California FTB

FTB Court-Ordered Debt Collections: Why California's Tax Agency Is Collecting Your Court Fines (2026)

The short answer: FTB court ordered debt collections is the California program that lets courts refer unpaid fines, fees, and victim restitution to the Franchise Tax Board for collection. The FTB can garnish wages, levy bank accounts, and intercept state refunds — but it cannot reduce the debt. Only the referring court can change what you owe.

The letterhead says Franchise Tax Board, but the balance isn't taxes — it's a court case, maybe one you'd half forgotten: an old traffic fine, a criminal fine, a restitution order. You run your own 1099 work, your taxes are filed, and now the state's tax collector is demanding money for something a courtroom decided. That's not a mistake. It's how California is designed to work — and it's manageable once you know which agency controls which lever.

Two details on that letter control everything: the referring court and the case number, both printed near the top of your notice. The visual guide below maps the key facts, deadlines, and options — keep reading and you'll see why every path forward starts there.

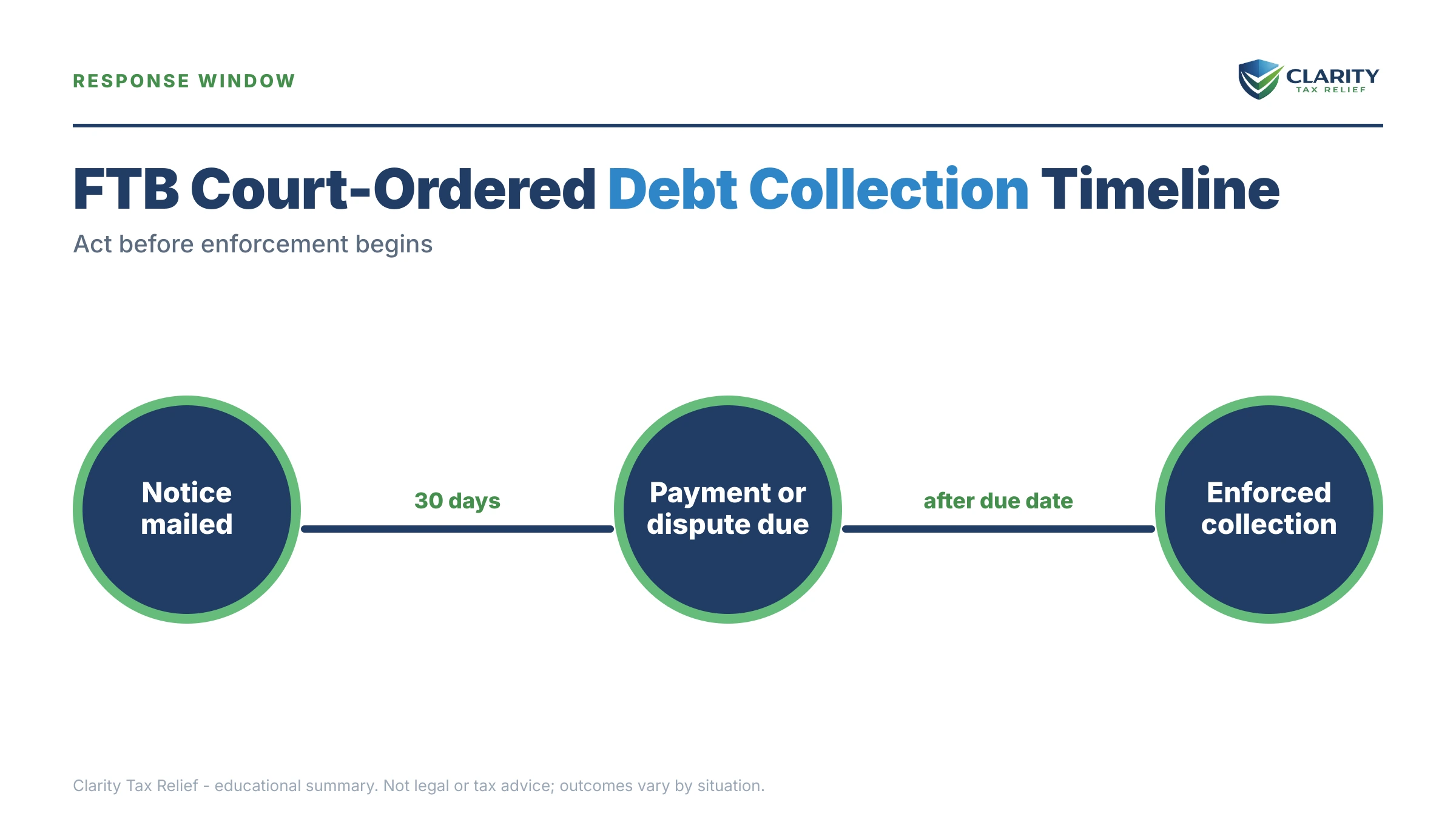

⏱ Your deadline: the response date printed on your FTB court-ordered debt notice controls. There is no fixed statutory window like an IRS notice — but once that date passes, the FTB can typically begin wage garnishment, bank levies, and refund intercepts without sending another warning, and restitution balances generally keep growing with interest.

Why you got a court-ordered debt notice from the FTB

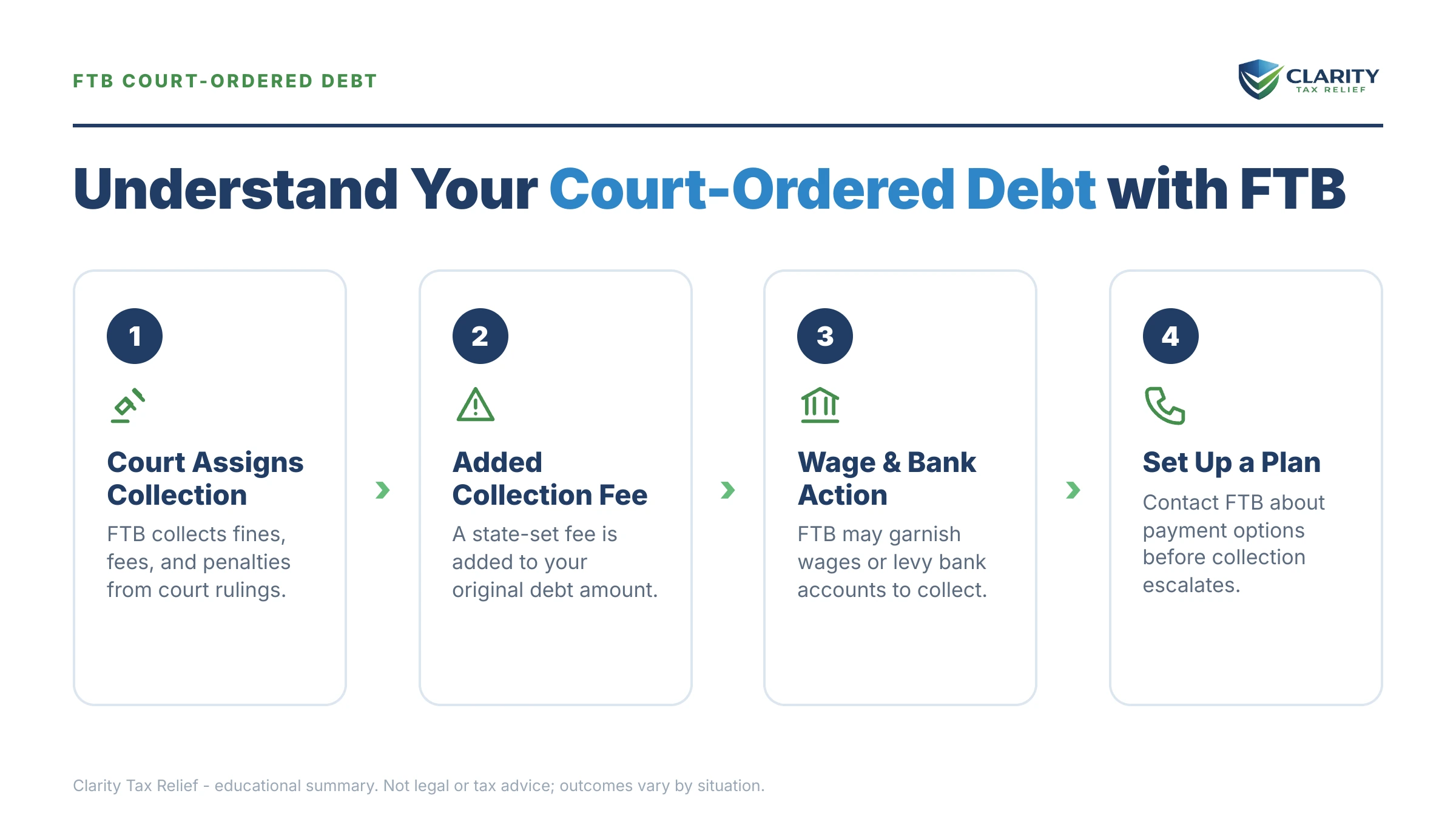

California Revenue and Taxation Code §19280 lets courts and certain state agencies refer delinquent court-ordered debt to the Franchise Tax Board for collection. Once you miss the court's payment deadline, the court doesn't chase you forever — it hands the account to the state's most efficient collector and moves on.

The debts that land in this program include criminal fines, traffic and vehicle-related fines, court fees, penalties, forfeitures, and victim restitution orders. The FTB collects them using the same machinery it uses for back taxes, which is why the letter looks and feels like a tax bill even though no tax is involved.

Here's the part most people miss: once the debt is referred, you pay the FTB — not the court clerk. But if you want to dispute the debt, reduce it, or prove you already paid it, you go back to the referring court, because the FTB has zero authority over the amount. Getting those two roles backwards is the single most common way people burn weeks they don't have.

One more distinction worth checking before you go further: the FTB runs three separate non-tax collection programs — court-ordered debt, vehicle registration collections, and the intercept program. If your notice references DMV registration rather than a court case, you're actually dealing with an FTB DMV hold, which follows different steps.

How FTB court-ordered debt is different from FTB tax debt

The FTB cannot reduce, dismiss, or change a court-ordered debt — only the referring court can. That single fact reroutes almost every strategy that works on tax debt. Penalty abatement, an FTB offer in compromise, amended returns — none of them touch a court judgment, because the FTB is collecting someone else's debt, not its own.

| Question | FTB tax debt | Court-ordered debt |

|---|---|---|

| Where the debt came from | Your return or an FTB assessment | A California court judgment or sentence |

| Who can reduce it | The FTB (abatement, offer in compromise) | Only the referring court |

| Payment plan | Standard FTB payment plan | Arrangement with the FTB's court-ordered debt unit |

| Settle for less than owed | Possible via FTB OIC if you qualify | Not through the FTB — court petition only |

| Collection time limit | Generally 20 years under R&TC §19255 | Follows the judgment's rules; restitution is generally collectible until paid |

| Survives bankruptcy? | Sometimes dischargeable | Criminal fines and restitution generally are not |

That collection-clock difference matters more than it looks. California's 20-year FTB collection statute applies to state tax debt. Victim restitution, by contrast, is generally enforceable until paid in full and typically accrues 10% annual interest under California law. Waiting out a restitution balance isn't a strategy — it's a compounding problem.

One piece of recent good news: a 2022 state law cut the civil assessment courts add for missed payments from up to $300 down to $100, and directed courts to discharge many older unpaid civil assessments. If your balance includes civil assessments from before mid-2022, ask the referring court whether they're still legally owed — some balances shrink just by asking.

What happens if you ignore the notice

Once the response date on an FTB court-ordered debt notice passes, the FTB can garnish up to 25% of your disposable wages and levy your bank account without further warning. There are no Collection Due Process rights on this track and, with FTB collections heavily automated, no human review before enforcement fires. The sequence runs like this:

- You miss the court's payment deadline. The court marks the case delinquent and may add a $100 civil assessment on top of the fine.

- The court refers the balance to the FTB under R&TC §19280. From this point, the FTB owns collection and the court owns the amount.

- The FTB sends its demand notice — the letter you're holding — naming the referring court, case number, balance, and a response date. You are here.

- Involuntary collection begins. An earnings withholding order to your employer, an order to withhold on your bank or your clients, and automatic intercepts of your state refund and lottery winnings.

- The debt persists and grows. Restitution accrues interest, garnishments run continuously until paid, and — unlike tax debt — there's no reliable expiration date to run out.

Each tool hits differently depending on how you're paid, which is where 1099 income changes the math entirely:

| Collection tool | How it hits | What to know |

|---|---|---|

| Earnings withholding order | Up to 25% of disposable wages, continuous | Runs until paid or replaced by an arrangement — see how much can FTB garnish |

| Order to withhold (bank) | One-time grab of funds in the account that day | Bank holds funds only briefly before remitting — details in our FTB bank levy guide |

| Order to withhold (payors) | Sent to businesses that owe you money | Can capture the full amount a client owes you that day — not limited to 25% |

| Interagency intercept | State tax refund and lottery winnings taken automatically | No separate warning per refund — see FTB refund intercept |

Read that third row again if you're self-employed. A W-2 worker loses a quarter of each paycheck; a contractor can lose an entire invoice the day a levied client pays it. That's why 1099 earners with referred court debt tend to feel nothing for months — then lose a whole month's revenue in one hit.

Holding an FTB court-ordered debt notice right now?

Once the response date on it passes, the FTB can garnish wages, levy your bank account, or intercept client payments without another letter. Send us a photo of your notice — an experienced tax professional will map exactly which levers the FTB can pull on you and which arrangement stops them. Free, confidential, no pressure.

Your options for resolving FTB court-ordered debt

Every resolution path runs through one of two doors: the FTB's court-ordered debt unit (payment) or the referring court (amount). The general playbook in our guide to how to settle tax debt yourself covers negotiating with tax agencies — but court-ordered debt plays by its own rules, so here's the version that actually applies:

| Option | Who handles it | Best when |

|---|---|---|

| Pay in full | FTB court-ordered debt unit | You can cover it — stops interest and enforcement immediately |

| Payment arrangement | FTB, via the number on your notice | Steady income but can't pay at once; set up before the response date |

| Financial hardship review | FTB court-ordered debt unit | Income can't cover basic living costs; may delay enforcement, debt remains |

| Ability-to-pay petition | Referring court | Fines are out of proportion to your income; many courts offer online tools for traffic infractions |

| Community service conversion | Referring court | The court allows it for your fine type; restitution usually can't be converted |

| Dispute / already paid | Referring court, with proof | Records show an error, identity mix-up, or a payment the referral missed |

| Bankruptcy | Bankruptcy court | Rarely helps — criminal fines and victim restitution generally survive it |

Notice what's not on the list: any FTB program that shrinks the number. If a company promises to "settle" your court-ordered debt with the Franchise Tax Board, they're describing a program that doesn't exist for this debt type.

A worked example: $19,700 in referred court debt on 1099 income

Say you're a self-employed contractor and a referred balance of $19,700 — an old criminal fine plus victim restitution that's been accruing 10% interest — lands with the FTB. This is hypothetical, but the arithmetic is real:

- If you do nothing: an order to withhold hits your biggest client the week they owe you $8,000, and the FTB captures the full $8,000 — not 25% of it. Your remaining balance drops to $11,700, but you just lost a month's operating cash with no say in the timing.

- If you set up an arrangement first: a 36-month arrangement on $19,700 works out to roughly $548/month ($19,700 ÷ 36). Predictable, and it keeps levies off your clients — which for a contractor also protects the relationships those invoices come from.

- If you work the court side too: suppose the itemized breakdown shows $700 of pre-2022 civil assessments the court agrees to discharge, and an ability-to-pay petition trims the fine portion by $3,300. The balance falls to $15,700 — about $436/month over the same 36 months, and roughly $4,000 that never leaves your pocket.

The sequence matters: verify and shrink the number at the court while an FTB arrangement holds enforcement off. Doing only one leaves money — or an invoice — on the table.

How to respond to FTB court-ordered debt collections, step by step

- Find the referring court and case number on your notice. They're printed near the top of the FTB letter, and every dispute, reduction request, or records search starts with them.

- Verify the balance with the referring court. Ask the clerk for an itemized breakdown showing the original fine, fees, civil assessments, restitution, and any interest — errors and already-paid amounts surface here.

- Contact the FTB at the number printed on your notice. Once a debt is referred, payments and payment arrangements go through the FTB's court-ordered debt unit, not the court clerk's window.

- Set up a payment arrangement or request a hardship review before the response date. An arrangement in place before that date is what prevents wage garnishments, bank levies, and client-payment intercepts.

- Petition the referring court if you dispute the debt or need it reduced. Only the court can lower a fine based on ability to pay, convert it to community service, or correct a case error — the FTB cannot.

When you can handle this yourself — and when help changes the outcome

If the balance is small, accurate, and you can pay it within a few months, you don't need anyone — call the number on your notice and set up the arrangement yourself. The court-ordered debt unit handles straightforward payment setups every day, and there's no fee-charging middleman worth paying for a $900 traffic fine you agree with.

Experienced help earns its cost in the messier situations: a garnishment or bank levy already in motion, an order to withhold threatening your client relationships, a hardship case that needs a properly documented financial statement, or — very common in California — court-ordered debt stacked on top of actual California FTB back taxes, where the resolution order across two debt types changes what you pay. An experienced tax professional can also tell you honestly when your real remedy is at the courthouse, not the FTB — and a court dispute itself is a legal matter where the court's self-help center or an attorney is the right resource, not a tax firm.

Terms on your notice, decoded

- Referring court: the courthouse that imposed your fine and sent it to the FTB — the only body with power over the amount.

- Civil assessment: a penalty (now capped at $100) a court adds when you miss a payment or appearance date.

- Victim restitution: money a criminal court ordered paid to a victim; generally accrues 10% interest and survives bankruptcy.

- Earnings withholding order: the FTB's wage garnishment — up to 25% of disposable earnings, continuous until resolved; see our FTB wage garnishment guide.

- Order to withhold: a one-time seizure order sent to your bank or to people who owe you money, including 1099 clients.

- Interagency Intercept Collection: the program that automatically applies your state tax refund and lottery winnings to referred debt.

For the court side — payment petitions, ability-to-pay tools, and case lookups — start with the California Courts self-help resources. For the collection side, the Franchise Tax Board website covers its court-ordered debt program and payment options.

FTB court-ordered debt questions, answered

Why is the Franchise Tax Board collecting my court fines?

California law (Revenue and Taxation Code §19280) lets courts and certain state agencies refer delinquent court-ordered debt — fines, fees, penalties, and victim restitution — to the FTB for collection. The FTB acts purely as the collector: it uses its tax-collection machinery (garnishments, levies, intercepts) but has no authority over whether the debt is correct. If you believe the underlying fine is wrong, that fight happens at the referring court, not with the FTB.

Can the FTB garnish wages for court-ordered debt?

Yes. The FTB can issue an earnings withholding order taking up to 25% of your disposable earnings, and it runs continuously until the debt is paid or an arrangement replaces it. If you're a 1099 contractor, there's no paycheck to garnish — instead the FTB can send an order to withhold to your clients or your bank, which can capture the full amount owed to you on that day rather than a 25% slice.

Can I settle FTB court-ordered debt for less than I owe?

Not through the FTB. The FTB's Offer in Compromise program applies only to tax liabilities — it has no legal authority to compromise a court's judgment. Any reduction must come from the referring court, which in some cases can lower fines based on ability to pay, convert them to community service, or correct errors. The FTB side is limited to payment arrangements and hardship-based delays in enforcement.

Does California court-ordered debt ever expire?

Don't count on it. The FTB's 20-year collection statute applies to state tax debt, not to court-ordered debt, which follows the rules of the underlying judgment. Victim restitution in particular is generally enforceable until paid in full and typically accrues 10% annual interest under California law. Criminal fines and restitution also generally survive bankruptcy, so waiting the debt out is usually not a real strategy.

Can the FTB take my state tax refund for court-ordered debt?

Yes. Through the Interagency Intercept Collection program, your California income tax refund — and even lottery winnings — can be intercepted and applied to referred court-ordered debt before you ever see the money. The intercept happens automatically once the debt is in the system, with no separate warning for each refund. If you're expecting a state refund while carrying referred court debt, assume it will be taken unless the debt is resolved first.

What if I already paid the court before the FTB got involved?

Get proof and work both ends. Pull your receipts or bank records, then contact the referring court clerk and ask them to update the case and notify the FTB that the referral should be recalled or adjusted. Also call the FTB at the number on your notice so a note goes on the collection file while the court corrects its records. Don't ignore the notice while you sort it out — enforcement systems don't pause on their own.

Can I set up a payment plan with the FTB for court-ordered debt?

Yes. Once a debt is referred, payment arrangements go through the FTB's court-ordered debt unit at the phone number printed on your notice — not through the court clerk and not through the FTB's regular tax payment plan system. An arrangement in place before the response date on your notice is what prevents garnishments and bank levies. If your income genuinely can't support payments, ask the unit about a financial hardship review instead.

Will unpaid court-ordered debt suspend my driver's license?

Not just for inability to pay — California ended license suspensions for failure to pay traffic fines in 2017. A failure-to-appear can still create a DMV hold in some cases, so check your case status with the referring court. Note that the FTB also runs a separate Vehicle Registration Collections program for unpaid DMV registration; if your notice mentions vehicle registration rather than a court case, you're dealing with that program instead.

Your next 24 hours

- Find three things on your notice: the referring court, the case number, and the response date. Write the date somewhere you'll see it — it's the line between voluntary and involuntary collection.

- Gather your paper: the notice itself, any court paperwork or payment receipts from the original case, and — since arrangements and hardship reviews turn on income — your last two or three months of pay stubs or contractor invoices.

- Get a free case review before the response date passes: call (888) 825-7779 or use the 2-minute form. An experienced tax professional will sort what belongs at the FTB from what belongs at the court, and map the arrangement that keeps garnishments and client levies off the table.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS and state programs depends on individual facts and circumstances; no outcome is guaranteed.