Self-Employed & Gig Taxes

Side Hustle Taxes: How Much to Save in 2026

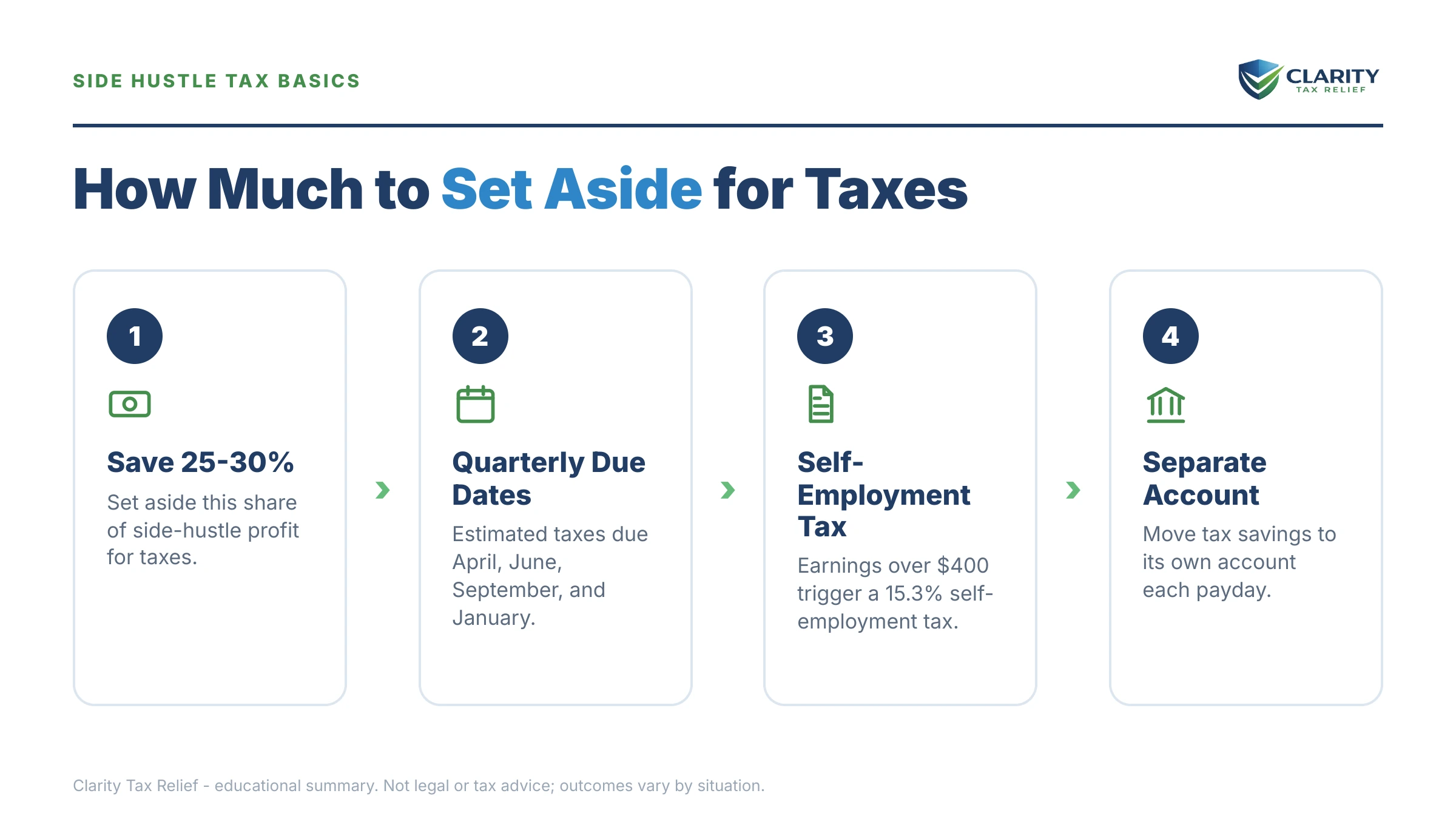

The short answer: for side hustle taxes, how much to save is 25% to 30% of your net profit for most people in 2026. Self-employment tax takes 15.3% of net earnings, and income tax at your marginal rate stacks on top — with nothing withheld. Lower earners can save 20–25%; higher earners need 30–40%.

The divorce is final, the bills are in your name alone, and the freelance work that started as breathing room is now real money — deposited with nothing withheld from any dollar of it. It's unnerving to realize no one is setting the tax money aside for you. But the fix is a percentage, a separate account, and four dates a year — and this guide gives you all three, tuned to your new filing status.

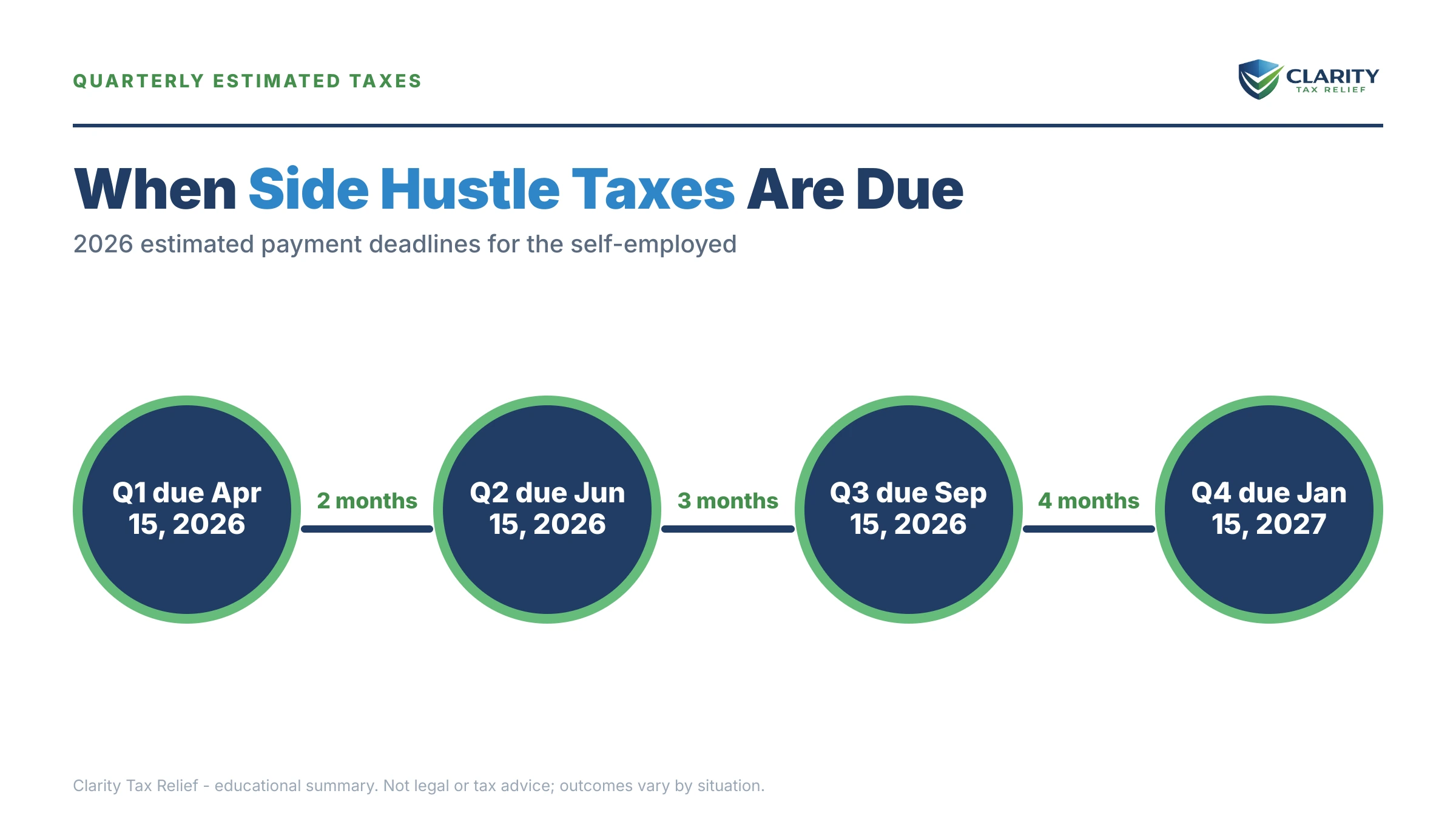

⏱ Your real clock: tax on side-hustle income is due four times a year, not once in April. The next 2026 estimated payment deadlines are September 15, 2026 and January 15, 2027. Fall short in a quarter and the IRS adds an underpayment charge for that quarter — even if you pay everything by April 15.

Why side hustle income creates a tax bill nobody withheld

A side hustle pays two federal taxes at once: 15.3% self-employment tax plus income tax at your marginal rate — and no employer withholds either. Your W-2 job splits Social Security and Medicare with your employer and skims income tax from every check. Your 1099 income does neither, so the full bill lands on you at filing time.

The self-employment tax is 12.4% for Social Security plus 2.9% for Medicare, computed on Schedule SE against 92.35% of your net profit. It applies from the first $400 of net earnings — long before any client is required to send you a 1099-NEC.

Then income tax stacks on top. Because your day job already fills the lower brackets, every side-hustle dollar is taxed at your highest rate. That stacking is why the first year self-employed tax bill shocks so many people: the side money felt like extra, but the IRS taxes it as the top slice.

One more trap: no form does not mean no tax. The 1099-K $20,000 threshold is back for 2026, so most payment apps won't report your income — but you still owe on it, and the IRS can match deposits years later.

Side hustle taxes: how much to save in 2026 (the percentage table)

Most side hustlers should save 25% to 30% of net profit for federal taxes, plus their state's income tax rate. The right number depends on your total income — day job plus side profit — because that total sets the marginal rate your side dollars hit. Save on net profit (income minus expenses), not gross deposits.

| Total income (day job + side profit) | Likely federal picture (single filer) | Set aside from net profit |

|---|---|---|

| Under roughly $50,000 | 10–12% income tax + 15.3% SE tax | 20–25% |

| Roughly $50,000–$100,000 | 22% income tax + 15.3% SE tax | 25–30% |

| Roughly $100,000–$200,000 | 24% income tax + 15.3% SE tax | 30–35% |

| Over roughly $200,000 | 32%+ income tax + SE tax + 0.9% extra Medicare tax | 35–40% |

Two adjustments to the table. First, add your state: state income tax runs from zero to more than 10% depending on where you live. Second, deductions pull the real bill down — half your SE tax comes off your income, and the qualified business income (QBI) deduction shields up to 20% of net profit from income tax. That's why the set-aside bands land lower than the raw rates suggest.

Expenses matter more than most new side hustlers realize. Mileage at the 2026 mileage rate for the self-employed, supplies, platform fees, phone use, and home-office costs all reduce the net profit you save against. The rules are the same whether you freelance, drive, or rent a room — though hosts have their own reporting wrinkles, covered in our guide to Airbnb host back taxes.

Divorce changed your math: the filing-status trap

Filing single instead of jointly can push the same side income into a higher tax bracket, because single-filer bracket thresholds are roughly half the joint thresholds. Income that stayed in the 12% bracket on a joint return can land in the 22% bracket on your first single return — which alone can move your set-aside up several percentage points.

Three specific things to check the year after a divorce:

- Your W-4 at your day job. If it still says "married," your paycheck withholding is calibrated to a return you no longer file. That under-withholding compounds the side-hustle gap — two leaks, one April bill. File a new W-4 now.

- Head of household. If your kids live with you most of the year, head-of-household status gives you wider brackets and a bigger standard deduction than single — and can move you down a row in the table above.

- Your safe harbor number. The prior-year safe harbor is normally 100% of last year's total tax — but last year's tax was on a joint return, and it doesn't carry over cleanly to your new separate return. After a divorce, targeting 90% of your current year's tax is usually the safer play.

One clarification while you're untangling finances: a divorce decree assigning old joint tax debt to your ex doesn't bind the IRS. If that's part of your picture, see divorce and IRS debt: who pays — it's a separate problem from this year's set-aside, and it has separate fixes.

A worked example: saving on $13,600 of side income

On $13,600 of net side-hustle profit, a single filer with a mid-five-figure salary owes roughly $4,100 in federal tax. Say you're newly single, earn $58,000 at your W-2 job, and cleared $13,600 freelancing this year. Here's the math, rounded:

- Self-employment tax: $13,600 × 92.35% = $12,560 of SE earnings, × 15.3% = about $1,922.

- Half-SE deduction: about $961 comes off your taxable income.

- QBI deduction: roughly 20% of the remaining profit — about $2,528 — is shielded from income tax.

- Income tax: the ~$10,111 still taxable lands largely in the 22% bracket at that salary — about $2,224.

Total: roughly $4,146 on $13,600 of profit — about 30.5 cents per dollar. A 30% set-aside ($4,080, or $340 a month) nearly covers it; your state's income tax goes on top. And note the divorce effect: on a joint return at a similar combined income, more of that profit might have stayed in the 12% bracket. The same side hustle can cost meaningfully more the year your filing status changes — which is exactly why the old "save 20%" advice fails newly single filers.

When to send it: quarterly deadlines and the safe harbor

The IRS expects tax on side-hustle income four times a year, and each quarter stands on its own. Setting the money aside is half the system; sending it in on time is the other half. Full mechanics are in how quarterly estimated taxes work — here are the dates:

| Payment | Income earned | Due date |

|---|---|---|

| Q1 | January 1 – March 31, 2026 | April 15, 2026 |

| Q2 | April 1 – May 31, 2026 | June 15, 2026 |

| Q3 | June 1 – August 31, 2026 | September 15, 2026 |

| Q4 | September 1 – December 31, 2026 | January 15, 2027 |

You avoid the underpayment penalty entirely by hitting a safe harbor: 100% of last year's total tax (110% if your AGI topped $150,000), or 90% of this year's — through any mix of quarterly payments and paycheck withholding. That last part is the shortcut many W-2-plus-side-hustle filers miss: withholding counts as paid evenly all year, so raising your day-job withholding can cover side income without you ever mailing a voucher. Details and edge cases are in quarterly estimated tax deadlines 2026.

If you've already missed a quarter or two this year, don't wait for the next deadline to "catch up evenly" — the charge accrues per quarter, so paying now stops it now. The math on what a missed quarter actually costs is in didn't pay estimated taxes penalty.

What happens if you don't save (and can't pay in April)

An unpaid side-hustle tax bill starts growing the day after the filing deadline — 0.5% per month in failure-to-pay penalty plus interest that compounds daily — before the first IRS notice even prints. From there the sequence is automated, and each stage carries more enforcement power than the last:

- April 15 passes. The failure-to-pay penalty (0.5%/month) and daily interest begin. If you didn't file at all, the failure-to-file penalty runs 5%/month — ten times worse — so file even with no money attached.

- The first bill arrives. A CP14 notice shows the balance with penalties and interest and gives you about 21 days before the next notice queues up.

- Reminder notices. CP501 and CP503 follow, each with a bigger balance. Still just bills — but the window for cheap fixes is narrowing.

- CP504 — intent to levy. The IRS can now take your state tax refund, and a federal tax lien becomes a live possibility.

- LT11 — final notice. A 30-day clock starts; after it, the IRS can levy bank accounts and garnish wages. For a self-employed person, that can mean a levy that reaches client payments too.

Along the way, any federal refund you're owed in a future year gets applied to the debt automatically. And 2026's IRS staffing cuts don't help you here: humans are harder to reach, but these notices are generated by systems that never went home. You can estimate what an unpaid balance grows into with our IRS Penalty & Interest Calculator.

Behind on side-hustle taxes already?

Whether it's last year's balance or missed quarterlies this year, an experienced tax professional can map your cheapest way out — free, before the September 15 estimated payment deadline stacks another quarter on top.

Already owe? Your realistic options

Every IRS payment program stays available for side-hustle debt — eligibility depends on the balance and your finances, not how the income was earned. The full DIY playbook lives in our guide to how to settle tax debt yourself; here's the map by option:

| Option | Who it fits | Cost and catch |

|---|---|---|

| Short-term payment plan | You can pay in full within 180 days | $0 setup; interest and the 0.5%/month penalty keep accruing until paid |

| Long-term installment agreement | Balances up to $50,000 — set up online, up to 72 months | Setup fee (reduced with direct debit or low income); interest continues |

| Guaranteed installment agreement | Balances of $10,000 or less with a clean filing history | The IRS must approve it if you meet the conditions; interest still accrues |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living costs | Collection pauses; the debt and interest remain and the IRS reviews your finances |

| Offer in Compromise | Your assets and future income genuinely can't cover the full debt | $205 fee + 20% down on lump-sum offers (both waived with low-income certification); per IRS data, the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance record for the prior 3 years | Removes penalties, not tax or interest; the new Automatic Exemption from Penalty applies automatically starting summer 2026 |

For most first-time side-hustle balances, the answer is simple: file, then set up an IRS payment plan online the same day. That single step stops the notice escalation while you fix the set-aside system so next year never repeats this one.

How to set up your side-hustle tax savings system, step by step

- Total your net profit — add up gross earnings from every app and client, subtract business expenses, and update the number monthly.

- Pick your percentage — use the table above: 20–25% in the lowest brackets, 25–30% for most W-2-plus-side-hustle filers, 30% or more at higher incomes.

- Open a separate savings account — move your percentage the same day each payout lands, before the money starts to feel spendable.

- Send quarterly payments — pay from that account through IRS Direct Pay by each estimated-tax deadline, or raise your day-job withholding to cover the gap instead.

- Recheck every quarter — income growth, a filing-status change, or a new W-4 can all move your percentage; adjust before the gap compounds.

Payments take about five minutes at IRS.gov/payments — pick "estimated tax" and the current tax year. If you prefer paper, the vouchers and worksheet are on the IRS page for Form 1040-ES.

When you can handle this yourself — and when help changes the outcome

Most side hustlers never need professional help with tax set-asides — they need a percentage, a separate account, and four calendar reminders. If you're current on filings and your only problem is that nothing's been saved yet this year, start moving 25–30% of net profit today and pay the shortfall at the next quarterly date. If you owe one year's balance and can clear it within 180 days, the $0-setup short-term plan is a ten-minute self-serve fix.

Experienced help changes the outcome in a few specific situations: multiple unfiled years (the order you file and resolve them changes what you pay), balances across several years or above $10,000, IRS notices already escalating past the reminder stage, a levy or garnishment in motion, or a divorce year where old joint debt and new separate liability are tangled together. In those cases the free review is worth the twenty minutes — the mistakes are expensive and mostly invisible until they're made.

Side-hustle tax terms, decoded

- Net profit: your side income minus business expenses — the Schedule C bottom line, and the number every percentage in this guide applies to.

- Self-employment tax: the 15.3% Social Security and Medicare tax on net earnings, computed on Schedule SE — separate from and additional to income tax.

- Safe harbor: the amount of tax you must pay during the year (100% of last year's tax, 110% at higher incomes, or 90% of this year's) to avoid the underpayment charge.

- Underpayment penalty: the interest-like charge added for each quarter you paid in less than required — it applies even if you pay in full by April 15.

- 1099-K: the payment-app and platform reporting form; for 2026 it's issued only above $20,000 and 200 transactions, but income below that is still taxable.

- QBI deduction: the qualified business income deduction, which shields up to 20% of net profit from income tax (not from self-employment tax).

Side hustle tax questions, answered

How much should I set aside for taxes on a $1,000-a-month side hustle?

Plan on $250 to $300 per month if the full $1,000 is profit. Self-employment tax takes about 14.1% of your net profit (the 15.3% rate applies to 92.35% of profit), and federal income tax at your marginal rate stacks on top of your day-job income. If expenses like mileage or supplies cut your profit to $700, save the percentage on $700 — you owe tax on net profit, not gross deposits.

Do I owe taxes on a side hustle if I made less than $600?

Yes. The $600 figure is only the threshold at which a client must send you a 1099-NEC — it is not a tax exemption. Self-employment tax applies once your net side-hustle earnings reach $400 for the year, and every dollar of profit is reportable income regardless of whether any form was issued.

Do I owe taxes if I never got a 1099-K from PayPal or Venmo?

Yes. For 2026 the 1099-K threshold is back to $20,000 and 200 transactions, so most casual sellers and gig workers won't receive one — but the income is taxable either way. The IRS can match bank deposits and platform records years later, and the resulting bill arrives with penalties and interest already attached.

Is saving 20% enough for side hustle taxes?

Only if your total household income keeps you in the lowest federal brackets. Self-employment tax alone consumes roughly 14.1% of net profit, which leaves almost nothing for income tax inside a 20% set-aside. Most people with a W-2 job in the 22% bracket or higher need 25% to 30%, plus their state's income tax rate on top.

Do I have to pay quarterly, or can I wait until April?

You can legally skip quarterly payments if enough tax is withheld from a W-2 paycheck to meet the safe harbor — 100% of last year's total tax (110% if your AGI topped $150,000) or 90% of this year's. Otherwise the IRS charges an underpayment penalty for each quarter you fall short, even if you pay in full by April 15.

Does getting divorced change how much I should save from side income?

Usually yes — often by several percentage points. Filing single or head of household compresses the tax brackets, so the same side income can land in a higher marginal rate than it did on a joint return. Your W-4 at your day job also needs updating, and last year's joint-return safe harbor number no longer maps cleanly to your new separate return.

What if I didn't save anything and now owe the IRS?

File the return anyway — the failure-to-file penalty (5% per month) is ten times the failure-to-pay penalty (0.5% per month). Then set up a payment arrangement: balances payable within 180 days qualify for a $0-setup short-term plan, and balances up to $50,000 can go on a monthly plan of up to 72 months online. Interest keeps accruing until the balance is paid.

Can business expenses lower how much I need to save?

Significantly. You save a percentage of net profit — gross income minus deductible expenses like mileage, supplies, platform fees, phone use, and home-office costs. On top of that, most side hustles qualify for the qualified business income deduction, which shields up to 20% of net profit from income tax (though not from self-employment tax).

Your next 24 hours

- Pull your year-to-date number. Open every earnings dashboard and bank account your side income touches, total the gross since January 1, and subtract expenses for a rough net profit.

- Open the account and move the money. Set up a separate savings account and transfer your percentage of everything earned so far — 25–30% for most people. What's there by September 15 is what makes the next quarterly payment painless.

- If you're already behind, get eyes on it. A balance you can't pay or unfiled years won't wait — penalties and interest accrue monthly until it's addressed. Get a free case review through the 2-minute form or at (888) 825-7779.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.