IRS Notices

IRS CP05 Notice: Why Your Refund Is on Hold and What to Do in 2026

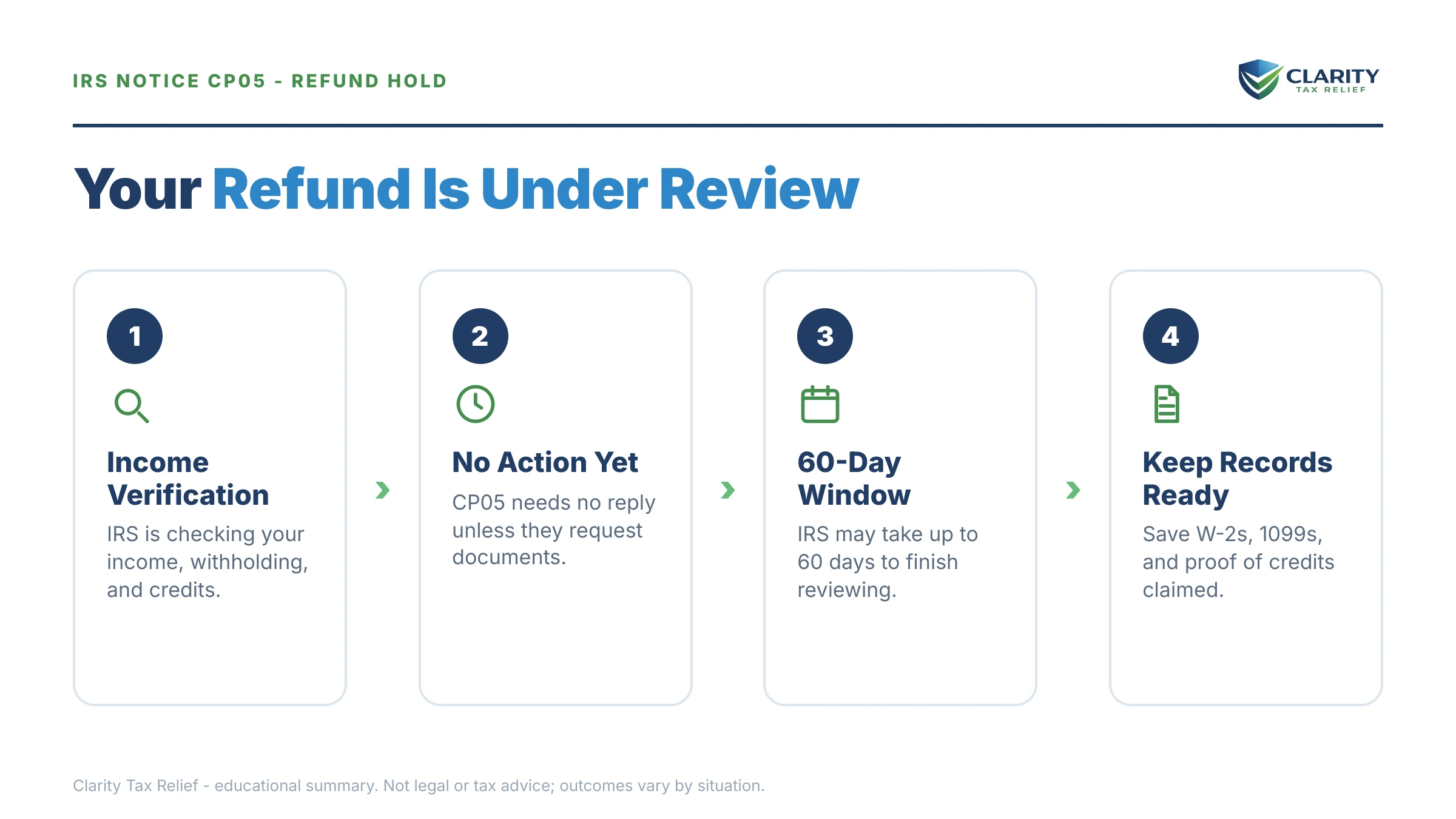

The short answer: a CP05 notice means the IRS is holding your tax refund while it verifies the income, withholding, and credits you reported. You don't owe money, it isn't an audit, and the first CP05 requires nothing from you — the notice typically gives the IRS 60 days to finish its review.

You filed your first return on your own after the divorce, watched "Where's My Refund" sit frozen for weeks, and now a letter arrived saying your money is "under review" — with no amount to pay, no form to send, and no explanation of what triggered it. That limbo is the whole point of a CP05: the IRS is checking your numbers against its records before it pays you.

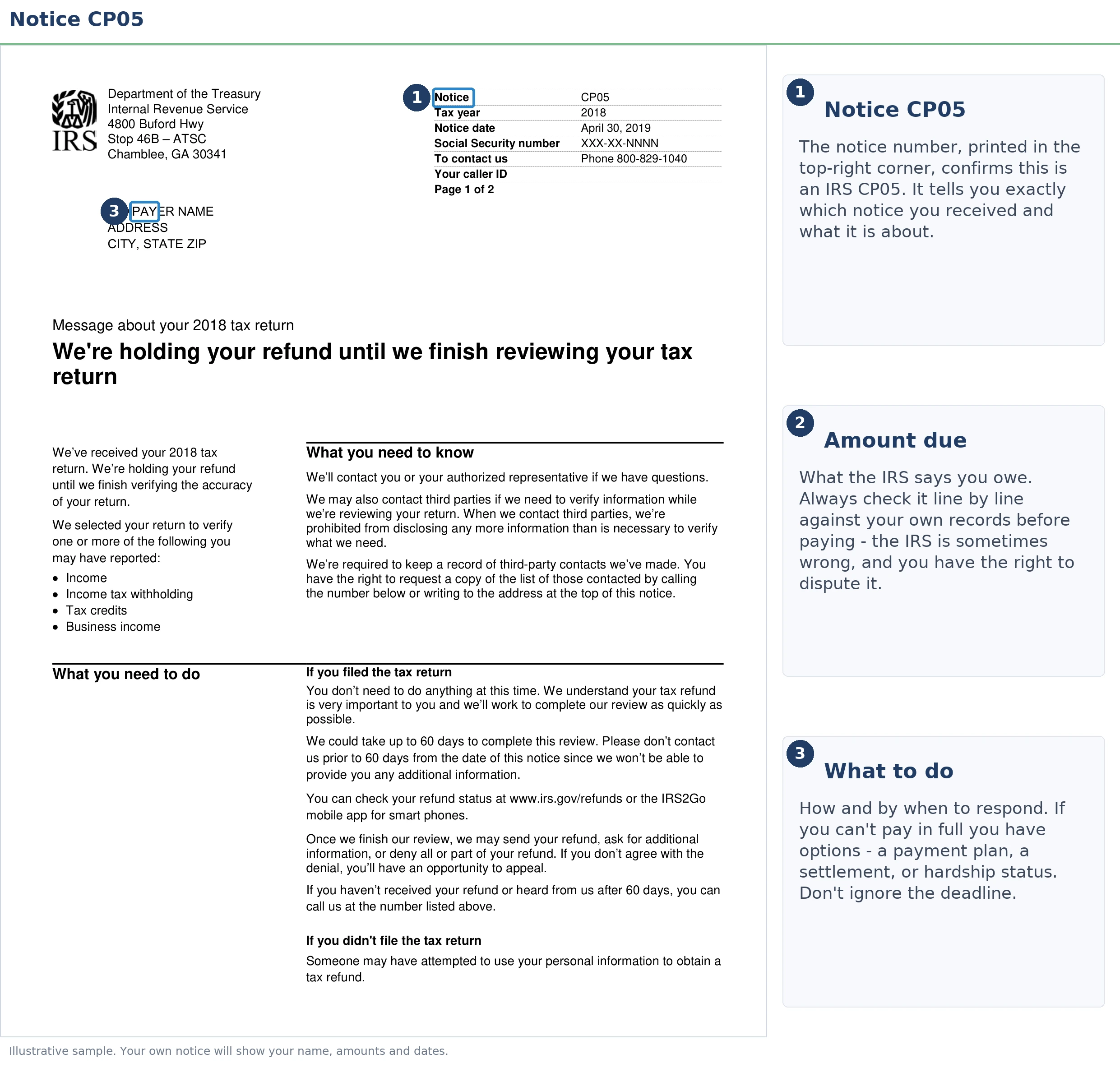

The good news is that most CP05 reviews end with the refund released, untouched. The image below shows you exactly what a CP05 looks like and where to find the review-window date — the one date on this letter that actually matters.

⏱ The clock runs on the IRS, not you. Your CP05 states a review window — typically 60 days from the notice date. You have no deadline on the first CP05. Mark the window's end date on your calendar: that is the day you're entitled to start demanding answers. And if the refund arrives more than 45 days after the filing deadline (or your filing date, if later), the IRS adds interest to it.

Why you got a CP05 notice

The IRS sends a CP05 when its verification systems can't immediately confirm something on your return — usually the income, the federal withholding, or a refundable credit. Your return got routed to a review unit before your refund was paid, and the CP05 is the letter telling you so. (Background on how the IRS decides who gets which letter is in our guide to why did I get a letter from the IRS.)

The most common triggers are specific and mechanical, not accusations:

- Withholding mismatch. The withholding on your return doesn't match what your employers reported on W-2s and 1099s — because a W-2 was filed late, an employer made an error, or a number was transposed.

- Refundable credits. The Earned Income Tax Credit and Additional Child Tax Credit are the most-verified lines on any return, especially when the dependents claimed are new to your return.

- A return that looks different from last year's. A filing status change — married filing jointly one year, head of household the next — plus new dependents plus a new withholding pattern is exactly the profile a divorce-year return presents.

- Payments the IRS credited differently than you claimed. Estimated payments made under a joint account during the marriage may sit under your ex-spouse's SSN even though you're the one claiming them.

Notice what's not on that list: fraud findings, audit selection, or a balance due. A CP05 review is run by the IRS's Integrity and Verification Operations unit, and its only question is "can we confirm these numbers before we pay this refund?" If the answer is yes, the money moves.

What a CP05 hold looks like in dollars: a worked example

A CP05 costs you time, not money — but on a large refund, the time is expensive. Say you finalized a divorce last year and your refund is $31,200, built like this (hypothetical numbers):

- Federal withholding from your W-2: $27,600 — set at married rates early in the year and never adjusted after the divorce.

- Estimated payments your attorney had you make against the settlement year: $16,000.

- Total payments: $27,600 + $16,000 = $43,600.

- Actual tax as head of household with two kids, after the Child Tax Credit: $12,400.

- Refund: $43,600 − $12,400 = $31,200.

To the verification system, that return has four flags stacked: a filing-status change, two dependents appearing on your SSN for the first time, withholding far above the tax owed, and $16,000 in estimated payments that may still be credited under a joint or ex-spouse account. Any one of those can trigger the hold; together they almost guarantee it.

The fix isn't to call and plead — it's to make each flag verifiable. Confirm the W-2 the IRS has on file matches yours, confirm the estimated payments posted to your account, and confirm you (not your ex) are entitled to claim the kids under the divorce decree and IRS residency rules. If both parents claimed the same children, that's a separate fight with its own process — see both parents claimed child IRS.

What happens next: the CP05 review sequence

A CP05 review ends one of three ways: the refund is released in full, the IRS asks you for documents, or the IRS changes the refund. The sequence is automated and moves in stages:

- CP05 arrives. Your refund is held. On your account transcript this usually shows as code 570 on IRS transcript (the hold) paired with code 971 IRS transcript (the notice going out).

- The review window runs — typically 60 days. Most returns clear here with no contact at all: the hold reverses (code 571) and code 846 posts with your deposit date.

- If the IRS can't verify something, a CP05A notice arrives demanding documents — pay stubs, W-2s, proof of withholding or credits — by a printed deadline, typically about 30 days out. This is the stage where inaction starts costing money.

- If you don't respond to the CP05A, the IRS resolves the question against you: withholding it can't verify is removed, credits it can't verify are disallowed, and the refund is reduced or eliminated by an adjustment notice.

- If credits are the issue, the review can escalate to a CP75 notice — a correspondence audit of your EITC or dependent claims, with formal document demands.

One 2026 reality check: the IRS workforce shrank roughly 27% in 2025, and manual-review queues are where that shows. Reviews that once wrapped in a few weeks now routinely use the whole window — and some run past it with only a "we need more time" letter to show for it.

| Stage | What you see | Your move |

|---|---|---|

| Day 0 | CP05 arrives; transcript shows 570/971 | Verify the notice, calendar the window's end date, check your numbers |

| During the window (typically 60 days) | Silence, or transcript movement | Nothing required — watch the transcript weekly, don't amend |

| Review clears | Code 571, then 846 with a deposit date | Confirm the amount matches your return |

| IRS needs proof | CP05A with a printed deadline (typically ~30 days) | Send every requested document by the deadline — this is now mandatory |

| Window passes, nothing happens | No refund, maybe a Letter 2645C asking for more time | Call the notice number; TAS via Form 911 if the delay causes hardship |

| IRS can't verify | Adjustment notice or CP75 exam letter | Respond with documentation — this is where refunds get lost |

Refund held past the review window — or a CP05A demanding records the divorce scattered?

Send us a photo of your notice. An experienced tax professional will read your transcript, pinpoint what's actually holding the refund, and map the fastest legitimate path to release — free and confidential. Interest and delays only grow while the file sits.

Your options while the IRS holds your refund

You can't force a CP05 review to finish, but you can make sure it finishes in your favor — and know exactly which letter you're actually dealing with, because the IRS sends several refund-hold letters that look alike but demand very different responses:

| Letter | What it means | Action required |

|---|---|---|

| CP05 | Refund held while income, withholding, and credits are verified | None — wait, verify your numbers, calendar the window |

| CP05A | Review found something it can't verify | Yes — send documents by the printed deadline |

| 4464C letter | A parallel pre-refund review from a different IRS unit | None initially — same wait-and-verify posture as a CP05 |

| 5071C letter | The IRS doubts you filed the return — identity check | Yes — verify your identity online or by phone before anything moves |

| CP12 notice | The IRS already changed your refund amount for a math error | Only if you disagree — you typically have 60 days to contest |

While the window runs, four moves are worth your time:

- Pull your wage and income transcript. The IRS wage and income transcript shows every W-2 and 1099 payers filed under your SSN. If it matches your return, your review will almost certainly clear; if it doesn't, you've found the trigger before the IRS asks.

- Confirm where joint estimated payments posted. Your IRS online account shows payments credited to you. If the $16,000 you claimed sits under your ex-spouse's account, that's fixable — but it takes a call or correspondence, and it's the single most common divorce-year hang-up we see on these reviews.

- Watch the transcript, not the mailbox. Codes move days before letters arrive. Our guides to code 570 on IRS transcript and code 846 decode what each line means.

- Use hardship channels if you genuinely need the money. If the held refund is the difference between paying rent and not, the Taxpayer Advocate Service exists for exactly this — see how to contact the Taxpayer Advocate Service.

One thing not to do: don't file an amended return to "hurry things along." A 1040-X filed mid-review doesn't release the hold — it adds a second, slower process on top of the first.

| Code | Meaning | Good or bad sign? |

|---|---|---|

| 570 | Refund hold in place | Neutral — this is the CP05 itself |

| 971 | A notice was issued | Neutral — could be the CP05, a CP05A, or a 2645C |

| 571 / 572 | Hold reversed or resolved | Good — the review cleared |

| 846 | Refund issued, with a date | Good — money is moving |

| 420 | Return routed to examination | Bad — the review became an audit; get help |

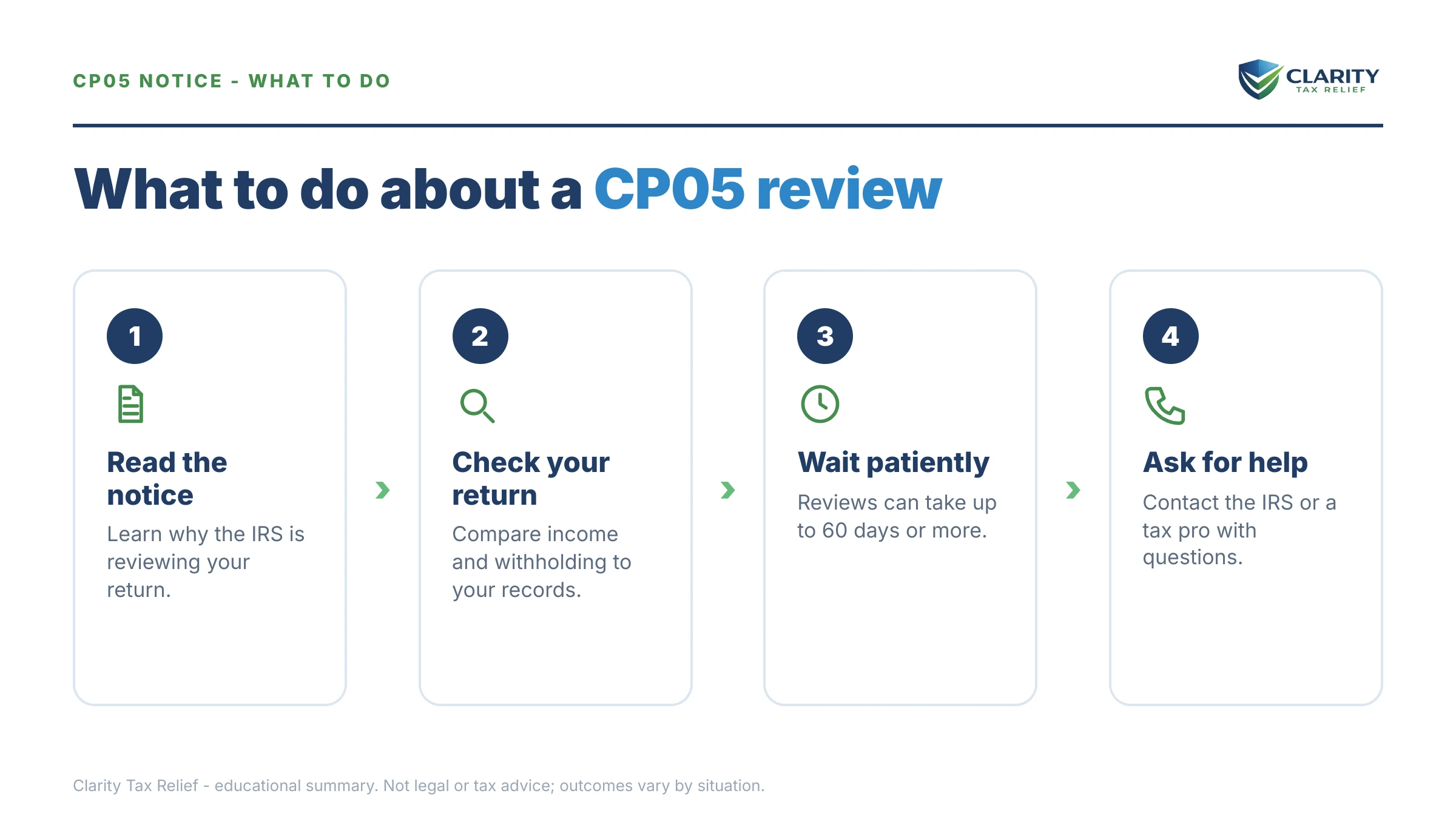

How to respond to a CP05 notice, step by step

- Read the notice and calendar the review window. Find the tax year and the review-window date on your CP05, and mark that date — it's the day you're allowed to start escalating.

- Verify the notice in your IRS online account. Log in at IRS.gov and confirm the notice appears in your account — a real CP05 asks for no payment and no personal information, so anything demanding either is a scam.

- Pull your transcripts and compare. Get your wage and income transcript and check every W-2 and 1099 the IRS has on file against what you reported — a mismatch here is almost always what triggered the hold.

- Fix real mismatches carefully. If an employer misreported your wages or withholding, ask for a corrected W-2c; if you find an error in what you filed, talk to an experienced tax professional before amending mid-review, because a 1040-X filed during a hold can reset the clock.

- Escalate when the window closes. If the review date passes with no refund and no letter, call the number on the notice for a specific status — and if the delay is causing financial hardship, file Form 911 with the Taxpayer Advocate Service.

When you can handle a CP05 yourself

Most CP05s need no professional help at all — and it would be dishonest to tell you otherwise. Handle it yourself when the first CP05 just arrived, your wage and income transcript matches your return, and you can afford to wait out the window. In that scenario the review clears on its own more often than not, and the correct action is patience plus a calendar entry.

Experienced help changes the outcome in a narrower set of situations:

- A CP05A arrived and the records are scattered. Divorce-year documentation — joint estimated-payment records, custody and residency proof for dependent claims, a W-2 from an employer that no longer exists — often lives in two households. A professional knows exactly which documents satisfy each verification item, and a weak response can cost the whole refund.

- Estimated payments are credited to the wrong spouse. Reallocating joint payments between divorced spouses is a correspondence-and-phone fight most people lose to hold music.

- The review became a CP75 exam or code 420 posted. Once it's an audit of your EITC or dependents, response strategy matters and mistakes compound.

- The window passed long ago and calls go nowhere. A representative with a power of attorney can work the practitioner channels and TAS routes you can't reach from the general line.

Terms on your CP05, decoded

- Integrity and Verification Operations (IVO): the IRS unit that screens refunds before payment — the "we're reviewing your return" on your notice is them.

- Refund hold (code 570): the transcript entry that freezes your refund while the review runs; it isn't a penalty and doesn't create a debt.

- Wage and income transcript: the IRS's copy of every W-2 and 1099 filed under your SSN — the yardstick your return is being measured against.

- CP05A: the follow-up letter that converts your wait into a task — documents due by a printed deadline.

- Taxpayer Advocate Service (TAS): an independent office inside the IRS that can force movement on a stalled refund when the delay causes financial hardship, requested via Form 911.

- Refund interest: interest the IRS adds automatically when it pays your refund more than 45 days after the filing deadline or your filing date, whichever is later — it's taxable income the year you receive it.

CP05 notice FAQs

How long does a CP05 review take?

The CP05 typically tells you the IRS expects to finish within 60 days of the notice date — many reviews resolve sooner, and some stretch longer. With IRS staffing down roughly 27% since 2025, longer waits are more common. If your window passes with no refund and no follow-up letter, call the number on the notice, and if the delay is causing financial hardship, the Taxpayer Advocate Service can step in.

Is a CP05 notice an audit?

No. A CP05 is a pre-refund verification hold, not an examination — the IRS is matching your reported income, withholding, and credits against what employers and payers reported. You have nothing to prove at this stage. A small share of reviews do escalate: if credits like the EITC can't be verified, the IRS may open a CP75 audit, which is a different letter with document demands.

Do I need to respond to a CP05?

No — the first CP05 asks for nothing, and there is no address or deadline for you on it. Your job is to verify the notice is real, confirm your own numbers match employer-reported records, and calendar the review-window date. Action is only required if a CP05A arrives asking for documents; that letter has a printed response deadline, and missing it can cost you the refund.

Can I speed up a CP05 review?

Mostly no — calling before the review window ends rarely moves your file, because the hold sits with an automated verification unit. What you can do: pull your wage and income transcript and confirm every W-2 and 1099 matches your return, so any follow-up request is answered same-day. If the held refund is causing genuine hardship — an eviction notice, utility shutoff, or medical need — the Taxpayer Advocate Service can expedite via Form 911.

What if 60 days pass and I still don't have my refund?

Call the number printed on your CP05 and ask for the specific status of the review — not just "it's processing." Check your account transcript first: code 571 or 846 means it resolved; a new 971 may mean another letter (often a 2645C "we need more time" letter) is coming. If calls go nowhere and the delay is creating hardship, file Form 911 with the Taxpayer Advocate Service.

Will the IRS pay me interest on the held refund?

Generally yes, if the refund is issued more than 45 days after the later of the filing deadline or the date you actually filed. Interest accrues at the IRS's quarterly rate and is added automatically to the refund — you don't request it. One catch: that interest is taxable income, so a long hold on a large refund can add a line to next year's return.

Why did I get a CP05 after my divorce?

Divorce-year returns hit several verification triggers at once: your filing status changed from married filing jointly, dependents appear on your return alone for the first time, your withholding pattern shifted mid-year, and any estimated payments made jointly may be credited differently than you claimed them. None of these means you did anything wrong — they mean your return looks different from last year's, and the system checks before paying.

What's the difference between a CP05 and a CP05A?

A CP05 says the IRS is reviewing your refund and needs nothing from you. A CP05A says the review found something it can't verify and demands documents — pay stubs, W-2s, proof of withholding or credits — by a deadline printed on the letter, typically about 30 days out. Ignoring a CP05 costs you nothing; ignoring a CP05A can end with your refund reduced or disallowed.

Your next 24 hours

- Find the review-window date on your CP05 — it's stated near the top with the tax year — and put it on your calendar as "call the IRS if no refund by today."

- Gather your proof now, not when a CP05A demands it: a copy of the return, every W-2 and 1099, records of estimated payments (and who made them), and — if you claimed the kids — the divorce decree and school or medical records showing they live with you.

- Get a free case review if your window has already passed, a CP05A is sitting on your counter, or joint payments from the marriage are tangled in the hold. Call (888) 825-7779 or use the 2-minute form — the review itself keeps running while you wait, so find out where your file actually stands.

Primary sources: the IRS's own page at Understanding your CP05 notice, your balance and payment history in your IRS online account, and hardship help through the Taxpayer Advocate Service.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.