IRS Notices

IRS CP62 Notice: We Applied a Payment to Your Account (2025)

The short answer: a CP62 notice means the IRS applied a payment or credit to your tax account and is confirming where it went. It's usually good news, not a bill. Verify the payment landed on the correct year, and respond within 60 days if anything looks wrong.

Not sure your CP62 is correct?

Send us a photo of it. An experienced tax professional will read your account, confirm the payment went to the right year, and flag anything that needs fixing — free, confidential, no pressure.

⏱ Your deadline: there's no payment due, but if the notice applied your money to the wrong tax year or account, contact the IRS within 60 days. The longer a misapplied payment sits, the longer the correct year keeps building penalties and interest as if you never paid.

Why you got a CP62

A CP62 notice goes out when the IRS locates a payment or credit and applies it to one of your tax accounts. Most often it's a payment you made — a check, an online payment, or an estimated tax deposit — that the IRS matched to a balance after the fact. Sometimes it's a credit transferred from another year or from a spouse's account.

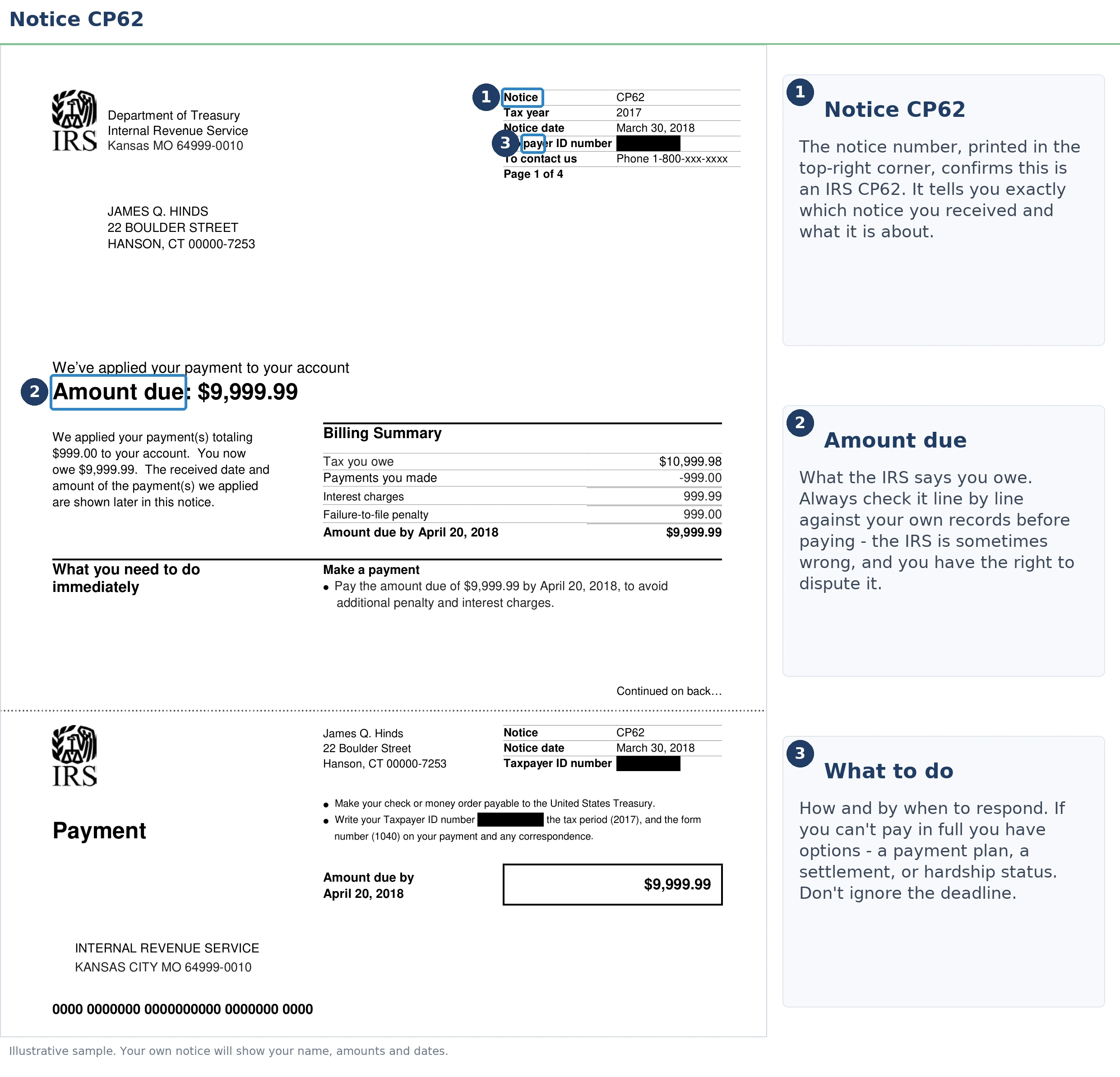

In plain terms: the IRS found money, decided where it belonged, and is telling you. The notice shows the tax year it touched, the amount applied, and your new balance (if any). Unlike a CP14, this is not a demand for money — it's a receipt.

It helps to know how a CP62 fits with its close cousins. A CP60 notice tells you the IRS removed a payment from an account. A CP49 notice tells you the IRS took your refund and applied it to back taxes. A CP62 is the "we added a payment" version of the same family.

What a CP62 actually means for you

For most people, a CP62 is a relief. The money you sent did its job, and the notice proves it. There are only a few outcomes:

- Your balance dropped to zero. The payment covered the debt. Keep the notice and you're done.

- Your balance dropped but isn't gone. The payment helped; you still owe the rest. Plan to pay the remainder or set up an arrangement.

- The payment created a credit. You may be owed a refund or the credit may roll to another year.

- The payment went to the wrong place. This is the one to catch — it's rare, but it's the reason to read the notice carefully.

What to check before you file it away

Spend ten minutes confirming the IRS got it right. Misapplied payments do happen, and the system won't always fix them on its own.

- The tax year. Does the notice apply your payment to the year you intended? A 2024 payment posted to 2023 leaves your real balance untouched.

- The amount. Match the figure on the notice to your payment confirmation or canceled check.

- Your IRS online account. Log in and compare. The IRS online account shows balances by year, and your account transcript shows the exact payment posting.

- The notice is real. A genuine CP62 arrives by postal mail and never asks you to send money — it confirms money already applied. Anyone calling or texting about it asking for gift cards, wire transfers, or app payments is a scammer.

The IRS explains the notice in its own words on the Understanding your CP62 notice page.

What happens if a misapplied payment isn't fixed

If the payment landed correctly, nothing happens — you're finished. But if the IRS applied your money to the wrong year and you leave it, the system treats the year you meant to pay as still unpaid. That can set off the automated collection sequence on a debt you actually already covered:

- Balance stays open on the correct year, quietly adding the 0.5%-per-month failure-to-pay penalty plus interest.

- CP14 — the first bill arrives for a balance you thought you paid.

- CP501 / CP503 — reminder notices, with the balance still growing.

- CP504 — Notice of Intent to Levy, which can take your state refund and signals a federal tax lien may follow.

None of this should happen if you catch the error early. That's the whole point of reading the CP62 closely the day it arrives.

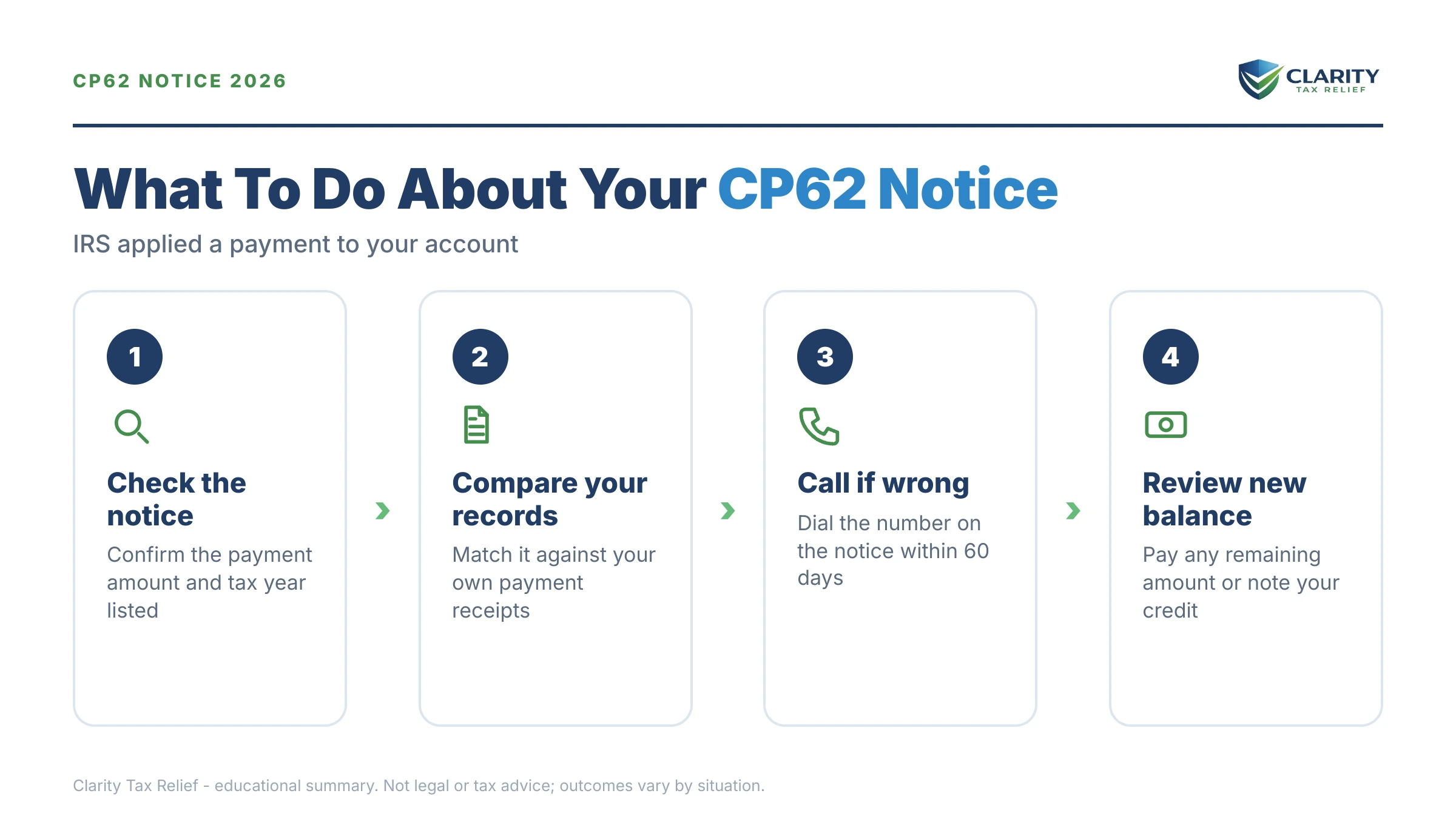

How to respond, step by step

- Read the notice. Note the tax year, the amount applied, and the new balance.

- Verify in your online account. Confirm the payment posted to the right year and the balance matches what you expect.

- If it's correct: keep the notice with your tax records. No response is needed.

- If the year or amount is wrong: call the number printed on the notice within 60 days. Have your payment confirmation and the notice in front of you, and ask the IRS to move the payment to the correct account.

- If a balance remains: pay it at IRS.gov/payments, or set up a plan if you can't pay in full.

- If the credit created an unexpected refund: make sure no other year is owed first — the IRS often applies overpayments to other balances before sending cash.

CP62 questions, answered

Is a CP62 notice good or bad news?

It's usually good news. A CP62 simply confirms the IRS found a payment or credit and applied it to your tax account. It's not a bill and not an audit. The only thing to watch for is whether the money landed on the correct tax year and balance.

What do I do when I get a CP62 notice?

Read which tax year and amount the notice shows, then log into your IRS online account and confirm the payment posted where it should have. If everything matches, keep the notice with your records — no response is needed. If the year or amount is wrong, contact the IRS within 60 days.

What if my CP62 applied the payment to the wrong year?

Call the number on the notice and ask the IRS to move the payment to the correct year. Have your payment confirmation and the notice in front of you. Until it's fixed, the year that should have the payment may still show a balance and accrue penalties and interest, so don't wait.

Do I need to respond to a CP62 notice?

If the payment was applied correctly, you don't have to respond — just save the notice. You only need to act if the tax year, the amount, or the account is wrong, or if the credit created a refund you didn't expect. In those cases, contact the IRS within 60 days.

How do I know my CP62 is real and not a scam?

A real CP62 arrives by postal mail and never asks for payment by gift card, wire, or app. It confirms money already applied — it doesn't demand money. Verify everything by logging into your account at IRS.gov, and never call a phone number from a text or email claiming to be the IRS.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.