Unfiled Tax Returns

Haven't Filed Taxes in 7 Years? Here's Exactly How to Catch Up (2026)

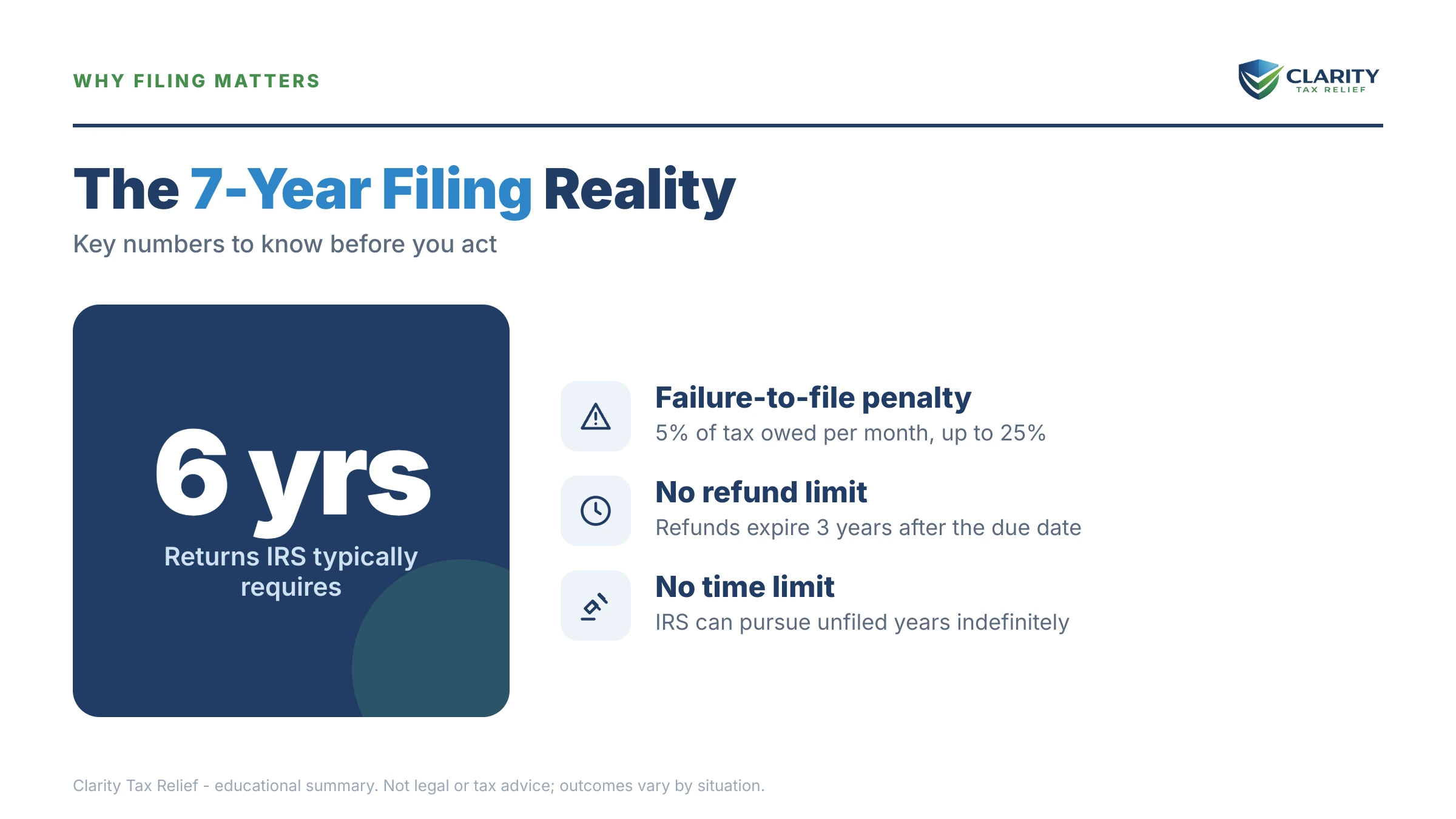

The short answer: if you haven't filed taxes in 7 years, you usually only need to file the last six — IRS Policy Statement 5-133 generally treats six years of returns as full compliance. File before the IRS files substitute returns for you, and voluntary filers are almost never referred for criminal charges.

Seven tax seasons have come and gone. The first year, you were slammed with work and figured you'd catch up. By year three, the 1099s went straight into a drawer unopened, because opening them made it real. Now it's 2026, you're still self-employed, and you have no idea whether you owe $5,000 or $50,000.

Here's what almost nobody in your position knows: you probably don't have to file all seven years, refunds are still alive on the newest three, and the IRS has an established, non-dramatic path for people who come forward on their own. The image below maps how an unfiled-return case escalates — and where in that sequence you can still step in on your own terms.

⏱ The clock that actually matters: an unfiled year never expires — the IRS can assess tax on it forever, because the assessment clock only starts when you file. The deadlines run the other way: refunds die 3 years after each return's due date, and penalties grow monthly until they cap at their maximums.

Do you have to file all 7 years? Usually not — here's the six-year rule

The IRS generally requires only the last six years of returns to consider a non-filer compliant, under its own Policy Statement 5-133. For most people reading this in mid-2026, that means tax years 2020 through 2025 — the seventh year back is typically left alone unless the IRS specifically demands it, an substitute return already exists for it, or there's significant unreported business income sitting in it. The full mechanics are in our guide to how many years of back taxes you have to file.

This changes the size of the project. You're not reconstructing seven Schedule Cs — probably six, sometimes fewer if some years fell below the filing threshold. Here's where each of your seven years stands right now:

| Tax year | Usually required under the six-year rule? | Refund still claimable? |

|---|---|---|

| 2025 | Yes | Yes — typically until April 15, 2029 |

| 2024 | Yes | Yes — typically until April 15, 2028 |

| 2023 | Yes | Yes — typically until April 15, 2027 |

| 2022 | Yes | No — window closed April 15, 2026 |

| 2021 | Yes | No — expired |

| 2020 | Yes (sixth year back) | No — expired |

| 2019 | Usually not — unless the IRS filed an SFR or sent a written demand for it | No — expired |

One more clock that hits the self-employed specifically: self-employment income only earns Social Security credits if it's reported within roughly 3 years, 3 months, and 15 days after the tax year ends. Your 2019–2022 earnings have generally dropped off your Social Security record permanently — but 2023 can still be credited if you file before April 2027. Seven years of missing SE income is a real dent in a future benefit check.

If your gap is shorter or longer, the math shifts: at haven't filed taxes in 3 years every refund may still be recoverable, at haven't filed taxes in 5 years you're straddling the refund cutoff, and at haven't filed taxes in 10 years the six-year rule does even more work for you.

Why the IRS already knows about your 7 unfiled years

Every 1099-NEC, 1099-MISC, and 1099-K a client or platform sent you was also filed with the IRS — the agency holds a year-by-year record of your gross income even though you never filed. That record lives in your wage and income transcript, and it's exactly what the IRS's automated non-filer program uses to decide which accounts to work.

What the IRS does not have is your expense side. It knows a builder paid you $88,000; it doesn't know $41,000 of that went to materials, subcontractors, insurance, and mileage. That asymmetry is the core danger of waiting: any return the IRS constructs for you is built on gross income with zero business deductions.

Two things have changed the odds of being noticed in 2026. The IRS revived its high-income non-filer sweeps, and while the workforce shrank about 27% in 2025, non-filer selection is automated — the computer that flags seven missing returns under one Social Security number never got laid off. Note the reporting nuance for platform income: the 1099-K threshold reverted to $20,000 and 200 transactions, so some smaller platform years may not appear on your transcript — but direct-client 1099-NEC income almost always does.

What happens if you haven't filed taxes in 7 years and keep waiting

The IRS can file a substitute for return (SFR) for any unfiled year — a return prepared against you, using your gross 1099 income, single or married-filing-separately status, and no business deductions at all. The sequence from silence to seizure runs like this:

- CP59 — "You didn't file." The first non-filer notice for a given year. No enforcement yet; the cheapest possible moment to act.

- CP516 / CP518 — escalating demands. The CP518 is the final written request for the return before the IRS starts building the year itself.

- SFR proposed (CP2566). The IRS shows you the tax it computed from gross income — for a sole proprietor, routinely two to four times what an accurate Schedule C would show — with a response window printed on the notice.

- CP3219N — Notice of Deficiency. A statutory 90-day letter. Petition Tax Court or file your real return within the window, or the inflated number becomes a legal assessment.

- Assessment → the collection stream. Once assessed, the year enters the standard billing sequence (CP14 → CP504 → LT11), ending in the power to levy bank accounts and garnish income. Current-year refunds get held against unfiled years (CP63), a federal tax lien can attach to everything you own, and once the certified debt passes $66,000 in 2026, your passport can be denied or revoked.

- Criminal referral — the rare last lane. Willful failure to file is a misdemeanor per year, but prosecutions target fraud and defiance after IRS contact, not people who come forward. The line between the two is explained in can you go to jail for not filing taxes.

- And the trap nobody expects: the 10-year collection statute hasn't even started on your unfiled years. No return, no assessment, no clock. Waiting doesn't run out any statute — it delays the start of the only one that helps you.

Seven years unfiled and not sure where you stand?

Before the IRS builds those years from your gross 1099s — with none of your deductions — let an experienced tax professional pull your transcripts and map exactly which years need filing and what you'd realistically owe. Free, confidential, no pressure.

Your options once the returns are filed

Every IRS resolution program — payment plan, hardship status, Offer in Compromise — requires filing compliance first, which is why the returns come before any deal. The general playbook for resolving a balance on your own lives in our guide to how to settle tax debt yourself; here's how each option applies to a seven-year catch-up:

| Option | Typical eligibility | What limits or disqualifies you |

|---|---|---|

| Short-term payment plan | You can pay the full balance within 180 days | Interest and the 0.5% monthly late-payment penalty keep running until paid |

| Guaranteed installment agreement | Tax owed of $10,000 or less | Must be able to pay within the program's term; all required returns filed |

| Streamlined installment agreement | Balance up to $50,000; up to 72 months, set up online with no financial statement | Defaults if you miss payments or fall behind on current-year estimated taxes |

| Currently Not Collectible (CNC) | Income barely covers IRS allowable living expenses | Debt keeps growing; refunds get offset; IRS re-reviews when income rises |

| Offer in Compromise (OIC) | Assets plus future income genuinely can't cover the debt before the collection statute runs | Roughly 1 in 5 offers were accepted in FY2024; requires staying compliant for 5 years after acceptance |

| Penalty relief | Reasonable cause (illness, disaster, family crisis), or first-time abatement for a qualifying year | FTA needs a clean prior 3 years — tough mid-streak; interest on the tax itself isn't abated |

Penalty relief deserves special attention in a seven-year case because penalties, not tax, are often a third of the balance. First-time penalty abatement can only clear one year and requires a clean prior three — a problem when the prior three were also unfiled — so multi-year cases usually pair it with a reasonable-cause argument tied to whatever started the non-filing streak. And beginning in summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies some penalty relief automatically, with no request needed, so don't pay a preparer to "fight" a penalty the system may remove on its own.

| Step or option | What it costs | How long it takes |

|---|---|---|

| Filing the back returns | $0 if you prepare them yourself; preparer fees vary with complexity | Weeks to prepare; paper-filed old years can take months to process |

| Short-term payment plan | $0 setup fee | Usually same-day online |

| Long-term installment agreement | Modest setup fee, reduced or waived for lower incomes | Same-day online under $50,000; longer if financials are required |

| Currently Not Collectible | $0, but full financial disclosure required | Weeks — after the IRS reviews your income and expenses |

| Offer in Compromise | $205 application fee plus 20% down on lump-sum offers — both waived with low-income certification | Commonly 6–24 months; auto-accepted if the IRS doesn't decide within 2 years, with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count |

| Penalty abatement request | $0 | Phone requests can resolve same-day; written reasonable-cause requests take months |

What 7 unfiled years really costs: a worked example

Say you're a sole proprietor and, once all six required returns are accurately prepared, you owe $19,700 in combined income and self-employment tax across your three balance-due years. Here's the honest arithmetic:

- Failure-to-file penalty: 5% per month, capping at 25% of the tax — and every one of your years hit the cap long ago. When it runs alongside the failure-to-pay penalty it's reduced to 4.5%/month, capping at 22.5%.

- Failure-to-pay penalty: 0.5% per month, capping at 25% after about 50 months — your older years are at or near the cap.

- Combined penalties: up to 47.5% of the tax. On $19,700, that's roughly $9,350 before interest.

- Interest: compounds daily on the tax and the penalties, so years that old typically add several thousand more — a total balance in the low $30,000s is realistic. You can rough out your own numbers with our IRS penalty and interest calculator.

- The payment path: a total near $32,000 fits a streamlined 72-month plan at roughly $445 a month, with interest continuing to accrue as you pay it down.

Now the counterfactual that shows why filing beats waiting: if the IRS instead files an SFR on a single year where your gross 1099s totaled $88,000 — no expenses, no home office, no mileage, no self-employed health insurance deduction — the assessed tax for that one year alone can rival what you'd genuinely owe for all seven. Your Schedule C deductions only exist if you file them.

How to catch up on 7 years of unfiled taxes, step by step

- Pull your IRS transcripts. Get wage and income transcripts for each unfiled year plus account transcripts, so you can see every 1099 the IRS holds and whether any substitute returns were filed.

- Confirm which years you must file. Apply the six-year rule: for most non-filers in mid-2026, tax years 2020 through 2025 satisfy compliance, plus any year where the IRS filed an SFR or sent a written demand.

- Reconstruct your income and expenses. Match transcript 1099 totals against your bank deposits, then rebuild Schedule C deductions from bank statements, card statements, and mileage records.

- Prepare and file the required returns together. File them as one package (older years generally go on paper), including corrected returns for any SFR years so inflated assessments get replaced with real numbers.

- Set up your resolution before the first bill lands. Choose a payment plan, hardship status, or an Offer in Compromise based on your finances, and request penalty relief at the same time.

- Stay current going forward. Start quarterly estimated payments now — every resolution agreement defaults if you fall behind on the current year.

If reconstructing years feels impossible from where you sit, start with filing back taxes with no records — the income side is almost always recoverable from the IRS's own files, and coming forward on your own terms is covered in coming clean on unfiled returns voluntarily.

When you can handle this yourself — and when help changes the outcome

You can do this yourself if your seven years are simpler than they feel: mostly W-2 income with withholding, likely refunds on the open years, no SFRs on your account, and records you can actually find. Pulling transcripts, preparing six returns, and setting up a streamlined payment plan online are all things a patient person can do without paying anyone.

Experienced help earns its cost in specific situations: substitute returns already assessed (replacing them is a reconsideration process, not just a late filing), six or seven self-employed years with thin records, a projected balance large enough that OIC or CNC math matters, a revenue officer already assigned, or any year where income was left off deliberately. In those cases, the order of operations — which years, which relief requests, which resolution — changes the final number by more than any preparer fee.

Terms you'll run into, decoded

- Substitute for Return (SFR): a return the IRS files for you from third-party income data — gross income, no deductions, worst filing status.

- Policy Statement 5-133: the internal IRS policy that generally treats six years of delinquent returns as full filing compliance.

- Wage and income transcript: the IRS's year-by-year record of every W-2 and 1099 filed under your Social Security number.

- ASED (assessment statute): the IRS's deadline to assess tax — normally 3 years, but it never starts on an unfiled return.

- CSED (collection statute): the 10-year limit on collecting an assessed tax; it doesn't begin until an assessment exists.

- SE tax: the 15.3% Social Security and Medicare tax on self-employment profit — usually the biggest surprise on catch-up returns.

7 years of unfiled taxes: your questions, answered

Can you go to jail for not filing taxes for 7 years?

It's legally possible — willful failure to file is a misdemeanor carrying up to a year per unfiled return — but it's rare for people who come forward voluntarily. The IRS reserves criminal referrals almost entirely for fraud and for non-filers who refuse to comply after contact. Filing your back returns before the IRS opens an investigation is the single strongest protection you have.

Do I have to file all 7 years of back taxes?

Usually no. Under IRS Policy Statement 5-133, filing the last six years of returns is generally enough to be considered compliant, so a seventh year is often left alone. Exceptions apply: if the IRS filed a substitute return for that year, sent you a written demand for it, or you had a business or large income in it, you may need to address it anyway.

Can I still get tax refunds from years I didn't file?

Only for the most recent three. A refund must be claimed within three years of the return's due date, so as of mid-2026 only your 2023, 2024, and 2025 returns can still produce refunds. Refunds from 2019 through 2022 are permanently forfeited — filing those years can stop penalties from growing, but that money itself is gone.

How does the IRS know my income if I'm self-employed?

Through information returns. Every 1099-NEC, 1099-MISC, and 1099-K your clients and payment platforms issued was also filed with the IRS, and those totals sit in your wage and income transcript year by year. What the IRS doesn't have is your expenses — which is why a substitute return computed from gross 1099 income almost always overstates what you really owe.

What if I have no records from 7 years ago?

You can rebuild them. IRS wage and income transcripts show roughly ten years of the 1099s and W-2s filed under your Social Security number, which covers the income side. For Schedule C expenses, bank and credit card statements, mileage estimates from your calendar, and supplier records are all accepted reconstruction methods.

Will the IRS forgive penalties on 7 years of returns?

Sometimes, partially. First-time penalty abatement can wipe penalties for one year, but it requires a clean prior three years — hard when several years in a row are unfiled — so most multi-year cases lean on reasonable-cause relief for events like illness, divorce, or disaster. Starting in summer 2026, the IRS's Automatic Exemption from Penalty (AEP) also applies some relief automatically, with no request needed.

Does the 10-year rule erase taxes from 7 years ago?

No — the 10-year collection statute never started. That clock (the CSED) runs from the date tax is assessed, and an unfiled year has no assessment, so those balances can be assessed and then collected far into the future. Filing is actually what starts the clocks working in your favor.

Do unfiled tax returns affect Social Security?

For the self-employed, yes. Self-employment earnings only count toward your Social Security record if they're reported within roughly 3 years, 3 months, and 15 days after the tax year ends. That means your 2019 through 2022 self-employment income has generally fallen off your earnings record for good, while 2023 can still be credited if you file before April 2027.

Your next 24 hours

- Open an IRS online account and request your transcripts. Wage and income transcripts for each year, plus account transcripts — this tells you what the IRS knows and whether any SFRs exist. Start at IRS.gov Get Transcript.

- Gather what you have. Any 1099s in that drawer, bank statements for your business account, and a simple list of the seven years and roughly what you earned in each.

- Get a free case review. An experienced tax professional can confirm which years actually need filing, estimate the real balance with penalties, and pick your resolution before the first bill arrives — the penalties are already at their caps, but interest compounds daily until this is handled. Use the 2-minute form at claritytaxrelief.com/#consult or call (888) 825-7779.

For the IRS's own guidance, see Filing past due tax returns and the official payment plans page.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.