California State Taxes

FTB Payment Plan: How to Set One Up With California in 2026

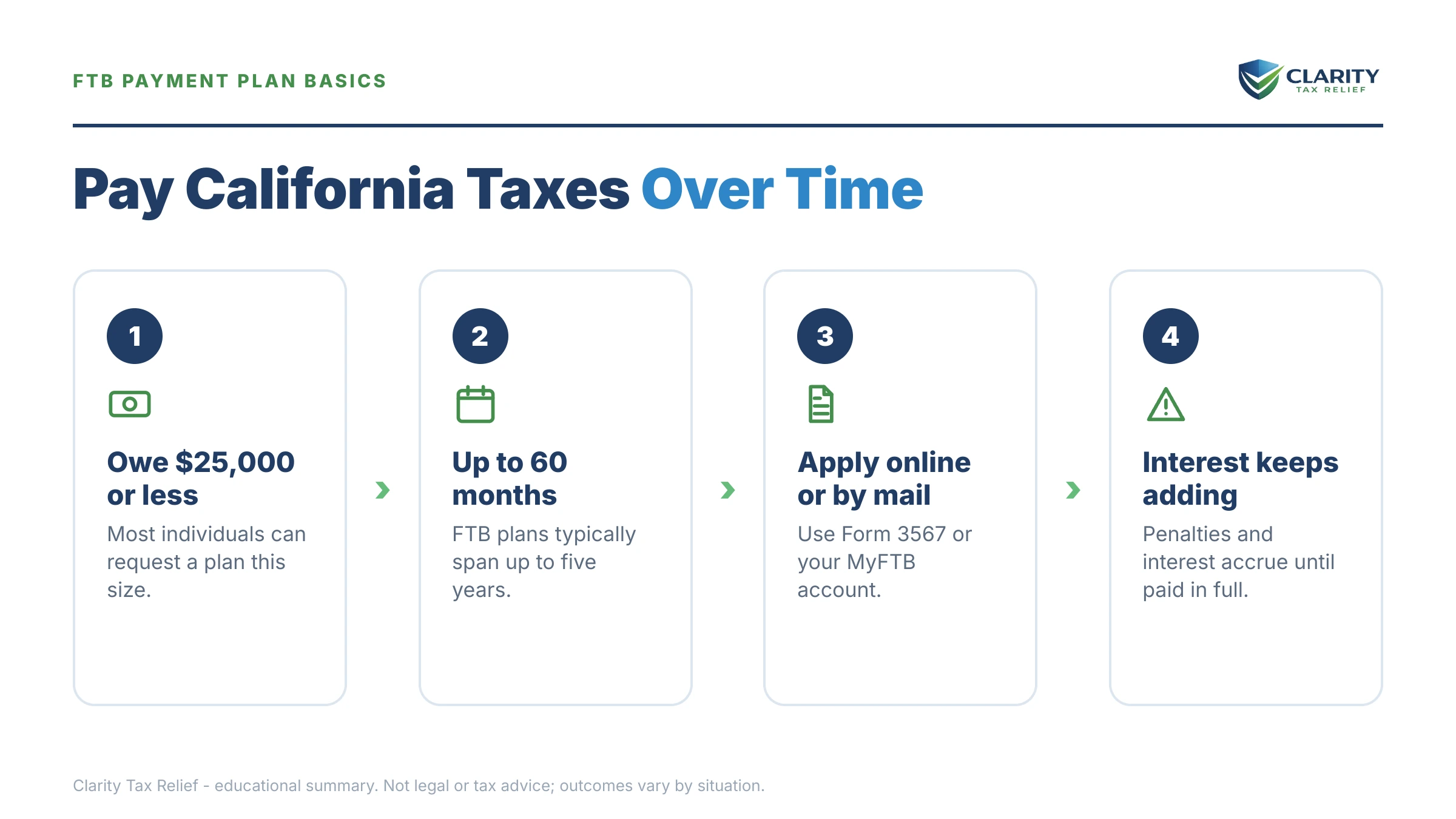

The short answer: an FTB payment plan (installment agreement) lets you pay California income tax debt in monthly payments. Individuals who owe $25,000 or less, can pay within 60 months, and have filed all required returns can usually apply online in minutes. The FTB adds a $34 fee to your balance, and interest keeps accruing until it's paid.

The envelope isn't from the IRS — it's from Sacramento, and the Franchise Tax Board is telling you it intends to take money from your paycheck or bank account. You rent, there's no $48,000 sitting in savings, and the state wants an answer before the date on that notice. The fix is more routine than the letter sounds: the FTB approves monthly payment plans every day, and an approved plan is usually what switches the levy machine off.

This guide covers who qualifies for an FTB payment plan under the $25,000 / 60-month rule, what it costs, what to do when your balance is bigger than the streamlined limit, and how California's plan differs from a federal one. The image below shows the application path at a glance — where the $25,000 line falls and which door your balance puts you through.

⏱ Your deadline: there is no fixed deadline to request an FTB payment plan — but if you've received an FTB intent to levy notice, the controlling date is printed on that notice, and you need the plan requested before it passes. Either way, interest accrues on the balance every day, and collection fees stack on top the longer the account sits in collections.

Who qualifies for an FTB payment plan: the $25,000 / 60-month rule

The FTB approves streamlined individual payment plans when you owe $25,000 or less and can pay the balance within 60 months. Meet those two numbers — and have every required California return filed — and approval is close to routine. You apply online through your MyFTB account, by phone, or by mailing form FTB 3567, the Installment Agreement Request.

Approval comes with conditions the FTB enforces strictly:

- Payments run by automatic bank withdrawal. FTB installment agreements are paid by electronic funds withdrawal from your checking account — there's no "mail a check each month" version to fall behind on.

- A $34 setup fee is added to your balance rather than charged up front.

- Interest keeps accruing on the unpaid balance for the life of the plan. The plan stops enforcement, not the meter.

- Your state refunds get intercepted and applied to the debt every year until it's gone — and they don't count as your monthly payment.

- You must stay compliant going forward. A late return or a new unpaid balance in a future year can default the agreement.

- The FTB can still record a state tax lien in some cases even with an approved plan, which becomes public record.

Owe more than $25,000, or need longer than 60 months? A plan is still possible — it just moves from "automatic" to "negotiated," built on the financial statement covered in the options section below. Business entities are a different track entirely: the FTB generally requires businesses to call and negotiate directly, on shorter and stricter terms than individuals get (the business IRS installment agreement rules don't carry over to the state either).

One scope note that trips up a lot of Californians: the FTB only collects income tax. If you owe sales tax, that's a CDTFA payment plan; payroll tax debt runs through an EDD payment plan. Each agency has its own rules, and a plan with one does nothing to stop the others.

What happens if you don't set one up

An unresolved FTB balance moves through an automated collection sequence that ends in wage garnishment and bank levies — and California's version moves with less warning than the IRS's. The stages run in this order:

- Balance due and demand notices. The FTB bills you, and penalties and interest accrue from the original due date.

- Collection fees get added. Once the account moves into active collections, the FTB tacks its cost-recovery fees onto the balance — you now owe more for having waited.

- A state tax lien is recorded. Filed with the county recorder, it attaches to property you own now or acquire later and is fully public record.

- Final intent-to-levy notice. This letter carries a printed deadline. After it, the FTB doesn't need your permission or a court order to take money.

- Orders to Withhold and wage garnishment. An Order to Withhold freezes and takes funds from your bank account — an FTB bank levy moves on a far shorter hold than the IRS's 21-day version. An Earnings Withholding Order for Taxes goes to your employer and takes a slice of every paycheck until the debt is paid; see how much can FTB garnish.

- Long-tail enforcement. Refund intercepts continue every year, and the state's largest debtors face publication on the Top 500 list with professional and driver's license suspension attached.

And unlike the IRS, waiting the state out is a two-decade proposition: California has 20 years to collect under R&TC §19255 — the full breakdown is in our guide to California's 20-year collection statute. A renter isn't insulated, either. No house means no lien target on real estate, but paychecks and bank accounts are exactly what the FTB's automated levies reach first.

FTB levy notice in hand?

Get your FTB notice reviewed free before the date printed on it passes. An experienced tax professional will tell you whether a payment plan, hardship status, or an offer is the right move for your balance — no pressure, no obligation.

Your options for an FTB balance, compared

A payment plan is the most common resolution for FTB debt, but it isn't the only one — and above $25,000, it isn't even the automatic one. Here's the full menu:

| Option | Upfront cost | Timeline | The catch |

|---|---|---|---|

| Pay in full | The balance | Immediate | Stops interest and enforcement, but drains cash; penalty relief may still be worth pursuing after. |

| Streamlined payment plan (≤ $25,000) | $34 fee added to balance | Up to 60 months | Interest continues; refunds intercepted; automatic bank withdrawal required. |

| Financial-statement plan (over $25,000) | $34 fee; documentation of income/expenses | Terms set case-by-case after review | The FTB sets the payment from FTB form 3561, not from what feels comfortable. |

| Hardship status | $0, but full financial disclosure | Reviewed periodically | Collection pauses; the debt and interest don't. See FTB currently not collectible. |

| Offer in compromise | Full financial disclosure | Months to decide | Only for genuine inability to ever pay; the FTB offer in compromise is stricter than the IRS version and generally expects no reasonable prospect of paying in full. |

Which door you walk through mostly depends on the size of the balance:

| Balance owed | Realistic path | What to watch |

|---|---|---|

| Under $10,000 | Streamlined online plan — roughly $170+/month clears $10,000 in 60 months | Shorter terms cost less in interest; pay it off early if you can. |

| $10,000–$25,000 | Streamlined plan, still online | Lien risk rises with balance size; the plan doesn't guarantee no lien. |

| $25,001–$100,000 | Financial-statement plan via FTB 3561; hardship or OIC if the numbers show you can't pay | How you present income and expenses drives the monthly payment. |

| Over $100,000 | Negotiated plan with active FTB collections involvement | Top 500 delinquent list exposure and license suspension; professional representation usually pays for itself here. |

Say you owe the FTB $48,300: a worked example

Say you owe the FTB $48,300 across two tax years, you rent, and a levy notice just arrived. Here's the realistic math — hypothetical numbers, shown so you can run your own:

- Streamlined plan: not available. $48,300 is nearly double the $25,000 line, so the online 60-month plan is off the table as-is.

- Financial-statement plan: you complete FTB 3561 with your income, rent, and necessary expenses. Suppose the review shows $950/month available after essentials. $48,300 ÷ $950 ≈ 51 months of principal alone — and because interest keeps accruing, the real payoff runs somewhat longer than that.

- The pay-down move: paying the balance down by $23,300 — to $25,000 — would unlock the streamlined plan at $25,000 ÷ 60 ≈ $417/month, no financial review. Most renters facing a levy can't produce $23,300, but if a family loan or asset sale is possible, this converts a negotiated case into a routine one.

- If $950/month doesn't exist: when the 3561 shows nothing left after necessities, hardship status — not a plan you'll default on — is the honest answer. And if your assets and future income genuinely can't cover $48,300 within the collection period, an offer in compromise is worth pricing out before signing up for years of payments.

The levy piece matters most: requesting the plan before the date on the intent-to-levy notice is what generally keeps the Order to Withhold from ever reaching your bank. After that date, you're negotiating for a release instead of preventing a seizure — a much weaker position.

How to set up an FTB payment plan, step by step

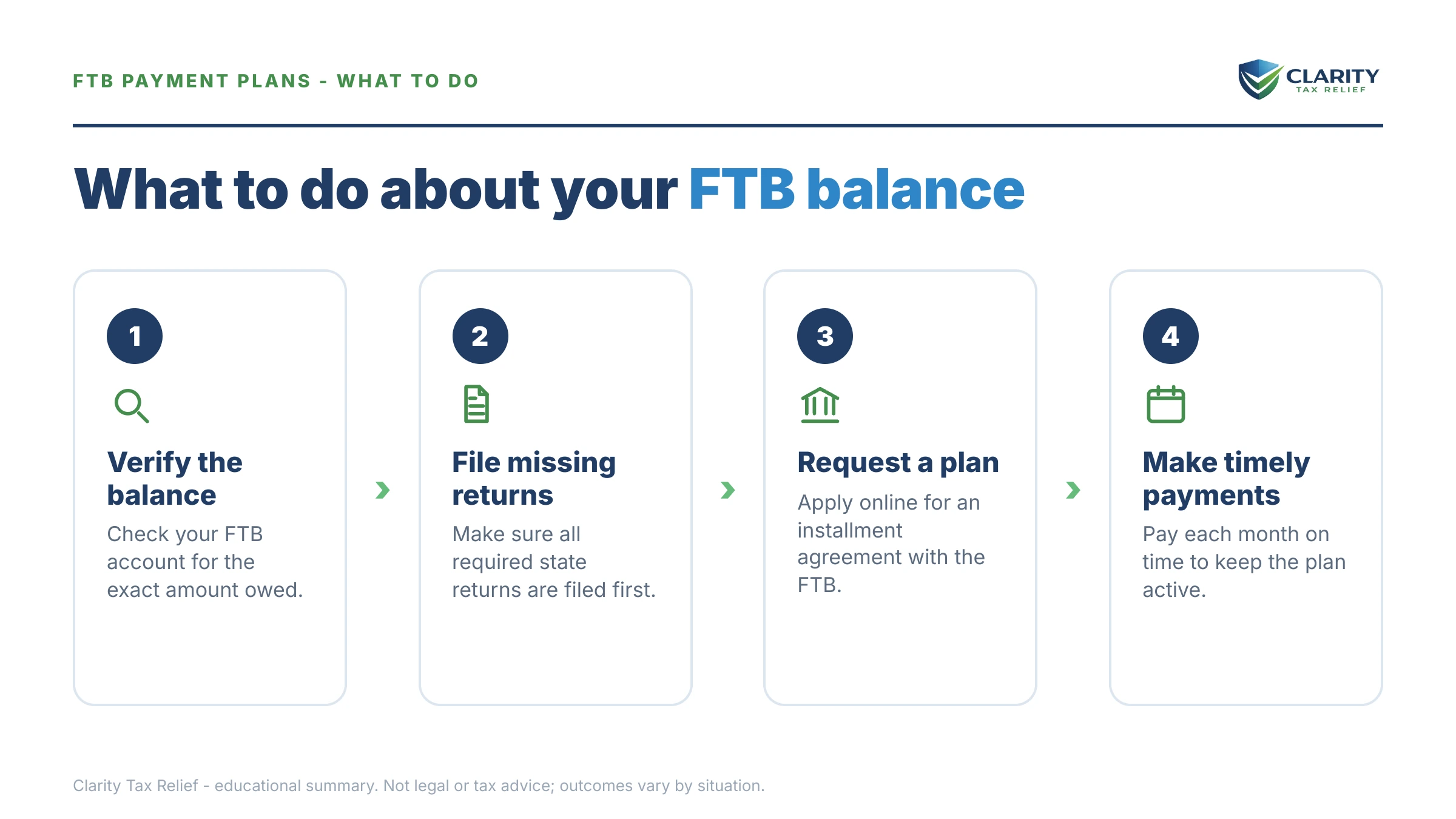

- Confirm every required return is filed. The FTB will not approve a payment plan with missing returns. If you've received a Demand to File, resolve it first — file the actual return even if the FTB already estimated a balance for you.

- Check the $25,000 / 60-month test. Owe $25,000 or less and able to pay within 60 months? You likely qualify for the streamlined plan. Owe more? Gather pay stubs, rent, and bank statements now — you'll need them for FTB 3561.

- Apply online through your MyFTB account, or call the number on your notice. The online application takes minutes for streamlined cases. If an intent-to-levy notice is in play, call instead — a phone request gets a hold on enforcement noted faster than a mailed FTB 3567.

- Set up the automatic bank withdrawal. FTB plans are paid by electronic funds withdrawal from your bank account. Pick a due date that lands after your paycheck clears, and note the $34 fee the FTB adds to your balance.

- Stay current going forward. File and pay every future California return on time and keep enough in the account for each withdrawal. A new balance in a later year can default the entire agreement.

FTB payment plan vs. IRS payment plan: the differences that cost money

California's installment agreement is tighter than the federal one on almost every dimension — a $30,000 balance that fits the IRS's online plan does not fit the FTB's. If you owe both, the differences decide sequencing (our step-by-step on the IRS payment plan online covers the federal side, and the IRS payment plan changes 2026 guide covers what shifted this year):

| Feature | FTB (California) | IRS (Federal) |

|---|---|---|

| Streamlined/online threshold | $25,000 or less | Up to $50,000 online |

| Maximum standard term | 60 months | Up to 72 months |

| Setup fee | $34, added to balance | Varies by method; $0 for short-term plans up to 180 days |

| Collection statute | 20 years (R&TC §19255) | 10 years from assessment (with tolling) |

| Payment method | Automatic bank withdrawal, generally required | Direct debit required on larger streamlined balances |

| Refunds during the plan | State refunds intercepted and applied | Federal refunds applied to the balance |

The practical takeaway: the same dollar owed to the state demands a higher monthly payment (60 months vs. 72), survives twice as long on the books, and hits the streamlined ceiling at half the balance. That's a big part of why practitioners consider the FTB the harsher collector — and why the state balance often deserves attention first when money is limited.

When you can handle this yourself

If you owe the FTB $25,000 or less, your returns are filed, and the balance is correct, set up the plan yourself — the online application is genuinely simple, and no firm should charge you for it.

Experienced help changes outcomes in a narrower set of situations: a levy or garnishment already in motion, a balance over $25,000 where the FTB 3561 presentation determines your payment for years, unfiled California returns (especially where the FTB estimated your income and inflated the balance), simultaneous IRS and FTB debt that needs sequencing, or a financial picture weak enough that hardship status or an offer beats any plan. In those cases, the question isn't whether you can get a plan — it's whether the plan you'd get on your own is the right resolution at the right number.

Terms on your FTB notice, decoded

- Installment agreement — the FTB's official name for a payment plan; monthly automatic withdrawals until the balance, penalties, and interest are paid.

- FTB 3567 — the paper Installment Agreement Request form; the mail-in alternative to applying online.

- FTB 3561 — the financial statement the FTB uses to set payments on balances over $25,000 or terms beyond 60 months.

- Earnings Withholding Order for Taxes (EWOT) — the FTB's wage garnishment order, sent to your employer and continuous until released or paid.

- Order to Withhold — the FTB's bank levy; it freezes funds in your account and sends them to the state after a short hold.

- Collection cost recovery fee — a fee the FTB adds to your balance when the account enters active collections, on top of penalties and interest.

- R&TC §19255 — the California statute giving the FTB 20 years to collect, twice the federal window.

FTB payment plan questions, answered

Does the California FTB offer payment plans?

Yes. The Franchise Tax Board offers installment agreements that let you pay a state income tax balance in monthly payments. Individuals who owe $25,000 or less, can pay in full within 60 months, and have filed every required return can usually apply online and get an answer quickly. Larger balances require a financial statement and FTB approval.

How long can an FTB payment plan last?

The standard individual plan runs up to 60 months — five years. That's shorter than the IRS's 72-month online plan, so the same balance costs more per month with the state. If you owe more than $25,000 or genuinely can't pay it off in 60 months, the FTB can approve different terms, but only after reviewing a completed FTB 3561 financial statement.

How much does an FTB payment plan cost to set up?

The FTB adds a $34 installment agreement fee to your balance — you don't pay it out of pocket up front. Interest continues to accrue on the unpaid balance for the life of the plan, and any penalties already assessed stay in the balance. The plan stops enforced collection, not the interest clock.

Will an FTB payment plan stop a wage garnishment or bank levy?

An approved plan generally stops new levies, but it does not automatically undo one already in motion. If an Earnings Withholding Order has reached your employer or an Order to Withhold has hit your bank, you or your representative must ask the FTB to modify or release it — and bank levy funds move fast, so call before the date on your notice, not after.

What if I owe the FTB more than $25,000?

You can still get a payment plan — it just isn't automatic. You'll complete FTB 3561, a financial statement listing your income, expenses, and assets, and the FTB sets a payment based on what it shows. Another path: if you can pay the balance down to $25,000 or less, you may qualify for the streamlined 60-month plan without the financial review.

Does the FTB keep my tax refunds while I'm on a payment plan?

Yes. The FTB applies your California state refunds to the balance every year until it's paid, and an intercepted refund does not replace your monthly payment — you still owe it that month. Federal refunds can also be intercepted for state debt through the offset program, so plan on seeing no refund until the balance is gone.

What happens if I miss an FTB payment plan payment?

A missed payment puts the agreement at risk of termination, and once a plan terminates, enforced collection — levies, garnishment, refund intercepts — can resume on the full remaining balance. If you know a payment will bounce, call the FTB before the due date; keeping the state informed is usually the difference between a skipped beat and a defaulted plan.

Does FTB tax debt ever expire?

Eventually — but California gives itself 20 years to collect under Revenue and Taxation Code Section 19255, double the IRS's 10-year window. Waiting out the FTB is rarely a realistic strategy, especially since liens, garnishments, and refund intercepts continue the whole time. A payment plan or offer in compromise almost always costs less than two decades of accrual.

Your next 24 hours

- Find the date and total balance on your most recent FTB notice. If it's an intent-to-levy notice, that printed date — not some general grace period — is your clock.

- Gather three things: your last California return, the notice itself, and a recent pay stub or income record. That's everything the online application or FTB 3561 will ask for.

- Get a free case review before that notice date passes — use the 2-minute form or call (888) 825-7779. An experienced tax professional will confirm whether a plan, hardship status, or an offer is the right resolution at your balance, before the FTB decides for you.

Primary sources: the California Franchise Tax Board publishes its payment plan criteria and applications directly, and the federal comparison figures come from IRS.gov/payments.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.