International & Offshore

Didn't File an FBAR? Penalty Amounts and How to Fix It (2026)

The short answer: if you didn't file an FBAR, the penalty depends on willfulness. Non-willful failures carry a statutory $10,000 per year, inflation-adjusted above $16,000 today; willful failures risk 50% of the account balance per year. But if you come forward first, official catch-up procedures often cut that to 5% — or to zero.

You're gathering documents for a refinance — returns, bank statements, asset lists — and the account overseas suddenly becomes a question you can't answer: it's never been reported on anything. Take a breath. Millions of people miss this form because no one tells them it exists, and the government built specific, protected paths for exactly your situation.

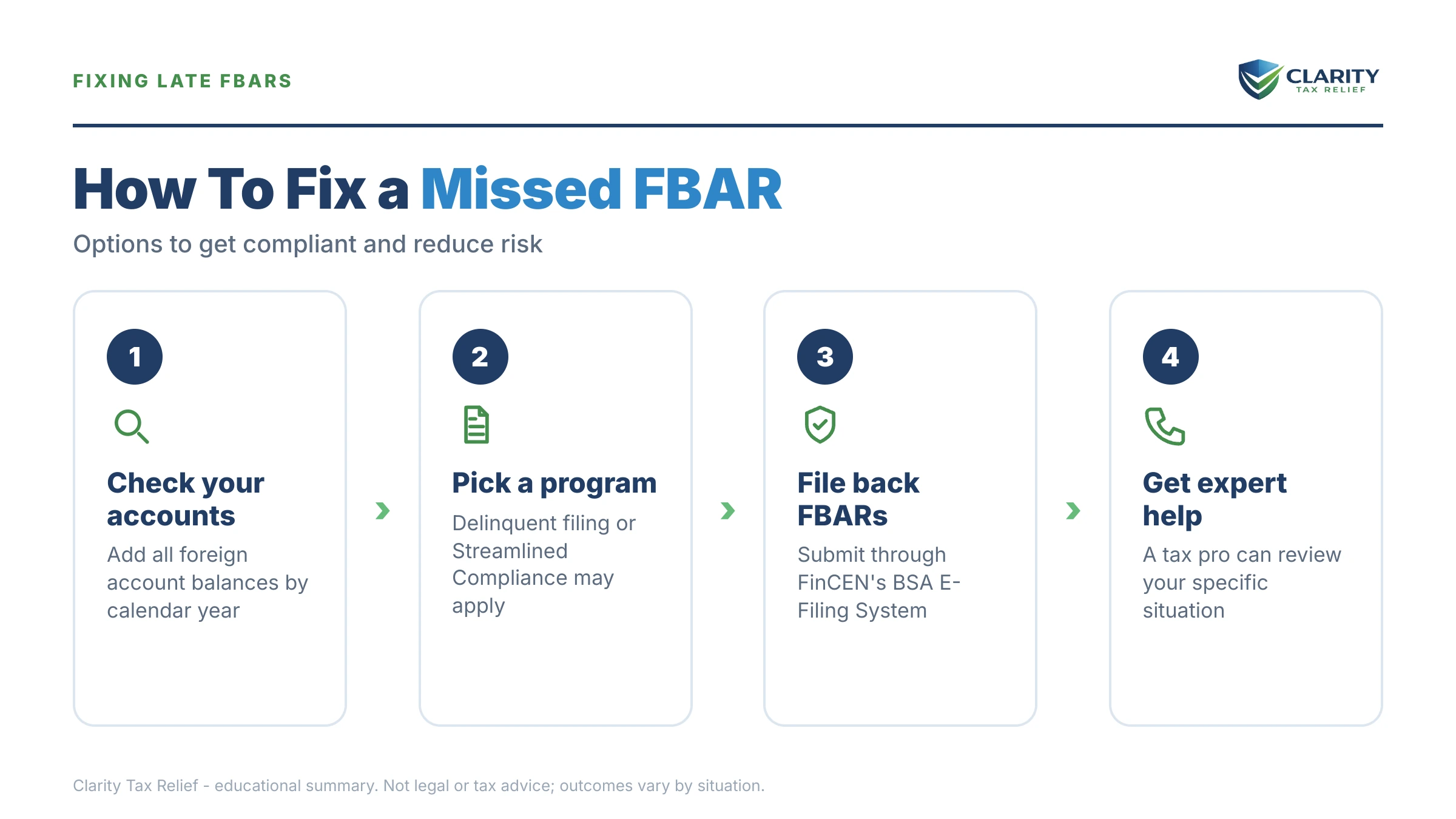

The form you didn't file is FinCEN Form 114 — it goes to the Treasury's Financial Crimes Enforcement Network, not the IRS, and it's separate from your tax return. The visual guide below maps the deadlines and options, so you can see how manageable the catch-up process is.

⏱ Your real clock: there is no printed deadline once an FBAR is late — but there is a closing window. The streamlined catch-up path is only available before the IRS contacts you or opens an exam. Foreign banks already report your account data under FATCA, and the government has six years per unfiled report to assess penalties.

Who has to file an FBAR — and why you're on the hook

You must file an FBAR (FinCEN Form 114) if the combined value of your foreign financial accounts exceeded $10,000 at any point during the calendar year. It's an aggregate test across every account — bank, brokerage, many foreign pensions — and it counts accounts you only have signature authority over, like a parent's account you help manage.

Two details trip people up. First, $10,000 is the combined peak: four small accounts holding $3,000 each put you over, even if no single account ever did. Second, crossing the line for one day triggers the requirement for the whole year.

The FBAR is due April 15 with an automatic extension to October 15 — no request needed. It's filed electronically through FinCEN's BSA E-Filing System, not attached to your 1040. That separateness is exactly why so many otherwise-compliant filers miss it: your tax software's foreign-account question is easy to click past, and the form never shows up in the return you sign.

Married couples get one wrinkle: a spouse can be covered by a joint FBAR only when all of their accounts are jointly owned and the filing spouse reports them all. If either of you has any separately owned foreign account, you each need your own FBAR for that year.

How much is the penalty if you didn't file an FBAR?

The non-willful FBAR penalty is a statutory $10,000 per unfiled report, inflation-adjusted annually to more than $16,000 per year today. Thanks to the Supreme Court's 2023 decision in Bittner v. United States, that penalty applies per report — per year — not per account, which ended the IRS's practice of multiplying it across every account you held.

Willful failures are a different universe: the greater of roughly $160,000 (inflation-adjusted from a statutory $100,000) or 50% of the account balance at the time of the violation — again, per year. "Willful" doesn't require intent to cheat; courts have found willfulness in reckless disregard, like signing returns that ask about foreign accounts and never checking. Our guide to willful vs. non-willful FBAR penalties breaks down where that line actually sits.

Three more facts frame your exposure:

- Six-year assessment window. The government has six years from each FBAR's due date to assess a penalty for that year. Older unfiled years generally age out of civil penalty reach.

- Reasonable cause can eliminate the penalty for non-willful failures where the income was reported and there's a credible explanation.

- It's not a tax penalty. FBAR penalties arise under Title 31 (the Bank Secrecy Act). They don't follow the normal IRS collection track — no CP14, no federal tax lien — and standard tax-penalty relief like first-time abatement doesn't apply. Collection of an assessed FBAR penalty runs through federal payment offsets and, ultimately, a government lawsuit.

| Violation level | Penalty amount | When it applies |

|---|---|---|

| Non-willful | $10,000 statutory per year, inflation-adjusted to $16,000+ (per report, not per account) | You didn't know or misunderstood the requirement; no concealment |

| Non-willful with reasonable cause | $0 possible | Income was reported and paid; credible explanation for the missed filings |

| Willful (civil) | Greater of ~$160,000 (inflation-adjusted) or 50% of the account balance, per year | Knowing violation or reckless disregard — including ignoring the Schedule B foreign-account question |

| Willful (criminal) | Fines up to $250,000 and up to 5 years in prison | Rare; deliberate concealment — nominee names, structured transfers, hidden ownership |

What happens if you keep not filing

Unfiled FBARs don't get discovered by luck — they get discovered by data matching, and the sequence runs in a predictable order. Each stage you wait through removes a cheaper option from the table:

- Your bank reports you. Under FATCA, financial institutions in more than 100 countries send U.S. account holders' names, account numbers, and balances directly to the IRS. If your account is at a bank of any size, assume this has already happened.

- The IRS matches and sends a soft letter. Foreign-account compliance letters like Letter 6291 tell you the IRS sees a mismatch between the bank's data and your filings. This is the warning shot — and the signal that your quiet window is closing.

- An examination opens. Once the IRS starts a civil exam of any covered year, the streamlined procedures are off the table. An examiner now decides willfulness and penalty amounts, year by year, within the six-year window — with your explanation carrying far less weight than it would have as a voluntary filing.

- Assessment and collection. Assessed FBAR penalties can be collected through offsets against federal payments and, for larger amounts, a Department of Justice lawsuit that converts the penalty into a court judgment. Willful fact patterns can also be referred for criminal review.

One 2026 reality worth knowing: IRS staffing fell sharply in 2025, but FATCA data matching and letter generation are automated. The comparison runs whether or not a human ever looks at your file — and international non-compliance remains one of the areas the smaller IRS has said it will keep prioritizing.

Sitting on unfiled FBARs right now?

These catch-up paths only work if you move before the IRS contacts you about the accounts. Get a free, confidential review of which path fits your facts — before a Letter 6291 decides it for you. Call (888) 825-7779 or use the 2-minute form.

Your options to fix unfiled FBARs

Which catch-up path fits depends on two questions: did you report the accounts' income on your tax returns, and was the failure non-willful? General penalty mechanics for ordinary tax debt are covered in our guide to how much IRS penalties on back taxes really cost — but FBAR fixes run through these dedicated paths instead:

| Path | Who qualifies | What it costs | What's involved |

|---|---|---|---|

| Late FBAR filing with explanation (the former Delinquent FBAR Submission Procedures were removed by the IRS on June 30, 2026) | You reported and paid tax on the account income; the IRS hasn't contacted you | Penalties are not automatic when the income was reported and taxed — but there is no longer a guaranteed penalty-free program | E-file the late FBARs through FinCEN with a short explanation statement; typically done in days |

| Streamlined Domestic Offshore Procedures (SDOP) | U.S. residents; non-willful failure; unreported foreign income; no exam open | 5% miscellaneous offshore penalty on the highest aggregate year-end balance, plus tax and interest on amended returns | 3 years of amended returns + 6 years of FBARs + Form 14654 non-willful certification |

| Streamlined Foreign Offshore Procedures (SFOP) | Non-willful filers who meet the non-residency test (broadly, you lived abroad in one of the last three years) | 0% offshore penalty; tax and interest on the returns only | 3 years of returns + 6 years of FBARs + Form 14653 certification |

| IRS Voluntary Disclosure Practice | Willful conduct or potential criminal exposure | Substantial — typically one willful FBAR penalty on the highest-balance year, plus tax, interest, and a fraud penalty | Formal preclearance through IRS Criminal Investigation; attorney-driven |

| Quiet disclosure (just filing late) | No one — the IRS screens for it | Risks full non-willful or willful penalties with no protection | See why quiet disclosure backfires |

One companion item: if your foreign assets were large enough, you may also owe Form 8938 (FATCA reporting) with your tax return — a separate form with its own $10,000 penalty. The streamlined packages fold missed 8938s into the same fix, which is one more reason a coordinated filing beats piecemeal patching.

A worked example: three unfiled years, $36,900 year-end balance

Say you're a homeowner heading into a refinance with an inherited account abroad whose highest year-end (December 31) aggregate balance across the last six years was $36,900, earning about $500 a year in interest you never put on your returns. Here's the honest math, clearly hypothetical:

- Worst case (wait for the exam): three non-willful penalties at today's inflation-adjusted level — 3 × $16,000+ ≈ $48,000 or more. That's more than the account holds, and it assumes the examiner doesn't find willfulness.

- SDOP (come forward first): the 5% miscellaneous offshore penalty applies to the highest aggregate year-end balance of your foreign financial assets across the six-year covered FBAR period (and three-year return period) — here the highest December 31 aggregate, $36,900, yields $1,845. Add three amended returns picking up $500/year of interest — roughly $110 in tax per year at a 22% rate, about $330 total, plus modest interest and a small late-payment charge. All-in, call it under $2,300 — about 5% of the do-nothing number. (The tax-side add-ons work like ordinary failure-to-file and failure-to-pay penalties; you can estimate them with our IRS penalty & interest calculator.)

- Late filing (if the income WAS reported): if that $500 of interest actually appeared on your Schedule B each year, penalties are not automatic — e-file the six back FBARs through FinCEN with an explanation. Note that the IRS removed the Delinquent FBAR Submission Procedures on June 30, 2026, so there is no longer a guaranteed penalty-free program.

For the refinance itself: unfiled FBARs don't appear on credit reports and create no lien. The clean streamlined or late filing — done before underwriting asks questions — keeps it that way.

How to respond, step by step

- Confirm you were required to file. Add up the highest balance of every foreign account for each year. If the combined total ever topped $10,000 in a year, that year needed an FBAR.

- Pull six years of foreign account statements. You'll need each account's highest balance for each year to complete the late FBARs and to size your real penalty exposure.

- Check your filed tax returns. Did you report the accounts' interest and income? The answer decides whether a straightforward late FBAR filing or the streamlined path fits your case.

- Assess willfulness honestly. The streamlined certification is signed under penalty of perjury. If there are bad facts — hidden ownership, moved money — get advice before you certify anything.

- File through the right procedure. E-file the late FBARs on FinCEN's system with an explanation statement, or submit the full streamlined package: returns, six years of FBARs, and the certification form.

- Stay current going forward. File this year's FBAR by the automatic October 15 extension, answer the foreign-account question on Schedule B, and keep the account income on your return.

When you can handle this yourself

If you reported every dollar of the foreign accounts' income on your returns and simply never knew Form 114 existed, filing the late FBARs yourself through FinCEN is genuinely DIY-able. The e-filing takes an evening, the explanation statement is short, and penalties are not automatic when the income was reported and taxed — though since the IRS removed the Delinquent FBAR Submission Procedures on June 30, 2026, there is no longer a guaranteed penalty-free program.

Experienced help changes the outcome in four situations: the income was not reported (so you're choosing between streamlined paths and signing a perjury-backed certification), the facts have willful shading (foreign entities, moved funds, ignored advice), the balances are large enough that a 50% willful penalty is a life-changing number, or the IRS has already sent a foreign-account letter — which narrows your options and raises the stakes of every response. In those cases, the choice of procedure is the outcome, and it can't be un-chosen later.

Terms on your FBAR paperwork, decoded

- FinCEN Form 114: the FBAR itself — an information report of foreign accounts filed with the Treasury's Financial Crimes Enforcement Network, separate from your tax return.

- Willful blindness: deliberately avoiding knowledge of the requirement — courts treat it as willfulness, which is why "I never read Schedule B" is a dangerous defense.

- FATCA / Form 8938: a separate foreign-asset report filed with your tax return at higher thresholds; FATCA is also the law that makes foreign banks report you to the IRS.

- Miscellaneous offshore penalty: the single 5% penalty that replaces all FBAR and information-return penalties inside the streamlined domestic program.

- Forms 14653 / 14654: the streamlined certification forms (foreign and domestic) where you swear, under penalty of perjury, that your failure was non-willful and explain why.

- Reasonable cause: a fact-based excuse — reliance on a professional, genuine ignorance despite ordinary care — that can eliminate a non-willful penalty entirely.

Didn't-file FBAR penalty questions, answered

What is the penalty for not filing an FBAR?

The civil penalty for a non-willful failure starts at a statutory $10,000 per year, inflation-adjusted to more than $16,000 today. Willful failures face the greater of roughly $160,000 (inflation-adjusted from $100,000) or 50% of the account balance, per year. Most people who come forward before the IRS contacts them pay far less — often nothing — through the late-filing or streamlined procedures.

Can I go to jail for not filing an FBAR?

Jail is possible only for willful violations, and criminal prosecution is rare — it's reserved for cases involving deliberate concealment, like nominee names or moving money to dodge reporting. A willful criminal violation can carry fines up to $250,000 and up to five years in prison. If you simply didn't know the form existed, your exposure is civil, not criminal, and the compliance procedures exist precisely for you.

Can I just file my old FBARs late without telling anyone?

You can e-file late FBARs any time through FinCEN with a short explanation, and penalties are not automatic when the account income was reported and taxed. But the IRS removed the Delinquent FBAR Submission Procedures on June 30, 2026, so there is no longer a guaranteed penalty-free program. Filing cold while quietly amending returns is called a quiet disclosure, and the IRS screens for it — if the income wasn't reported, use the streamlined program instead; it exists to give you a protected path.

How far back do FBAR penalties go?

The government has six years from each FBAR's due date to assess a penalty for that year, so your realistic exposure window is the last six years of unfiled reports. That's also why the streamlined procedures require exactly six years of back FBARs. Older years generally fall out of reach for penalty assessment, though willful cases with criminal angles are evaluated differently.

Does the IRS actually know about my foreign account?

Very likely, yes. Under FATCA, foreign banks in more than 100 countries report U.S. account holders' names, account numbers, and balances directly to the IRS, and the IRS matches that data against filed returns and FBARs. That matching is what generates soft letters like Letter 6291. The safe assumption in 2026 is that your account is already in the IRS's data — the only question is when it gets worked.

Does first-time abatement or the new AEP apply to FBAR penalties?

No. FBAR penalties are assessed under Title 31 (the Bank Secrecy Act), not the tax code, so first-time abatement and the new Automatic Exemption from Penalty (AEP) rolling out in summer 2026 don't reach them. Relief comes instead through reasonable cause, late-filed FBARs with an explanation, or the streamlined program's reduced penalty terms.

Will unfiled FBARs stop my mortgage refinance?

Not directly — an unfiled FBAR doesn't appear on your credit report, and no lien exists until a penalty is assessed and reduced to judgment. The real refinance risk is downstream: amended returns that create a tax balance, or an assessed penalty the government sues to collect. Cleaning up the filings before underwriting, on your terms, is far cheaper than explaining a federal judgment later.

What counts toward the $10,000 FBAR threshold?

Every foreign financial account you own or control, added together, at each account's highest point in the year: bank accounts, brokerage accounts, many foreign pension accounts, and accounts you merely have signature authority over. It's an aggregate test — four accounts holding $3,000 each put you over. And crossing $10,000 for even one day of the year triggers the filing requirement for that whole year.

Your next 24 hours

- Find your peak balances. Log into each foreign account (or email the bank) and pull the highest balance for each of the last six years — that single list determines your threshold, your exposure, and your best path.

- Gather your filings. Pull your last three tax returns and check Schedule B: was the foreign-account box answered, and was the account's income reported? That answer separates the simple late-filing fix from the 5% fix.

- Get the path chosen before the IRS chooses for you. The streamlined door closes the moment the IRS contacts you about the accounts. A free, confidential case review — the form at claritytaxrelief.com/#consult or (888) 825-7779 — tells you which path fits your facts while your options are still open.

Primary sources: the IRS's official FBAR overview page, its Streamlined Filing Compliance Procedures, and the Financial Crimes Enforcement Network (FinCEN), which operates the BSA E-Filing System where FBARs are submitted.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.