California FTB

FTB Bank Levy: How to Stop It and Get Your Money Back (2026)

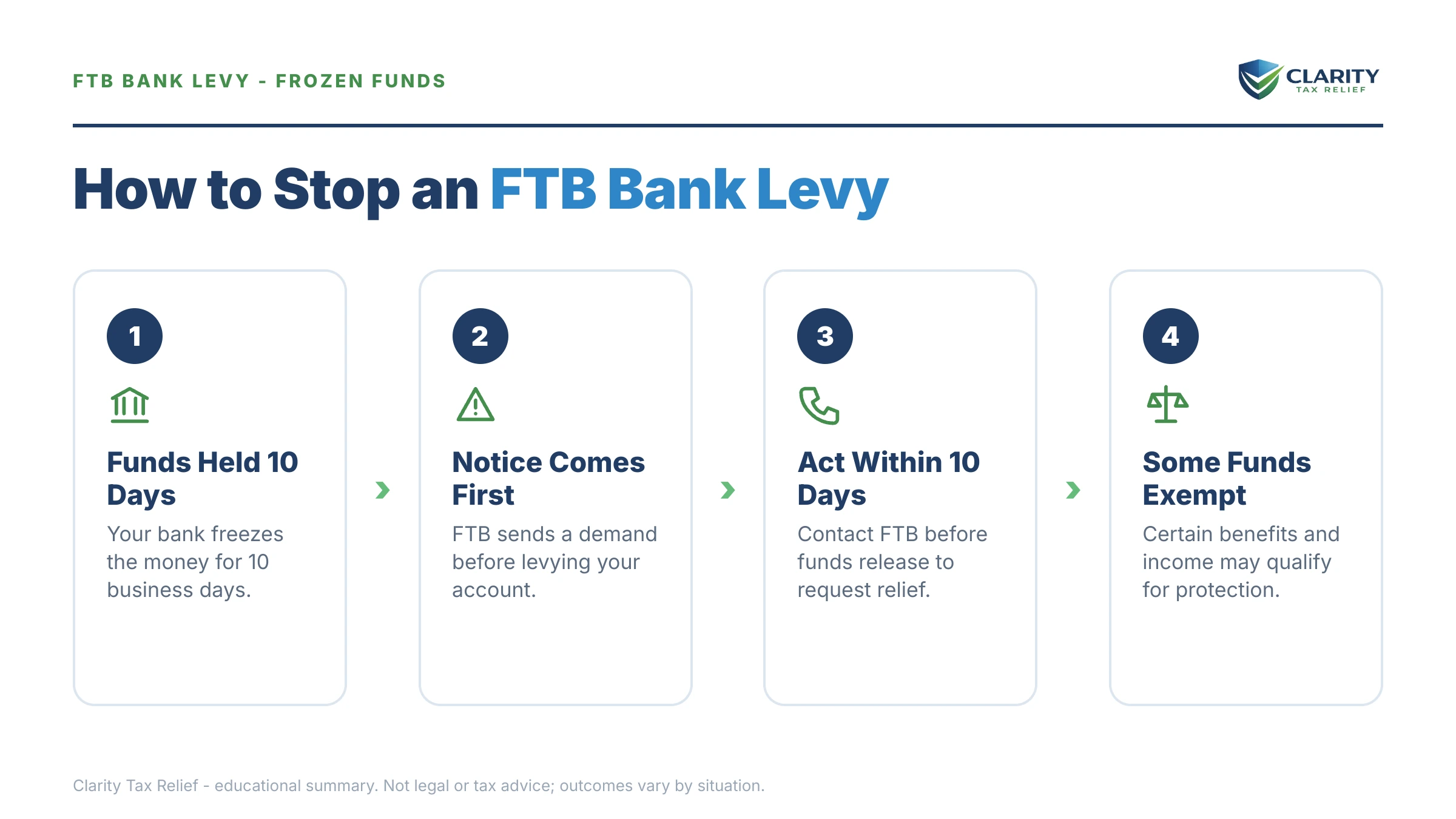

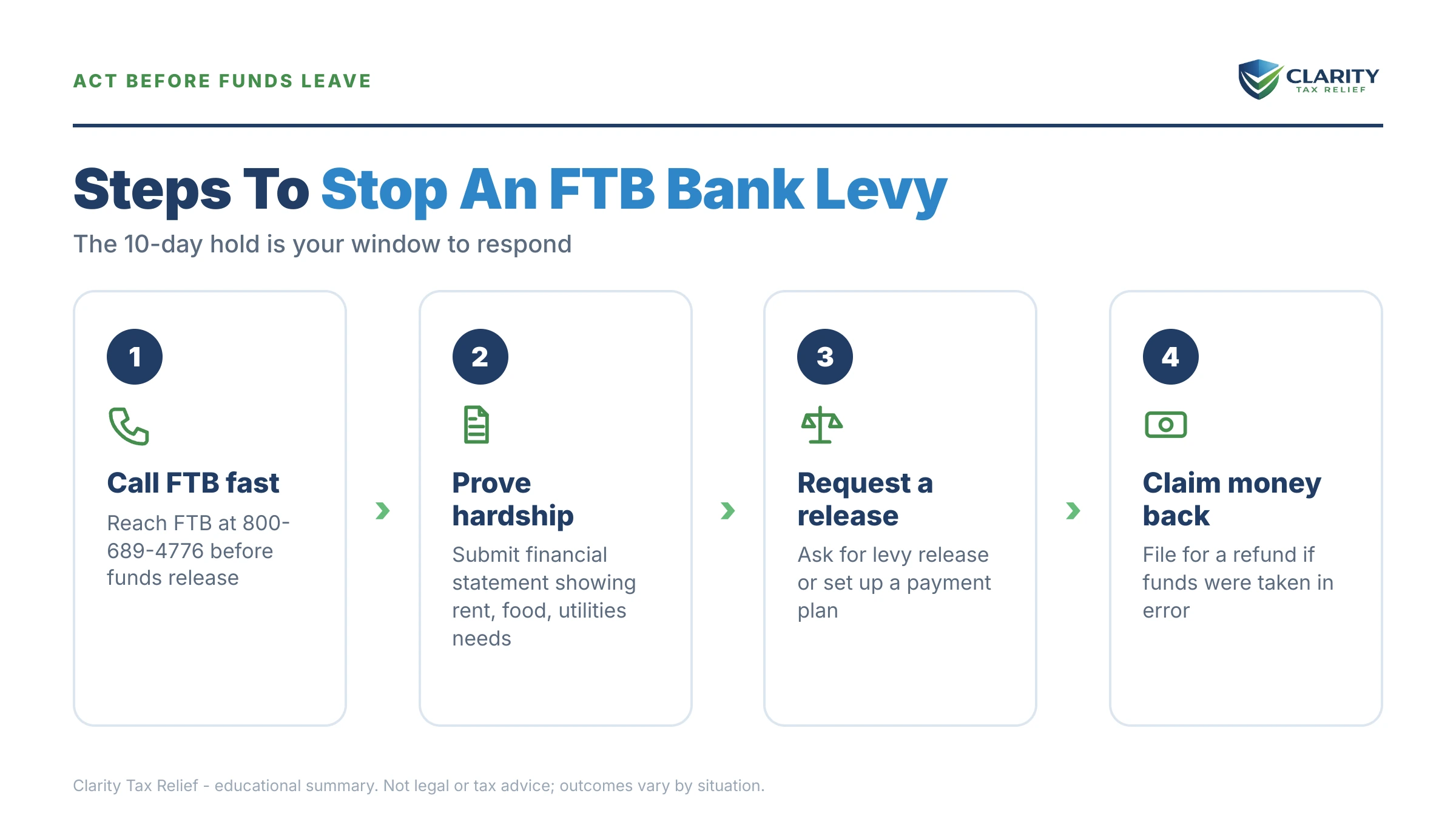

The short answer: an FTB bank levy — officially an Order to Withhold — is a one-time seizure of the money sitting in your account the day your bank processes it. The bank typically holds the frozen funds about 10 days before sending them to the Franchise Tax Board. That hold is your window to fight for a release.

You went to pay a subcontractor, or your rent, and the money wasn't there — just a "legal order" hold and a bank rep who could only say "contact the Franchise Tax Board." That lurch in your stomach is real, and so is this: the money may not be gone yet, and there is a short, specific sequence of moves that can still get some or all of it back.

This guide covers exactly how an FTB bank levy works, the hold window that controls everything, every release path California actually grants, and how to make sure a second levy never lands. The image below shows what the FTB's levy paperwork looks like and where to find the two details that matter most — the date and the balance.

⏱ Your real deadline: your bank typically holds levied funds for about 10 days after it receives the FTB's Order to Withhold, then remits them to the state. Call your bank today and get the exact date it received the order and the date the money goes out — every release argument is stronger before that transfer than after.

What an FTB bank levy is — and why you got one

An FTB bank levy is a legal order, called an Order to Withhold, that requires your bank to freeze and turn over the funds in your account, up to the balance you owe California. It is a snapshot, not a pipe: it grabs what's in the account when the bank processes it, and deposits that arrive afterward are not captured by that order.

You got one because the Franchise Tax Board's records show a final, collectible balance — and its mailed warnings went unanswered. For 1099 workers, the trigger is often not a return you filed at all. California receives your 1099 data through IRS information-sharing, and when it sees income with no California return behind it, it sends an FTB demand to file. Ignore that, and the FTB assesses tax for you — usually on the gross 1099 amount with none of your business expenses — then collects that inflated number as if it were gospel.

Other common triggers: a filed return with an unpaid balance, an audit adjustment that became final, or a defaulted FTB payment plan. Whatever the source, by the time an Order to Withhold hits your bank, the FTB considers the debt settled law — the fight now is about the money, not the merits, unless the assessment itself is wrong.

The notices that came before the levy

The FTB cannot legally levy your bank account without first mailing a final warning to your last known address. That warning is the Final Notice Before Levy — the state-side cousin of an FTB intent to levy notice — and once its window closes, the Order to Withhold can issue at any time with no further heads-up to you.

Here is the sequence most levies follow. If you moved and never updated your address with the FTB, these letters went somewhere — just not to you — and the levy is still legally valid.

| Stage | What it means | Your window |

|---|---|---|

| Demand for Tax Return | The FTB has income records (often IRS 1099 data) but no California return from you | Respond by the date printed on the notice |

| Notice of Proposed Assessment | The FTB estimates your tax — usually high — and proposes to make it final | Protest window printed on the notice, typically 60 days |

| Balance-due notices / Statement of Tax Due | The assessment is final and collectible; interest and fees are accruing | Pay or arrange terms before the final notice arrives |

| Final Notice Before Levy | The last letter before enforcement — the FTB's intent-to-levy warning | Typically 30 days from the notice date (check yours) |

| Order to Withhold served on your bank | The levy itself — funds freeze the day your bank processes it | Bank typically holds funds about 10 days before remitting |

Unlike the IRS, California gives you no Collection Due Process hearing right before a levy. There is no state equivalent of Form 12153, no automatic pre-levy appeal that freezes enforcement. Your formal chance to dispute the tax was back at the Notice of Proposed Assessment stage — which is why so many FTB levies feel like they came out of nowhere.

What happens if you do nothing after an FTB bank levy

One Order to Withhold is almost never the end — an unresolved FTB balance triggers an escalating chain of enforcement that runs for up to 20 years. Here is the sequence, in the order it typically unfolds:

- The hold expires and your money leaves. After the hold period — typically about 10 days — your bank remits the frozen funds to the FTB. Your bank may also charge you its own legal-processing fee on top.

- The FTB finds your other accounts. Under the Financial Institution Record Match (FIRM) program, banks doing business in California report accounts held by delinquent taxpayers to the state. A new Order to Withhold can follow to any account it finds — opening a new account rarely buys more than a short delay.

- Your income gets attached. If you're a W-2 employee, an Earnings Withholding Order for Taxes takes a slice of every paycheck — see our guide to FTB wage garnishment. If you're a 1099 contractor, the FTB can serve a Continuous Order to Withhold on your clients, intercepting generally 25% of each payment before it ever reaches you. (The parallel federal process is covered in our guide on how to stop IRS wage garnishment.)

- A lien goes public. A recorded Notice of State Tax Lien attaches to your property and shows up in title searches — an FTB tax lien complicates selling or refinancing anything you own.

- Fees stack on top. The FTB adds cost-recovery and lien fees to your balance as enforcement escalates; our breakdown of FTB collection fees shows what gets tacked on and when.

- The clock keeps running — for two decades. Under R&TC §19255, the FTB generally has 20 years to collect, twice the IRS's window. Waiting it out is not a strategy; California's 20-year collection statute explains why.

The through-line: every stage costs more than the one before it, and none of it requires a human at the FTB to look at your file. The system escalates on its own.

Is the hold still on your account?

If your bank hasn't remitted the funds yet, this is the window where releases actually happen. Send us your FTB notice and the levy details — an experienced tax professional will map your fastest release path free, before the money leaves.

How to stop an FTB bank levy: every release path

The FTB releases bank levies in specific, documented situations — not because you asked nicely, and not because a company "negotiated." Match your facts to the right path:

1. The levy took exempt money

Certain public benefits — Social Security, SSI, public assistance, and similar payments — are generally protected from levy even after they land in your bank account. The protection is not automatic, though: you must claim it and prove it, typically with bank statements tracing the deposits and an award letter showing the source. Call the FTB immediately, before the remit date, and ask exactly how to submit the proof.

2. The levy creates a financial hardship

If losing these funds means you can't cover rent, utilities, medicine, or the payroll that keeps your income flowing, the FTB can release some or all of the levy on hardship grounds. Expect to document it — usually with the FTB's financial statement, covered in our FTB Form 3561 walkthrough, plus bills and bank statements. Partial releases are common: the state keeps a portion and returns what you need to stay afloat.

3. The levy is simply wrong

If you already paid, if the debt belongs to someone with a similar name, or if the balance comes from a Demand for Tax Return assessment on income that a real return would show is far smaller — say so, with proof. Filing the actual return for an assessed year is often the single highest-value move a 1099 contractor can make, because it replaces a gross-income assessment with a net-income reality.

4. Get into an agreement so the next levy never issues

Paying in full stops everything, but few people staring at a levy can. The workhorse alternative is an installment agreement — the FTB's online application is generally available for individuals owing $25,000 or less who can pay within 60 months, and larger balances can still be negotiated with financial disclosure. Our FTB payment plan guide covers thresholds and setup. Be clear-eyed about one thing: entering a plan protects you going forward, but it doesn't automatically refund money the bank already remitted.

5. Longer-term paths: settlement, hardship status, bankruptcy

An FTB offer in compromise can settle the debt for less when your assets and income genuinely can't cover it — but California's program is strict, slow, and won't stop this week's levy. FTB hardship status can pause collection entirely while your finances recover, with periodic re-review. And filing bankruptcy triggers an automatic stay that halts levies while the case is open — whether the tax itself survives is a separate analysis, covered in does bankruptcy stop a levy. If phone lines fail and the hold clock is running out on a genuine hardship, the FTB's own Taxpayers' Rights Advocate office exists for exactly that kind of stuck case.

| Moment | Typical window | What you can still do — and what you lose |

|---|---|---|

| Final Notice Before Levy arrives | Date printed on the notice, typically 30 days | Set up a plan and no levy ever issues; let it pass and the FTB can serve your bank without further warning |

| Bank receives the Order to Withhold | Hold of about 10 days (varies by bank) | Request a release for exempt funds, hardship, or error while the money is still sitting at your bank |

| Bank remits to the FTB | After the hold expires | Money is applied to your balance; recovering it now means a formal claim and a long wait |

| Debt remains unresolved | Generally up to 20 years (R&TC §19255) | Repeat levies, withholding orders on wages or client payments, and lien filings all stay on the table |

What a $31,200 FTB levy looks like for a 1099 contractor

Say you're an independent contractor who never filed California returns for two busy years. The FTB saw your 1099s, sent a Demand for Tax Return you never received, and assessed $31,200 in tax, penalties, and interest — calculated on your gross receipts, with zero deduction for mileage, materials, or subs. This example is hypothetical, but the mechanics are exactly what happens:

- Levy day: your checking account holds $6,850 when the bank processes the Order to Withhold. All $6,850 freezes (your bank may add its own legal-processing fee). About 10 days later, it's remitted. Balance remaining: $31,200 − $6,850 = $24,350, still growing with interest.

- If you do nothing: the FTB serves a Continuous Order to Withhold on your biggest client, who pays you about $8,000 a month. At generally 25%, that's roughly $2,000 a month intercepted before it reaches you — on the state's terms, indefinitely, until the debt clears.

- If you act: a payment plan on $24,350 over 60 months runs roughly $406 a month before continuing interest — about a fifth of the client intercept, on a schedule you chose. And filing the actual returns for the assessed years, with real business expenses, could shrink the assessed tax itself before you ever agree to pay it.

That last point is the one most levied contractors miss: when the debt comes from a demand-to-file assessment, the cheapest dollar you'll ever save is the one that was never really owed.

How to respond to an FTB bank levy, step by step

- Call your bank first. Ask for the exact date it received the Order to Withhold, the amount frozen, and the date it will send the funds to the FTB. Write all three down — they define your deadline.

- Assemble the paper trail. Find the Final Notice Before Levy, your most recent FTB balance statement, and proof of any payments or filed returns for the years listed.

- Gather release evidence. Pull bank statements showing any exempt deposits, plus rent, utility, medical, and payroll obligations if you'll argue the levy creates a hardship.

- Call the FTB before the hold expires. Request a levy release or reduction based on exempt funds, hardship, or error — and ask the agent to note your account while your documents are in transit.

- Lock in a resolution. Set up a payment plan, hardship status, or offer so a second Order to Withhold never issues.

- File any missing returns. If the balance came from a Demand for Tax Return assessment, filing the actual return can shrink the debt the levy is chasing.

FTB bank levy vs. IRS bank levy: why the state version is harsher

An FTB bank levy gives you roughly half the time an IRS bank levy does, with none of the IRS's pre-levy hearing rights. If you owe both agencies — common for 1099 contractors, since the same unfiled 1040 usually means an unfiled 540 — the differences below decide which fire to fight first (our FTB vs IRS which first guide goes deeper):

| Feature | FTB bank levy | IRS bank levy |

|---|---|---|

| Levy instrument | Order to Withhold | Notice of Levy |

| Bank hold before funds leave | Typically about 10 days | 21 days |

| Final warning notice | Final Notice Before Levy | LT11 / Letter 1058 |

| Pre-levy hearing right | None — no Collection Due Process equivalent | CDP hearing via Form 12153 within 30 days |

| Collection clock | Generally 20 years (R&TC §19255) | 10 years from assessment (CSED) |

The federal side has its own mechanics and its own release paths — see IRS bank levy 21 days for how the longer federal hold works, and IRS.gov/payments for setting up the federal side once California is contained. The strategic rule of thumb: the agency with a live levy and the shorter clock gets your attention first — and today, that's the FTB.

When you can handle this yourself — and when help changes the outcome

You can likely handle an FTB bank levy on your own if the debt is accurate, it's under about $25,000, and you can qualify for the FTB's standard payment plan. In that case your path is short: call the bank, call the FTB, set up the agreement, and confirm in writing that no further levies will issue while you're current. The FTB's contact channels and payment tools are all at ftb.ca.gov, and you don't need to pay anyone to make those calls.

Experienced help tends to change the outcome in four situations: the hold clock is running and you need a hardship or exempt-funds release argued correctly the first time; the balance comes from demand-to-file assessments on unfiled years, where filing real returns can shrink the debt before you negotiate it; you're juggling FTB and IRS collection at once and the sequencing matters; or the levy hit a business account and your operating cash, payroll, or receivables are exposed — a scenario with its own dynamics, similar to an IRS levy business bank account situation but on California's faster timeline. In a 10-day window, a wrong first phone call is expensive.

Terms on your FTB levy paperwork, decoded

- Order to Withhold (OTW): the FTB's bank levy — a one-time order requiring your bank to freeze and remit the funds on hand, up to your balance.

- Continuous Order to Withhold (COTW): the FTB's tool for non-wage income — it intercepts a portion (generally 25%) of payments your clients or other payers owe you, and keeps working over time.

- Earnings Withholding Order for Taxes (EWOT): the FTB's wage garnishment, served on an employer to take a slice of each paycheck.

- Financial Institution Record Match (FIRM): the program requiring banks doing business in California to report accounts held by delinquent taxpayers — how the FTB finds your money.

- Notice of State Tax Lien: a public recorded claim against your property securing the FTB debt — different from a levy, which actually takes assets.

- R&TC §19255: the California statute giving the FTB generally 20 years to collect a final tax liability.

If the FTB has levied you once, a second Order to Withhold is usually a matter of when, not if — get a free FTB levy review before the next one issues, or call (888) 825-7779.

FTB bank levy questions, answered

Can the FTB levy my bank account without warning?

Not legally without any warning — the FTB must first mail a series of notices, ending with a Final Notice Before Levy, to your last known address. But the Order to Withhold itself arrives at your bank with no same-day heads-up to you, so if you moved or ignored the mail, the freeze feels like it came from nowhere. Update your address with the FTB immediately so you never miss the next deadline.

How long does the bank hold money after an FTB levy?

Your bank typically holds the levied funds for about 10 days after it receives the FTB's Order to Withhold, then sends them to the state. The exact remit date varies by bank, so call and ask for the date the order was received and the date the funds go out. Everything you do to fight the levy is easier before that transfer than after.

Can I get my money back after an FTB bank levy?

Yes, in three main situations: the funds came from an exempt source such as Social Security or public assistance, the levy creates a documented financial hardship, or the levy was issued in error — for example, you already paid or the assessment came from a return you never actually owed. Releases are far easier to win while the bank still holds the money; after it remits, you're filing a refund claim and waiting.

Does an FTB bank levy take deposits I make after the freeze?

No. An Order to Withhold is a one-time snapshot — it captures only the funds in the account at the moment your bank processes it, up to the balance you owe. Deposits that land afterward are yours. The catch: the FTB can issue a new Order to Withhold at any time until the debt is resolved, so an untouched account today is not a safe account tomorrow.

Can the FTB take Social Security or disability money from my account?

Certain public benefits — including Social Security, SSI, and public assistance — are generally exempt from levy, but the protection isn't automatic once the money sits in a bank account. You must claim the exemption and prove the deposits came from the exempt source, usually with bank statements and award letters. Contact the FTB immediately, before the bank remits, and send the proof in whatever format the agent requests.

Can the FTB levy a joint bank account?

Yes. If your name is on the account, the FTB can levy it — even if most of the money belongs to a spouse, parent, or business partner who owes nothing. The non-liable co-owner can contest the levy by proving the funds are theirs, typically with deposit records tracing the money to their income. That claim is time-sensitive, so start it while the bank still holds the funds.

How is an FTB bank levy different from an IRS bank levy?

Three big differences: the hold window (banks typically hold FTB-levied funds about 10 days versus 21 days for an IRS levy), the hearing rights (the IRS must offer a Collection Due Process hearing before most levies; California has no equivalent), and the clock (the FTB generally has 20 years to collect versus the IRS's 10). In short, the FTB moves faster and keeps collecting longer.

How many times can the FTB levy my bank account?

As many times as it takes. Each Order to Withhold is a one-time grab, but nothing stops the FTB from issuing another next month — and its Financial Institution Record Match program means California banks report your accounts to the state, so switching banks rarely hides money for long. The only reliable way to stop repeat levies is a resolution: full payment, a payment plan, hardship status, or an accepted offer.

Does bankruptcy stop an FTB bank levy?

Filing bankruptcy triggers an automatic stay that halts FTB collection, including bank levies, while the case is open. Whether the underlying tax debt is actually wiped out is a separate question that depends on the age of the debt, when returns were filed, and the chapter you file. Bankruptcy is a serious step with long-term costs — treat it as one option among several, not the default.

Your next 24 hours

- Call your bank and get three facts in writing: the date it received the Order to Withhold, the amount frozen, and the date it will remit the funds to the FTB.

- Gather your file: the Final Notice Before Levy (or whatever FTB mail you have), your last two years of returns — filed or not — and bank statements showing your deposits and essential bills.

- Get the levy reviewed before the hold expires: use the 2-minute form or call (888) 825-7779 — an experienced tax professional will tell you which release path fits your facts while the money is still at your bank.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.