Back Taxes by Profession

Owner Operator Truck Driver Back Taxes: How to Fix Them in 2026

The short answer: owner operator truck driver back taxes usually come from 15.3% self-employment tax with zero withholding, skipped quarterlies, and unfiled years the IRS replaced with inflated substitute returns. Fix it in this order: file accurate returns with your real trucking deductions, then set up the payment plan or hardship option your numbers support.

You ran hard all year. The carrier reported every settlement on a 1099-NEC, nothing was withheld, and after the truck note, fuel, and insurance there was never a spare $8,000 sitting around in April. Now the balance spans more than one year and it's showing up at the worst time — like when a lender pulls your file for a refinance.

This is fixable, and the order you fix it in decides what you pay. Here is the whole map: why the balance got this big, what the IRS does next, which deductions shrink it, and which program actually fits an owner-operator's income.

⏱ The clock that's actually running: there's no single deadline on back taxes, but the meter never stops. The failure-to-file penalty runs 5% per month (up to 25%) — ten times the 0.5% monthly failure-to-pay penalty — and interest compounds on top of both. Every quarter of waiting adds real money and moves you one notice closer to a levy.

Why owner-operator truck drivers end up with back taxes

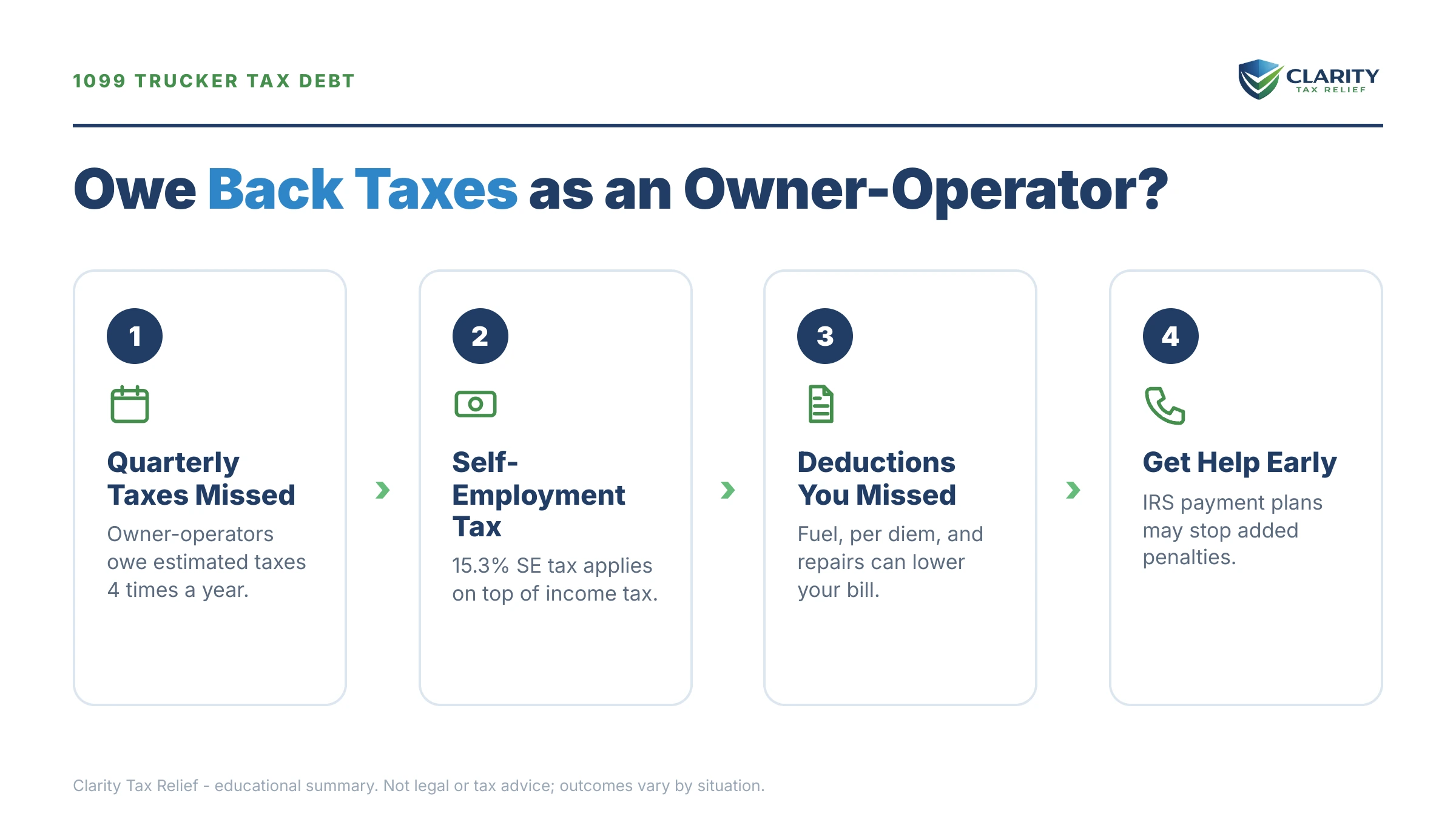

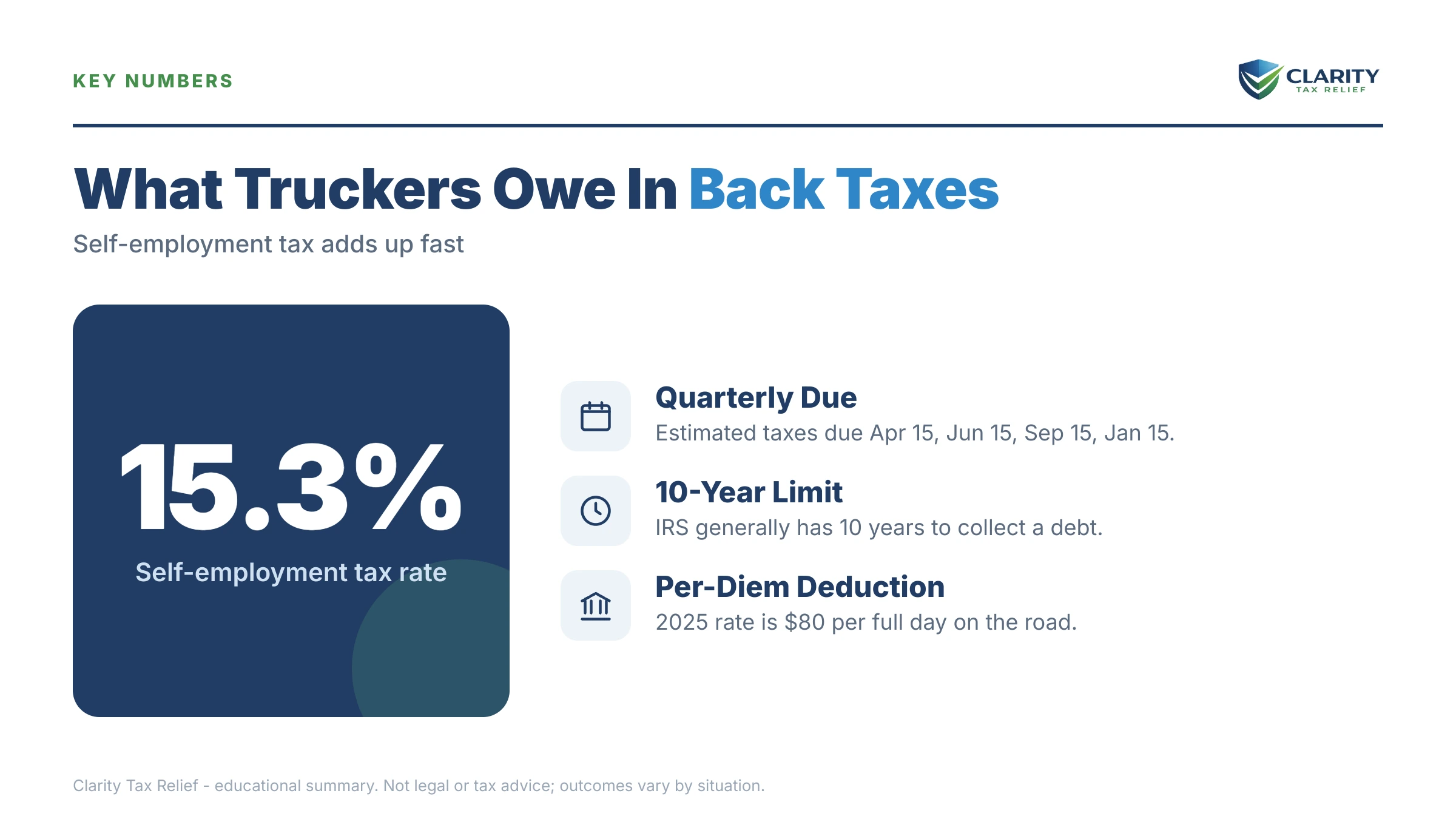

An owner-operator pays 15.3% self-employment tax on net profit before regular income tax even starts — with no employer withholding a dime of it. That structural gap, not carelessness, is why trucker tax debt is so common.

Four things stack the deck against you specifically:

The 1099 shows gross, not what you kept. Your carrier or the brokers you haul for report the full settlement amounts. The IRS's computers see that top-line number. Your fuel, truck payment, maintenance, and insurance only enter the picture when you put them on a Schedule C — and if you don't file, they never do.

Quarterlies collide with cash flow. Estimated payments come due four times a year whether freight rates are up or down. One blown engine or one soft quarter, and the money earmarked for the IRS goes into the truck instead — because without the truck there's no income at all. Our guide to how quarterly estimated taxes work covers the mechanics; the point here is that skipping them is how a one-year problem becomes a three-year problem.

Unfiled years turn into substitute returns. If you stop filing, the IRS eventually files for you — a substitute for return (SFR) built on your gross 1099 income with almost no trucking deductions. A driver who grossed $180,000 and netted $55,000 gets assessed as if most of that gross were profit. This is the single biggest reason owner-operator balances look impossibly large, and it's also the most correctable (more on that below).

Missed per diem leaves money on the table. Drivers subject to DOT hours-of-service rules can deduct 80% of the transportation-industry meal per diem for every qualifying night away from home — a deduction many self-prepared returns skip entirely. Over a 250-night year, that's a meaningful cut to taxable profit, and it can be claimed on late-filed or amended returns.

One boundary worth naming: this article covers the individual 1099 owner-operator. If you run multiple trucks with drivers on payroll, the stakes and the rules change — see our guide to trucking company tax debt for fleet payroll and IFTA issues.

What happens if you ignore trucker back taxes

Ignored back taxes move through an automated notice sequence that ends with a levy on your bank account — and on the carrier or factoring company that pays you. The sequence runs itself: IRS staffing fell roughly 27% in 2025, but the notice and levy systems are software, and software doesn't take layoffs.

- CP14 — the first bill. The balance, penalties, and interest, with roughly 21 days to respond before the next notice queues up.

- CP501 / CP503 — reminders. Still just bills, but the balance grows monthly while they arrive.

- CP504 — intent to levy your state refund. Under IRC §6331(d), the IRS can now take your state tax refund, and a Notice of Federal Tax Lien becomes a live possibility — the event that matters most if you own a home.

- LT11 / Letter 1058 — final notice of intent to levy. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After it runs, the IRS can levy bank accounts and reach the money your carrier or factoring company owes you.

- Levy stage. A bank levy freezes funds with a 21-day hold before the money leaves. A levy served on your carrier grabs whatever settlements they owe you the day it lands — see can the IRS garnish 1099 income for how contractor levies actually work.

Unfiled years run on a parallel track: non-filer notices escalate until the IRS files the SFR and issues a 90-day deficiency notice (CP3219N), after which the inflated balance becomes legally assessed and joins the collection sequence above.

Two more consequences hit drivers harder than most. Once your total certified debt passes $66,000 (the 2026 threshold), the IRS can certify it to the State Department and your passport can be denied or revoked — a direct problem for cross-border runs. And every balance carries a 10-year collection statute (CSED) from the date it was assessed, which is why waiting out the IRS almost never works on debt this fresh.

| Notice | What it means | Your window |

|---|---|---|

| CP14 | First bill: tax, penalties, interest | Typically 21 days from the notice date |

| CP501 / CP503 | Reminder bills; balance still growing | Notices typically arrive weeks apart — use the date printed on yours |

| CP504 | Intent to levy your state refund; lien filing becomes likely | The pay-by date printed on the notice |

| LT11 / Letter 1058 | Final notice of intent to levy; Collection Due Process rights attach | 30 days to request a CDP hearing (Form 12153) |

| After LT11 | Bank levy (21-day hold), levy on carrier/factoring settlements | Ongoing until you resolve or the IRS releases it |

Owner-operator with IRS letters stacking up?

Before the sequence reaches your settlements or a lien hits your home's title, get a free review of exactly where your account stands — which years are unfiled, what the IRS thinks you owe, and which option your numbers actually support.

Owner operator truck driver back taxes: every resolution option compared

Every IRS resolution option is means-tested against your filed returns — which is why accurate filing comes before any deal. For the general mechanics of each program, see how to settle tax debt yourself; what follows is how each option behaves when the income is settlement checks and the biggest assets are a tractor and a house.

| Option | Who it fits | Cost and catch |

|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup; interest and penalties keep accruing |

| Guaranteed installment agreement | Balance ≤ $10,000, all returns filed, current on this year | Approval is set by statute; up to 3 years to pay |

| Streamlined installment agreement | ≤ $25,000, or ≤ $50,000 with direct debit; up to 72 months | Setup fee applies; no financial disclosure; direct debit generally avoids a lien filing |

| Partial-pay agreement / non-streamlined | Over $50,000, or can't full-pay before the 10-year CSED | Form 433 financials required; lien filing likely |

| Currently Not Collectible | Allowable living and operating expenses meet or exceed income | Collection pauses; debt and interest remain; refunds still offset |

| Offer in Compromise | Equity plus future income genuinely can't cover the debt | $205 fee; 20% down on lump-sum offers (both waived if AGI ≤ 250% of poverty); roughly 1 in 5 accepted in FY2024 |

| Penalty abatement | Clean 3-year history (first-time abate) or reasonable cause | Removes penalties, not the tax or interest on the tax |

Three owner-operator-specific notes on that table:

Seasonal freight income breaks fixed payments. If a streamlined agreement's monthly number only works in a good quarter, look at a partial payment installment agreement — payments sized to what your financials actually show — or currently not collectible status while self-employed if a bad market has you at break-even. Both use IRS allowable-expense math, and your fuel, truck payment, and insurance count as business expenses in that math.

Truck equity works against an offer. The IRS values what it could collect from everything you own. A paid-off tractor worth $60,000 usually sinks an offer on a $36,900 debt all by itself, before your house even enters the calculation. An OIC is real relief for the right facts — but for most working owner-operators with equipment and home equity, the honest answer is a payment plan plus penalty relief.

Penalty relief has two paths in 2026. First-time abatement still works if your prior three years were clean, and reasonable cause covers documented breakdowns, medical events, or a freight-market collapse that made compliance impossible. Starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies qualifying relief without a request. To see how much of your balance is penalties and interest rather than tax, run your numbers through our IRS Penalty & Interest Calculator — it estimates the accruals so you know what abatement is worth fighting for.

The refinance problem: back taxes, liens, and your mortgage

A filed Notice of Federal Tax Lien — not the tax debt itself — is what stalls a refinance. The lien attaches to your home's title, and no underwriter will close over an unresolved federal claim without a plan for it.

That makes timing everything. Before a lien is filed, a balance of $50,000 or less can usually go onto a direct-debit streamlined installment agreement — and on those agreements the IRS generally does not file a lien at all. Set the agreement up first, and the refinance conversation is about a documented monthly payment, not a title defect. Most lenders will want to see the agreement in place and a record of on-time payments.

If a lien is already on record, you still have routes: paying through closing, lien subordination via Form 14134 (the IRS agrees to let the new mortgage take priority so the refi can close), or discharge of the specific property. Our guide to refinancing with an IRS lien walks through each path. The takeaway: if a refinance is on your calendar, resolving the back taxes isn't just about the IRS — it's about locking your rate.

Worked example: an owner-operator who owes $36,900

Say you owe $36,900 across two tax years — mostly self-employment tax from seasons when the quarterlies didn't get paid — and you're planning to refinance your house this year. This is a hypothetical, but the math is real:

The payment plan path. At $36,900 you're under the $50,000 streamlined ceiling, so you can set up a direct-debit agreement online with no financial disclosure. Spread over the maximum 72 months, the base payment is $36,900 ÷ 72 = about $513 per month. Interest and the 0.5% monthly failure-to-pay penalty keep accruing on the declining balance, so paying more than the minimum — say $650 when freight is good — shortens the payoff and cuts the total cost meaningfully.

Why direct debit is the whole ballgame here. On a direct-debit streamlined agreement, the IRS generally does not file a tax lien. No lien means clean title, which means the refinance can proceed on normal terms. Wait until after a CP504-stage lien filing, and you're negotiating subordination paperwork with the IRS while your rate lock expires.

Why an offer likely fails on these facts. An Offer in Compromise requires showing the IRS that your equity plus future income can't cover $36,900 before the collection statute runs. A homeowner with enough equity to refinance almost always fails that test — the home equity alone typically exceeds the debt. Spending months and fees on a doomed offer, while notices escalate, is the classic mistake in exactly this situation.

Where the balance can still shrink. If either year's return missed per diem or under-claimed depreciation, an amended return can cut the underlying tax. And if your three years before the first bad year were clean, first-time penalty abatement can strip that year's penalties — on a balance this size, often four figures.

Rebuild the returns first: the deductions that shrink the balance

A substitute-for-return assessment taxes your gross settlements with almost none of your trucking deductions — so filing your own accurate returns is usually worth more than any negotiation. If the IRS filed a substitute return for you, submitting your original return generally gets the balance corrected down to what you actually owe.

Two ground rules for heavy trucks: the standard mileage rate doesn't apply to a semi tractor — you deduct actual expenses — and you generally need the last six years of returns filed before the IRS will approve any agreement. Lost paperwork isn't fatal: settlement statements from your carrier, fuel card annual summaries, bank records, and ELD logs can reconstruct most of a trucking Schedule C — here's how to file back taxes without records.

| Deduction | What counts | Records that prove it |

|---|---|---|

| Fuel | Diesel, DEF, reefer fuel | Fuel card annual summaries, IFTA filings |

| Truck depreciation / Section 179 | Tractor and trailer cost recovery | Purchase contract, loan documents |

| Repairs and maintenance | Tires, engine work, PMs, roadside | Shop invoices, bank and card statements |

| Insurance | Physical damage, bobtail, cargo, occupational accident | Policy declarations, settlement deductions |

| Per diem (meals) | 80% of the transportation-industry daily rate for DOT hours-of-service drivers | ELD logs showing nights away from home |

| Interest on the truck note | Interest portion of equipment financing | Lender year-end statements |

| Permits, plates, HVUT | Base plates, permits, Form 2290 heavy vehicle use tax | Registration receipts, Schedule 1 stamped copies |

| Tolls, scales, parking | Road tolls, CAT scales, paid truck parking | Transponder statements, receipts |

| Technology and fees | ELD subscription, load boards, phone, factoring fees | Subscription invoices, settlement statements |

The per diem line deserves emphasis: the IRS publishes a flat daily rate for transportation workers each fall, and DOT hours-of-service drivers deduct 80% of it instead of the usual 50% — with ELD logs serving as ready-made proof of every qualifying night. On late-filed returns covering hundreds of road nights per year, this one line can move the balance by thousands.

How to fix owner-operator back taxes, step by step

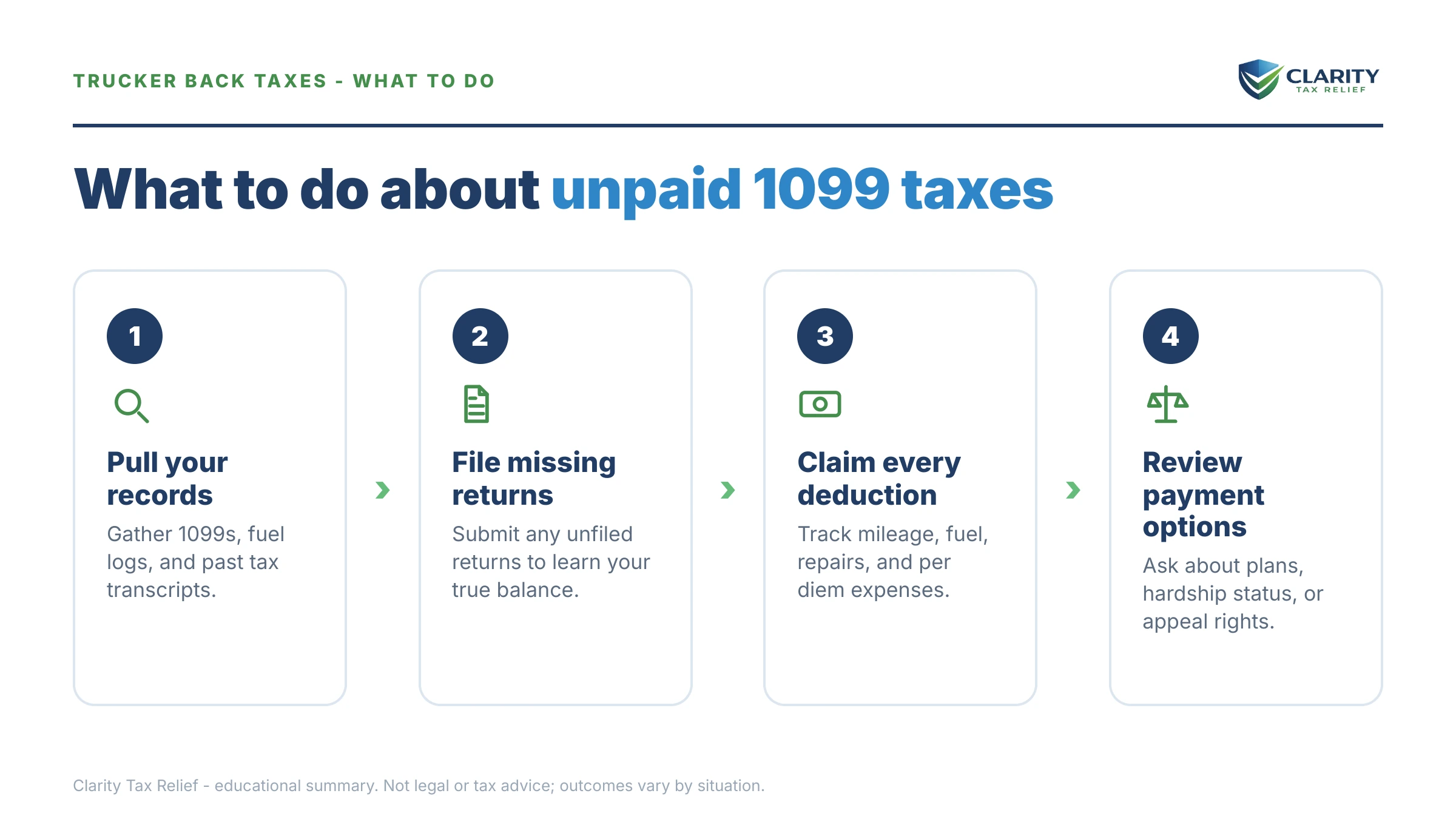

- Pull your IRS transcripts. Get your wage and income transcripts and account transcripts for every open year through your IRS online account. They show every 1099 the IRS has on file, which years are unfiled, and whether any substitute-for-return assessments exist.

- File the missing returns with real deductions. Prepare the last six years (or fewer, if fewer are missing) using settlement statements, fuel card annual reports, and ELD logs to capture fuel, depreciation, insurance, and per diem. This step alone often shrinks the balance before you negotiate anything.

- Replace any substitute-for-return assessments. If the IRS filed for you, submit your own original return for that year so the inflated SFR balance is corrected before you agree to pay it.

- Set up the resolution that fits your numbers. Under $50,000 with steady settlements, a direct-debit streamlined installment agreement usually fits and generally avoids a lien filing. Thin or seasonal freight income may point instead to a partial-pay agreement, hardship status, or an offer.

- Request penalty relief. Ask for first-time abatement on a qualifying year and reasonable-cause relief where a breakdown, medical event, or freight collapse explains the lapse. Starting summer 2026, the IRS's Automatic Exemption from Penalty applies qualifying relief automatically.

- Fix your quarterlies so the debt never rebuilds. Set aside a fixed percentage of every settlement and pay quarterly estimates going forward — a payment agreement defaults if a new balance posts next April.

Situations that change the playbook

Married and filing jointly. On a joint return, your spouse is equally liable and their W-2 withholding and refund get pulled into the balance. If the debt predates the marriage or comes from your separate filings, their refund share can be protected with an injured-spouse claim (Form 8379). Which filing status to use going forward is a real strategic decision while a balance exists.

You put a driver in a second truck. The moment you pay someone to drive, you've entered payroll territory — and if you withheld taxes and didn't deposit them, that's a different animal entirely, with personal liability that survives almost everything. See 941 back taxes before you make any other move. If you paid the driver on a 1099, misclassification exposure is the risk to get evaluated.

You formed an LLC or S-corp mid-stream. Entity changes split the debt across different taxpayer identities and can create payroll obligations for your own salary. Resolution still works, but the account structure needs to be mapped before anyone calls the IRS.

Multiple years, some disputed. If one year's assessment is genuinely wrong — an SFR, a duplicated 1099, income that belonged to your business entity — fix that year first. Never put an inflated balance on a payment plan; you'll pay the error monthly for six years.

When you can handle this yourself

Plenty of owner-operators don't need professional help. If all your returns are filed, the balance is accurate, and you owe under $50,000, you can set up a streamlined direct-debit agreement online in an evening — no negotiation, no fees beyond the IRS setup charge. If you can clear the whole balance within 180 days, the short-term plan is free to set up and even simpler. And a single clean year's penalties often come off with one first-time-abatement phone call.

Experienced help changes outcomes in a different set of situations: several unfiled years with SFR assessments that need replacing, a levy already sitting on your carrier or factoring company, a lien threatening a refinance you can't postpone, payroll debt from drivers you hired, or offer math that depends on how a tractor and a home get valued. In those cases the sequencing — which year to fix first, which agreement to request, when to invoke appeal rights — is where the money is won or lost.

If your settlements are already being intercepted or you're staring at three-plus unfiled years, have an experienced tax professional map the sequence before you call the IRS — the free case review at (888) 825-7779 covers exactly that, with no obligation.

Terms on your notices, decoded

SFR (substitute for return): a return the IRS files for you using gross 1099 income and almost no deductions — replaceable by filing your own original return.

Lien vs. levy: a lien is a legal claim against what you own (it clouds your home's title); a levy is the actual taking of money — from a bank account or from what your carrier owes you.

CSED: the Collection Statute Expiration Date — the IRS generally has 10 years from assessment to collect, though offers, appeals, and bankruptcy pause the clock.

CDP rights: Collection Due Process — the 30-day right to a hearing (Form 12153) after a final levy notice, which pauses levy action while it's pending.

Per diem: a flat daily meal allowance for nights away from home; DOT hours-of-service drivers deduct 80% of it.

1099-NEC vs. 1099-K: the NEC reports what a carrier or broker paid you directly; the K reports payment-app or card-network volume — the IRS matches both against your return.

Owner-operator back-tax questions, answered

Can the IRS levy my settlement checks from the carrier I'm leased to?

Yes. The IRS can serve a levy on the carrier or factoring company that pays you, and it captures whatever they owe you on the day the levy lands. Unlike a W-2 wage garnishment, a levy on 1099 income is generally one-time — but the IRS can serve a fresh levy on every settlement cycle until you set up an agreement.

Can the IRS take my truck for back taxes?

It is legally possible but rare. Seizing your tractor destroys the income the IRS collects from, so revenue officers usually push for a payment agreement instead, and asset seizures require multiple levels of approval. The realistic risks come earlier: bank levies, levies on your settlements, and a federal tax lien that attaches to the truck's equity.

Can I lose my CDL over IRS back taxes?

The IRS cannot suspend your CDL — driver's licenses are state-issued, and federal tax debt does not touch them. Two license-adjacent risks are real, though: some states suspend licenses over state tax debt, and the IRS can certify seriously delinquent debt over $66,000 (the 2026 threshold) to the State Department, which can deny or revoke your passport — a problem if you run Canada loads.

How many years of back tax returns does an owner-operator have to file?

The IRS generally requires the last six years of returns to consider you compliant, even if you have more unfiled years than that. Filing those six accurately — with your fuel, depreciation, insurance, and per diem deductions — is the gate to every resolution option; the IRS will not approve a payment plan or offer while required returns are missing.

Will back taxes stop me from refinancing my house?

Not automatically. What blocks a refinance is a filed Notice of Federal Tax Lien, because it clouds title and puts priority questions on the closing table. If you owe $50,000 or less and set up a direct-debit streamlined installment agreement before a lien is filed, the IRS generally does not file one — which is why timing matters so much for homeowners.

Can I claim trucker per diem on back tax returns?

Yes — per diem is claimed on the return for each year you file or amend, using the transportation-industry rate that was in effect for that year. Drivers subject to DOT hours-of-service rules deduct 80% of the meal allowance instead of the usual 50%. At 250 or more nights on the road per year, that single deduction can cut a back-tax balance by thousands per year.

Do owner-operators qualify for an Offer in Compromise?

Only if the math works: the IRS accepts an offer when your equity plus future income genuinely cannot cover the debt before the collection statute expires. Truck and home equity count against you, and the IRS accepted roughly 1 in 5 offers in FY2024. There is a $205 application fee and, for lump-sum offers, 20% down — both waived if your AGI is at or below 250% of the federal poverty level.

What if the IRS already filed a return for me (SFR)?

File your own original return for that year. A substitute for return counts your gross 1099 income with almost none of your trucking deductions, so the assessment is usually far higher than what you actually owe. When you file an accurate return, the IRS generally adjusts the balance down to the correct figure — often the single biggest reduction available in an owner-operator case.

Is my spouse liable for my trucking back taxes?

It depends on how you filed. On a joint return, you are both fully liable for the entire balance, and a joint refund can be taken. If the debt comes from years you filed separately or before the marriage, your spouse is not personally liable — but a joint refund can still be offset, and Form 8379 (injured spouse) can recover their share.

Your Next 24 Hours

- Pull your account. Log into your IRS online account and write down two things: the total balance by year, and which years show no return filed. That list is your whole case in miniature.

- Gather your trucking records. Last filed return, every 1099-NEC, settlement statements, fuel card annual summaries, and your ELD login — everything needed to rebuild accurate returns and prove the deductions.

- Get the free case review. Bring that balance list to the 2-minute form or call (888) 825-7779. Penalties and interest are accruing monthly either way — an experienced tax professional can tell you in one conversation whether filing, abatement, or an agreement should come first.

Primary sources for this guide: the IRS Trucking Tax Center, the official IRS payment plans page, and IRS.gov/payments for making payments directly.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.