the seizure was premature. Act now: a fast, organized response is what gets assets released.

The IRS already took business assets — or threatened to?

Don't wait for the auction notice. Send us the letter or the seizure paperwork and an experienced tax professional will tell you exactly what can still be released and how — free, confidential, no pressure.

⏱ Your deadline: if assets were already taken, time is short — the IRS may sell seized property after a public-notice period (often around 10 days minimum for the notice, then a set sale date). If you only received a Final Notice of Intent to Levy, you have 30 days to request a Collection Due Process hearing and stop the seizure before it happens.

Why the IRS seized your business assets

The IRS almost never seizes business assets out of the blue. A seizure is the end of a long, automated chain of notices that started months — sometimes more than a year — earlier. By the time a revenue officer is loading equipment or padlocking a door, the agency believes it has run out of softer options.

The most common reason a business gets here is unpaid employment taxes — the income tax, Social Security, and Medicare you withhold from employee paychecks. The IRS calls this "trust fund" money because you collected it on the government's behalf. When it isn't deposited, the IRS treats it far more seriously than ordinary income tax, because, in its view, you spent money that was never yours. If you've fallen behind here, our guide to 941 back taxes for a business walks through exactly what happens.

That seriousness has a personal edge. Through the Trust Fund Recovery Penalty, the IRS can hold owners, officers, and even bookkeepers personally liable for the withheld portion of the debt — meaning a business seizure can follow you home.

What "seizure on a going concern" actually means

A "going concern" is a business that's still operating. The IRS distinguishes between seizing scattered assets and seizing an entire operating business — and the second is treated as an extreme step.

Seizing a going concern requires high-level approval inside the IRS, because shutting down a working business usually destroys the very value the IRS is trying to collect. Used restaurant equipment or a half-finished inventory sold at a forced auction rarely brings what the business is worth running. This is your leverage: the IRS generally collects more from a business that stays open and pays than from one it liquidates.

What happens if you ignore it

If you do nothing, the automated collection system keeps escalating. Each step carries more enforcement power than the last:

- CP504 — Notice of Intent to Levy. The IRS can seize state tax refunds and signals that levies are coming. See our CP504 notice guide.

- LT11 / Letter 1058 — Final Notice of Intent to Levy. After 30 days, the IRS can levy bank accounts, accounts receivable, and physical assets. This is the last clean window to request a hearing.

- Revenue officer assignment. Business cases — especially payroll cases — are often handed to a person, not a computer. Learn the difference in our guide to what an IRS revenue officer is.

- Bank and receivables levies. The IRS drains accounts and orders your customers to pay it instead of you. This alone can starve a business of cash.

- Seizure of physical assets. Equipment, vehicles, inventory, and in some cases the premises. The IRS posts public notice and sells the property at auction.

The lesson isn't that the IRS is out to get you. It's that the system is automated and unforgiving of silence. Every step is reversible if you engage — and far harder to reverse once assets are gone.

How to get seized business assets released

By law, the IRS must release a levy or seizure when any of these apply:

- The seizure creates an economic hardship — it prevents you from meeting basic, necessary business or living expenses.

- You enter an installment agreement that doesn't allow the levy to continue.

- Releasing the levy would actually help the IRS collect the tax (the going-concern argument).

- The seizure was premature or didn't follow proper procedure.

- The value of the property exceeds the debt and a partial release won't hinder collection.

Our guide on an emergency levy release for hardship covers how to document a hardship request. The official rules are on the IRS pages for IRS levies and getting help with tax debt.

Your alternatives to losing the business

The notice makes it feel like the choice is "pay in full or lose everything." It isn't. Depending on your situation, these may apply:

- Installment agreement. A monthly payment plan on the business balance. Getting current and proposing realistic payments is often enough to win a levy release.

- Currently Not Collectible status. If the business genuinely can't pay anything right now without folding, collection can be paused. The debt stays, but seizures stop.

- Offer in Compromise. A settlement for less than the full balance — real, but only when the IRS's own math shows you can't pay the full amount. Anyone promising to settle for "pennies on the dollar" before reviewing your books is selling you something, not helping you.

- Trust Fund Recovery Penalty defense. If the IRS is trying to hold you personally responsible, who was actually "responsible and willful" is a fact-specific fight worth having early.

- Get current going forward. No agreement survives if new payroll deposits go unpaid. Staying current on the current quarter is the price of every alternative above.

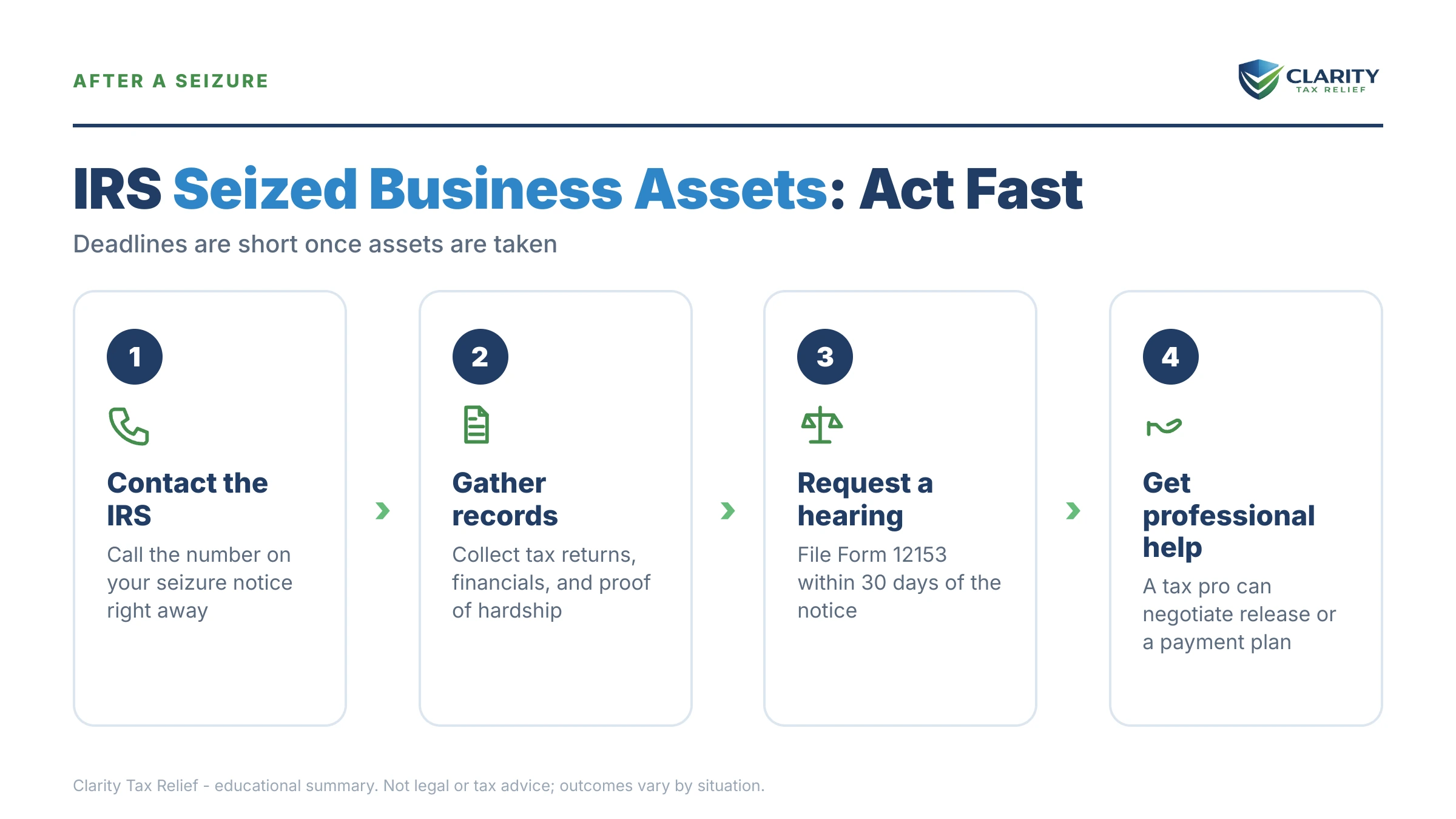

How to respond, step by step

- Find out exactly where you are. Is this a Final Notice (a warning) or an actual seizure (assets taken)? The letter or the revenue officer's paperwork will say. A Letter 725-B revenue officer visit means a person is now on your case.

- Contact the revenue officer immediately. Their direct number is on the notice. Returning that call — calmly and quickly — is the single biggest factor in getting a release. Silence is what triggered the seizure.

- File every missing return and tax deposit. The IRS will not negotiate while you're non-compliant. File the delinquent 941s and make the current deposit first.

- Build a payment proposal. Pull together a profit-and-loss statement, bank records, and a realistic monthly figure. This is the document that converts "we're seizing this" into "let's set up a plan."

- Request a hearing if you're still within 30 days. A Collection Due Process hearing can pause collection and put your case in front of the independent Appeals office.

- Get experienced help on payroll cases. Trust-fund cases carry personal liability and move fast. An experienced tax professional can talk to the revenue officer for you and protect you and the business at the same time.

Business asset seizure questions, answered

Can the IRS shut down my business by seizing its assets?

It can, but it's rare and it's a last resort. The IRS usually levies bank accounts and receivables first. Seizing physical assets like equipment or inventory requires manager approval and, in most cases, a court order. The goal is to collect the debt, not to destroy the business — which is why a fast response often gets the seizure released.

How do I get the IRS to release seized business assets?

Contact the revenue officer assigned to your case right away and ask about a release. The IRS must release a levy if it creates an economic hardship, if you set up an installment agreement, if the seizure was premature, or if releasing it would actually help collect the tax. File any missing returns and bring a payment proposal — that's what moves a release fastest.

What kind of business tax debt leads to seizures?

Unpaid payroll (941) taxes are the most common trigger. The IRS treats withheld employee taxes as trust-fund money the business held on the government's behalf, so it pursues those debts aggressively and can hold owners and officers personally liable through the Trust Fund Recovery Penalty.

Will I get warning before the IRS seizes my equipment?

Almost always, yes. Before seizing assets the IRS must send a Final Notice of Intent to Levy and give you 30 days to request a Collection Due Process hearing. If you're getting CP504, LT11, or a revenue officer visit, you are in the warning window — that's the time to act, before anything is taken.

Can I keep operating while I owe the IRS business taxes?

Yes, if you address the debt. The IRS would rather have a paying, operating business than a pile of used equipment sold at auction. An installment agreement, currently-not-collectible status, or an offer in compromise can let you stay open while you resolve the balance — but you must stay current on new tax deposits going forward.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. If you believe a seizure is causing immediate, serious harm, you can also contact the Taxpayer Advocate Service, an independent organization inside the IRS.