IRS Letters & Payroll Tax

Letter 3164: The IRS TFRP Investigation Contact Letter, Explained (2025)

The short answer: Letter 3164 means the IRS has opened a Trust Fund Recovery Penalty (TFRP) investigation and may contact third parties — your bank, employees, bookkeeper, or accountant — to decide who was personally responsible for a business's unpaid payroll taxes. It's not a bill yet, but it's a serious early warning.

Got Letter 3164 with your name on it?

Send us a photo of the letter. An experienced tax professional will explain exactly where you stand in the TFRP process, what the revenue officer is looking for, and how to protect yourself — free, confidential, no pressure.

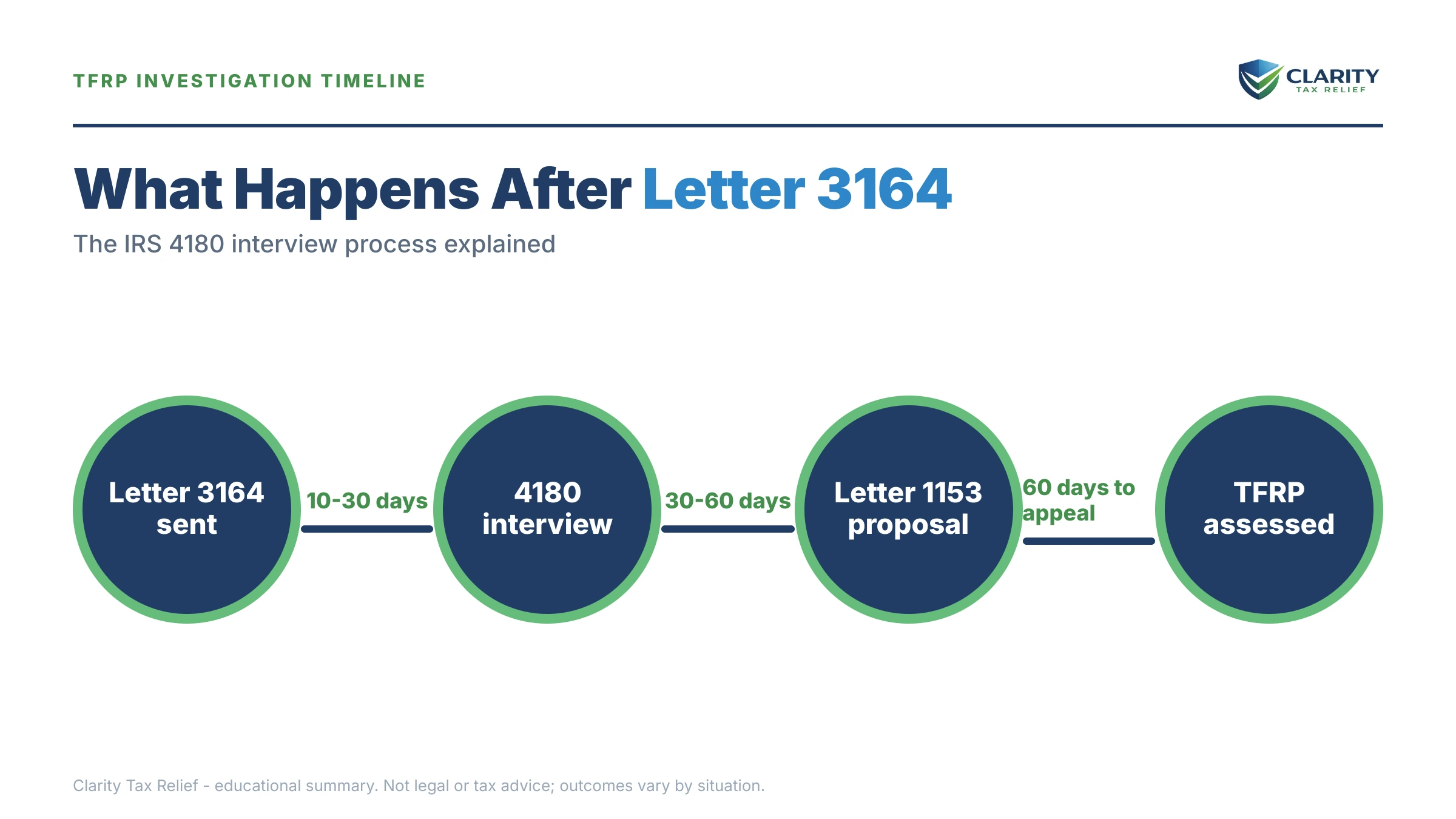

⏱ Why timing matters: Letter 3164 itself has no single "pay by" date, but it starts a clock. After the revenue officer interviews you (Form 4180), the IRS issues Letter 1153 proposing the penalty — and that letter carries a strict 60-day deadline to appeal. The choices you make now, before that interview, shape everything that follows.

Why you got Letter 3164

Somewhere behind this letter is a business that fell behind on payroll taxes. When an employer withholds income tax and the employees' share of Social Security and Medicare from paychecks, that money is held "in trust" for the government. If the business doesn't pay it over, the IRS can come after the people who were responsible — personally.

Letter 3164 is how a revenue officer tells you they may reach out to other people while building that case. Under the law (Internal Revenue Code section 7602(c)), the IRS has to give advance notice before contacting third parties about your tax matter. This letter is that notice. The IRS explains the penalty itself on its Trust Fund Recovery Penalty page.

So getting Letter 3164 usually means two things at once: the IRS is looking at unpaid payroll taxes, and your name is on the list of people it wants to investigate as a "responsible person."

What happens if you ignore it

The TFRP process moves in stages. Each one narrows your options and raises the stakes. Ignoring Letter 3164 doesn't slow it down — it just means the case gets built without your side of the story:

- Letter 3164 — third-party contact notice. The investigation has started. No assessment yet. You are here.

- Form 4180 interview — the revenue officer questions you (and others) to decide if you were "responsible" and acted "willfully." Your answers become evidence.

- Letter 1153 & Form 2751 — the IRS formally proposes the penalty against you and gives you 60 days to agree or appeal.

- Assessment — if you don't respond, the penalty becomes your personal debt. Standard collection follows: federal tax liens, bank levies, and wage garnishments — against you, individually, not just the business.

The hard part of the Trust Fund Recovery Penalty is that it survives almost everything. The business can close, file bankruptcy, or disappear — and the IRS can still collect the trust fund piece from the people it names. That's why the early stage you're in right now is the best time to act.

Who the IRS can hold responsible

The TFRP can apply to more than just the owner. The IRS looks for anyone who had the duty to collect or pay over the taxes and willfully failed to do it. That can include:

- Owners, officers, partners, and members of an LLC

- Bookkeepers and payroll managers who decided which bills got paid

- People with check-signing authority or control over the bank account

- Sometimes outside accountants or family members, if they made the financial calls

"Willful" doesn't mean evil intent. It usually means you knew the taxes were due and chose to pay other bills — rent, suppliers, payroll — first. More than one person can be held liable for the same debt, and the IRS often pursues several people at once. Our deeper guide on the Trust Fund Recovery Penalty and who is personally liable walks through both tests in plain English.

How much is at stake

The TFRP equals 100% of the trust fund portion of the unpaid payroll taxes. Here's a simple worked example:

- A business owes $80,000 in unpaid Form 941 payroll taxes for several quarters.

- Of that, roughly $50,000 is the trust fund portion — income tax withheld plus the employees' half of Social Security and Medicare.

- The remaining ~$30,000 (the employer's matching share, plus penalties and interest) stays with the business.

- The IRS can assess that $50,000 personally against each responsible person it identifies.

The penalty does not include the employer's share or business-level penalties — but $50,000 following you home is still life-changing. If the underlying business debt is itself a problem, our guide to 941 back taxes when a business falls behind on payroll taxes explains how the business and personal sides connect.

Your options after Letter 3164

You have more control at this stage than later. Depending on your situation, you may be able to:

- Show you weren't a responsible person. If you had no real authority over the money — no check signing, no decisions about which bills got paid — that's a defense worth documenting now.

- Show you didn't act willfully. If you genuinely didn't know about the unpaid taxes, or were misled, that matters.

- Challenge the numbers. The trust fund figure the revenue officer is working from isn't always right.

- Resolve the underlying balance. If the business can pay or set up an agreement, that can shrink or end the personal exposure.

- Prepare for the interview. The Form 4180 questions are predictable. Knowing how your answers will be read is half the battle.

One thing to be clear-eyed about: nobody can promise the penalty goes away. Anyone guaranteeing they'll make a TFRP disappear before reviewing the facts is selling you something. The honest goal is to put the strongest, best-documented version of your case in front of the IRS before it's locked in.

How to respond to Letter 3164, step by step

- Don't panic, and don't ignore it. This is the investigation stage — you still have options and rights. But the clock is running.

- Read it carefully. Note the revenue officer's name, the tax periods involved, and any response date or interview request.

- Gather your records. Pull bank signature cards, payroll records, corporate minutes, and anything showing who actually controlled the money during the unpaid quarters.

- Decide on representation before the interview. The Form 4180 interview is the heart of the case. You can authorize an experienced tax professional to handle it using Form 2848 power of attorney, so you're not answering on the spot.

- Verify it's really the IRS. A real revenue officer carries two forms of ID (a pocket commission and an HSPD-12 card). Payments never go to gift cards or wire transfers — only to the U.S. Treasury. The IRS describes the rules on its third-party contact page.

- Watch for Letter 1153. If the penalty is proposed, you generally have just 60 days to appeal. Our guide to Letter 1153 and the 60-day deadline covers exactly how to protest.

Letter 3164 questions, answered

What does IRS Letter 3164 mean?

Letter 3164 is a notice that the IRS may contact third parties — like your bank, employees, bookkeeper, or accountant — as part of a Trust Fund Recovery Penalty investigation. It means a revenue officer is trying to decide who was personally responsible for a business's unpaid payroll taxes. It is not a bill yet, but it is a serious signal.

Does Letter 3164 mean I have to pay the trust fund penalty?

No. Letter 3164 is the investigation stage, not the assessment. The penalty is only proposed later, in Letter 1153 with Form 2751, after the revenue officer interviews you and decides whether you were responsible and acted willfully. You have appeal rights before any amount becomes your personal debt.

Who can the IRS hold responsible for the trust fund recovery penalty?

Anyone who had the duty to collect or pay over payroll taxes and willfully failed to do so. That can include owners, officers, partners, bookkeepers, payroll managers, and sometimes people who signed checks or decided which bills got paid. More than one person can be held liable for the same debt.

Should I talk to the revenue officer myself?

You can, but the Form 4180 interview is designed to establish your responsibility and willfulness, and your answers are used to assess the penalty against you. Many people choose to have an experienced tax professional review the situation and represent them first, because what you say early shapes everything that follows.

How much is the trust fund recovery penalty?

The penalty equals 100% of the trust fund portion of the unpaid payroll taxes — the income tax withheld plus the employees' share of Social Security and Medicare. It does not include the employer's share or business-level penalties, but it becomes your personal liability and follows you individually.

Can the trust fund recovery penalty be appealed?

Yes. After Letter 1153 proposes the penalty, you generally have 60 days to file a written protest with IRS Appeals. You can argue you were not a responsible person, did not act willfully, or that the numbers are wrong. Acting before that deadline is critical — missing it lets the IRS assess the penalty.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.