Gig Economy Tax Debt

Uber Driver Back Taxes: What You Owe and How to Fix It (2026)

The short answer: Uber driver back taxes usually come from 1099 income with no withholding — 15.3% self-employment tax plus income tax you never set aside. Most balances under $10,000 qualify for a guaranteed installment agreement, mileage deductions can shrink the assessed amount, and penalties can often be reduced. Interest compounds monthly until you act.

Maybe it started with an IRS letter listing income Uber reported that you never put on a return. Maybe you filed, saw the number, and couldn't pay it. Either way, you drove those hours, you spent most of what you earned on gas and the car, and now the IRS wants a chunk you don't have. Here's the part that matters: rideshare tax debt is one of the most fixable kinds there is — because the IRS's number for a driver is almost always too high, and the law gives you specific tools to correct it before you pay a dime.

The core problem with Uber driver back taxes is unique to rideshare: Uber's Form 1099-K reports gross fares — what riders paid, not what you received — so an IRS bill built from that form ignores Uber's cut and every mile you drove. The image below shows exactly what these documents look like and where the gross-fares number that drives your balance appears, so you can compare it against what actually hit your bank account.

⏱ The clock that's running: there's no single statutory deadline on old rideshare tax debt — but the failure-to-file penalty adds 5% per month (up to 25%) on unfiled years, the failure-to-pay penalty adds another 0.5% per month, and interest compounds on top of both. If you're holding a specific IRS notice, the response date printed on it controls — find it before you do anything else.

Why Uber drivers end up owing back taxes

Uber drivers owe back taxes because the IRS treats every driver as a self-employed business owner — with 15.3% self-employment tax on net profit and zero withholding along the way. Nobody at Uber takes taxes out of your weekly payout. The full bill lands at filing time, and if you didn't set money aside, it lands as debt.

Three forces stack the deck against drivers:

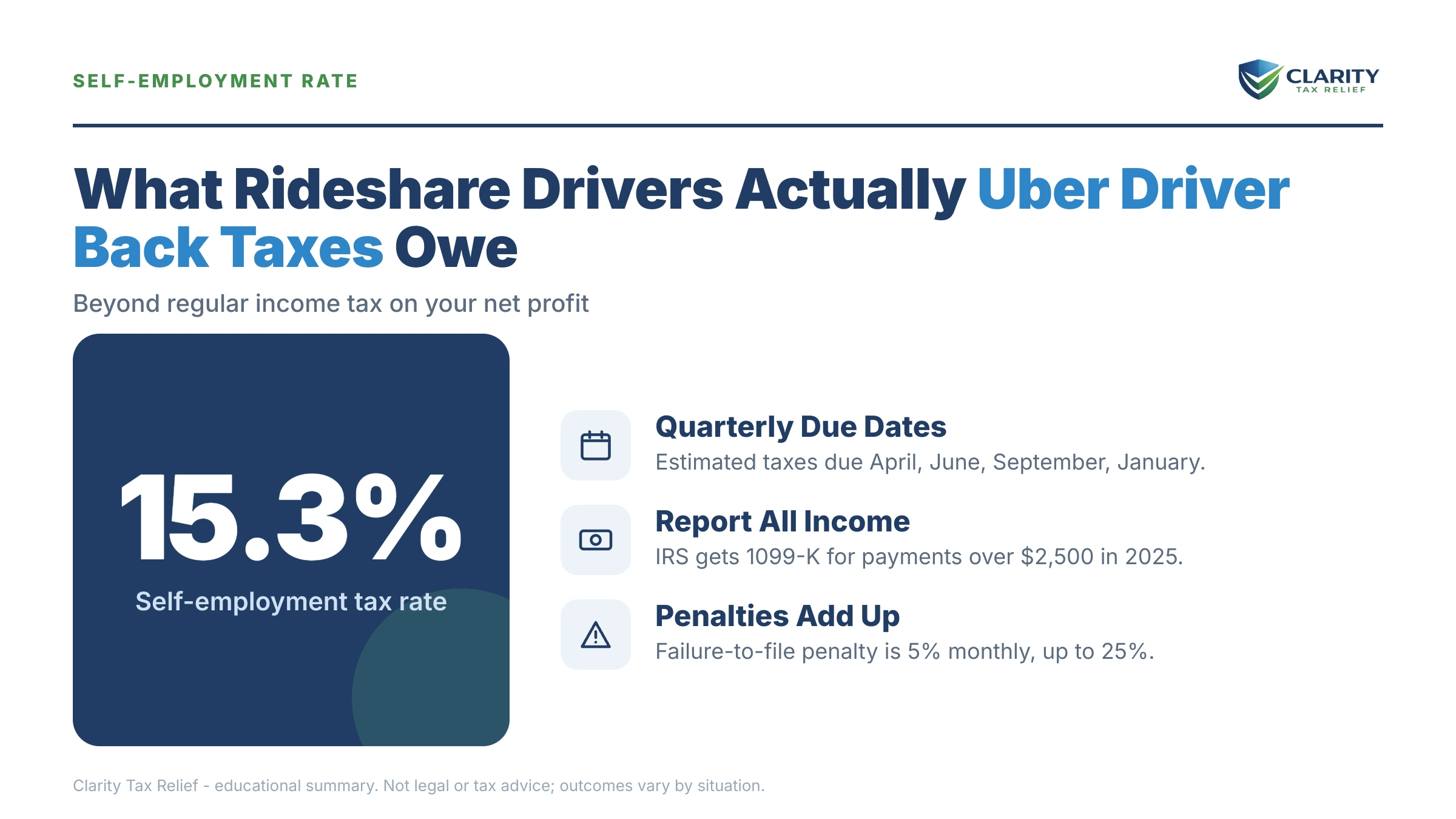

- Self-employment tax comes first. Before you owe a dollar of income tax, you owe 15.3% of your net driving profit for Social Security and Medicare — both halves, since you're the employer and the employee. Once net profit passes $400, that tax applies. Our guide to the self-employment tax shock walks through why this number surprises almost everyone.

- A W-2 day job makes it worse, not better. If you drive nights and weekends around a regular job, your Uber profit stacks on top of your salary and gets taxed at your highest bracket. Your paycheck withholding was calibrated for your wages alone — it covers none of the driving income.

- The IRS already has Uber's numbers. Uber files its 1099-K and 1099-NEC directly with the IRS. A computer matches those forms against your return. If you skipped the income — or skipped filing entirely — the mismatch generates an automated notice, no human required.

None of this makes you a tax cheat. It makes you one of hundreds of thousands of drivers who found out after the fact that gig pay is pre-tax pay. What separates a manageable fix from a five-figure mess is what you do next — and whether you let the IRS's inflated version of your income stand.

Why the IRS thinks you earned more than you did

An IRS balance built from Uber's 1099-K overstates a driver's real income, because the form reports gross fares before Uber's service fees and before any vehicle expenses. Your job — whether you're filing late, answering a notice, or challenging an assessment — is to get from the gross number down to your actual profit.

| Document | What it reports | When it's issued | The trap |

|---|---|---|---|

| Form 1099-K | Gross rider payments — fares before Uber's fees and commissions | Over $20,000 and 200+ transactions (federal, 2026); some states set lower thresholds | The number is bigger than your bank deposits — often by thousands. The IRS matches against this figure. |

| Form 1099-NEC | Bonuses, referral payments, promotions, quests | $600 or more | Easy to forget alongside the 1099-K — a second matching document the IRS also has. |

| Uber Tax Summary | Gross fares, Uber's fees itemized, and your on-trip miles | Every driver, every year — regardless of 1099 thresholds | Not sent to the IRS at all. It's the single best evidence for your deductions, and most drivers never open it. |

Two deductions do most of the work of closing the gap. First, Uber's own fees and commissions are a deductible business expense — the difference between the 1099-K and your deposits. Second, the standard mileage deduction, which for high-mileage drivers is frequently the largest single number on the whole Schedule C. Even if you never kept a log, Uber's Tax Summary records your on-trip miles, and business miles between trips can often be reconstructed — see our guide to rescuing deductions when you didn't track miles.

One more 2026 wrinkle: the federal 1099-K $20,000 threshold is back after the $600 rule died. That changes which drivers get the form going forward — it does nothing for tax already owed from earlier years, and it never changed what's legally taxable.

What happens if you ignore Uber back taxes

Unpaid rideshare tax debt moves through an automated IRS collection sequence that ends at your bank account, your refunds, and your Uber payouts. The 2026 IRS is harder to reach by phone than it's been in decades — the workforce shrank roughly 27% in 2025 — but the notice-and-levy machinery is software, and it never stopped running. Here's the sequence for a driver:

- The computer flags the gap. Document matching compares Uber's 1099s to your return. Underreported income triggers a CP2000 notice proposing extra tax — computed on gross fares, with no expenses. If you never filed, a CP59 non-filer notice starts the same clock.

- The proposal becomes a legal assessment. Ignore the CP2000 and a CP3219A Notice of Deficiency follows, giving you 90 days to petition Tax Court. Ignore a non-filer notice and the IRS can eventually file a Substitute for Return — a return it prepares for you using the gross 1099-K, single, no deductions, no mileage.

- The bills start: CP14, then CP501 and CP503. Once assessed, the balance is a legal debt. The first bill typically gives about 21 days; the reminders that follow just add interest and urgency.

- CP504 — the IRS can take your state tax refund. This intent-to-levy notice under IRC §6331(d) authorizes seizure of state refunds and signals a federal tax lien is on the table.

- LT11 or Letter 1058 — the final notice. A 30-day clock starts. You can demand a Collection Due Process hearing with Form 12153; let the window pass and you lose that appeal right while the IRS gains full levy power.

- Levies begin. A bank levy freezes funds for a 21-day hold before they're sent to the Treasury. The IRS can also serve a levy on Uber itself, intercepting payouts due to you, and it will keep every federal tax refund you're owed until the debt is gone. Drivers whose combined balances cross $66,000 (the 2026 threshold) also face passport certification.

Each stage strips away an option you had at the stage before. This table shows the rights on the line at each notice:

| Notice | Your window | What passes with the deadline |

|---|---|---|

| CP2000 | Date printed on the notice (typically about 30 days) | The easy chance to substitute your real mileage and fees before tax is assessed |

| CP3219A | 90 days to petition Tax Court | Your only chance to dispute the amount in court before paying it |

| CP14 | Pay-by date on the notice (typically about 21 days) | The pre-escalation window — cheapest moment to set up a plan |

| CP504 | 30 days | Your state tax refund becomes seizable; lien filing becomes likely |

| LT11 / Letter 1058 | 30 days to file Form 12153 | Your Collection Due Process hearing — the strongest appeal right in collections |

Meanwhile the balance itself grows every month. You can estimate what penalties and interest have already added to your driving debt with our IRS Penalty & Interest Calculator. One quiet upside: the collection statute gives the IRS 10 years from assessment to collect — but appeals, offers, and bankruptcy pause that clock, so "wait it out" is rarely a real strategy for a working driver.

Holding an IRS notice about your Uber income?

Send it to us before the balance is set in stone. An experienced tax professional will check whether the IRS computed your debt on gross fares — and map the cheapest way out. Free, confidential, no pressure: (888) 825-7779 or the 2-minute form.

How to resolve Uber driver back taxes: every option compared

Every IRS resolution program is means-tested — which one fits depends on your balance, your filing status with the IRS, and your real monthly budget. The shared mechanics of these programs are covered in our pillar on how to settle tax debt yourself; here's how each maps to a rideshare debt:

| Option | Who may qualify | Cost & terms | Driver notes |

|---|---|---|---|

| Short-term payment plan | Can pay in full within 180 days | $0 setup; interest and penalties continue | Good if a busy season or a W-2 bonus will cover the balance |

| Guaranteed installment agreement | Individuals only; income-tax balance of $10,000 or less (excluding penalties and interest); all returns filed; filed and paid on time for the past 5 years with no installment agreement in that period; full pay within 3 years | Setup fee applies; no financial disclosure | The default answer for most single-year rideshare debts |

| Streamlined installment agreement | Up to $25,000 — or up to $50,000 with direct debit | Up to 72 months, set up online, no detailed financials | Fits multi-year driver debts; direct debit cuts the setup fee |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living expenses (Form 433-F) | $0; collection pauses, debt and interest remain | Realistic when driving income has collapsed or expenses eat everything |

| Offer in Compromise | IRS math shows it can't collect the full amount from your income and assets | $205 fee; 20% down on lump-sum offers; both waived with low-income certification (AGI ≤ 250% of poverty) | Accepted roughly 1 in 5 times in FY2024 — real, but never a given; deemed accepted if the IRS doesn't decide within 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count |

| Penalty abatement | Clean compliance for the prior 3 years (first-time), or reasonable cause | Free to request; removes penalties, not tax or interest | Stacks with any option above — always check this first |

Two details drivers routinely miss. First, no payment plan can be approved until all required returns are filed — the IRS won't negotiate with a non-filer, so unfiled years come first no matter what. Second, penalty relief is nearly free money: first-time penalty abatement can erase failure-to-file and failure-to-pay penalties for one year if your prior three years are clean, and starting summer 2026 the IRS's new Automatic Exemption from Penalty (AEP) begins applying similar relief automatically, no request needed. Ask anyway — don't assume the automation caught your year.

On every plan, interest keeps accruing until the balance hits zero, though the failure-to-pay penalty rate is cut in half while an approved installment agreement is active. Paying a plan off early always saves money; there's no prepayment penalty.

What a $4,800 Uber tax debt actually costs — a worked example

Say you owe $4,800 from one year of side-driving — you're single, you have a W-2 day job, and the IRS assessed the balance after matching Uber's forms. Everything here is hypothetical, but the arithmetic is real. Two paths:

Path 1 — the number is right, you just can't pay it. At $4,800 you're under the $10,000 line for a guaranteed installment agreement — available to individuals whose income-tax balance is $10,000 or less (excluding penalties and interest), who have filed all required returns, who filed and paid on time for the past 5 years with no installment agreement in that period, and who can pay in full within 3 years; no financial disclosure required. That's $4,800 ÷ 36 = about $134 per month — a Friday night of driving. Interest and a reduced failure-to-pay penalty keep accruing on the shrinking balance, so paying $200 or $250 a month instead retires the debt faster and cheaper.

Path 2 — the number was built on gross fares. Suppose the IRS computed that $4,800 from a 1099-K showing $21,400 in gross fares — but Uber's Tax Summary shows $5,600 of Uber fees and 9,500 on-trip miles. Those miles at the standard mileage rate (70 cents per mile for 2025) are a $6,650 deduction. Combined, that's $12,250 of deductions the IRS's computation ignored, dropping your real net profit to about $9,150. At a side-driver's combined marginal rate — roughly 22% income tax plus an effective ~14% self-employment tax — each $1,000 of missed deductions represents about $360 of tax. Run the recomputation and most of that $4,800 can evaporate before you ever discuss a payment plan, with penalties recalculated on the smaller number too.

That's the whole strategy for rideshare debt in one example: fix the number first, then pay the number. Drivers who jump straight to a payment plan on an inflated assessment lock in years of payments on tax they never legally owed.

How to respond to Uber driver back taxes, step by step

- Pull your IRS and Uber records. Log into your IRS online account, request wage and income transcripts for every open year, and download Uber's annual Tax Summary from the driver dashboard.

- File or fix every open return. File missing years with a complete Schedule C, respond to any CP2000 with corrected figures, and request reconsideration on substitute-for-return years using your real mileage and fees.

- Shrink the balance before you agree to pay it. Claim Uber's service fees and your reconstructed mileage, then request first-time penalty abatement if your prior three years are clean.

- Choose a payment path that fits the final number. Under $10,000 usually means a guaranteed installment agreement; up to 180 days of breathing room costs nothing to set up; genuine hardship points to Currently Not Collectible or an Offer in Compromise.

- Set up quarterly estimates for this year. Put 25–30% of each week's net rideshare pay aside and pay quarterly so next April doesn't restart the cycle.

- Escalate to an experienced tax professional if it's bigger than DIY. Multiple unfiled years, a levy notice already in motion, or a CP2000 built on gross fares are the situations where representation changes the outcome.

What if you never filed for your Uber years at all?

Unfiled rideshare years are worse than unpaid ones — because the failure-to-file penalty (5% per month) runs ten times the failure-to-pay penalty (0.5%), and because the IRS may eventually file the return for you. That Substitute for Return uses the gross 1099-K, single filing status, and zero deductions: the worst legal version of your year. If that already happened, filing your own accurate return generally replaces the SFR's inflated assessment — our guide to what happens when the IRS filed a substitute return covers the reconsideration process.

If you're several years behind, you almost never need to file everything since you started driving. IRS policy generally requires the most recent six years to get back into compliance — the details are in how many years of back taxes you have to file. And one old-year deadline cuts the other way: refunds expire three years after the return was due, so a driver with heavy mileage in an old unfiled year may be leaving a refund on the table that vanishes if they keep waiting.

Situations that change the playbook

Most side-drivers fit the worked example above, but three variations change the math enough to plan around:

- You drive on multiple apps. Uber, Lyft, and delivery platforms each file their own 1099s, and the IRS matches all of them. Resolve every platform's income in the same set of returns — a plan built around one app's forms defaults the moment the next mismatch is assessed. The mechanics for the other major platform are in our guide to Lyft driver back taxes; full-time drivers who own their vehicle as a business should compare the owner-operator truck driver back taxes playbook, where depreciation and per-mile economics dominate.

- You formed an LLC for your driving. A single-member LLC is disregarded for income tax — the debt is still personally yours, on your Schedule C, and an LLC offers no shield from it. How entity choice actually affects exposure is covered in sole proprietorship vs LLC taxes.

- Your state wants its cut too. If you drove in a state with an income tax, an IRS assessment usually triggers a matching state bill on the same income. State agencies run their own programs and timelines — and the IRS can seize your state refund via a CP504 while you're sorting it out — so sequence both debts deliberately rather than fixing one and getting blindsided by the other.

Stop next year's bill while you fix this one

A resolution plan only works if you don't create a new debt on top of it — and a new unpaid year can default an existing installment agreement. Going forward, treat roughly 25–30% of your net weekly rideshare pay as the government's money: move it to a separate account, and send it in as quarterly estimated payments. The full system — safe-harbor rules, due dates, and how to compute the payments — is in how quarterly estimated taxes work. If you have a W-2 day job, there's an even simpler lever: increase the extra withholding on your W-4 so your paycheck covers the driving tax automatically. The IRS's own Gig Economy Tax Center is the primary-source reference for what platforms report and what drivers owe.

When you can handle this yourself — and when help changes the outcome

Plenty of Uber back-tax situations are genuinely DIY. Handle it yourself if:

- You owe a single year, the amount matches your own math, and it's under $10,000 — set up the guaranteed installment agreement online at the IRS payment plans page and be done.

- You can pay in full within 180 days — the short-term plan costs nothing to set up.

- You got one CP2000, you have your Uber Tax Summary, and the fix is simply reporting your fees and mileage — a careful written response handles it.

Experienced help earns its cost when the situation compounds: multiple unfiled years, an SFR assessment built on gross fares, a CP2000 you dispute, an LT11 with the 30-day CDP clock running, a levy already hitting your bank or your Uber payouts, or a balance large enough that Offer in Compromise math is worth running properly. In those cases, the order of operations — returns first, then penalty relief, then the payment structure — often changes the final cost by more than the fee, and a professional can invoke rights (audit reconsideration, CDP hearings, hardship releases) that the notices never mention. Be equally skeptical of anyone promising a specific settlement before seeing your transcripts; eligibility for every program is means-tested.

If your driving debt spans multiple years or a levy notice has already arrived, get a free rideshare-specific case review at the 2-minute form or (888) 825-7779 before the balance grows another month.

Terms on your notices, decoded

- 1099-K — the form Uber files reporting gross rider payments processed for you, before Uber's fees came out.

- Schedule C — the tax form where your driving becomes a business: income minus fees, mileage, and expenses equals the profit you're actually taxed on.

- Self-employment tax — the 15.3% Social Security and Medicare tax on net profit that no one withheld from your payouts.

- Substitute for Return (SFR) — a return the IRS prepares for a non-filer using gross 1099 figures and no deductions; replaceable by filing your own accurate return.

- CP2000 — the automated notice proposing extra tax when Uber's forms don't match your return; a proposal you can correct, not a final bill.

- CSED — the Collection Statute Expiration Date: the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

Uber back-tax questions, answered

Why do Uber drivers owe so much in back taxes?

Because nothing is withheld from rideshare pay: you owe 15.3% self-employment tax on net profit plus regular income tax, and the IRS matches Uber's 1099-K and 1099-NEC against your return. A driver who nets $15,000 and reports nothing can owe roughly $5,000–$6,000 for that one year before penalties. The bill gets worse when the IRS computes it from gross fares with no mileage deduction.

Why is my Uber 1099-K higher than what Uber actually paid me?

The 1099-K reports gross fares — the full amount riders paid, before Uber subtracted its service fees and commissions. Your bank deposits are the net figure, so the 1099-K can run thousands of dollars higher than what you actually received. Uber's fees are a deductible business expense on Schedule C, but only if you (or whoever responds to the IRS) actually claim them.

Can I still claim mileage if I didn't track my miles?

Usually, yes — you can reconstruct a reasonable mileage log rather than forfeit the deduction. Uber's annual Tax Summary shows your on-trip miles, and app history, trip records, and maintenance receipts can support additional business miles driven between rides. The IRS wants a credible reconstruction backed by records, not perfection — and mileage is usually the single biggest number standing between a rideshare driver and a smaller balance.

Can the IRS take my Uber earnings for back taxes?

Yes. The IRS can serve a levy on Uber that captures payments owed to you, levy your bank account (funds are held 21 days before they're sent to the IRS), and keep your tax refunds every year until the debt is paid. Because levies on contractor pay are typically one-time grabs rather than continuous, timing matters — but any levy notice means you should act immediately.

How many years of Uber taxes do I have to file?

IRS policy generally requires the last six years of returns to get back into filing compliance, though it can ask for more in unusual cases. If the IRS already filed substitute returns for missing years, filing your own accurate returns — with mileage and Uber's fees deducted — usually replaces those inflated assessments. Start with the oldest year the IRS is actively pursuing.

Does the $600 1099-K rule still apply to Uber drivers?

No — the federal 1099-K threshold reverted to $20,000 and 200 transactions for 2026. But that only changes the paperwork, not the law: you owe self-employment tax once net rideshare profit passes $400, and income tax applies whether or not a form was issued. Back taxes from earlier years don't disappear because the reporting threshold moved, and some states keep lower 1099-K thresholds of their own.

Can Uber back taxes be settled for less than I owe?

Sometimes — through an Offer in Compromise — but only when the IRS's own math shows it could never collect the full balance from your income and assets before the collection statute expires. The application costs $205 (waived with low-income certification), lump-sum offers require 20% down, and the IRS accepted roughly one in five offers in FY2024. For a typical few-thousand-dollar rideshare debt, a payment plan is usually faster and cheaper.

Will I go to jail for not filing taxes on Uber income?

Almost certainly not — unpaid tax debt is a civil matter, and the IRS's remedies are penalties, liens, and levies, not arrest. Criminal exposure exists only for willful evasion or fraud, which requires far more than falling behind on gig-work filings. Voluntarily filing before the IRS forces the issue is the strongest protection you have.

Do I owe taxes on Uber income if I already have a W-2 job?

Yes — your day job's withholding covers only your W-2 wages, not your rideshare profit. Uber income lands on top of your salary, taxed at your highest bracket plus 15.3% self-employment tax, which is why side-drivers are so often shocked at filing time. Adjusting your W-4 to withhold extra, or paying quarterly estimates, prevents the same bill from repeating next year.

Your next 24 hours

- Find the controlling number and date. Pull out any IRS notice and locate the amount claimed and the response date printed on it — then log into your account at IRS.gov to see every year with a balance.

- Download your Uber Tax Summaries. Grab the Tax Summary for every year in question from the driver dashboard — the fees and on-trip miles on those pages are the raw material for shrinking your balance.

- Get the numbers checked before you commit to anything. A free case review at the 2-minute form or (888) 825-7779 will tell you whether your assessment was built on gross fares — while penalties and interest are still compounding on the current balance, every month you wait costs real money.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.