California Tax Debt

California FTB Back Taxes: How to Resolve What You Owe in 2026

The short answer: California FTB back taxes are unpaid state income taxes collected by California's Franchise Tax Board — an agency with 20 years to collect, twice the IRS's 10. You can resolve a balance through an FTB payment plan, hardship status, an Offer in Compromise, or penalty relief, but interest accrues until it's paid.

Maybe a gray envelope from Sacramento showed up this week — or maybe you're pulling documents together for a refinance and just discovered the Franchise Tax Board says you owe for a year you thought was closed. That knot in your stomach is normal. But an FTB balance is one of the most fixable tax problems there is, provided you move before the automated machinery does — and this page maps every path.

If your search started with a notice, the visual guide below maps the key facts, deadlines, and options so you can quickly see where your account stands and what controls your window to act.

⏱ Your real clock: there's no single federal-style deadline on California FTB back taxes — the governing clock is Revenue & Taxation Code §19255, which gives the FTB 20 years to collect, while interest, penalties, and collection fees accrue every month until you resolve the balance. If your notice prints a "pay by" date, that date controls your next step.

Why you owe the FTB: the five common triggers

The Franchise Tax Board collects California personal income tax and corporate franchise tax, and a back-tax balance almost always traces to one of five triggers. Which one applies to you changes both the size of the debt and the fastest way to shrink it.

- You filed but didn't pay in full. The FTB assesses the balance from your own return, then adds a late-payment penalty and interest. This is the simplest version to fix.

- You never filed, so the FTB filed for you. After a FTB demand to file goes unanswered, the FTB issues a Notice of Proposed Assessment built from W-2s, 1099s, mortgage-interest records, and even professional-license data. A Notice of Proposed Assessment allows no deductions, no credits, and the least favorable filing status — which is why these balances run high and why filing the real return usually cuts them.

- An IRS change flowed downhill. If the IRS audits you or adjusts a return (a CP2000, for example), California law requires you to report the federal change to the FTB. If you don't, the FTB eventually assesses the state-side tax itself — with penalties stacked on top.

- A residency dispute. If you left the state but the FTB believes you were still a California resident for the years in question, it can assess tax on income you earned elsewhere. That's a california residency audit issue, and the rules around moving out of california taxes are more demanding than most people expect.

- Self-employment underwithholding. 1099 earners who missed California estimated payments get hit with the underpayment penalty on top of the tax itself, and the shortfall compounds year over year until quarterlies get fixed.

One scope note: the FTB only handles income and franchise tax. Sales tax debt belongs to the CDTFA — see california back sales tax — and payroll tax debt belongs to the EDD, covered in california edd payroll tax. Owing one California agency doesn't resolve — or worsen — your account with another; each collects on its own track.

The 20-year collection clock (and why "waiting it out" fails)

Under California Revenue & Taxation Code §19255, the FTB has 20 years to collect back taxes — double the IRS's 10-year collection statute. A federal debt from 2016 may be nearing expiration; the same year's California debt can legally be collected until the mid-2030s.

Two decades changes the strategy math completely. Hardship status that quietly outlasts an IRS debt rarely outlasts an FTB one. Limited situations can extend the 20 years further, and the FTB's systems automatically re-check your income and assets over time. The full mechanics — when the clock starts, what pauses it — are in California's 20-year collection statute.

The practical takeaway: with the FTB, resolution beats endurance. Almost everyone comes out ahead choosing a program rather than hoping the clock wins.

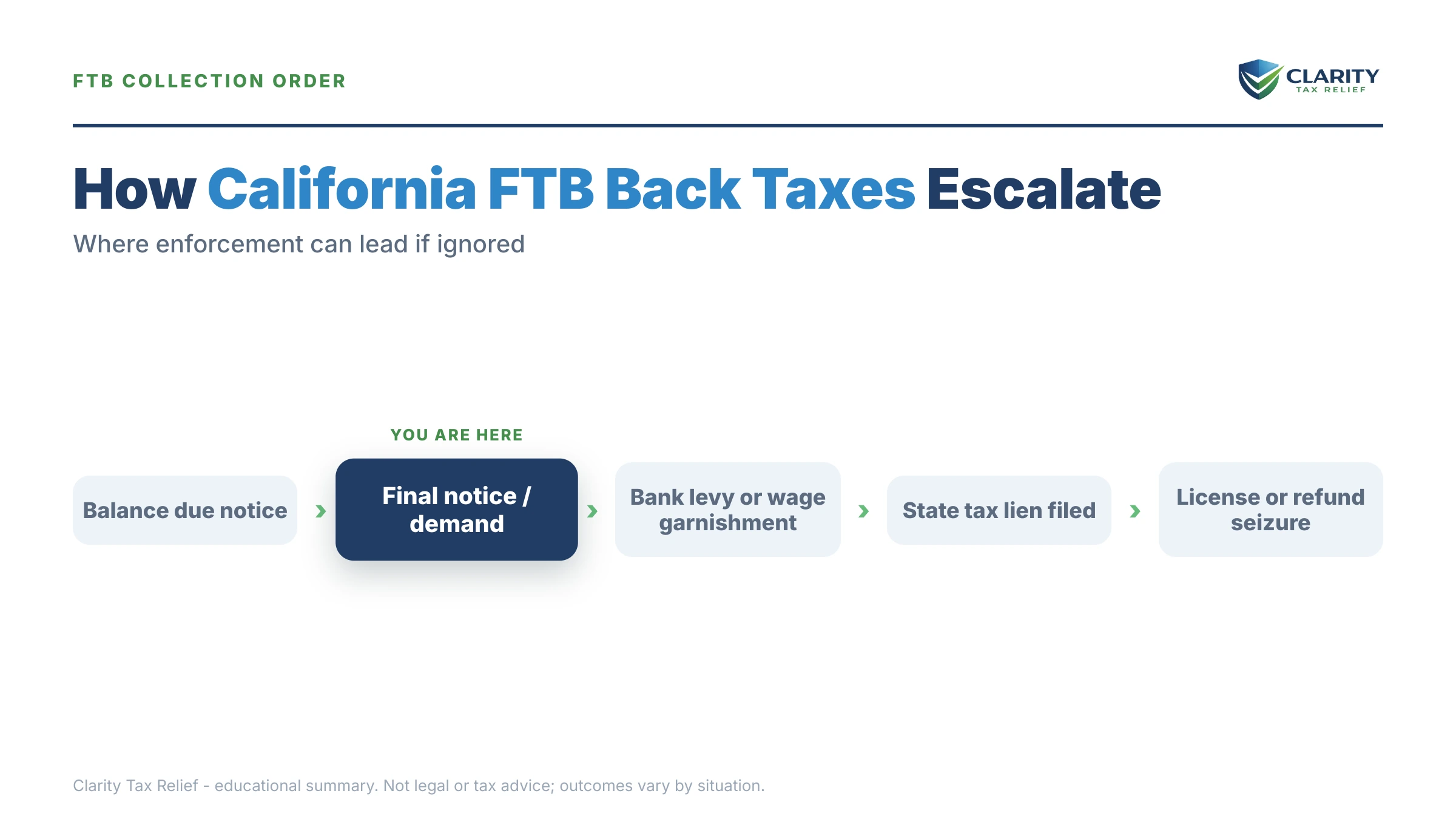

What happens if you ignore FTB back taxes

Ignoring FTB back taxes triggers an automated sequence that ends in a recorded lien, a bank levy, and a continuous wage garnishment. The FTB sends fewer warning notices than the IRS before it levies, and it offers no equivalent of the IRS's Collection Due Process hearing — so the runway is shorter than federal experience suggests.

- Balance assessed, first bill mailed. The cheapest moment in the entire sequence: tax, initial penalty, and interest only. Every option on this page is still open.

- Demand for payment. A follow-up notice arrives, and the FTB typically adds a collection cost recovery fee to the balance. Your account moves toward involuntary collection.

- Final notice before levy. The last warning, with its own printed deadline. After it passes, the FTB doesn't need your permission or a hearing to act.

- Involuntary collection. In whatever order its system chooses: your state refund is intercepted, an FTB tax lien is recorded against everything you own — including your home — an Order to Withhold hits your bank (see FTB bank levy), and an Earnings Withholding Order starts an FTB wage garnishment that typically takes up to 25% of disposable pay until the debt is gone.

- Escalated enforcement for large balances. Debts generally above $100,000 can land on the FTB's public Top 500 delinquent taxpayer list, which can trigger suspension of professional and driver's licenses and state contract ineligibility.

Every stage in that list appears somewhere on the notices themselves — and the visual guide above maps the full escalation sequence, so you can tell exactly which stage your account has reached.

| Stage | What the FTB does | What it means for you |

|---|---|---|

| First balance-due notice | Bills the tax plus initial penalty and interest | Cheapest moment to resolve; every option still available |

| Demand for payment | Follow-up notice; collection cost recovery fee typically added | The balance grows and the account moves toward enforcement |

| Final notice before levy | Last warning, with its own printed deadline | Your last window to set up a resolution voluntarily |

| Involuntary collection | Refund intercept, recorded state tax lien, bank Order to Withhold, wage garnishment | Paycheck and bank at risk; the lien is public and blocks refinancing |

| Escalated enforcement (generally $100,000+) | Top 500 delinquent list; professional and driver's license suspension possible | Public listing plus direct threats to your livelihood |

Facing FTB back taxes right now?

Interest, penalties, and collection fees are compounding on your FTB balance today — and the FTB's automated system escalates on schedule whether or not a human ever reviews your file. Get your notice and balance reviewed free by an experienced tax professional before the next stage fires.

Your options for resolving California FTB back taxes

The FTB offers four main resolution paths for back taxes: a payment plan, hardship status, an Offer in Compromise, and penalty relief. Every one of them requires the same first move — all of your required California returns must be filed before the FTB will approve anything.

| Option | Generally fits when | What to know |

|---|---|---|

| Pay in full | You can cover the balance without hardship | Stops all accrual and enforcement immediately; pay online through ftb.ca.gov |

| Payment plan (installment agreement) | Individuals owing $25,000 or less, payable within 60 months, all returns filed | Interest keeps accruing; a missed payment or unfiled future return can default the plan; larger balances need financial disclosure |

| Hardship delay (Form FTB 3561) | Paying anything would leave you unable to cover basic living expenses | Collection pauses, the debt remains, and the 20-year statute means the FTB re-reviews your finances over time |

| FTB Offer in Compromise | No reasonable ability to pay the full balance now or in the foreseeable future | Separate program from the IRS's OIC; strict means testing; an accepted IRS offer does not settle FTB debt |

| Penalty abatement | Reasonable cause, or eligibility for California's one-time timeliness abatement | Removes qualifying penalties, not the underlying tax; interest is rarely waived |

Payment plan. This is the workhorse for most balances. Individuals who owe $25,000 or less and can pay within 60 months can generally apply online; confirm the current criteria on the FTB's site, since they can change. The full application walkthrough is in our FTB payment plan guide. Expect the FTB to require future returns filed and paid on time — a new balance can default the whole agreement.

Hardship status. If your budget genuinely can't produce a payment, the FTB can mark the account uncollectible for a period based on Form FTB 3561, its financial statement. It pauses garnishments and levies but doesn't erase anything, and unlike the IRS version, the 20-year clock means the FTB has plenty of time to revisit. Details in FTB currently not collectible.

FTB Offer in Compromise. Real, but narrow. The FTB settles for less than the full balance only when it concludes you have no reasonable ability to pay in full now or in the foreseeable future — typically fixed or limited income with little equity. It is a completely separate application from the federal program, so settling with the IRS leaves your California debt untouched. See FTB offer in compromise for the criteria and process.

Penalty relief. The FTB abates penalties for reasonable cause — serious illness, disaster, reliance on wrong written advice — and California has added a one-time abatement option for timeliness penalties in recent years. Interest generally survives abatement. How to request each type is covered in FTB penalty abatement.

Two situations that change the menu. If the debt comes from a joint return and your spouse caused it, the FTB runs its own innocent-spouse program separate from the IRS's — worth raising before you agree to pay. And if you dispute the amount itself (an inflated Notice of Proposed Assessment, a residency assessment you disagree with), protest and appeal rights exist, but they run on the deadlines printed on the assessment notice — dispute first, then arrange payment on whatever survives.

If none of these payments fit your budget at all, start with owe california state taxes cant pay — it walks the hardship-first sequence in detail.

FTB back taxes and your refinance: a worked example

A recorded FTB tax lien attaches to your home and appears in the title search on every refinance or sale. Before a lien exists, your balance is a private debt between you and Sacramento. After it's recorded at the county, it's a public encumbrance that most lenders require paid or released before closing — and payoff-and-release processing can add weeks to escrow.

Say you owe the FTB $4,800 from your 2023 return, and you're planning to refinance in about six months. Here's the arithmetic on your three paths:

- Pay in full now: $4,800, done. No lien, nothing in the title search, clean file for the underwriter.

- Payment plan: $4,800 ÷ 24 months = $200/month before interest, or $400/month on a 12-month plan. Interest continues to accrue at the FTB's adjustable rate, so total cost runs modestly above $4,800. An active plan generally keeps enforcement paused, but ask directly whether a lien will still be recorded — the FTB retains that right in some cases, and for a refinance the lien is the whole ballgame.

- Ignore it: a collection cost recovery fee gets added, interest compounds, and a lien is eventually recorded. Now your $4,800 problem includes lien fees, a payoff demand during escrow, and a release that has to be processed and recorded before the lender funds. If your refinance would save $250 a month, every month the lien delays closing costs more than the original monthly plan payment would have.

This is a hypothetical, but the ranking is nearly universal: resolving before the lien is recorded is always the cheap version. If a lien already exists, a payoff through escrow or — in limited cases — a subordination request can still get you closed; that's a situation where experienced help meaningfully speeds things up.

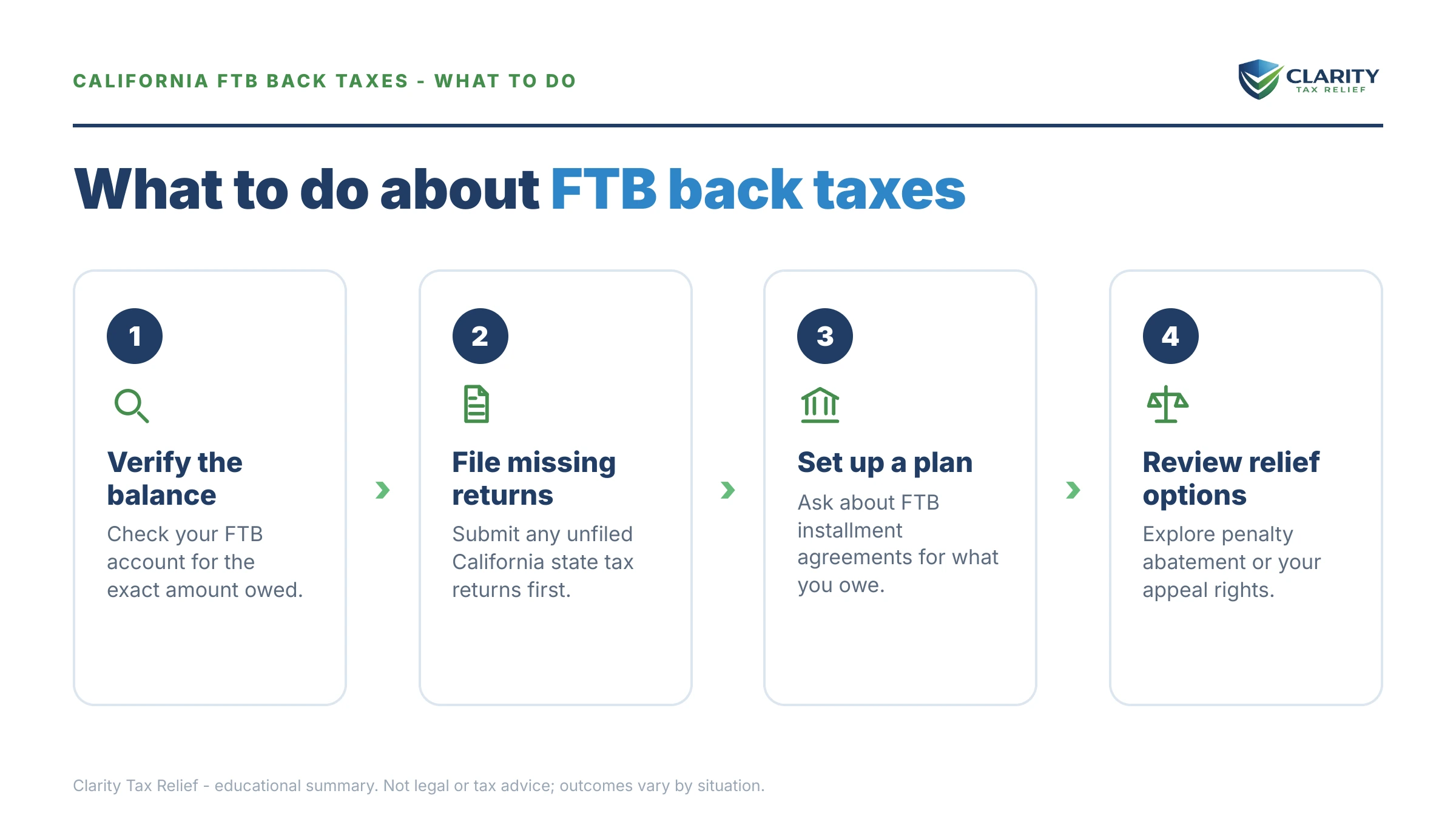

How to respond to California FTB back taxes, step by step

Responding to FTB back taxes takes five steps, and the order matters — resolution options open only after your filings are current.

- Confirm the real balance. Register for a MyFTB account or call the number on your notice and get a year-by-year breakdown of tax, penalties, interest, and fees.

- Check how the balance was assessed. If it came from a Notice of Proposed Assessment on an unfiled year, filing the actual return usually lowers it.

- File every missing California return. The FTB will not approve a payment plan, hardship status, or an offer while required returns are outstanding.

- Choose and set up your resolution. Pay in full, apply for a payment plan, submit Form FTB 3561 for hardship, or apply for the FTB's Offer in Compromise.

- Request penalty relief. Ask about California's one-time penalty abatement or reasonable-cause relief once your payment path is in place.

Owe the FTB and the IRS both? Sequence it deliberately

The IRS and the FTB collect independently — resolving one does nothing to the other, and each can intercept refunds and levy on its own schedule. The sequencing logic (which agency's payment plan to set first, how each agency's budget rules treat the other's payment) is a topic of its own; the full framework lives in our state tax debt vs irs guide. The one FTB-specific point worth knowing here: because the FTB's clock runs 20 years to the IRS's 10 and its enforcement is faster to fire, ignoring the state side while you negotiate with the IRS is usually the wrong order.

When you can handle this yourself — and when help changes the outcome

You can usually resolve FTB back taxes yourself when you agree with the balance, owe $25,000 or less, and every California return is filed. In that case, the online payment plan application takes minutes and doesn't require professional help — set it up, keep future filings clean, and you're done. The same is true for a small balance you can simply pay in full before the next notice.

Experienced tax professionals change outcomes in the harder versions of this problem:

- A garnishment or bank levy already in motion — negotiating a release while keeping the underlying resolution intact is time-sensitive and technical.

- Balances built from unfiled years — reconstructing and filing real returns against a Notice of Proposed Assessment often shrinks the debt more than any payment program could.

- Residency and part-year disputes — the difference between resident and nonresident treatment can be the entire liability.

- A lien threatening a refinance or sale — payoff demands, release timing, and subordination requests have to be choreographed with escrow.

- Multi-agency debt — when the FTB, EDD, and CDTFA (or the IRS) are all collecting, the order you resolve them in changes what you pay.

- FTB Offer in Compromise math — the means testing is strict, and a poorly built application wastes months.

If your situation is in that second list — a garnishment running, an inflated assessment, or a lien standing between you and a closing — get a free FTB case review or call (888) 825-7779 before the next automated step fires.

Terms on your FTB notice, decoded

- Notice of Proposed Assessment (NPA): the FTB's proposed tax bill — often an estimate for an unfiled year — which becomes final and collectible if you don't protest by its printed deadline.

- Demand for Tax Return: the FTB's formal request that you file a missing return; ignoring it leads to an estimated assessment plus a demand penalty.

- Earnings Withholding Order for Taxes (EWOT): the FTB's wage garnishment order to your employer, typically taking up to 25% of disposable pay continuously until released.

- Order to Withhold (OTW): the FTB's bank levy — a one-time order that freezes and remits funds from your account, repeatable as new deposits land.

- State tax lien: a public claim recorded against all your property, including your home; it survives until paid or released and surfaces in every title search.

- R&TC §19255: the California statute giving the FTB 20 years from the date a liability becomes due and payable to collect it.

Official program details, payment portals, and current eligibility criteria live at the California Franchise Tax Board. If your California debt is actually sales tax or payroll tax, the right agencies are the CDTFA and the EDD, respectively — each with its own programs and deadlines.

California FTB back taxes: your questions, answered

How long can the California FTB collect back taxes?

The FTB has 20 years from the date your liability became due and payable to collect, under California Revenue and Taxation Code §19255 — twice the IRS's 10-year window. Limited situations can extend that period, so waiting out an FTB balance is rarely a realistic plan. Interest and collection fees keep accruing the entire time, which means a small balance can grow substantially over two decades.

Can the FTB garnish my wages for back taxes?

Yes. The FTB issues an Earnings Withholding Order for Taxes to your employer, which typically takes up to 25% of your disposable pay each check and continues until the debt is paid or released. Unlike the IRS, the FTB does not offer a Collection Due Process hearing before it garnishes, so the practical window to act is before the final notice deadline passes.

Does the FTB offer payment plans for back taxes?

Yes. Individuals can generally apply online if they owe $25,000 or less, can pay the balance within 60 months, and have all required returns filed. Interest continues to accrue during the plan, and missing a payment or a future filing can default the agreement. Larger balances usually require submitting financial information before the FTB approves terms.

Can I settle California FTB back taxes for less than I owe?

Sometimes — the FTB runs its own Offer in Compromise program, separate from the IRS's. It is designed for people who have no reasonable ability to pay the full balance now or in the foreseeable future, often those on fixed or limited incomes. An accepted IRS offer does not settle your FTB debt; you must apply to each agency separately.

Will FTB back taxes stop me from refinancing my house?

An unrecorded balance usually won't, but a recorded FTB state tax lien will surface in your title search and most lenders won't close until it's paid or released. If you're planning a refinance, resolving the balance before the FTB records a lien is dramatically cheaper and faster than clearing a lien during escrow. Payoff and release processing can add weeks to a closing timeline.

Is the California FTB worse than the IRS?

In several ways, yes. The FTB has 20 years to collect versus the IRS's 10, sends fewer warning notices before levying, and offers no equivalent of the IRS's Collection Due Process hearing. Its systems are heavily automated, so garnishments and bank levies fire on schedule. That's why many experienced tax professionals resolve an FTB balance before, or alongside, an IRS one.

What happens if I never filed a California return?

The FTB will usually send a Demand for Tax Return, and if you don't respond, it files an assessment for you using W-2s, 1099s, and even professional-license data — with no deductions, credits, or accurate filing status. That estimated bill is almost always higher than what a real return would show. Filing the actual return, even years late, is often the single biggest way to shrink the balance.

Do I still owe the FTB if I moved out of California?

Yes. Moving out of state does not erase an FTB liability, and the FTB routinely collects across state lines through liens, out-of-state bank levies, and third-party collectors. If your dispute is about whether you were a California resident during the years at issue, that's a residency question worth fighting — but an assessed balance follows you wherever you live.

Can the FTB take money directly from my bank account?

Yes. The FTB issues an Order to Withhold to your bank, which freezes and remits funds up to the amount you owe. It can reach accounts at banks with a California presence even if you've moved away, and it can repeat the order as new deposits arrive. A hardship claim or a resolution agreement is the usual way to stop repeat levies.

Your next 24 hours

- Find your account number and total balance on your most recent FTB notice — or register at MyFTB and pull the year-by-year breakdown so you know exactly which stage of the sequence you're in.

- Gather three things: the notice itself, your last filed California return, and a rough picture of your monthly income and expenses. That's everything needed to match you to the right program.

- Get a free case review. Interest and collection fees are accruing on your FTB balance every month, and a recorded lien can stall a refinance for weeks — call (888) 825-7779 or use the 2-minute form and an experienced tax professional will map your fastest path to resolved.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. The same is true of California FTB programs, which apply their own state-specific criteria.