IRS Programs

IRS Fresh Start Program Requirements: What It Takes to Qualify in 2026

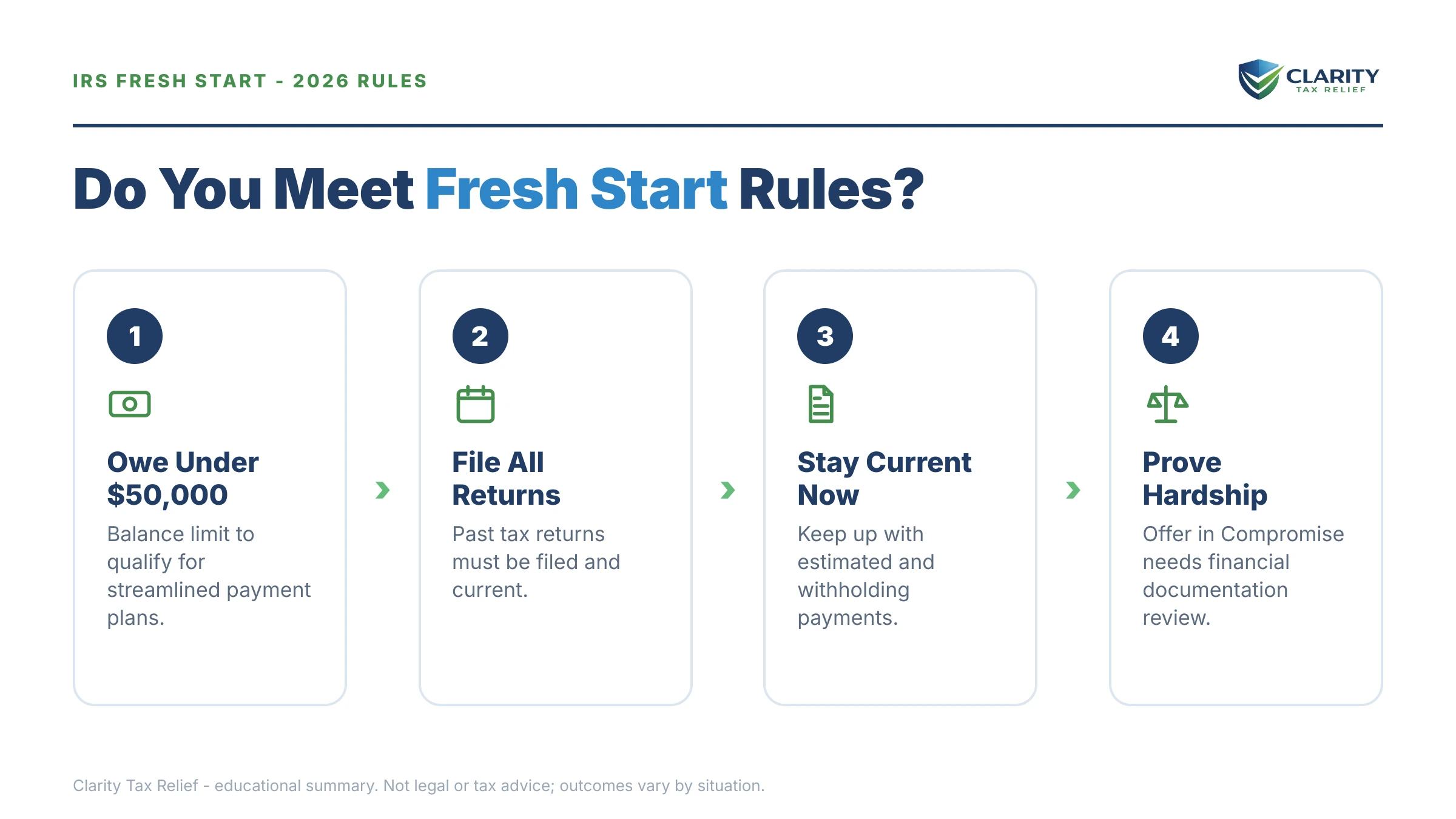

The short answer: the IRS Fresh Start program requirements come down to three universal rules — all required returns filed, current-year taxes being paid, and finances that fit a specific program: a balance of $50,000 or less for a streamlined payment plan, means-tested math for an Offer in Compromise, or documented hardship for collection relief.

You've probably heard "Fresh Start" from an ad, a radio spot, or a mailer that arrived suspiciously soon after the IRS did — and now you're trying to find out what the IRS Fresh Start program requirements actually are before anyone charges you a dime. Smart move. The requirements are real, they're specific, and they're checkable — most of them from your own IRS online account in about ten minutes.

The catch nobody's ad mentions: "Fresh Start" is not one program with one application. It's a family of six IRS options, and each has its own threshold, cost, and list of things that disqualify you. This guide walks through every one, with the exact 2026 numbers.

⏱ The real clock: Fresh Start has no application deadline — but your balance never stands still. The failure-to-pay penalty adds 0.5% every month and interest compounds until you're inside a program. And once your total passes $66,000 (the 2026 threshold), your debt can be certified as "seriously delinquent," putting your passport at risk.

What the IRS Fresh Start program actually is in 2026

The Fresh Start program is not a single program — it's the umbrella name for IRS rule changes from 2011–2012 that permanently loosened eligibility for payment plans, Offers in Compromise, and lien relief. Those changes never expired. They're baked into the ordinary collection rules you'd apply under today.

Fresh Start raised the streamlined payment-plan ceiling to $50,000 over 72 months, cut the future-income math for Offers in Compromise to 12 or 24 months, and lifted the general lien-filing threshold to $10,000. Every one of those numbers still governs your options in 2026 — the details of what's genuinely new this year are covered in our IRS Fresh Start 2026 update.

What Fresh Start is not: a forgiveness giveaway, a secret application, or something a company can "enroll" you in. If you're still wondering whether the whole thing is legitimate, start with is the IRS Fresh Start program real — the initiative is real; much of the marketing around it is not.

The three requirements every Fresh Start option shares

Every Fresh Start option runs through the same three gatekeeper requirements before any threshold even matters. Miss one, and the IRS won't process your request — no matter how sympathetic your situation is.

1. All required returns filed. As a matter of policy, the IRS generally wants the most recent six years of returns on file before it considers you compliant. An unfiled year anywhere in that window stalls a payment plan and gets an Offer in Compromise returned unprocessed.

2. Current-year taxes being paid. The IRS won't formalize a deal on old debt while you're creating new debt. For a W-2 employee, that means your withholding has to actually cover this year's tax — a two-minute W-4 fix with your payroll department if it doesn't.

3. No open bankruptcy — for an offer. An active bankruptcy case makes an Offer in Compromise ineligible; the bankruptcy court controls the debt instead. Payment plans and hardship status have their own compliance checks, but bankruptcy is the hard stop on the offer side.

Get those three squared away and the question shifts from "do I qualify for Fresh Start?" to "which option does my balance and income fit?" — which is where the thresholds below take over.

What happens if you wait to apply

Waiting doesn't just grow your balance — it can disqualify you from the cheapest Fresh Start options entirely. The IRS collection system is automated, and it escalates in a fixed sequence whether or not a human ever reviews your file:

- The balance compounds. The 0.5% monthly failure-to-pay penalty plus daily-compounding interest push the total up every month you're not in a program.

- The notice sequence runs. CP14 bill, then CP501/CP503 reminders, then a CP504 intent to levy your state refund, then an LT11 final notice that opens the door to wage and bank levies after 30 days.

- You cross thresholds you can't uncross cheaply. A balance that compounds past $50,000 loses streamlined-plan eligibility; past $66,000, passport certification becomes possible once collection escalates.

- A federal tax lien gets filed. A recorded lien attaches to everything you own and complicates selling or refinancing a home.

- Levies begin. A bank levy freezes funds with a 21-day hold before the money leaves; a wage levy is continuous — it repeats every paycheck until released.

In 2026 there's an extra wrinkle: per TIGTA reports, the IRS workforce shrank roughly 27% in 2025, so reaching a human to negotiate is harder than it's been in years. The automated notices, liens, and levies never slowed down. Applying before enforcement starts means you set the terms; applying after means you're negotiating with a levy already in motion.

Not sure which Fresh Start option your numbers fit?

Send us your balance and your situation. An experienced tax professional will map your filing history, income, and assets to the right Fresh Start program — free, before interest compounds you past another threshold. No pressure, no obligation.

IRS Fresh Start program requirements by option (2026 thresholds)

The IRS Fresh Start program requirements break down into six options, each with its own eligibility line, cost, and disqualifiers. Here's the full map — details on each option follow the table.

| Fresh Start option | Core requirement | Cost to apply | Common disqualifier |

|---|---|---|---|

| Short-term payment plan | Can pay the full balance within 180 days | $0 setup fee | Unfiled required returns |

| Guaranteed installment agreement | Owe $10,000 or less (tax only); clean filing/payment history for the prior 5 years; full pay within 3 years | Standard setup fee (reduced online) | An installment agreement within the prior 5 years |

| Streamlined installment agreement | Owe $50,000 or less (tax, penalties, and interest); up to 72 months | Setup fee — lowest online with direct debit; waivable for low income | Balance above $50,000 without a paydown |

| Non-streamlined installment agreement | Any balance; Form 433-F financial disclosure required | Standard setup fee | Refusing or fudging the financial statement |

| Offer in Compromise | Reasonable Collection Potential below the balance owed | $205 fee + 20% down on lump-sum offers (both waived with low-income certification) | Income/assets showing you can full-pay; open bankruptcy; unfiled returns |

| Currently Not Collectible | Allowable living expenses equal or exceed income (documented hardship) | $0 | Income above IRS expense standards for your area |

| Penalty relief (FTA / AEP) | Clean compliance for the prior 3 years | $0 | Penalties assessed within the prior 3 years (for FTA) |

Short-term payment plan: up to 180 days, $0 setup

A short-term plan gives you up to 180 days to pay in full with no setup fee. The only requirements are filed returns and a balance you can realistically clear in that window — a bonus, a tax refund, or an asset sale on the horizon. Interest and the monthly penalty keep running, but the notice sequence stops escalating while you're in it.

Guaranteed installment agreement: $10,000 or less

If you owe $10,000 or less in tax (penalties and interest don't count against the line), have filed and paid on time for the prior five years, haven't had a payment plan in that period, and agree to full pay within three years — the IRS is required by law to accept your plan. The guaranteed installment agreement is the one corner of Fresh Start where approval isn't discretionary.

Streamlined installment agreement: the $50,000 line

The streamlined installment agreement is Fresh Start's signature change: owe $50,000 or less in combined tax, penalties, and interest, and you can get up to 72 months to pay — online, usually approved the same day, with no financial statement. The IRS generally requires direct debit for balances between $25,000 and $50,000, which also lowers the setup fee.

The $50,000 line is measured against your total assessed balance across all years. If you're a few thousand over, a targeted paydown to slip under the threshold is often the single cheapest move available — more on that in the worked example below.

Non-streamlined agreement: over $50,000, financials required

Above $50,000, the online shortcut closes. You'll submit Form 433-F — a snapshot of your income, assets, and monthly expenses — and the IRS sets your payment using its allowable-expense standards, not your actual budget. Expect a lien determination as part of the process. Our guide to an IRS payment plan over $50,000 covers what the review looks like and how to prepare the numbers before the IRS sees them.

Offer in Compromise: the only option that reduces the debt

An Offer in Compromise settles the debt for less than the full balance — but only when the math supports it. The IRS computes your Reasonable Collection Potential (RCP): your net asset equity plus your monthly disposable income times 12 (for a lump-sum offer) or times 24 (for a periodic offer). That 12/24 multiplier — down from as much as 48–60 months before Fresh Start — is the initiative's biggest gift to people who genuinely can't pay. You can estimate your own offer with our Offer in Compromise Calculator before deciding whether it's worth pursuing.

Requirements: all returns filed, current-year payments current, no open bankruptcy, a $205 application fee, and 20% down on lump-sum offers. Low-income certification — AGI at or below 250% of the federal poverty level — waives the fee, the down payment, and payments during review. Two honest numbers to hold onto: per IRS data, the IRS accepted roughly 1 in 5 offers in FY2024, and if the IRS fails to decide within 2 years, your offer is accepted automatically by law — with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count. The full mechanics are in how does an offer in compromise work.

Currently Not Collectible: hardship status

If paying anything would leave you unable to cover basic living expenses, Currently Not Collectible status pauses active collection — no levies, no garnishment — while your situation stands. You prove it with Form 433-F measured against the IRS's allowable-expense standards. The debt doesn't shrink (interest still accrues and refunds get kept), but the 10-year collection statute keeps running in the background while you're in it.

Penalty relief: FTA today, AEP starting summer 2026

Fresh Start also expanded penalty relief. First-time penalty abatement removes failure-to-file and failure-to-pay penalties for one year if your prior three years are clean — no penalties, all returns filed. And starting summer 2026, FTA is being replaced by the Automatic Exemption from Penalty (AEP), which applies the same relief automatically, with no request needed. If penalties are a big slice of your balance, check this before agreeing to pay them.

A worked example: you owe the IRS $68,500

Say you're a W-2 employee, filing single, and your IRS online account shows $68,500 across two tax years — roughly $61,000 in tax plus $7,500 in penalties and interest. This is a hypothetical, but the arithmetic is exactly what the IRS would run. Three things about that number matter immediately:

First, you're $18,500 over the streamlined line. Second, you're above the $66,000 passport-certification threshold for 2026, so if collection escalates to lien-and-levy territory, your passport can be certified for revocation — and entering a qualifying agreement is what prevents or reverses that. Third, penalty relief could shrink the problem before you solve it: if your prior three years are clean, abatement could knock a real chunk off that $7,500.

Path 1 — pay down to streamlined. Scrape together $18,600 (savings, a 401(k) loan you've priced out, a family loan) to bring the balance to $49,900. Now you qualify for a streamlined online plan: $49,900 ÷ 72 months ≈ $693 a month before the interest and penalties that continue to accrue. No financial disclosure, likely same-day approval, and the passport risk resolves.

Path 2 — non-streamlined plan at the full $68,500. No paydown means Form 433-F. Say your take-home pay is $5,600 a month and the IRS's allowable-expense standards for your county permit $4,700. The IRS expects the difference: about $900 a month — its number, not yours, so gym memberships and private-school tuition don't count.

Path 3 — test the Offer in Compromise math. Using the same $900 disposable income: the IRS first asks whether you can full-pay before the collection statute expires. With roughly 100 months left on the clock, $900 × 100 = $90,000 — more than $68,500, so an offer gets rejected as unnecessary. But change the facts: disposable income of $250 and $4,000 in net asset equity gives $250 × 100 = $25,000 + $4,000 = $29,000 — you can't full-pay, and a lump-sum offer floor would be $4,000 + ($250 × 12) = $7,000. Same balance, opposite outcomes. That's why the OIC is a math question, never a marketing promise.

For a steady W-2 earner at $68,500, Path 1 is usually cheapest if the paydown cash exists; Path 2 is the realistic default; Path 3 only works if your budget genuinely shows hardship the IRS's own standards recognize.

Fresh Start deadlines and rights: the windows that decide your case

Fresh Start itself has no application deadline, but once you're in — or once the IRS moves against you — a handful of fixed windows control what you keep and what you lose.

| Event | Window | The right at stake |

|---|---|---|

| Offer in Compromise rejected | 30 days from the rejection letter | Appeal via Form 13711 — miss it and you start the whole offer over |

| Offer in Compromise pending, no IRS decision | 2 years | Your offer is automatically accepted by law (with narrow exceptions — a returned or rejected offer stops the clock, and time during court disputes does not count) |

| Missed installment agreement payment (CP523 issued) | The termination date printed on the notice | Act before it and the plan can be reinstated; after it, the full balance is collectible |

| LT11 / Letter 1058 final notice of intent to levy | 30 days from the notice date | A Collection Due Process hearing via Form 12153 — your strongest pre-levy appeal right |

| Balance certified seriously delinquent ($66,000+ in 2026) | Until you enter a qualifying agreement | Passport denial or revocation; an approved plan or offer reverses certification |

How to apply for the IRS Fresh Start program, step by step

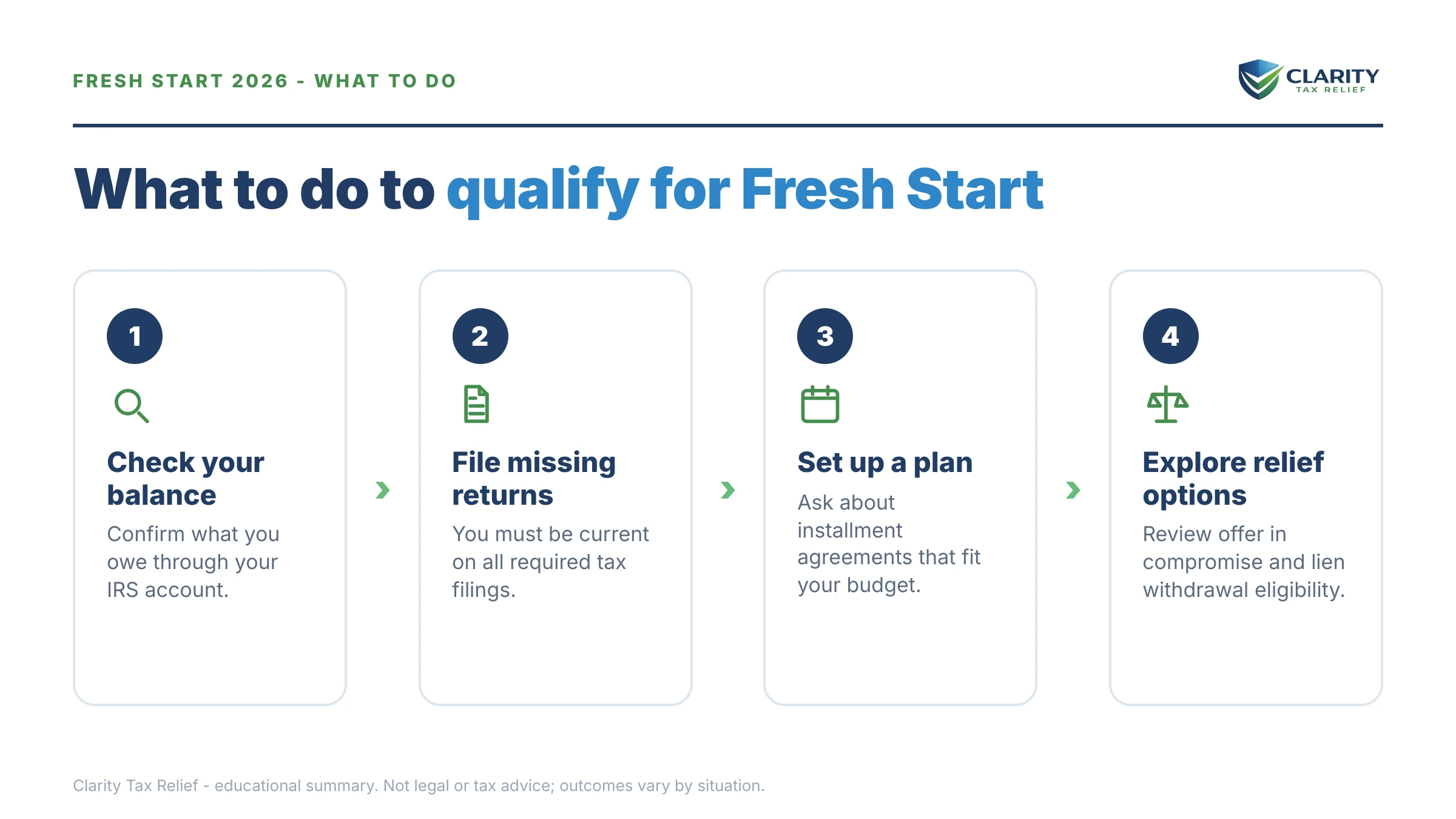

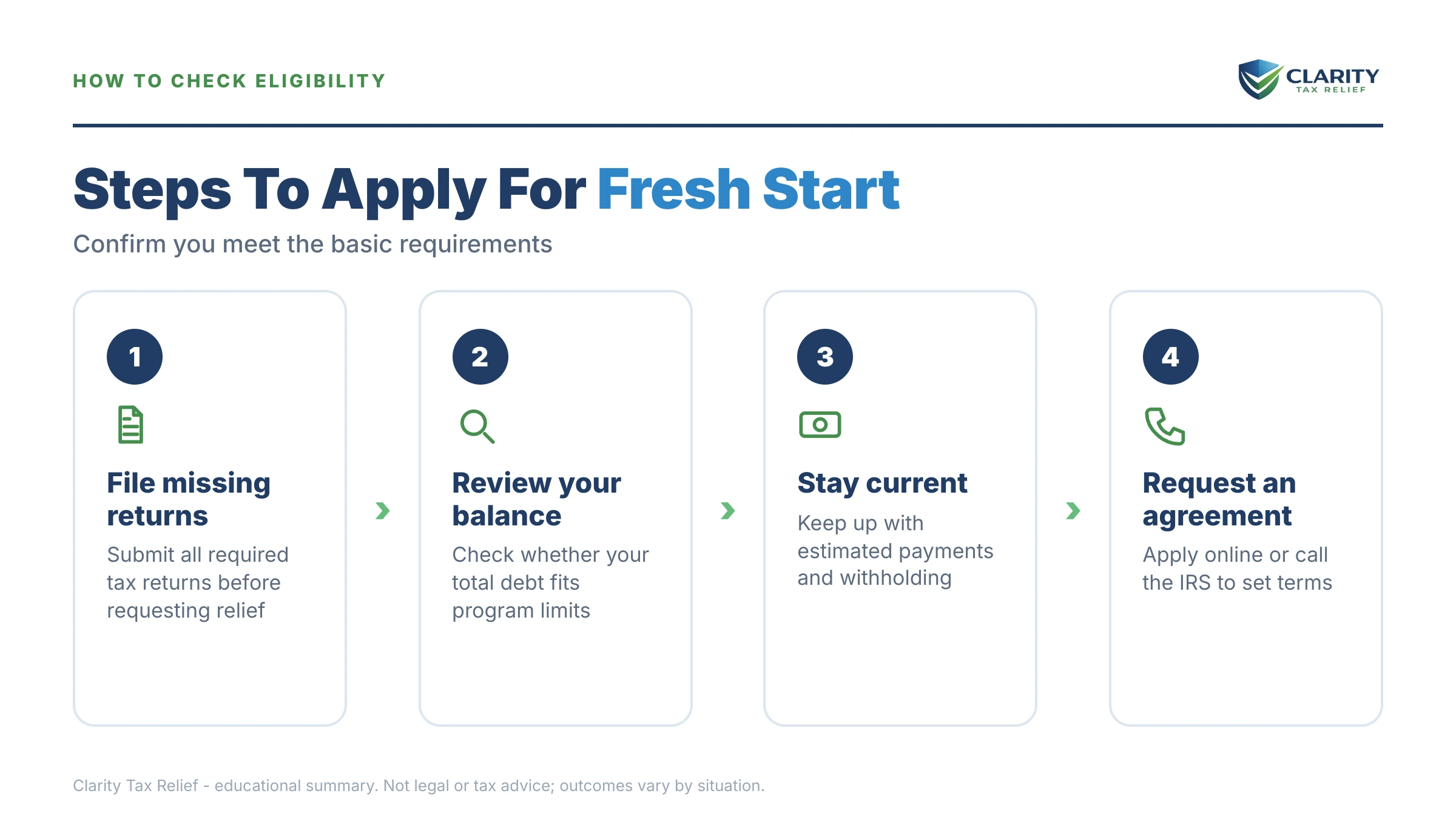

- Confirm every required return is filed. Check your filing history in your IRS online account — the IRS generally wants the last six years on file before it will approve anything.

- Fix your current-year withholding. Adjust your W-4 so this year's tax is actually being paid; adding new debt disqualifies you from nearly every program.

- Pull your exact assessed balance. Your IRS online account shows the total by year — that number decides which thresholds you fit.

- Match your numbers to one program. At or under $50,000, apply online for a streamlined plan; above it, complete Form 433-F — or run the offer math if hardship is real.

- Apply and keep written proof. Save the online confirmation or acceptance letter; a phone conversation with the IRS is not an agreement.

- Calendar every payment. One missed payment can start default proceedings on the whole agreement; direct debit removes that risk.

Payment plans are set up (and fees listed) at the IRS's own payment plans and installment agreements page; offers run through the IRS Offer in Compromise page and its pre-qualifier tool.

When you can handle Fresh Start yourself — and when help changes the outcome

If you owe $50,000 or less, have every return filed, and can afford a reasonable monthly payment, you can set up a streamlined plan yourself online in under an hour — no professional needed. The same goes for a short-term 180-day plan and for a simple first-time abatement request on a single year. Our how to settle tax debt yourself guide walks through every DIY path in detail.

Experienced help tends to change outcomes in four situations. Over $50,000 with a financial statement: how income, assets, and expenses are presented on Form 433-F directly sets your monthly payment, and the allowable-expense standards have traps a first-timer won't see. Offer in Compromise math: with a 1-in-5 acceptance rate, offers succeed on preparation, not hope — knowing your RCP before filing saves you $205 and months of frozen limbo. Multiple unfiled years: the order you file and resolve them changes the total. A levy already in motion: releases move faster when someone knows exactly which unit to call and what to send.

And honestly: if the review shows a simple streamlined plan is your best move, a reputable firm should tell you to go set it up yourself. That's the answer you should expect from us.

If your balance sits above the streamlined line — like the $68,500 example above — a free eligibility review with an experienced tax professional, or a call to (888) 825-7779, will tell you in one conversation whether a paydown, a financial-statement plan, or an offer is the cheaper route.

Terms on Fresh Start paperwork, decoded

- Streamlined installment agreement — a payment plan approved without a financial statement, available when you owe $50,000 or less.

- Reasonable Collection Potential (RCP) — the IRS's calculation of the most it could ever collect from you: asset equity plus 12 or 24 months of disposable income.

- CSED — the Collection Statute Expiration Date; the IRS generally has 10 years from assessment to collect, though appeals, offers, and bankruptcy pause the clock.

- Currently Not Collectible (CNC) — a status that pauses active collection because paying would create hardship; the debt itself remains.

- Seriously delinquent tax debt — a certified balance above the inflation-adjusted threshold ($66,000 in 2026) that can trigger passport denial or revocation.

- Allowable living expenses — the IRS's standardized budget caps for food, housing, transportation, and health care, used instead of your actual spending when setting payments.

IRS Fresh Start program requirements: your questions, answered

What are the requirements for the IRS Fresh Start program?

Every Fresh Start option requires the same three things: all required tax returns filed (generally the last six years), current-year taxes being paid through withholding or estimated payments, and finances that fit the specific program. Beyond that, each option has its own threshold — $50,000 or less for a streamlined payment plan, documented hardship for Currently Not Collectible, and asset-and-income math showing you cannot full-pay for an Offer in Compromise.

Is the IRS Fresh Start program real?

Yes — Fresh Start was a real IRS initiative launched in 2011–2012 that permanently loosened the rules for payment plans, Offers in Compromise, and lien filings. What is not real is a single application called 'Fresh Start' or a program that erases debt for everyone. Companies that promise guaranteed forgiveness under 'the Fresh Start program' are using the name as marketing, not describing an IRS program.

Do I have to file all my back tax returns to qualify for Fresh Start?

Yes — the IRS will not approve a payment plan, Offer in Compromise, or hardship status while required returns are missing. As a matter of policy, the IRS generally requires the most recent six years of returns to consider you compliant. If you have unfiled years, filing them is step one; it also stops the failure-to-file penalty, which runs ten times higher than the failure-to-pay penalty (in months where both apply, the failure-to-file portion drops to 4.5 percent, for 5 percent combined).

Is there an income limit for the IRS Fresh Start program?

No income limit applies to payment plans — a high earner with a $40,000 balance can use a streamlined agreement. Offers in Compromise work the opposite way: they are means-tested, and higher income usually disqualifies you because the IRS calculates you can pay in full over time. Low-income taxpayers, with AGI at or below 250% of the federal poverty level, get the $205 OIC fee and the 20% down payment waived.

Does the Fresh Start program forgive tax debt?

Only one Fresh Start option reduces what you owe: the Offer in Compromise, and only when your assets and future income genuinely cannot cover the balance. The IRS accepted roughly one in five offers in fiscal year 2024. Payment plans and Currently Not Collectible status do not reduce the debt — interest and penalties keep accruing — though penalty abatement can remove specific penalties from the total.

How much does it cost to apply for Fresh Start?

A short-term payment plan (up to 180 days) has a $0 setup fee. Long-term installment agreements charge a setup fee that is lower when you apply online with direct debit and can be waived or reimbursed for low-income taxpayers. An Offer in Compromise costs a $205 application fee plus a 20% down payment on lump-sum offers — both waived with low-income certification.

Can I qualify for Fresh Start if I owe more than $50,000?

Yes, but not through the streamlined online process. Above $50,000 you either pay the balance down below the threshold or submit a financial statement (Form 433-F) so the IRS can set a payment based on your income and allowable expenses. Owing more than $50,000 also raises the stakes: a federal tax lien becomes more likely, and above $66,000 your passport can be at risk.

Does entering a Fresh Start program stop IRS levies and garnishments?

Generally, yes — the IRS does not levy while an installment agreement is in good standing, and levy action is generally suspended while an Offer in Compromise is under review. Relief is not instant in every case, and interest and penalties continue to accrue under every option. If a levy is already in motion, getting into a program quickly is usually the fastest legitimate way to get it released.

How long does the Fresh Start program take?

It depends on the option. An online streamlined payment plan can be approved the same day you apply. Currently Not Collectible status typically takes weeks of financial review. An Offer in Compromise routinely takes many months from filing to decision — and by law, if the IRS does not decide within two years, your offer is automatically accepted, with narrow exceptions: a returned or rejected offer stops the clock, and time during court disputes does not count.

Will the Fresh Start program remove a tax lien?

It can. Fresh Start raised the general lien-filing threshold to $10,000 and allows lien withdrawal (Form 12277) once you owe $25,000 or less and are on a direct-debit installment agreement in good standing, generally after a few consecutive payments. Paying or settling the debt also releases the lien. Until then, a recorded lien attaches to everything you own, including your home.

Your next 24 hours

- Pull your exact balance. Log into your IRS online account and write down the assessed total for every year, plus which years show a filed return — those two facts determine every threshold above.

- Gather three things: your most recent tax return, a current pay stub, and a rough list of your monthly living expenses. That's everything needed to run the streamlined-versus-433-F-versus-offer math.

- Get the math checked free. Use the 2-minute form or call (888) 825-7779 — an experienced tax professional will match your numbers to the right Fresh Start option before another month of penalties and interest gets added to the balance.

If you'd rather work with the government directly and can't get traction, the independent Taxpayer Advocate Service exists for cases the normal IRS channels are mishandling.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.