Self-Employed & 1099 Tax Debt

Real Estate Agent Back Taxes: How to Fix IRS Debt From Commission Income (2026)

The short answer: real estate agent back taxes almost always start the same way — commissions paid on Form 1099-NEC with zero withholding, plus 15.3% self-employment tax nobody budgeted for. The fix is a sequence: file every missing return with your real deductions, then match the balance to a payment plan, hardship status, or Offer in Compromise.

You had a strong stretch — the closings were real, the checks cleared, the splits got paid. But somewhere between showings and inspection deadlines, the quarterly tax payments never happened, and now the IRS envelopes are stacking up next to your CE certificates. Here's what matters most: agent tax debt is one of the most fixable kinds there is, because most agent balances are inflated by unclaimed deductions and removable penalties. This guide is the map — including the trap that makes many agents owe far more on paper than they actually should.

⏱ The clocks already running: back taxes carry no single notice deadline, but the failure-to-pay penalty adds 0.5% of your balance every month, and interest compounds daily on top of it. And once seriously delinquent debt reaches $66,000 (the 2026 threshold), the IRS can certify you to the State Department for passport denial or revocation.

Why real estate agents fall behind on taxes

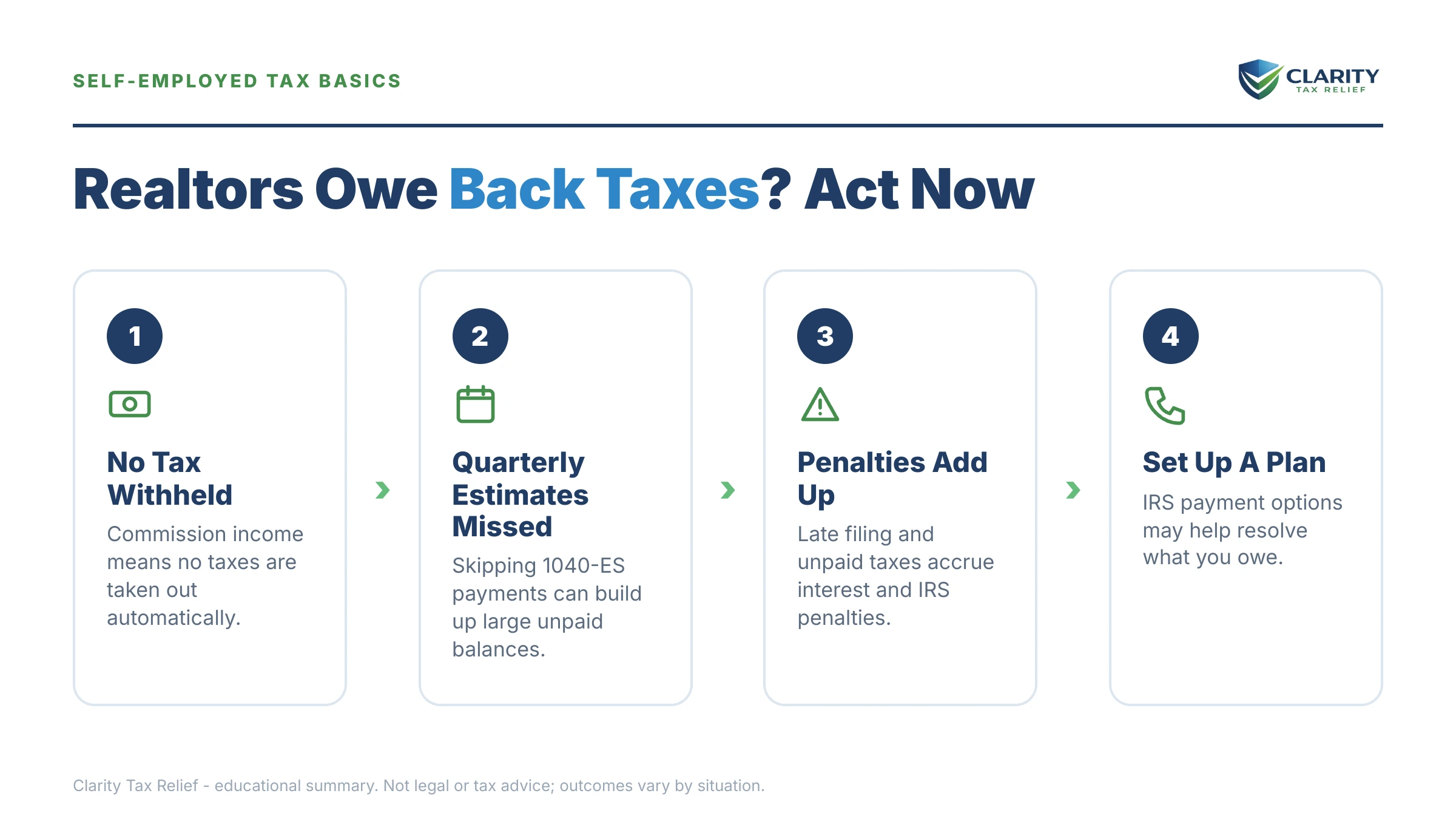

Real estate agents are 1099 independent contractors, which means every commission check arrives with $0 withheld for taxes. Your broker reports what it paid you on Form 1099-NEC, sends a copy to the IRS, and the entire tax burden — federal income tax plus both halves of Social Security and Medicare — lands on you at filing time.

That second piece is the one that blindsides new agents: self-employment tax runs 15.3% on your net commission income before income tax even starts. Between the two, many agents owe an effective 25–40% of net income — money that was supposed to be set aside from checks that felt like pure profit.

Three structural features of the business make it worse:

- Lumpy income vs. rigid deadlines. The IRS wants estimated payments four times a year on a fixed calendar. Your income arrives in bursts — three closings in May, nothing until September. Agents who didn't pay estimated taxes get hit with an underpayment penalty on top of the balance itself.

- High, scattered expenses. Mileage, MLS dues, staging, photography, desk fees, E&O insurance — the deductions are real but spread across a dozen cards and accounts. When records are messy, agents either overpay or stop filing entirely.

- Market whiplash. A big year sets a big tax bill due the following April — often right when rates rise and the pipeline dries up. The tax on last year's boom comes due during this year's drought.

None of this is a character flaw. It's a payment system designed for W-2 employees colliding with a commission business. But the IRS computer matching your broker's 1099-NEC filings against your returns doesn't grade on intent — it just escalates.

Unfiled years: the substitute-return trap that inflates agent balances

When a real estate agent doesn't file, the IRS eventually files for them — a Substitute for Return built on the gross 1099 amount with zero business deductions. No mileage. No brokerage splits beyond what the 1099 already reflects. No MLS dues, no marketing, no E&O insurance, and the least favorable filing status. If the IRS filed a substitute return for you, the balance on your notices may be dramatically higher than what you'd owe on an accurate return.

This is why filing your own back-year returns is step one even when you can't pay a cent: an original return with real Schedule C deductions typically replaces the SFR and shrinks the assessment, and the IRS won't approve any payment plan or settlement while required returns are missing. As a general rule, getting your last six years filed restores filing compliance for resolution purposes.

Lost your records? Most agent deductions can be reconstructed from sources you still have — see the table below, and the full guide to filing back taxes without records.

| Expense category | Common examples | Reconstruction source |

|---|---|---|

| Vehicle / mileage | Showings, listing appointments, closings, caravan tours | MLS showing history, calendar apps, lockbox access logs |

| Dues & licensing | MLS fees, board/association dues, license renewal, CE courses | Board and MLS billing records, state license portal |

| Marketing | Signs, photography, staging, online ads, open-house costs | Card statements, vendor invoices, ad-platform histories |

| Brokerage costs | Desk fees, transaction fees, E&O insurance, franchise fees | Broker's commission ledger and year-end statements |

| Office & technology | Home office, CRM software, e-signature tools, phone, Supra key | Subscription receipts, phone bills, bank statements |

| Client & referral costs | Referral fees paid, closing gifts (capped at $25 per recipient) | Settlement statements, referral agreements, gift receipts |

What happens if you ignore real estate agent back taxes

IRS collection on a 1099 agent runs on an automated notice sequence that ends with levies on your bank account and your commission pipeline. In 2026 the IRS workforce is down roughly 27% from 2025 cuts — humans are harder to reach, but the notice-and-levy machine is fully automated and never stopped. The stages arrive in this order:

- CP14 — the first bill. The IRS assessed a balance (from your return, an SFR, or a CP2000 underreporter match). You typically have about 21 days from the notice date before the sequence advances — 10 business days if the balance is $100,000 or more. No enforcement yet — this is the cheapest moment to act.

- CP501 / CP503 — automated reminders. Still just bills, but the balance grows every month they sit unanswered.

- CP504 — intent to levy your state refund. Under IRC §6331(d), the IRS can now seize your state tax refund, and a federal tax lien filing becomes a live possibility. A lien attaches to everything you own — including any real estate in your own name.

- LT11 / Letter 1058 — final notice of intent to levy. This starts a 30-day clock and your Collection Due Process rights (requested on Form 12153). After 30 days, the IRS can levy your bank accounts and serve levies on your broker.

- Active enforcement. A bank levy freezes funds for a 21-day hold before the money leaves. An IRS levy on commission income served on your brokerage grabs whatever the broker holds or owes you when it lands — and the IRS can serve fresh levies deal after deal. The rules for how far a levy reaches into contractor pay are covered in can the IRS garnish 1099 income.

- Passport certification. Once seriously delinquent debt reaches $66,000 in 2026, the IRS can issue a CP508C and certify you to the State Department — a real problem for agents with international clients or travel plans. Details in passport revoked for tax debt.

| Notice | What it does | Your window |

|---|---|---|

| CP14 | First bill for the assessed balance | Typically 21 days from the notice date (10 business days if the balance is $100,000 or more) |

| CP501 / CP503 | Automated reminder notices; balance keeps growing | The pay-by date printed on each notice |

| CP504 | Intent to levy your state tax refund (IRC §6331(d)); lien filing likely next | The date printed on the notice |

| LT11 / Letter 1058 | Final notice of intent to levy — bank accounts and broker-held commissions | 30 days to request a CDP hearing (Form 12153) |

| CP508C | Passport certification once debt is seriously delinquent | Triggered at $66,000+ (2026); reversed by entering a qualifying resolution |

One more clock runs in your favor: the IRS generally has 10 years from assessment to collect (the CSED), though appeals, an Offer in Compromise, or bankruptcy pause it. For most working agents, though, a decade of levy exposure on every commission is not a survivable waiting game — resolution is.

Behind on taxes from your commission income?

Whether it's one bad year or five unfiled ones, an experienced tax professional can pull your IRS transcripts, find the deductions the IRS didn't give you, and map the resolution that fits — free and confidential, before penalties and interest add another month to the balance.

Your options for resolving back taxes as a real estate agent

The IRS has six real resolution paths, and eligibility turns mostly on how much you owe and what your finances show. The full DIY playbook for each program lives in our guide to how to settle tax debt yourself — here's how each one applies to commission income specifically:

| Option | Who typically qualifies | Cost to set up | The catch for agents |

|---|---|---|---|

| Short-term payment plan | Any balance you can clear within 180 days | $0 setup fee | Penalties and interest keep accruing until paid |

| Streamlined installment agreement | Total debt ≤ $50,000, all returns filed | Setup fee (reduced with direct debit; waived for low income) | Up to 72 months online — pick a payment a slow quarter can carry |

| Non-streamlined installment agreement | Debt over $50,000 | Setup fee + financial disclosure (Form 433-F) | IRS sets the payment from your financials; lien filing is likely |

| Currently Not Collectible | Income barely covers IRS-allowed living expenses | $0 | Reviewed when income rises — one big closing can end it |

| Offer in Compromise | Assets + future income can't cover the debt before the CSED | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Roughly 1 in 5 offers accepted in FY2024; income averaging punishes rebound years |

| Penalty abatement (FTA / AEP) | Clean compliance history in the prior 3 years | $0 | Removes penalties, not tax — but interest on abated penalties drops too |

Payment plans are where most agents land. Under $50,000 total, a streamlined agreement can be set up online in minutes with no financial disclosure, spread over up to 72 months. Above $50,000, the IRS wants a Form 433-F financial statement and will size the payment itself — the terrain covered in IRS payment plan over $50,000. Under $10,000, a guaranteed installment agreement is available if you meet the conditions. On any plan, interest and the 0.5% monthly penalty keep running until the balance hits zero, so overpaying in good months genuinely saves money.

Currently Not Collectible fits agents in a genuinely dead market: if your commission income can't cover IRS-allowed living expenses, collection pauses — no levies, no payment — while the debt sits (and the 10-year collection clock keeps running). The trade-off is instability: the IRS reviews CNC accounts, and a strong quarter can reactivate collection.

An Offer in Compromise (Form 656) settles the debt for less than the full balance — but only when the IRS's own math says you can't pay in full before the statute expires. Variable commission income makes this math tricky in both directions: a documented multi-year downturn helps, while a single bad year sandwiched between strong ones usually doesn't, because the IRS averages income when projecting what it can collect. Self-employed offers have their own quirks — business assets, gross-vs-net income disputes — detailed in our guide to the OIC for the self-employed. One honest benchmark: the IRS accepted roughly 1 in 5 offers in FY2024. Anyone promising you a settled-for-a-fraction outcome before seeing your financials is selling, not advising.

Penalty relief is the most overlooked lever. If the prior three years were clean, first-time penalty abatement can wipe an entire year's failure-to-file and failure-to-pay penalties with one request — and starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies similar relief automatically, no request needed. Reasonable-cause relief can cover additional years where illness, disaster, or events outside your control caused the lapse.

Say you owe $68,500: the math on each path

Here's a clearly hypothetical example with the arithmetic shown. Say you're a 1099 agent who owes $68,500 across tax years 2023–2025 — tax, penalties, and interest combined — after a strong 2023 set a bill that a slow 2024–2025 market never let you pay.

- The cost of waiting: the failure-to-pay penalty alone adds 0.5% × $68,500 ≈ $342 per month, with daily-compounding interest on top. If one of those years is still unfiled, the failure-to-file penalty runs 5% per month on that year's unpaid tax — on a $20,000 unfiled year, that's $1,000 a month until it caps at 25%. You can estimate your own accrual with our Penalty & Interest Calculator.

- Straight installment agreement: $68,500 ÷ 72 months ≈ $951/month before ongoing interest. But at $68,500 you're over the $50,000 streamlined ceiling, so this route requires a Form 433-F financial disclosure — and likely a lien filing.

- The pay-down move: pay $18,501 up front to bring the balance to $49,999, and you're back under the streamlined line — eligible to set up roughly $695/month over 72 months online, no financial disclosure, no IRS-dictated payment. For agents expecting a commission check soon, this single move often changes the whole case.

- The passport angle: $68,500 is above the $66,000 certification threshold for 2026. Debt in a qualifying installment agreement is generally excluded from "seriously delinquent" status — so getting a plan in place doesn't just stop levies, it protects your passport.

- The OIC sketch: suppose your only assets are $6,000 of car equity and $2,500 in the bank, and after IRS-allowed expenses your income leaves $350/month. A lump-sum offer is roughly assets plus 12 months of that surplus: $8,500 + ($350 × 12) = $12,700 — filed with the $205 fee and a 20% deposit ($2,540). That's what a qualifying offer looks like. If your commission pipeline realistically supports $951/month, the IRS will say so and reject it — which is why the financial analysis has to come before the application, not after.

How to respond to real estate agent back taxes, step by step

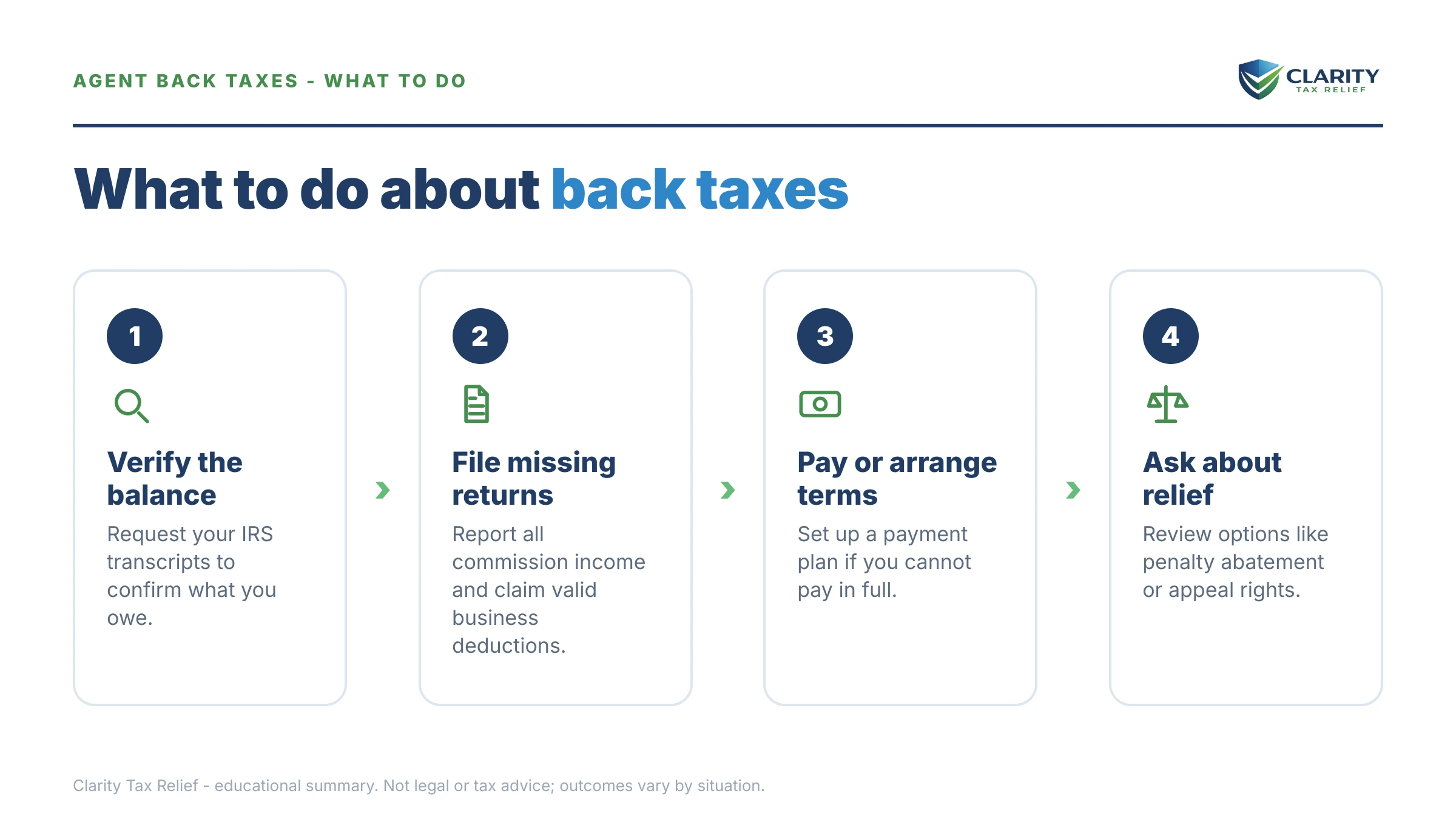

- Pull your IRS transcripts. Log into your IRS online account or request account and wage-and-income transcripts so you can see exactly which years are unfiled, what the IRS shows you earned, and what each year's balance is with penalties and interest.

- File every missing return. Prepare each unfiled year with your real Schedule C deductions — mileage, MLS dues, E&O insurance, marketing, desk fees — using broker commission ledgers and bank statements where receipts are long gone.

- Stop the current-year bleeding. Start quarterly estimated payments on this year's commissions immediately, because the IRS will not finalize most resolutions while you are still falling behind on the current year.

- Match the balance to a resolution. Choose a payment plan, Currently Not Collectible status, or an Offer in Compromise based on your total debt and what your finances genuinely support, and get it in place before enforcement notices escalate.

- Request penalty relief. Ask for first-time abatement or reasonable-cause relief on qualifying years — removing a penalty also removes the interest that was charged on it.

Fixing the engine: staying current while the old debt gets resolved

Every IRS resolution assumes you stop digging — a payment plan or offer defaults if next April brings a new unpaid balance. For agents, staying current means a set-aside habit: 25–35% of each net commission (after splits and expenses) moved to a separate tax account the day the check clears, then paid out on the four quarterly deadlines.

Two structural notes as your production grows. First, high-earning agents sometimes benefit from an S corporation for future income — but incorporating does nothing to old debt, and an entity brings payroll obligations that create a nastier debt category if missed; see sole proprietorship vs LLC taxes for how entity choice actually affects who owes what. Second, if you run a team and pay staff, withheld payroll taxes are a different animal entirely — falling behind there means 941 back taxes and potential personal liability that no entity shields.

And if part of your income comes from a short-term rental you own or manage, that revenue has its own reporting traps — covered in Airbnb host owes taxes.

When you can handle this yourself — and when help changes the outcome

Plenty of agent cases are genuinely DIY. If you owe under $25,000, every return is filed, and the balance is accurate, you can set up a streamlined plan online at the IRS payment plans page in under an hour — no professional required. Same if you can clear the balance within 180 days: take the $0-fee short-term plan and be done. If money is tight and your issue is with the IRS's own delays or errors, the Taxpayer Advocate Service is free.

Experienced help earns its cost in specific situations: multiple unfiled years where returns must be reconstructed to replace inflated SFR assessments; a levy already served on your broker or bank, where days matter; balances over $50,000, where the IRS analyzes your financials and the way commission income is presented directly changes your payment; OIC candidacy, where the math must work before you spend a dime applying; and any case with a revenue officer assigned. In those cases, the difference between a well-presented financial statement and a sloppy one is measured in hundreds of dollars a month for years.

If your balance is anywhere near $68,500 — or your broker just received a levy for your commissions — a free case review with an experienced tax professional takes about 15 minutes: call (888) 825-7779 or use the 2-minute form.

Terms on your IRS mail, decoded

- 1099-NEC: the form your broker files reporting nonemployee compensation — the IRS's copy is what its computers match against your return.

- Substitute for Return (SFR): a return the IRS files for a non-filer using gross income and no business deductions — almost always overstates what an agent owes.

- Self-employment tax: the 15.3% Social Security and Medicare tax on net self-employment income, owed on top of income tax.

- Levy vs. lien: a levy takes property (bank funds, broker-held commissions); a lien is a public legal claim against everything you own, securing the debt.

- CDP rights: your Collection Due Process right to a hearing (Form 12153) within 30 days of a final levy notice — it pauses levy action while heard.

- CSED: the Collection Statute Expiration Date — generally 10 years from assessment, pausable by appeals, an OIC, or bankruptcy.

Real estate agent back taxes: your questions, answered

Can the IRS garnish my real estate commissions?

Yes — but differently than a W-2 paycheck. Because commissions are 1099 income, a levy served on your broker generally captures only what the brokerage holds or owes you on the day the levy lands, not a continuous slice of every future check. The catch: the IRS can serve fresh levies again and again, and it can levy your bank account separately — so one-time does not mean one and done.

Can I lose my real estate license because I owe the IRS?

The IRS does not suspend state-issued real estate licenses. Some states take licensing action over unpaid state taxes, so a state balance can be a bigger licensing risk than a federal one — check with your state revenue agency and licensing board. The federal consequence that does apply: at $66,000 or more in seriously delinquent debt (the 2026 threshold), the IRS can certify you to the State Department for passport denial or revocation.

I haven't filed in several years. How many returns do I need to file?

As a general rule, the IRS treats you as back in filing compliance once your last six years of returns are in, though it can require more in unusual cases. Filing comes first no matter what: the IRS will not approve a payment plan or an Offer in Compromise while required returns are missing. If the IRS already filed substitute returns for you, filing your own corrected returns often shrinks the balance dramatically, because substitutes skip your business deductions entirely.

Does the IRS know how much I made if my broker paid me on a 1099?

Yes. Your broker files a copy of every Form 1099-NEC with the IRS, and its computers match those totals against what you reported. If you skip filing or underreport, the mismatch triggers automated action — a CP2000 underreporter notice, or a substitute return for non-filers — built on the gross 1099 figure with none of your expenses subtracted.

Is it worse to not file or to not pay?

Not filing is roughly ten times worse. The failure-to-file penalty runs 5% of the unpaid tax per month, capped at 25%, while the failure-to-pay penalty runs 0.5% per month. On a $20,000 balance that is $1,000 a month for not filing versus $100 for not paying. File every return on time even in a year you cannot pay a dollar.

Can a real estate agent settle IRS back taxes for less than the full amount?

Only if the numbers support it. An Offer in Compromise is accepted when your assets plus future income genuinely cannot cover the debt before the collection statute expires — the IRS accepted roughly 1 in 5 offers in FY2024. Variable commission income cuts both ways: a documented down market strengthens your case, but the IRS averages your income and will question a temporarily bad stretch that looks likely to rebound.

Will an IRS tax lien stop me from closing deals for clients?

No — a federal tax lien attaches to your property, not your ability to practice. Where it bites is your own finances: liens are public record, they complicate your own mortgage or refinance, and a title search will surface one if you sell property you own. Tax liens no longer appear on the three major credit reports, but lenders still find them in public records.

Does forming an LLC or S corporation make my old back taxes go away?

No. Back taxes from your Schedule C years are your personal debt, and routing future commissions through an entity does not touch them. An S corporation can reduce self-employment tax going forward for consistently high earners, but it adds payroll-tax obligations — and falling behind on payroll taxes creates a far more dangerous category of debt than the one you have now.

How much should a real estate agent set aside for taxes going forward?

A common working rule for self-employed agents is 25–35% of net commission — after brokerage splits and expenses — adjusted for your bracket and state. The mechanical fix that keeps you out of this situation again is quarterly estimated payments, four deadlines a year. Underpaying quarterlies triggers its own penalty, separate from anything you owe on old years.

Your next 24 hours

- Find your real number. Log into your IRS online account and note the balance for each year and which years show no return filed — the notices in your drawer may already be out of date.

- Gather three things: your 1099-NECs (your broker can reissue them), your broker's commission ledger for the unfiled years, and your last filed return. That's enough for a professional to size the whole case.

- Get the free case review. Call (888) 825-7779 or use the 2-minute form — every month you wait adds another 0.5% penalty plus interest to the balance, and nothing on your account improves by sitting still.

When you're ready to make a payment or set up a plan directly, the official starting point is IRS.gov/payments — never a third-party link from an email or text.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.