Self-Employed & Gig Tax Debt

Hair Stylist Taxes Owed 1099: What to Do About Back Taxes in 2026

The short answer: hair stylist taxes owed on 1099 income come from 15.3% self-employment tax plus income tax that no one withheld. File any missing Schedule C returns first — booth rent, supplies, and education cut the bill — then put the remaining balance on an IRS plan of up to 72 months if you owe $50,000 or less.

You rent your chair, the salon hands you a 1099-NEC instead of a W-2, and somewhere between backbar costs and slow Tuesdays, the tax money never got set aside. Maybe it's one bad season. Maybe it's three years of unfiled returns in a drawer. Either way, this is fixable — and the order you fix it in decides what you actually pay.

Two or three separate paper trails already tell the IRS what you earned behind the chair. The image below shows exactly what those 1099 forms look like and where the reported income figure sits, so you know what the IRS's computers are matching against.

⏱ The clock that's already running: there's no notice deadline yet, but the failure-to-file penalty grows at 5% of the unpaid tax per month, up to 25% — ten times the failure-to-pay rate. And any refund from a return due more than three years ago expires unclaimed. Filing, even without paying, stops the worst penalty immediately.

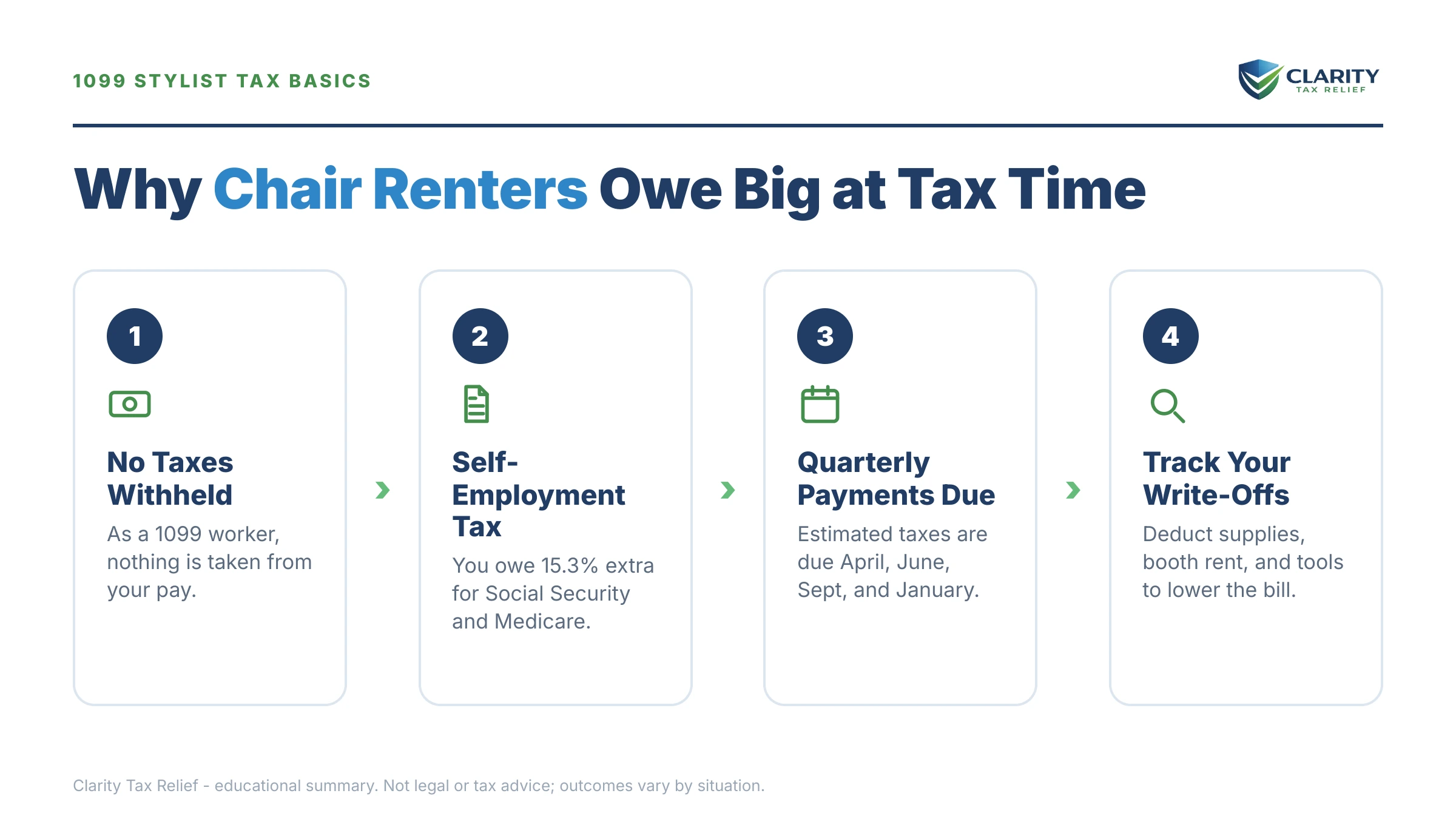

Why hair stylists owe taxes on 1099 income

A 1099 hair stylist pays 15.3% self-employment tax on net profit — on top of regular income tax — because no employer withholds anything from booth-rent or commission income. At a W-2 job, your employer paid half of Social Security and Medicare and withheld the rest before you ever saw the check. Behind a rented chair, all of it lands on you at filing time, computed on Schedule SE. That's the self-employment tax shock in one sentence.

What makes stylists different from most gig workers is that your income reaches the IRS through three separate channels:

- The salon's 1099-NEC. If you work on commission or the salon pays you directly, it reports what it paid you. The IRS's matching system compares that box to your return automatically.

- Card and app payments (1099-K). Square, your booking app, or Venmo business payments generate a 1099-K once you cross the $20,000 / 200-transaction threshold — the $600 rule is dead for 2026, but income below the threshold is still taxable, and balances from earlier years didn't go anywhere.

- Cash tips. No form reports them, but they're fully taxable — and in an exam, the IRS reconstructs them from your bank deposits and appointment book.

One more wrinkle specific to salons: some "1099 stylists" are really employees. If the salon sets your hours, your prices, your product line, and your schedule, you may be misclassified — a 1099 that should be a W-2. That matters because an employee owes half the payroll tax a contractor does. It's a genuine lever in some cases, but it puts the IRS between you and the salon, so weigh it before filing Form SS-8.

What happens if you ignore 1099 back taxes

If you never file, the IRS can build a substitute return for you — with your full gross income and zero deductions for booth rent, color, or supplies — and then collect on that inflated number. The sequence is automated, and in 2026 it runs on computers that didn't get cut when IRS staffing shrank. Here's the order it unfolds in:

- CP59 — no return on file. The first automated nudge for a missing year. Filing your own numbers now keeps you in control of the math.

- CP516 / CP518 — escalating requests. Still requests, but the file is moving toward the IRS doing your return for you.

- Substitute for Return (SFR) proposed. The IRS totals every 1099-NEC and 1099-K it holds and computes tax as if you had no business expenses. For a stylist paying chair rent, this routinely doubles the real liability. See what to do when the IRS files a return for you.

- CP3219N — notice of deficiency. Your 90-day window to contest the amount in Tax Court before it becomes a legal debt. Filing a correct return during this window usually replaces the SFR math.

- Assessment, then the bill cycle. CP14 arrives first, then reminders, then CP504 (the IRS can take your state refund), then LT11 — the final notice that opens the door to levies after 30 days.

- Levy. Bank accounts, and yes, your contractor pay: the IRS can garnish 1099 income by sending a levy to the salon or platform that pays you, capturing whatever is owed to you when it lands.

| Notice / stage | Your window | What you lose if it passes |

|---|---|---|

| CP59 — no return filed | Respond by the date printed on the notice | The easiest chance to file your own numbers before the IRS builds them for you |

| CP2566 — substitute return proposed | Response date printed on the notice | Replacing zero-deduction IRS math with a real Schedule C before assessment |

| CP3219N — notice of deficiency | 90 days | Your right to contest the amount in Tax Court before paying |

| CP14 — first bill | Typically 21 days | The cheapest moment to set up a plan before penalties stack on reminders |

| CP504 — intent to levy state refund | Date printed on the notice | Your state tax refund |

| LT11 — final notice of intent to levy | 30 days | Collection Due Process rights (Form 12153) — after this, bank accounts and contractor pay are levy targets |

Sitting on unfiled 1099 years right now?

Every month unfiled adds another 5% failure-to-file penalty until it caps — and the substitute-return math never includes your booth rent. An experienced tax professional can pull your IRS records, show you exactly what the IRS has, and map the cheapest way out — free, confidential, no pressure.

Your options once the returns are filed

Every IRS payment option requires filed returns first — a stylist with unfiled years must file before the IRS will approve any plan. Once the returns post, the balance can be handled several ways, and most of them can be done without hiring anyone; our full guide to settling tax debt yourself walks through each program in detail. Here's how they compare for a typical stylist balance:

| Option | Who qualifies | Cost & notes |

|---|---|---|

| Pay in full | Anyone | Cheapest total cost — penalties and interest stop accruing the day it's paid |

| Short-term plan (180 days) | A balance you can clear within 180 days | $0 setup fee; interest and the 0.5%/month late-pay penalty continue until paid |

| Guaranteed installment agreement | Tax owed of $10,000 or less, returns filed and current | The IRS must accept when the conditions are met — the one program with automatic approval |

| Streamlined installment agreement | Balance of $50,000 or less, all returns filed | Set up online in minutes, up to 72 months; interest and late-pay penalty keep accruing |

| Currently Not Collectible | Paying anything would leave you unable to cover basic living costs | Collection pauses after financial review (Form 433-F); the debt and interest remain |

| Offer in Compromise | Assets plus future income genuinely can't cover the debt before collection expires | $205 fee plus 20% down on lump-sum offers — both waived with low-income certification; the IRS accepted roughly 1 in 5 offers in FY2024 |

| Penalty relief (FTA / AEP) | Clean compliance for the prior 3 years | Removes penalties, not tax; starting summer 2026, Automatic Exemption from Penalty applies without a request |

Two notes worth flagging for stylists specifically. First, penalty relief is real money here: three late-filed years often carry maxed-out failure-to-file penalties, and first-time penalty abatement can wipe the penalty from one qualifying year outright, with reasonable-cause arguments available for the others. Second, an Offer in Compromise is means-tested math, not a discount program — a stylist with steady bookings and an ongoing business usually shows enough future income that a payment plan fits better. Be skeptical of anyone who promises settlement before seeing your financials.

Say you owe $31,200 across three unfiled years: the math

Here's a fully hypothetical example built the way stylist cases actually run. Say your wage and income transcripts show, for each of three unfiled years, a $16,000 salon 1099-NEC, a $30,000 Square 1099-K, and about $6,000 in cash tips — $52,000 gross per year.

Now the part the substitute return skips. Your real costs: booth rent at $1,150/month ($13,800), backbar and color ($4,200), license and education ($900), software and processing fees ($1,100) — about $20,000 in deductions, leaving roughly $32,000 net profit per year.

On that net: self-employment tax runs about $4,500 (92.35% of $32,000 × 15.3%), and federal income tax after the standard deduction adds roughly $1,600 — call it about $6,100 per year, or $18,300 across three years. Late-filing and late-payment penalties plus daily-compounding interest push the total to roughly $31,200 by the time everything posts. You can rough out your own penalty-and-interest stack with our IRS penalty & interest calculator — it estimates, and your notices control.

Where that leaves you: $31,200 is under the $50,000 streamlined ceiling, so an online installment agreement over 72 months works out to about $433/month before ongoing accrual — realistically closer to $475–$500 to actually retire it, and paying faster always costs less. A 180-day short-term plan would demand about $5,200/month, unrealistic for most chairs. And here's the number that justifies filing carefully: if the IRS had built substitute returns on the full $52,000 gross with no deductions, roughly $60,000 of phantom income across three years would have inflated the bill by many thousands of dollars. Filing real Schedule Cs isn't paperwork — it's the single biggest cut you'll ever make to this balance.

The deductions that shrink a stylist's back-tax bill

Every legitimate Schedule C deduction cuts both income tax and 15.3% self-employment tax — nearly double the savings per dollar compared with a W-2 deduction. Missing receipts don't kill this: back taxes can be filed without perfect records using bank statements, Venmo history, supplier accounts, and your booking calendar to reconstruct reasonable figures.

| Deduction | What counts & proof that works |

|---|---|

| Booth / chair rent | Weekly or monthly payments to the salon — Venmo history, canceled checks, or your booth lease |

| Backbar & supplies | Color, developer, foils, product used on clients — supplier invoices and card statements |

| Tools & equipment | Shears, clippers, dryers, styling chair — receipts; bigger purchases may be depreciated |

| License & education | Cosmetology license renewals, continuing-ed hours, advanced-cut and color workshops |

| Software & processing fees | Booking apps, Square/card processing fees, your website — the fee lines on settlement statements |

| Business mileage | Trips between salons, supply runs, education travel — a log reconstructed from your booking calendar (never your commute) |

| Capes, smocks & laundry | Work-only garments and the cost of cleaning them |

| Phone & internet (business share) | The percentage of your bill used for bookings, client messages, and marketing |

How to fix 1099 back taxes as a hair stylist, step by step

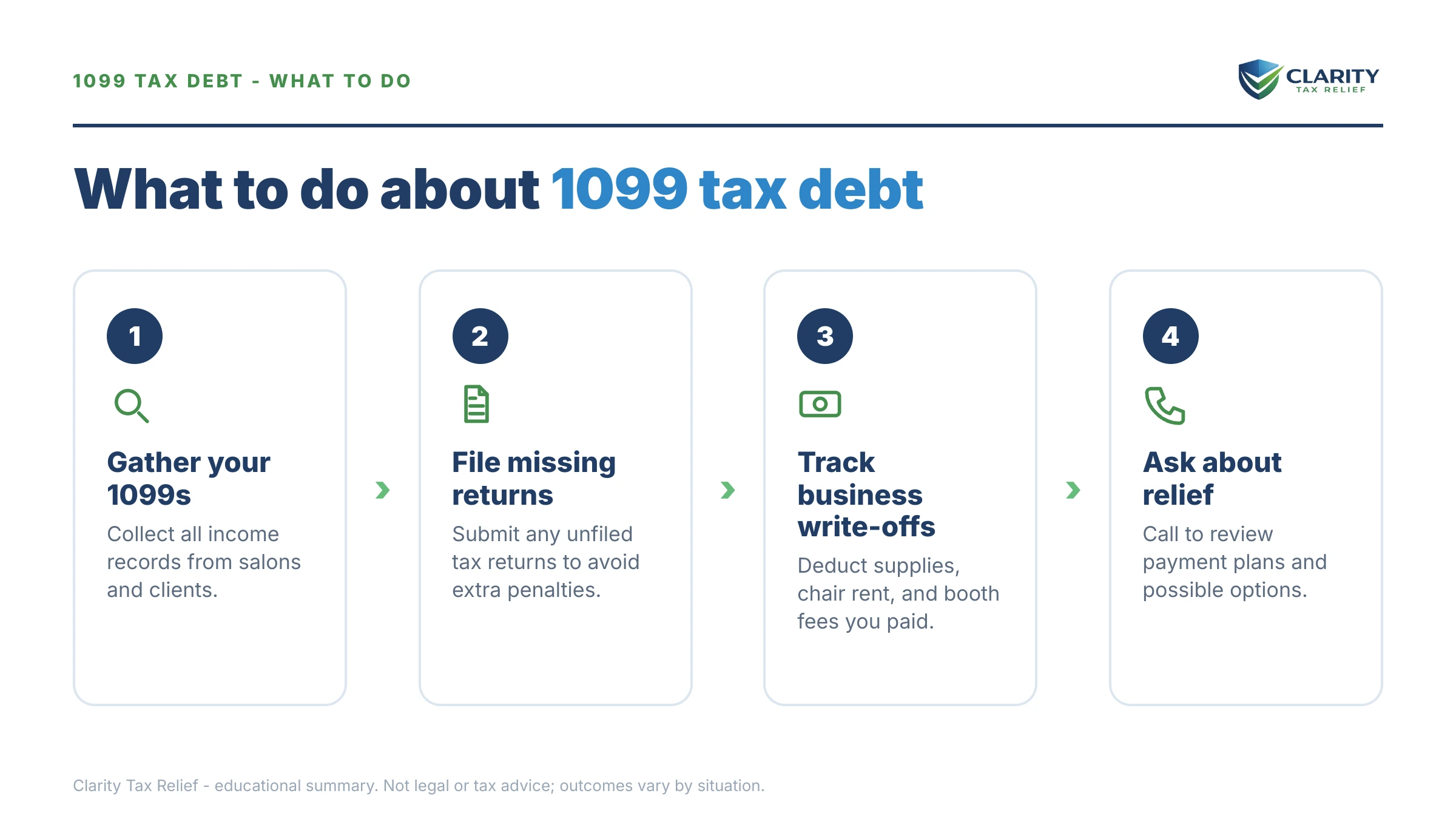

- Pull your IRS wage and income transcripts. Create an IRS online account and download the wage and income transcript for each unfiled year — it lists every 1099-NEC and 1099-K the IRS already has, so your returns match its records.

- Rebuild each year's deductions. Gather booth-rent proof, supply receipts, bank and card statements, and a reconstructed mileage log from your booking calendar — reasonable reconstruction is accepted when receipts are gone.

- File every missing return. Prepare and file all unfiled years — the IRS generally wants no more than the last six years — because filing stops the 5%-per-month failure-to-file penalty and unlocks every payment option.

- Choose a resolution before the first bill arrives. Match your balance to a payment plan, hardship status, or offer using the options table above, and set it up as soon as the returns post so the notice sequence never starts.

- Start quarterly estimated payments. Send in 25–30% of your net profit each quarter going forward so a new balance never stacks on top of the one you just resolved. Here's how quarterly estimated taxes work in plain English.

When you can handle this yourself — and when help changes the outcome

Plenty of stylist cases don't need a professional. If you're missing one year, you agree with the numbers, and the balance lands under about $25,000, the DIY path is real: file the return, set up a streamlined plan online, and request penalty abatement yourself. The IRS's own Self-Employed Individuals Tax Center and payment plans page cover the mechanics, and if you hit a wall the Taxpayer Advocate Service exists for exactly that.

Experienced help earns its cost in specific situations: multiple unfiled years where a substitute return has already been assessed (replacing SFR math is a process, not a phone call), a levy already in motion against your salon pay or bank account, genuine hardship where CNC or offer math is on the table, or a misclassification dispute with the salon. And if you've moved from renting a chair to owning the salon with stylists or assistants on payroll, the stakes change entirely — salon owner tax debt and 941 back taxes carry personal-liability rules that individual 1099 debt doesn't.

Terms on your forms, decoded

- 1099-NEC: the form a salon or business files when it pays a non-employee $600 or more — it's how the IRS knows your commission income.

- 1099-K: the form card processors and payment apps file once you cross $20,000 and 200 transactions — it reports your gross card receipts, before rent and supplies.

- Self-employment tax: the 15.3% Social Security and Medicare tax on net profit, computed on Schedule SE — both the employer and employee halves, because you're both.

- Schedule C: the business form attached to your 1040 where service income and tips go in and booth rent, supplies, and mileage come out.

- Substitute for Return (SFR): a return the IRS constructs for a non-filer from the 1099s it holds — gross income, zero deductions, worst-case tax.

Hair stylist 1099 tax questions, answered

Do hair stylists have to pay taxes on cash tips?

Yes — every dollar of tips is taxable income, whether it came in cash, on a card, or through Venmo, and whether or not any form reports it. In an audit, the IRS reconstructs tip income from bank deposits and card records, so leaving cash tips off a return creates risk rather than savings. Report tips on your Schedule C along with your service income.

How much should a hair stylist set aside for taxes on 1099 income?

A reliable rule of thumb is 25–30% of your net profit — what's left after booth rent and supplies, not your gross. That covers 15.3% self-employment tax plus federal income tax for most stylists. Set it aside every week and send it in four times a year as quarterly estimated payments so next April doesn't repeat this year.

Does Square or Venmo report my hair stylist income to the IRS?

For 2026, payment apps issue a 1099-K only if you take in over $20,000 AND more than 200 transactions — the $600 rule was repealed. But the reporting threshold doesn't change what's taxable: all of your service income is reportable whether a form arrives or not, and balances from earlier years don't disappear because the threshold moved.

What if my salon gave me a 1099 but treats me like an employee?

If the salon sets your hours, your prices, and which products you use, you may be misclassified — and Form SS-8 asks the IRS to decide your status. A worker ruled an employee owes only the employee share of Social Security and Medicare, not the full 15.3%. Weigh the relationship cost first: an SS-8 filing triggers IRS contact with the salon.

I haven't filed taxes in three years — can I go to jail?

Jail is extremely rare for stylists who come forward and file voluntarily — the IRS's civil system wants your returns and its money, not a prosecution. Criminal cases target willful, ongoing evasion, usually with large dollars and concealment. The practical risk of waiting isn't handcuffs; it's a substitute return with zero deductions and a growing penalty stack.

Can I still deduct booth rent on returns I file late?

Yes. A late-filed Schedule C claims every deduction an on-time one would — booth rent, supplies, education, license fees — and those deductions shrink both income tax and self-employment tax. The one clock that matters: if a late year would have produced a refund, you must file within three years of the original due date to collect it.

Can the IRS levy my 1099 pay from the salon?

Yes — once the final-notice stage passes, the IRS can send a levy to the salon or booking platform that pays you. Unlike a W-2 wage garnishment that takes a slice of each check, a levy on contractor pay typically captures 100% of whatever is owed to you when the levy lands. Setting up a payment plan before that stage prevents it.

Your next 24 hours

- Find every 1099 you can — or skip the hunt: create an IRS online account and pull the wage and income transcript for each missing year. That's the exact list the IRS is working from.

- Gather the proof that cuts the bill: booth-rent payments (Venmo history counts), supply receipts or supplier account statements, bank statements, and your booking calendar for mileage.

- Get a free case review. Unfiled 1099 years accrue a 5%-per-month failure-to-file penalty until they're in — send us what you have at the 2-minute form or call (888) 825-7779, and an experienced tax professional will map the filing order and the cheapest resolution before the notices start.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.