California Tax Debt

Is the FTB Worse Than the IRS? California vs. Federal Tax Collection in 2026

Is the FTB worse than the IRS? In most collection situations, yes. The California Franchise Tax Board can pursue a tax debt for 20 years — double the IRS's 10 — garnishes wages without a court order, adds its own collection fees to your balance, and offers fewer formal appeal rights before it levies.

Maybe you're assembling paperwork for a refinance and a $6,200 balance from Sacramento just became very relevant. Or you owe both agencies and keep hearing that California's collector is the meaner of the two. That reputation is mostly earned — and it should change which debt you tackle first and how fast you move.

⏱ The clock that's actually running: there's no single deadline on this question, but interest accrues on both balances every month, the FTB adds collection fees once enforcement starts, and California law lets the FTB pursue the debt for up to 20 years. Waiting doesn't run out either clock — it just raises the payoff.

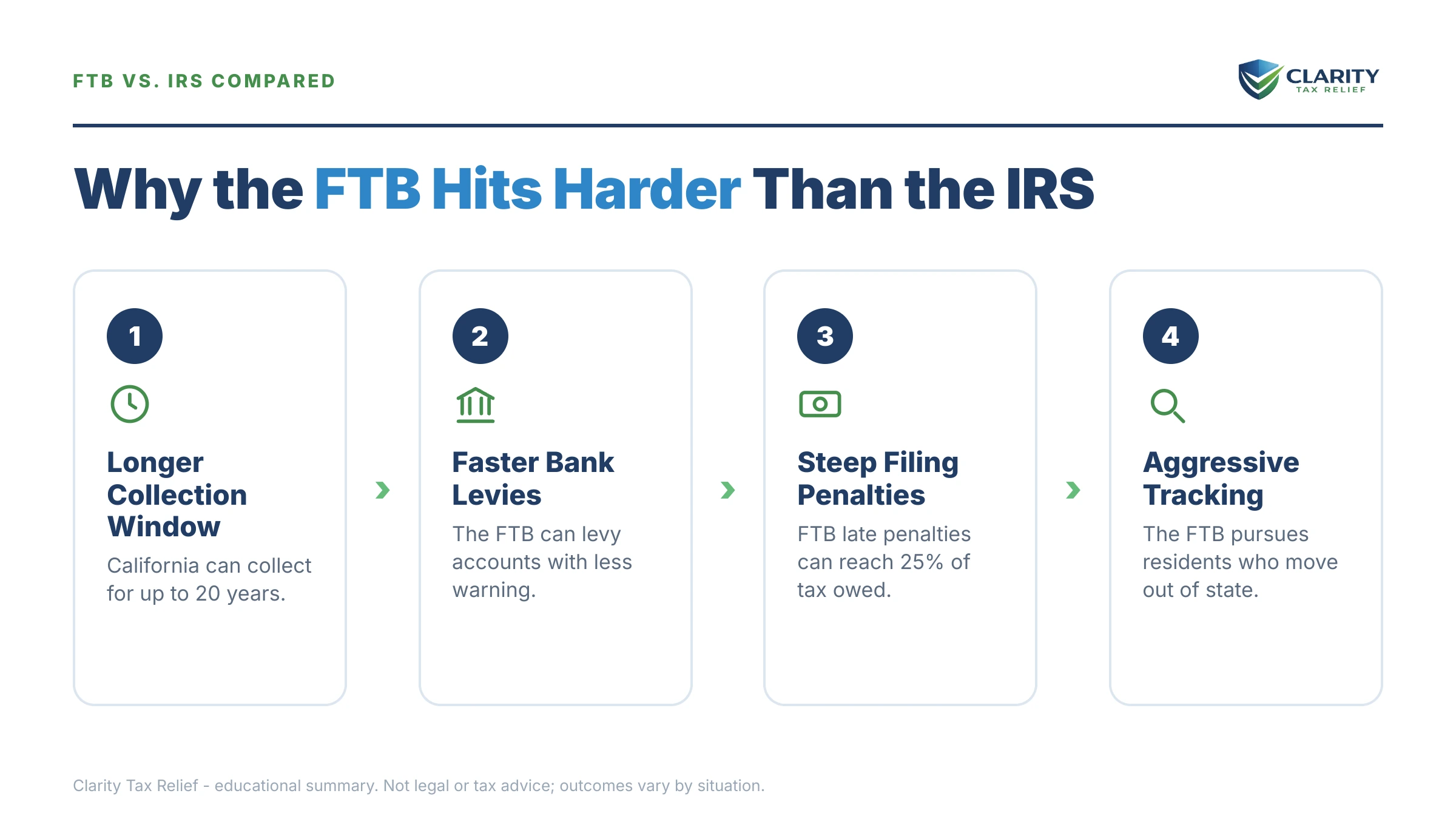

Why the FTB is worse than the IRS in collections: five structural differences

The California Franchise Tax Board can collect a tax debt for 20 years — twice the IRS's 10-year limit — and that's only the first of five ways it's the tougher collector.

1. The collection window is doubled. The IRS's Collection Statute Expiration Date (CSED) generally arrives 10 years after assessment. Under California Revenue & Taxation Code §19255, the FTB gets 20. Our guide to California's 20-year collection statute covers how that clock runs and what can extend it.

2. Fewer warnings before enforcement. Before the IRS can levy wages or a bank account, it must issue a final notice — an LT11 or Letter 1058 — that opens a 30-day window to request a Collection Due Process hearing on Form 12153. The FTB sends its own pre-levy notice, but California doesn't give you a federal-style CDP hearing; your dispute paths run through the FTB itself and, for the underlying tax, the state's Office of Tax Appeals.

3. Garnishment without a courtroom. The FTB sends an Earnings Withholding Order for Taxes straight to your employer — no lawsuit, no judgment. See what an FTB wage garnishment looks like in practice and how much the FTB can garnish from a paycheck.

4. Your balance grows by more than interest. Both agencies charge interest, but the FTB also tacks its own cost-recovery charges onto your account once collection activity begins — covered in our guide to FTB collection fees. Ignoring the FTB literally makes the bill bigger in ways the IRS's process doesn't.

5. Public and licensing pressure. The FTB publishes a Top 500 delinquent taxpayers list, and landing on it can trigger consequences for state-issued licenses. It can also suspend a delinquent LLC or corporation. The IRS has no public shaming list and no state license lever.

| Collection issue | IRS | California FTB |

|---|---|---|

| How long they can collect | 10 years from assessment (the CSED), pausable by appeals, offers, or bankruptcy | 20 years under R&TC §19255 — double the federal window |

| Warning before a levy | Multi-notice sequence ending in a final notice (LT11/1058) with a 30-day right to a Collection Due Process hearing | Its own final notice with a short response window; no federal-style CDP hearing — disputes run through the FTB and the Office of Tax Appeals |

| Wage garnishment | Only after the final-notice process; a portion of pay is exempt by table | Earnings Withholding Order sent directly to your employer — no court judgment needed |

| Costs added to the debt | Penalties, interest, and setup fees on some payment plans | Penalties, interest, plus its own collection cost-recovery fees once enforcement begins |

| Public pressure | No public delinquency list | Public Top 500 delinquent list, with license consequences for those on it |

| Business consequences | Liens and levies on business assets | Can also suspend an LLC or corporation, freezing its legal right to operate |

Where the IRS is actually tougher

The IRS can certify your passport for revocation once your federal tax debt passes $66,000 in 2026 — a power the FTB doesn't have. Honesty matters in this comparison, and the federal side wins a few categories.

The IRS can also take up to 15% of Social Security benefits through the Federal Payment Levy Program, and its criminal enforcement arm has a longer reach than any state agency's. Federal balances tend to be larger, too, so the same taxpayer often has more raw dollars at risk with the IRS.

And one 2026 wrinkle cuts both ways: the IRS workforce shrank roughly 27% in 2025, which makes reaching a human harder — but its automated levy systems never stopped. Neither agency's computer takes a day off, which is why "harder to reach" never means "safe to ignore."

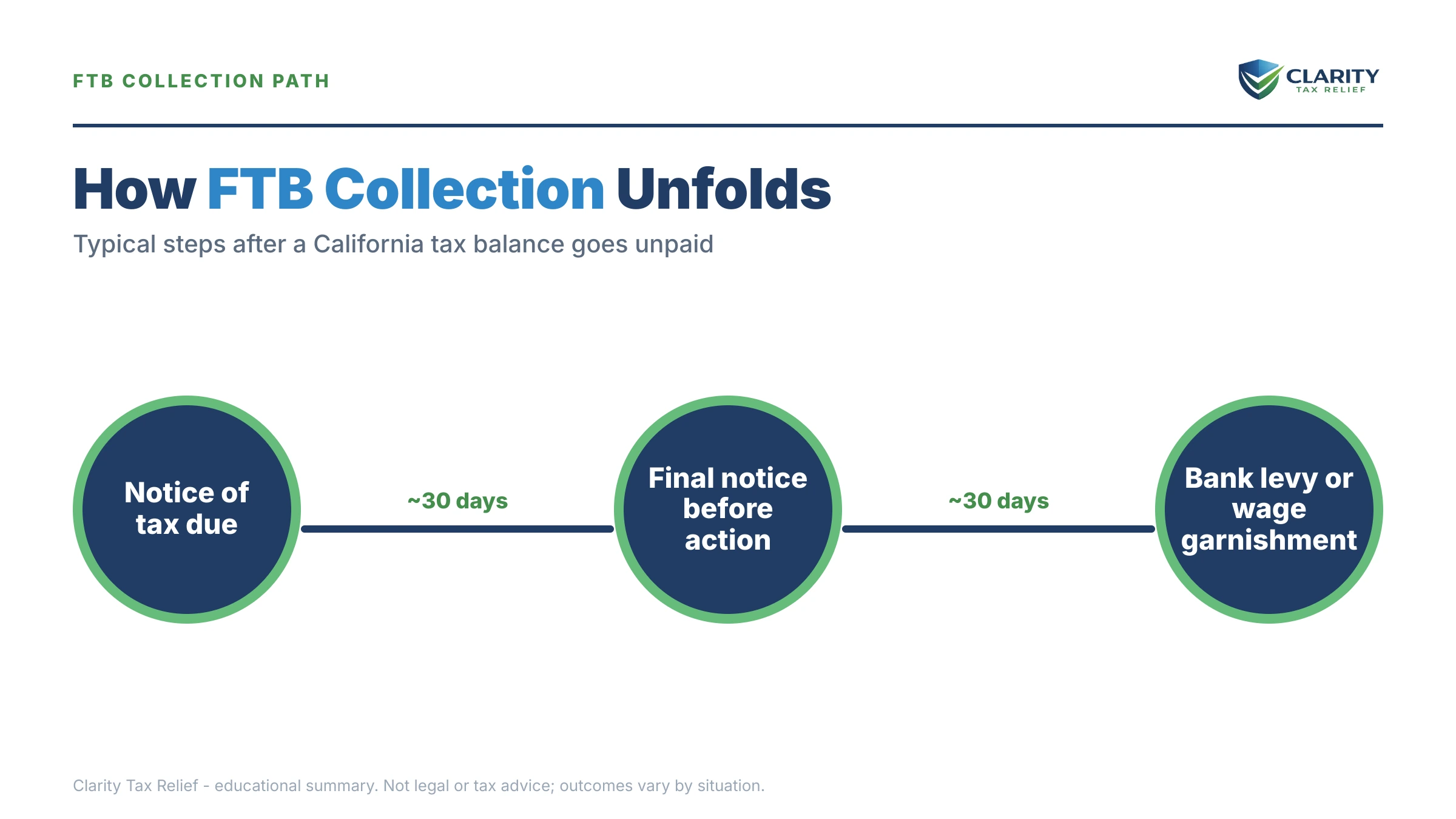

What happens if you ignore the FTB vs. the IRS

An ignored FTB balance typically reaches a wage order or bank levy in fewer steps than the same balance at the IRS. Here is the stage order on the California side — the exact response window is printed on each notice, so pull yours out and check the date:

- Balance assessed — from your filed return, an FTB adjustment, or an assessment the FTB built from wage data after a demand to file.

- Statement of Tax Due / demand for payment — the bill stage. Interest is accruing, but no enforcement yet.

- Final notice before levy — the FTB's intent to levy warning. This is the last off-ramp before enforcement, and collection fees start attaching around this stage.

- Enforcement — an Earnings Withholding Order to your employer, an Order to Withhold on your bank account (see FTB bank levy), and a Notice of State Tax Lien recorded with your county.

- Ongoing pressure — state refund intercepts every year, fees compounding the balance, and for large debts, the Top 500 list and license actions.

The IRS runs a longer runway for the same debt: CP14 bill, CP501/CP503 reminders, a CP504 that lets it take your state refund, and only then the LT11 final notice that opens levy power after 30 days. The FTB compresses that sequence — which is exactly why California debts blindside people who assume "the government moves slowly."

Owe the FTB — or the FTB and the IRS at once?

Get both balances reviewed free before enforcement starts and collection fees stack onto what you owe. An experienced tax professional will map which clock is shorter and the cheapest way to stop both — no pressure, no obligation.

Your options with each agency, side by side

Both agencies offer payment plans, hardship status, penalty relief, and an offer in compromise — but the terms differ, and an approval from one binds only that one. Resolving your IRS balance does nothing for Sacramento, and vice versa; you need a plan for each. The general playbook for negotiating a tax debt on your own lives in our guide to how to settle tax debt yourself — here's how the two agencies' versions compare:

| Option | IRS version | FTB version |

|---|---|---|

| Pay in full | Stops the penalty clock and the notice sequence; free online | Stops fee accrual and enforcement; paid through the FTB's online system |

| Short-term full payoff | Up to 180 days, $0 setup fee | No mirror-image program — the FTB sets its own arrangement terms; ask before assuming |

| Monthly payment plan | ≤ $10,000: guaranteed installment agreement; ≤ $50,000: up to 72 months, set up online | Own program with its own balance and term limits — see FTB payment plans |

| Offer in compromise | $205 fee (waived for low-income applicants); roughly 1 in 5 offers accepted in FY2024 | Separate application and stricter ability-to-pay standard — see FTB offer in compromise |

| Hardship pause | Currently Not Collectible status; the debt remains and interest accrues | The FTB has its own hardship deferral with its own financial review |

| Penalty relief | First-Time Abate (becoming automatic as AEP starting summer 2026); reasonable cause | Reasonable-cause relief, plus a one-time abatement for certain timeliness penalties — see FTB penalty abatement |

Two option-level takeaways. First, on smaller balances the IRS is genuinely accommodating: under $10,000 with clean filing compliance, an installment agreement is available as a matter of right. Second, don't assume an FTB settlement is realistic just because you've read about IRS offers — the FTB settles less readily, and each application stands alone.

A worked example: $6,200 to the FTB with a refinance on the line

Say you owe the FTB $6,200 from an adjusted 2023 California return, and you plan to apply for a refinance in about four months. This is hypothetical, but the mechanics are exactly what a homeowner in this spot faces:

- Path A — pay before you apply. $6,200 paid in full means no lien to surface on the title search and no monthly obligation for the underwriter to count against your debt-to-income ratio. Cleanest outcome if you have the cash.

- Path B — payment plan now. Spread over 12 months, $6,200 ÷ 12 ≈ $517/month; over 24 months, ≈ $259/month, with interest continuing on the shrinking balance. A plan in good standing generally lowers the odds of a lien filing, though it doesn't guarantee the FTB won't record one — ask when you set it up, and get the terms in writing for your lender's file.

- Path C — do nothing. The final notice arrives, a Notice of State Tax Lien gets recorded at the county, and now the title search flags it. Your lender will demand a payoff — the $6,200 plus accrued interest and collection fees — handled through escrow before or at closing, and the lien-release paperwork can add weeks to your timeline.

For contrast: the same $6,200 owed to the IRS sits comfortably under the $10,000 guaranteed installment agreement line, and the IRS typically reserves lien filings for larger balances. Same dollar amount, meaningfully different risk — which is the whole answer to this article's question in one example. If your debt is federal instead, start with buying a house while owing the IRS and the best way to pay the IRS.

How to respond when you owe the FTB (and maybe the IRS too), step by step

- Pull your balances from both agencies — register for a MyFTB account and an IRS online account, and compare what each system shows against the notices you received. You cannot pick a strategy until you know both numbers and both stages.

- File any missing returns — both agencies escalate against non-filers, and the FTB can assess you from wage and 1099 data — with penalties added — if you ignore a demand to file. Filing first also unlocks payment plans on both sides.

- Choose the resolution that fits each balance — match each balance to the options table above: pay in full, a payment plan, hardship status, penalty relief, or an offer in compromise. At a few thousand dollars, a payment plan usually takes days to set up, not months.

- Address the faster clock first — that is usually the FTB, unless the IRS has already issued a final notice of intent to levy — the 30-day federal appeal window then comes first. Put the second agency on a plan so it stops escalating while you work the first.

- Get help if enforcement has already started — a wage order, bank levy, or recorded lien — especially with a refinance pending — is the point where an experienced tax professional changes outcomes, because release requests and lien handling have to be sequenced correctly.

For a deeper decision framework on sequencing the two agencies, see FTB vs IRS which first.

Can you wait out the FTB like the IRS's 10-year rule?

No — California gives the FTB 20 years to collect, so the "run out the clock" logic that occasionally applies to old federal debt fails on the state side. Even the federal 10-year CSED is pausable by appeals, a pending offer, or bankruptcy, so it's rarely the escape hatch people hope for; you can estimate where your federal clock stands with our CSED Calculator.

Run the arithmetic on the state side: two decades of interest and collection fees on even a $6,200 balance dwarfs the cost of a 12- or 24-month payment plan today. On FTB debt, resolution is almost always cheaper than patience.

When you can handle this yourself — and when help changes the outcome

Plenty of FTB and IRS balances need no professional at all. If you agree with the balance, can pay it within a few months, and no lien or levy is in motion, set up the payment plan yourself through MyFTB or the IRS's online tools and move on — that's the whole job.

Experienced help earns its cost in specific situations: an Earnings Withholding Order or bank levy already in effect, a recorded lien colliding with a refinance or sale timeline, multiple unfiled years on either side, a balance you dispute, or debts to both agencies at once where the sequencing itself determines what you pay. Those are cases where the order of operations — release, plan, lien handling, penalty relief — matters more than any single form.

If your situation is broader than one balance, the California FTB back taxes hub maps every FTB scenario in one place.

Terms you'll see, decoded

- CSED — the IRS's Collection Statute Expiration Date, generally 10 years after a federal tax is assessed.

- R&TC §19255 — the California statute giving the FTB 20 years to collect a final tax liability.

- Earnings Withholding Order for Taxes (EWO) — the FTB's wage garnishment, sent directly to your employer without a court judgment.

- Order to Withhold — the FTB's levy on a bank account or other funds held by a third party.

- Notice of State Tax Lien — the FTB's recorded claim against your property; it's what shows up on a title search. Details in our FTB tax lien guide.

- Collection Due Process (CDP) — the federal hearing right (requested on Form 12153) the IRS must offer before levying; California has no direct equivalent.

Primary sources if you want them straight from each agency: the California Franchise Tax Board for state balances and payment options, the IRS payment plans page for federal arrangements, and the Taxpayer Advocate Service if an IRS process is causing hardship the normal channels won't fix.

FTB vs. IRS questions, answered

Is the FTB more aggressive than the IRS?

In collections, generally yes. The FTB moves from notice to enforcement in fewer steps, garnishes wages through an Earnings Withholding Order without any court judgment, and adds its own collection fees to your balance once enforcement begins. The IRS is slower and must send a final notice with a 30-day right to a hearing before levying — the FTB offers no equivalent federal-style hearing.

Does FTB tax debt expire like IRS debt does?

Not for a very long time. The IRS generally has 10 years from assessment to collect, but under California R&TC §19255 the FTB can collect for 20 years — and certain events can pause even that clock. Waiting out the FTB is not a realistic strategy for most people; almost any resolution option costs less than two decades of interest and fees.

Can the FTB garnish my wages without going to court?

Yes. The FTB issues an Earnings Withholding Order for Taxes directly to your employer — no lawsuit and no court judgment required. Your employer is legally obligated to comply. The order stays in place until the debt is paid or the FTB releases it, which usually means setting up a payment plan or documenting financial hardship.

Does the FTB have an offer in compromise program?

Yes, but it is completely separate from the IRS program, with its own application and its own standards. The FTB generally settles only when you have no realistic ability to pay the balance in full now or in the foreseeable future. Acceptance is the exception, not the rule — and an accepted IRS offer does not obligate the FTB to match it, or vice versa.

If I owe both the FTB and the IRS, which should I pay first?

There is no universal answer, but the FTB's speed often makes it the more urgent fire: it garnishes and levies with fewer warning notices and can collect for 20 years. The exception is when the IRS has already issued a final notice of intent to levy — that 30-day clock takes priority. Whichever agency you address second, get at least a payment plan in place so neither one escalates.

Can the FTB take my federal tax refund?

It can request it. Through the federal Treasury Offset Program, state tax agencies — including the FTB — can ask the U.S. Treasury to apply your federal refund to a state income tax debt. The reverse also happens: the IRS can take your California refund for a federal debt. A refund offset can occur even while you are still receiving ordinary collection notices.

Will an FTB balance stop my mortgage refinance?

An unpaid balance alone usually won't, but a recorded state tax lien often will. Liens appear on the title search, and most lenders require the lien to be paid or formally addressed before closing. If you are planning a refinance, resolving the FTB balance — or at least preventing a lien filing by getting a payment plan in place — before you apply is the safer sequence.

Your next 24 hours

- Pull out every notice from both agencies and find the balance and any "final notice" or "intent to levy" language — that tells you which clock is shortest and which agency moves first.

- Gather your last filed federal and California returns, recent pay stubs, and the notices themselves — that's everything needed to price a payment plan or spot missing returns on either side.

- Get a free case review — use the 2-minute form or call (888) 825-7779. An experienced tax professional will compare your FTB and IRS positions and map the cheapest sequence to resolve both, before interest and California's collection fees add to what you owe.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.