Self-Employed Tax Debt

Self-Employment Tax: What to Do When You Owe the IRS (2026)

The short answer: if you owe the IRS self-employment tax, it's the 15.3% Social Security and Medicare tax on 92.35% of your net self-employment profit — charged on top of income tax, with nothing withheld along the way. File first, then set up a payment plan; the balance grows monthly until you act.

You finished your return — or your tax software did — and the number at the bottom made you scroll back up to check for a typo. You have a mortgage, maybe a refinance in the works, and the IRS says your "self employment tax owe IRS" search result is a real, four- or five-figure debt. Here's the good news: this is the single most common tax debt in America, and every piece of it has a fix — the penalties, the balance, and the withholding gap that created it.

⏱ The real clock: there's no single notice deadline on a self-employment tax balance — the clock is the accrual. The failure-to-file penalty runs 5% per month; failure-to-pay runs 0.5% per month; interest compounds on top of both. Every month of waiting is the most expensive month yet.

Why you owe the IRS self-employment tax

Self-employment tax is 15.3% of 92.35% of your net self-employment profit — both halves of Social Security (12.4%) and Medicare (2.9%), because you're the employee and the employer. A W-2 worker sees only 7.65% leave each paycheck while the employer pays the matching half invisibly. Work for yourself and both halves arrive at once, on Schedule SE, in a lump.

Three details make the bill worse than people expect:

- It stacks on income tax. Self-employment tax and income tax are separate charges on the same profit. You do get to deduct half your SE tax before calculating income tax, but that only trims the second layer — it never touches the 15.3%.

- It applies even at low incomes. The 15.3% starts at just $400 of net self-employment earnings for the year — long before income tax kicks in. That's why a modest side hustle can produce a bill even when your bracket is low. (The 12.4% Social Security portion does stop above an annual wage-base cap; the 2.9% Medicare portion never caps, and an extra 0.9% Medicare tax applies above $200,000.)

- Nothing was withheld. No employer sent money to the Treasury during the year, and if you skipped quarterly estimated payments, the whole year's liability lands in April — usually with an underpayment charge attached. Our guide on how quarterly estimated taxes work covers the prepayment system this bill is punishing you for missing.

If this is your first year working for yourself, the shock has its own playbook — see first year self-employed and owe taxes. If it's a smaller gig on the side, side-hustle taxes and how much to save shows the set-aside math that prevents a repeat.

What happens if you ignore a self-employment tax debt

An unpaid Schedule SE balance enters the same automated collection machine as any other IRS debt — and the machine kept running even after the IRS cut roughly 27% of its workforce in 2025. Humans are harder to reach; the notices and levies are not. The sequence runs like this:

- CP14 — the first bill. It arrives weeks after you file with a balance due and gives you roughly 21 days (10 business days if the balance is $100,000 or more) to pay or arrange something before the next notice queues up.

- CP501 / CP503 — reminders. Still just bills, but the failure-to-pay penalty and daily-compounding interest are quietly growing the number on each one.

- CP504 — intent to levy your state refund. Under IRC §6331(d), the IRS can now take your state tax refund, and a federal tax lien — the thing that actually threatens a refinance — becomes a live possibility.

- LT11 / Letter 1058 — final notice. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After it expires, the IRS can levy bank accounts and, for the self-employed, send one-time levies to clients who owe you money — yes, the IRS can garnish 1099 income.

- Ongoing offsets. Every future federal refund is applied to the debt until it's gone — the IRS will take your refund every year, payment plan or not. And if multiple unpaid years stack past $66,000 (the 2026 threshold), the State Department can deny or revoke your passport.

Here's the same sequence as a rights table — what each stage means and what you still control at it:

| Stage | What it means | Your window / right |

|---|---|---|

| Return filed, balance unpaid | Penalties and interest begin accruing | Set up a plan now — cheapest moment to fix it |

| CP14 | First bill for the balance | Typically 21 days before escalation (10 business days if the balance is $100,000 or more) |

| CP501 / CP503 | Reminder notices, growing balance | All payment options still fully open |

| CP504 | IRS may seize your state refund; lien risk rises | Act before a lien is filed — critical if refinancing |

| LT11 / Letter 1058 | Final notice of intent to levy | 30 days to request a CDP hearing (Form 12153) |

| Levy stage | Bank levies (21-day hold), levies on client receivables | Release possible via agreement or hardship showing |

Staring at a self-employment tax balance you can't pay?

Penalties and interest are compounding on it every month you research alone. An experienced tax professional will review your balance free, tell you which penalties can come off, and match you to the right payment path — before the notice sequence reaches the lien stage.

Your options when you can't pay self-employment tax in full

The IRS has five real resolution paths for a self-employment tax debt, and eligibility is set by your balance and finances — not by what a sales pitch promises. The full DIY sequence for working these programs yourself lives in our guide to how to settle tax debt yourself; here's how each one applies at a typical Schedule SE balance:

| Option | Who it fits | Cost & catch |

|---|---|---|

| Pay in full | Anyone with the cash or credit at a lower rate | Stops all accrual immediately; often cheaper than any plan |

| Short-term plan (up to 180 days) | You can clear it within six months | $0 setup fee; interest and 0.5%/mo penalty continue |

| Long-term installment agreement | Balances of $50,000 or less — up to 72 months, set up online; under $10,000, the guaranteed installment agreement applies | Setup fee varies; accrual continues; keeps enforcement off |

| Currently Not Collectible | Paying anything would prevent basic living expenses — CNC works differently when you're self-employed | Collection pauses; debt and interest remain; IRS re-reviews income |

| Offer in Compromise | Assets + future income genuinely can't cover the debt — the OIC math for the self-employed counts business income and equipment | $205 fee, 20% down on lump-sum offers (both waived with low-income certification); roughly 1 in 5 offers accepted in FY2024 |

| Penalty relief | Clean prior three years (first-time abatement), or reasonable cause | Removes penalties, not tax or interest; AEP makes it automatic starting summer 2026 |

One threshold worth flagging: at $25,000 or less, a streamlined agreement on direct debit is the sweet spot — minimal paperwork, and the IRS typically does not file a federal tax lien on a balance that size when it's in a direct-debit agreement. That single fact is the difference between a refinance that closes and one that stalls. Details in our streamlined installment agreement guide.

A worked example: $19,700 of self-employment tax debt

Say your consulting business netted $86,000 last year and you made no estimated payments. The SE tax math: $86,000 × 92.35% = $79,421 of net earnings; × 15.3% ≈ $12,151 of self-employment tax. Add roughly $7,500 of federal income tax (after deducting half the SE tax and your standard deduction), and the return shows a balance right around $19,700.

At $19,700 you're under every friendly threshold: below $25,000 for a streamlined direct-debit agreement, well below the $66,000 passport line. Spread over the maximum 72 months, the base payment is about $274/month ($19,700 ÷ 72) — though interest and the 0.5% monthly penalty keep accruing, so a shorter payoff or bigger payments saves real money. You can estimate the accrual side with our IRS Penalty & Interest Calculator. And if your prior three years were clean, first-time abatement could strip the penalties off before you even start paying — shrinking the balance the interest is charged on.

How to respond when you owe self-employment tax, step by step

- Confirm the balance. Log into your IRS online account and compare it against your return. Note how much of the total is self-employment tax, how much is income tax, and how much is penalties and interest — the penalty portion may be removable.

- File every unfiled return. The failure-to-file penalty (5% per month) is ten times the failure-to-pay penalty (0.5% per month). Filing without paying immediately caps your most expensive penalty and starts your Social Security earnings credit.

- Choose your payment path. Pay in full if you can, take the free 180-day short-term plan if you're close, or set up an installment agreement online for balances of $50,000 or less — before the automated notice sequence escalates toward a lien.

- Request penalty relief. Ask for first-time penalty abatement if your prior three years were clean, and watch for the Automatic Exemption from Penalty rolling out in summer 2026. Removing penalties shrinks the balance interest is charged on.

- Close the withholding gap. Set up quarterly estimated payments — or raise a W-2 spouse's withholding — so next April's return doesn't rebuild the same debt while you're still paying off this one.

Owing the IRS while you're planning a refinance

An unpaid IRS balance does not automatically block a mortgage refinance — a filed federal tax lien usually does. Lenders care about two things: whether a lien clouds the title, and whether your IRS payment fits your debt-to-income ratio.

That means sequence matters. Set up the installment agreement before the collection notices reach the lien stage, make a few on-time payments, and bring the agreement paperwork to your loan officer up front. Many lenders will underwrite around a documented, current IRS plan; almost none will close over a recorded lien without extra steps. The rules and workarounds are covered in buying a house while owing the IRS, and if a lien has already been filed, refinancing with an IRS lien walks through subordination — the process that lets a lender jump ahead of the IRS so the loan can close.

One more refinance-specific point: don't drain the escrow or cash-out proceeds plan without checking the IRS math first. Sometimes a small cash-out at mortgage rates costs far less than years of IRS interest plus the 0.5% monthly penalty — and it clears the balance off your record entirely before underwriting ever sees a notice.

How to stop owing self-employment tax every year

A self-employment tax debt almost always repeats unless the prepayment gap is fixed, because the 15.3% applies again to every new year's profit. Three fixes, in order of reliability:

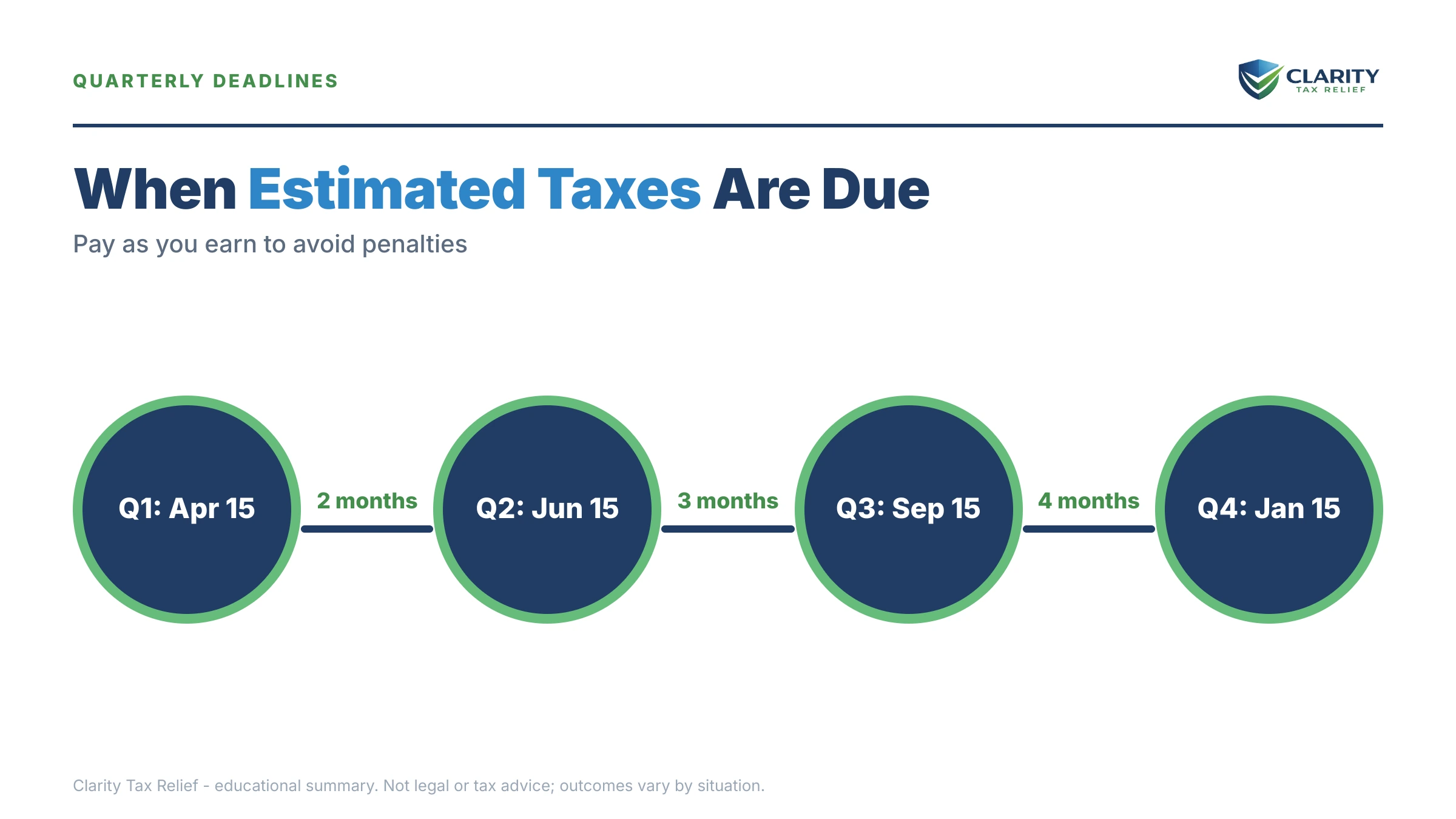

- Quarterly estimated payments. Send Form 1040-ES payments four times a year covering both SE tax and income tax. Skipping them triggers an underpayment charge on top of everything else — the math is in didn't pay estimated taxes: the penalty.

- A W-2 spouse's withholding. If you file jointly, extra withholding on your spouse's paycheck counts toward the household's total tax. Raising it via a new W-4 can cover your SE tax painlessly — withholding is treated as paid evenly through the year, which quarterlies are not.

- A real set-aside rate. Most self-employed people who land in debt saved 10% or nothing. Between SE tax and income tax, 25–30% of net profit is the realistic reserve for most earners.

Deductions matter too: SE tax is charged on net profit, so every legitimate business expense — mileage, home office, equipment, health insurance handled correctly — cuts the 15.3% directly. Cleaning up an over-reported Schedule C before resolving the debt can shrink the debt itself.

When you can handle this yourself

You likely don't need professional help if all three are true: this is one year of debt, the amount matches your own return (nobody's disputing the numbers), and the balance fits a plan you can genuinely afford. Setting up a 180-day plan or a streamlined agreement online takes under an hour, and first-time abatement is a phone call.

Experienced help tends to change the outcome when the picture is messier: multiple unfiled years (the filing order and penalty strategy affect the final number), a levy already in motion against your bank or your clients, an Offer in Compromise (where the self-employed income calculation is the most commonly botched part of the form), or an S-corp/payroll layer on top of the SE tax. And if a refinance is on a deadline, having someone who knows the lien-avoidance thresholds sequence the fix correctly is often the whole ballgame. If any of that describes you, a free case review costs nothing and tells you exactly where you stand.

Terms on your return and notices, decoded

- Schedule SE — the form attached to your 1040 that calculates the 15.3% self-employment tax on your net profit.

- SECA — the Self-Employment Contributions Act, the law behind SE tax; it's the self-employed twin of the FICA tax withheld from W-2 paychecks.

- Net earnings from self-employment — your profit after business expenses, multiplied by 92.35%; the base the 15.3% is charged on.

- Estimated tax (Form 1040-ES) — the quarterly prepayments the self-employed make in place of withholding; the missing piece behind most SE tax debts.

- Failure-to-pay penalty — 0.5% of the unpaid tax per month, capped over time, charged alongside interest until the balance is paid.

- CSED — the Collection Statute Expiration Date: the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

Self-employment tax debt questions, answered

Why do I owe so much in self-employment tax?

Because you pay both halves of Social Security and Medicare — 15.3% on 92.35% of your net self-employment profit — and no employer withheld anything along the way. A W-2 worker only sees 7.65% come out of each check; the employer quietly pays the other half. When you work for yourself, both halves land on your return at once, stacked on top of ordinary income tax.

Do I pay self-employment tax on top of regular income tax?

Yes — they are two separate taxes on the same profit. Self-employment tax funds Social Security and Medicare at 15.3%, while income tax applies at your bracket rate on top of it. One partial offset: you deduct half of your self-employment tax when calculating your income tax, which softens the second layer but never touches the first.

What if I owe self-employment tax and can't pay it?

File the return anyway — the failure-to-file penalty runs 5% per month versus 0.5% per month for failure-to-pay, so filing without payment cuts your penalty exposure roughly tenfold. Then pick a resolution: a 180-day short-term plan with no setup fee, an installment agreement of up to 72 months for balances of $50,000 or less, hardship status, or in genuinely limited-finances cases an Offer in Compromise.

Do I owe self-employment tax if I made less than $400?

No — self-employment tax only applies once your net earnings from self-employment reach $400 for the year. Below that line, Schedule SE isn't required. Two cautions: the $400 test uses net profit across all your self-employment activities combined, not per gig, and income under $400 can still owe ordinary income tax even though it escapes the 15.3%.

Will owing self-employment tax stop me from refinancing my house?

Usually not by itself — the real refinance killer is a filed federal tax lien, not the balance. Many lenders will close with an unpaid IRS balance if you have an installment agreement in place and can document on-time payments. Get the agreement set up before the IRS notice sequence reaches the lien stage, and tell your loan officer about it early rather than hoping it stays invisible.

Will the IRS take my refund if I owe self-employment tax?

Yes. Any federal refund you're due in a later year is automatically applied to the unpaid balance, even while you're current on a payment plan. That continues every filing season until the debt is gone. If your household counts on that refund, adjust a spouse's W-4 withholding or your estimated payments now so you're not lending the IRS money it will keep anyway.

Does paying self-employment tax count toward Social Security?

Yes — the net earnings you report on Schedule SE are what earn you Social Security credits toward retirement and disability benefits. That's a real reason to file even in a bad year. Skip filing, and the year contributes nothing to your earnings record; if the IRS later files a substitute return for you, it can assess the tax without properly crediting your Social Security account until you file your own return.

Can penalties on self-employment tax debt be removed?

Often, yes. If your prior three years were clean, first-time penalty abatement can wipe the failure-to-file and failure-to-pay penalties for one year — and starting in summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies similar relief automatically, with no request needed. Interest on the tax itself, though, generally cannot be waived; it only stops growing when the balance is paid.

Your next 24 hours

- Pull the numbers apart. Open your return and find Schedule SE. Write down three figures: the self-employment tax, the income tax, and (from your IRS online account) any penalties and interest already added. The penalty piece may be removable.

- Gather the file. Last year's return, every 1099 you received, and a rough monthly income-and-expense picture for the business. That's everything needed to pick the right plan — and everything a lender will eventually ask about too.

- Get the free case review. Interest and the monthly penalty compound whether you decide this week or this year — and if a refinance is coming, the order you fix things in matters. Call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map your options at no cost.

Primary sources: the IRS's own overview of self-employment tax (Social Security and Medicare taxes), current payment options at IRS.gov/payments, and independent taxpayer-rights help at the Taxpayer Advocate Service.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.