IRS Forms

Form 982 Insolvency Exclusion: How to Avoid Tax on a 1099-C (2026)

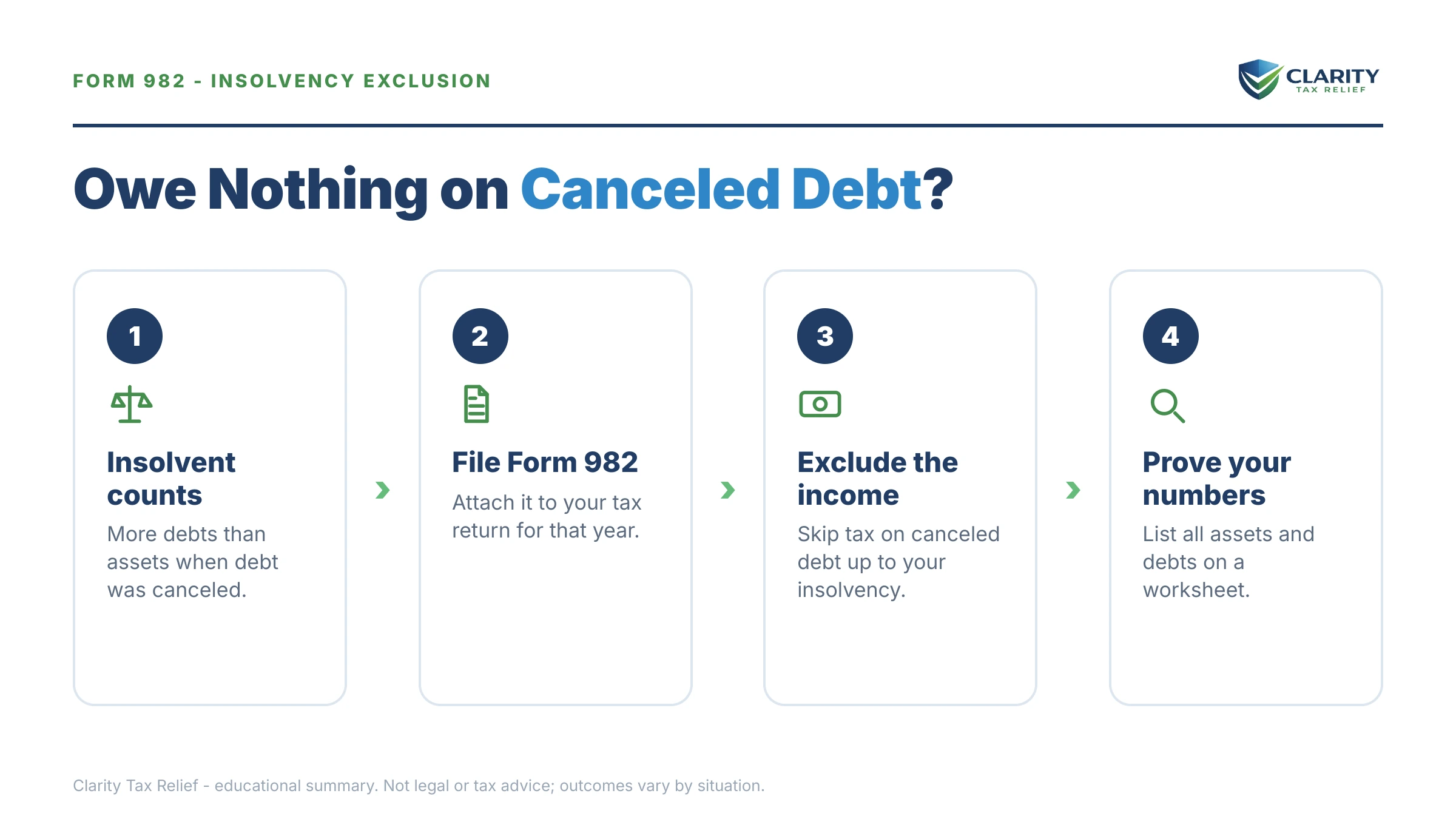

The short answer: the Form 982 insolvency exclusion lets you exclude cancelled-debt income from a 1099-C to the extent your total debts exceeded your total assets immediately before the debt was cancelled. Check box 1b, enter the excluded amount on line 2, and attach the form to your return for the cancellation year.

You settled a debt — or a creditor simply gave up on it — and months later a 1099-C arrived saying the forgiven balance is now taxable income. It feels like being billed for drowning. But Congress built an exit for exactly this situation: if you were broke on paper when the debt was cancelled, you may not owe tax on it at all.

The entire claim comes down to three entries on a one-page form plus a worksheet you keep in your records. The image below shows exactly what Form 982 looks like and where the insolvency exclusion lives on it, so you can see how little of the form actually applies to you.

⏱ Your deadline: Form 982 must be attached to your federal return for the year shown in box 1 of the 1099-C — typically due April 15 of the following year. Already filed without it? You generally have 3 years from the date you filed to claim the exclusion on Form 1040-X and recover tax you overpaid.

Why a cancelled debt counts as income in the first place

When a creditor cancels $600 or more of your debt, tax law treats the forgiven amount as income to you — money you borrowed, spent, and never repaid. The creditor reports it to the IRS on Form 1099-C, and the same copy that reaches your mailbox reaches the IRS matching computer.

Box 1 shows the cancellation date, which fixes the tax year. Box 2 shows the cancelled amount — the number the IRS expects to see on your return. Box 3, cancelled interest, is generally part of that total.

That's the general rule; the full income-shock picture, including when a 1099-C is issued in error, lives in our guide to 1099-C cancelled debt taxes. This page covers the escape hatch: IRC §108's insolvency exclusion, claimed on Form 982, "Reduction of Tax Attributes Due to Discharge of Indebtedness." If you're still not sure why the IRS is writing to you at all, start with why did I get a letter from the IRS.

How the Form 982 insolvency exclusion works

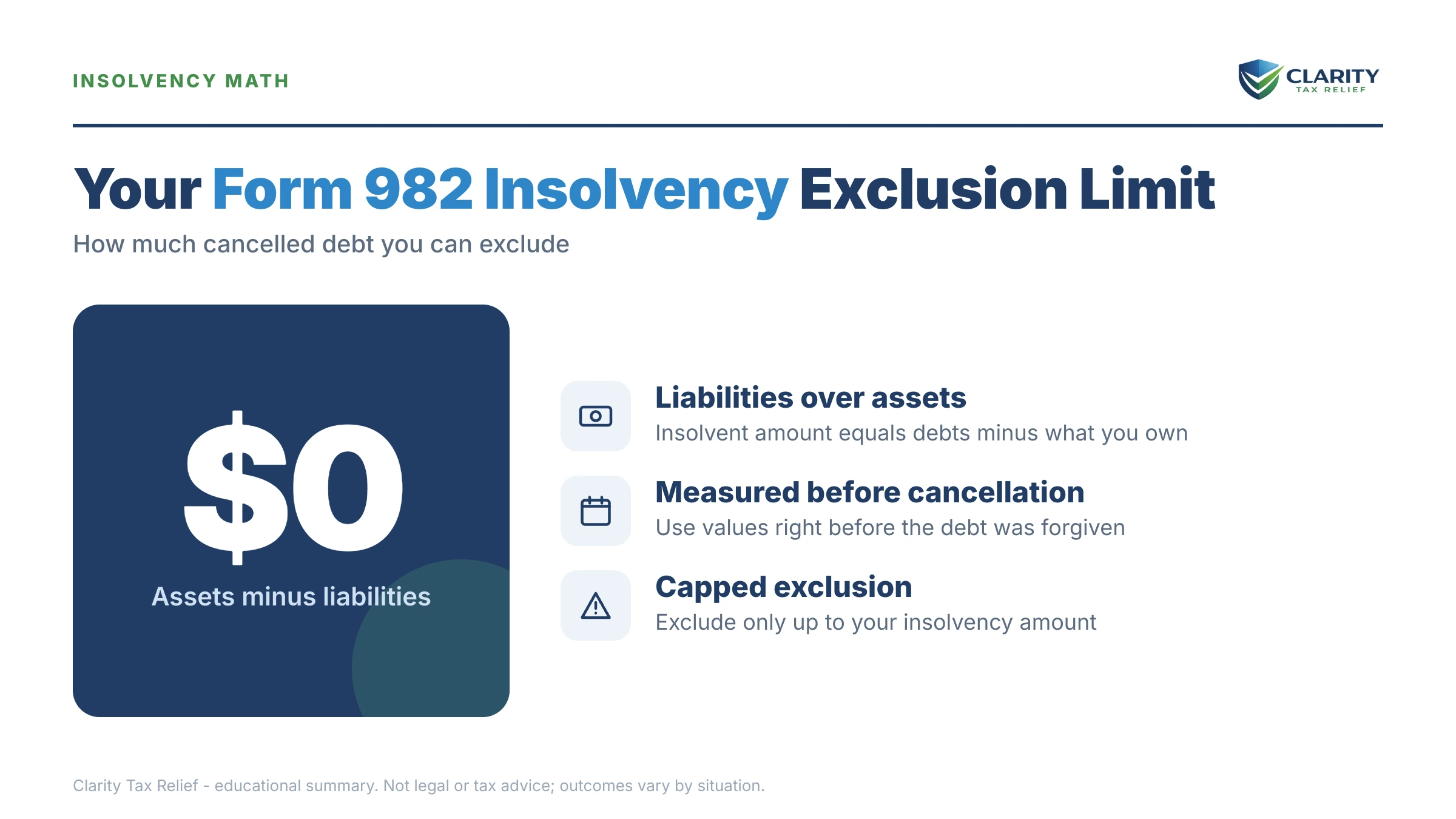

You were insolvent, for Form 982 purposes, if your total liabilities exceeded the fair market value of your total assets immediately before the cancellation. Not the day you file. Not the day the 1099-C arrives. The day before the date printed in box 1.

The exclusion is capped at your insolvency amount. If your debts topped your assets by $28,700, you can exclude up to $28,700 of cancelled debt — even if the creditor forgave more. Anything above the cap is still taxable.

Two details trip up more filers than everything else combined:

- The debt being cancelled counts as a liability. You measure the moment before discharge, so the balance about to be forgiven sits on your liability side of the ledger.

- Retirement accounts count as assets — 401(k)s, IRAs, and pension interests at full value, even though creditors can't reach them. Leaving them off is the most common way an insolvency claim collapses under IRS review.

| Assets (fair market value, day before cancellation) | Liabilities (balance owed, day before cancellation) |

|---|---|

| Cash, checking, and savings balances | The debt about to be cancelled (yes — include it) |

| Vehicles and real estate at current market value, not purchase price | Credit cards, personal loans, and medical debt |

| 401(k), IRA, and pension interests — even though creditors can't reach them | Mortgages, home equity loans, and auto loans |

| Household goods, electronics, jewelry, and clothing | Student loans |

| Brokerage accounts, crypto, and business interests | Past-due bills, taxes owed, and court judgments |

A worked example: $92,700 in debts, $31,000 cancelled

Say you're a W-2 employee, filing single, and a credit card issuer cancels $31,000 you stopped paying after a rough two years. The day before the cancellation, your balance sheet looked like this:

- Total liabilities: $92,700 — the $31,000 card about to be cancelled, a $38,500 car-and-personal-loan balance, $14,200 in other cards, and $9,000 in medical debt.

- Total assets: $64,000 — a car worth $9,500, $1,200 in checking, $5,300 in household goods and electronics, and a $48,000 401(k) you must count even though no creditor could touch it.

Insolvency = $92,700 − $64,000 = $28,700. You can exclude $28,700 of the $31,000. The remaining $2,300 is taxable income — in the 22% bracket, roughly $506 of tax instead of the roughly $6,820 you'd owe on the full $31,000. Form 982, box 1b, line 2 reading "$28,700," and a worksheet in your file is what stands between those two numbers.

Notice what the 401(k) did to the math: without it, you'd be insolvent by $76,700 and the entire $31,000 would vanish from income. With it, the exclusion is partial. That's why you run the worksheet honestly the first time — an overstated exclusion unravels years later, with penalties attached.

What happens if you ignore a 1099-C

The IRS already has its copy of your 1099-C, so leaving it off your return doesn't hide it — it just delays the bill and adds penalties. The underreporter sequence runs on autopilot:

- Computer matching. The Automated Underreporter program compares the creditor's 1099-C against your filed return — usually a year or more after you file, while interest quietly accrues from the original due date.

- CP2000 notice. The IRS proposes tax on the full box 2 amount, plus interest and often the 20% accuracy-related penalty. You typically get about 30 days to respond — and you can still claim insolvency at this stage by sending the worksheet and Form 982.

- CP3219A, the Notice of Deficiency. Ignore the CP2000 and the 90-day letter follows, starting your statutory 90-day window to petition Tax Court.

- Assessment and collection. Let the 90 days pass and the tax is assessed on debt you may never have owed tax on. The balance-due notice stream begins, ending in liens and levies if unpaid.

The bitter irony: many people who ignore a 1099-C were fully insolvent and would have owed nothing. The exclusion doesn't apply itself — it has to be claimed, and each stage of that sequence makes claiming it harder as bank statements age and asset values get fuzzy.

Holding a 1099-C and not sure the insolvency math works?

Send us the 1099-C and your rough numbers. An experienced tax professional will run the insolvency worksheet with you and tell you exactly how much you can exclude — free, confidential, before you file or respond to any notice.

Insolvency vs. your other Form 982 options

Insolvency is the most-used exclusion on Form 982, but it isn't the only one — and it isn't always the right one. Match your situation before you fill in a box:

| Your situation | The path | How much is excluded |

|---|---|---|

| Debts exceeded assets right before the cancellation | Insolvency exclusion — Form 982, box 1b | Up to your insolvency amount |

| Debt was discharged in a Title 11 bankruptcy case | Bankruptcy exclusion — Form 982, box 1a | 100% of the discharged debt, no insolvency math needed |

| Cancelled mortgage debt on your main home | Qualified principal residence exclusion — box 1e | Up to the statutory cap — confirm the provision covers your discharge year before relying on it |

| The 1099-C is wrong — amount, year, or not your debt | Corrected form from the creditor; identity theft goes on Form 14039 | None needed — income that isn't yours shouldn't be reported at all |

| Solvent, and no exclusion applies | Report the income; use a payment plan if you can't pay the resulting tax | $0 excluded — but the tax can be paid over time |

Three ordering rules worth knowing. First, bankruptcy beats insolvency: if the debt went through a Title 11 discharge, box 1a applies and you skip the worksheet entirely. Second, unlike the home-mortgage exclusion — which Congress has historically extended in short increments — the insolvency exclusion is permanent law with no expiration date. Third, a wrong 1099-C is never a Form 982 problem; if you got a 1099 you weren't expecting for a debt you don't recognize, dispute the form, don't exclude it.

And if the math says part of the cancelled debt is taxable and you can't pay the result, that's a solvable collection problem — the same options covered in CP2000: agree but can't pay apply, from 180-day short-term plans to monthly installment agreements.

How to respond, step by step: filing Form 982 for insolvency

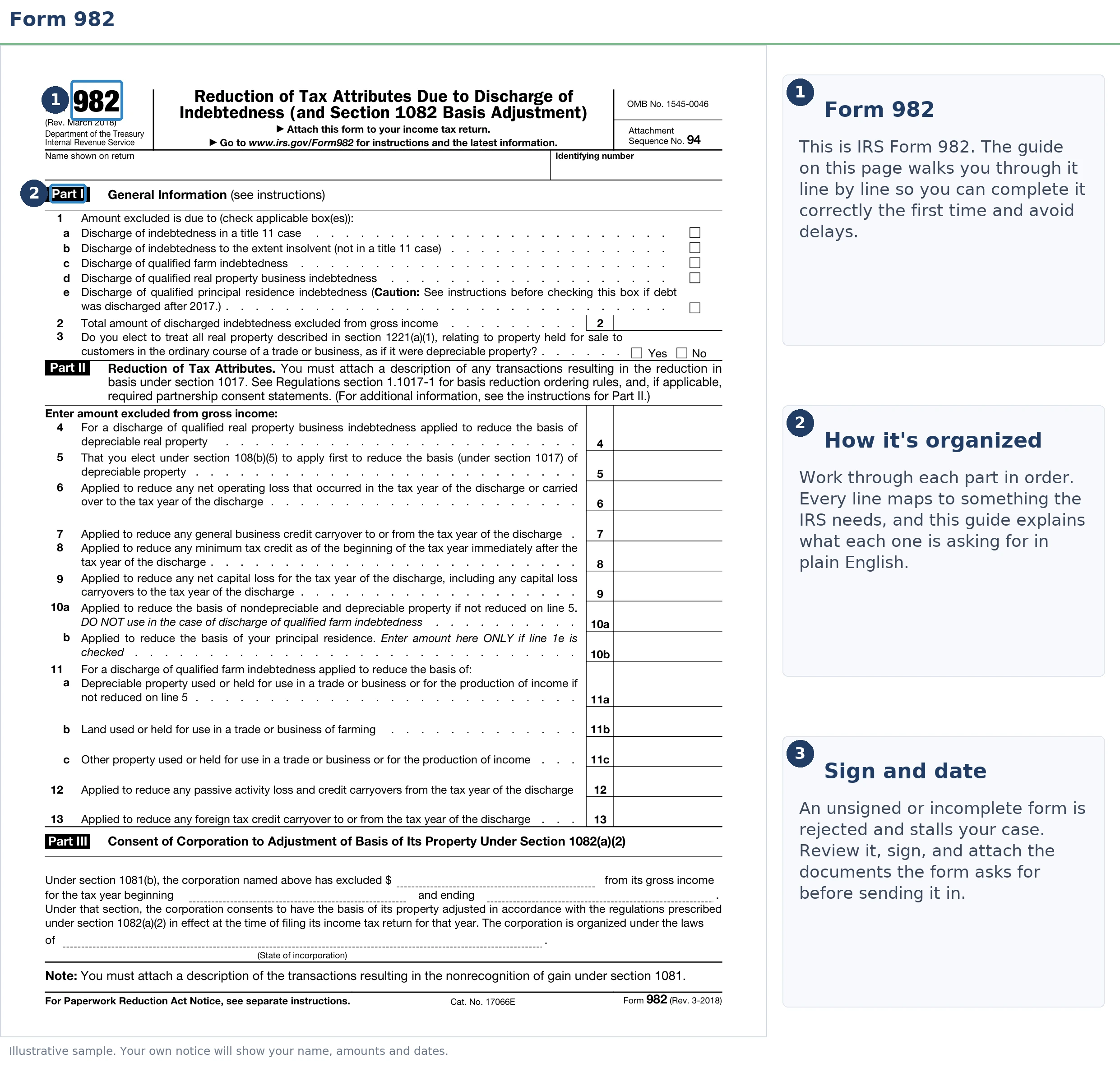

Filing the insolvency exclusion correctly takes six moves — and the ones the IRS never sees (your worksheet and records) matter as much as the ones it does. The form image on this page shows where each entry lands.

- Verify the 1099-C. Confirm box 1 (the cancellation date — it sets your tax year), box 2 (the cancelled amount), and that the debt is really yours and really cancelled. A wrong form gets disputed with the creditor, not excluded.

- Build your insolvency worksheet. Using the worksheet in Publication 4681, list every liability and every asset at fair market value as of the day before the cancellation — including retirement accounts. Liabilities minus assets is your insolvency amount.

- Complete Form 982. Check box 1b in Part I and enter your excluded amount on line 2 — the smaller of the cancelled debt or your insolvency amount.

- Reduce tax attributes in Part II. Most W-2 filers have no loss carryovers, credits, or business property basis to reduce, so Part II is often blank. If you do have attributes, follow the ordering rules in Publication 4681.

- Attach Form 982 to your return and file. File the form with your return for the box 1 year. Keep the worksheet, account statements, and valuation records — the IRS can ask for proof long after you file.

- Amend if you already filed without it. File Form 1040-X with Form 982 attached, generally within 3 years of filing the original return, to claim the exclusion and recover tax you overpaid.

If you're amending, expect a wait — amended returns move slowly, and our guide to where's my amended return explains the realistic timeline.

Form 982 deadlines and the rights each one protects

The insolvency exclusion never expires as a law, but your chance to claim it for a given year does. Here is every clock on this problem, in order:

| Deadline | What to do | What you lose if it passes |

|---|---|---|

| January 31 after the cancellation year | Watch for the 1099-C — creditors send it by this date | Nothing yet, but the IRS gets its copy whether or not yours arrives |

| Your return due date (typically April 15) | Attach Form 982 to the return for the box 1 year | Nothing permanent — but the matching computer will flag the gap |

| Generally 3 years from the date you filed | Claim a missed exclusion on Form 1040-X | The refund from the exclusion is generally gone for good |

| CP2000 response date (typically about 30 days) | Respond with the worksheet and Form 982 | The proposed tax moves toward assessment unchallenged |

| 90 days after a CP3219A | Petition Tax Court or resolve the balance | The tax is assessed and collection begins |

One more right worth knowing: if the IRS examines your return and disallows the exclusion, the decision isn't final. Smaller disputes can go to Appeals with Form 12203, where the insolvency worksheet gets a fresh look from someone other than the examiner who rejected it.

When you can handle Form 982 yourself

Plenty of insolvency claims need no professional at all. You can confidently do this yourself when the picture is simple: one 1099-C, a clearly negative balance sheet (debts obviously dwarf assets even with retirement accounts counted), and clean records — statements showing every balance as of the cancellation date. Fill in box 1b, line 2, keep the worksheet, done.

Experienced help changes the outcome in a narrower set of situations:

- The math is close. When insolvency turns on how you value a car, a house, or household goods, valuation judgment — and documentation that survives review — decides whether you exclude $28,700 or $0.

- Multiple 1099-Cs across dates or years. Each cancellation needs its own insolvency snapshot, and the order matters because every discharge changes the next balance sheet.

- A CP2000 or exam is already open. Presenting insolvency to the underreporter unit is a documentation exercise with a deadline; if you'd rather a professional handle the correspondence directly, Form 2848 is how you authorize that.

- Business or rental debt was cancelled. Part II attribute reduction gets real when there's depreciable property, loss carryovers, or basis to adjust — a wrong ordering creates problems in future years.

- You can't pay whatever remains taxable. If the leftover tax needs a hardship or settlement analysis, the IRS will want your finances on Form 433-A, and how it's prepared shapes what you're offered.

Terms on your 1099-C and Form 982, decoded

- Cancellation-of-debt (COD) income — the forgiven balance the tax code treats as income because you kept money you never repaid.

- Insolvency — total debts greater than the fair market value of total assets, measured immediately before the cancellation; it's arithmetic, not a court status.

- Fair market value (FMV) — what an asset would actually sell for today, not what you paid for it or what you owe on it.

- Tax attributes — carryovers and basis (losses, credits, property basis) that Part II of Form 982 reduces in exchange for the exclusion; most wage earners have none.

- Identifiable event (box 6) — the creditor's code for why the debt was cancelled: settlement, expired collection, foreclosure, or a policy decision to stop collecting.

- Qualified principal residence indebtedness — cancelled mortgage debt on your main home, covered by its own on-again, off-again exclusion at box 1e.

Form 982 insolvency questions, answered

How do I prove insolvency to the IRS for Form 982?

You prove it with the insolvency worksheet in IRS Publication 4681 — a line-by-line list of every asset and every liability as of the day before the cancellation. You don't attach the worksheet to your return, but keep it with account statements, payoff letters, and valuation records, because the IRS can ask for it later through a CP2000 or an exam. The weakest worksheets are the ones built from memory two years after the fact.

Do retirement accounts count as assets on the insolvency worksheet?

Yes. Your 401(k), IRA, and pension interests count at full value on the insolvency worksheet, even though creditors generally can't touch them. This is the single most common Form 982 mistake — leaving out a $48,000 retirement balance can flip you from insolvent to solvent on paper and sink the whole exclusion. Count everything you own, protected or not.

Can I file Form 982 after I already filed my return?

Yes. File Form 1040-X for the cancellation year with Form 982 attached, generally within 3 years of the date you filed the original return (or 2 years from when you paid the tax, if later). If you reported the 1099-C as income and paid tax you could have excluded, the amendment produces a refund. After the window closes, the refund is generally lost even if the insolvency math was airtight.

What if I was only partially insolvent?

You exclude cancelled debt only up to your insolvency amount; the rest is taxable income. If you were insolvent by $28,700 and the creditor cancelled $31,000, you exclude $28,700 on Form 982 and report the remaining $2,300 as income. Partial exclusion is normal and the IRS accepts it routinely — the mistake is claiming 100% when the worksheet only supports part.

Do I have to file bankruptcy to use the Form 982 insolvency exclusion?

No. Insolvency is a math test, not a legal status — you qualify if your total debts exceeded the fair market value of your total assets immediately before the cancellation, whether or not you ever filed anything in court. If the debt actually was discharged in a Title 11 bankruptcy case, you use box 1a instead, and the entire discharged amount is excluded with no insolvency calculation at all.

Is Form 982 the same as disputing a wrong 1099-C?

No — Form 982 accepts that the debt was cancelled and excludes the income; a dispute says the 1099-C itself is wrong. If the amount, year, or debtor name is incorrect, contact the creditor for a corrected form and keep your proof. If the debt was never yours — an account opened in your name — that's an identity-theft problem handled with Form 14039, not an exclusion problem.

Does the insolvency exclusion apply to state income taxes?

Usually, but not automatically. Most states start their tax calculation from federal adjusted gross income, so income you exclude federally with Form 982 never enters the state return. A minority of states decouple from parts of the federal rules, so confirm how your state treats cancelled-debt income before assuming the exclusion carries through — especially if the amount is large.

What date do I measure insolvency on?

Immediately before the cancellation — in practice, the day before the date in box 1 of your 1099-C. Your liabilities on that date include the debt that's about to be cancelled. If you received multiple 1099-Cs with different dates, you run a separate insolvency calculation for each cancellation, because your balance sheet changes after each discharge.

Your next 24 hours

- Find two numbers on your 1099-C: the date in box 1 (it sets the tax year and your measurement date) and the amount in box 2 (the income the IRS expects to see).

- Gather your day-before snapshot: statements or balances for every debt and every asset — including retirement accounts — as of the day before that box 1 date, plus your most recent tax return.

- Get the math checked free. Use the 2-minute form or call (888) 825-7779. Whether you're filing this year's return, amending inside the 3-year window, or answering a CP2000 that's already ticking, an experienced tax professional can confirm your insolvency number before the IRS taxes debt you may not owe a dime on.

Primary sources: the IRS's official pages for Form 982 and Publication 4681 (which contains the insolvency worksheet), and IRS.gov/payments if part of the cancelled debt remains taxable and you need time to pay.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.