State Back Taxes

Connecticut Back Taxes in 2026: How DRS Collections Work and Every Way to Resolve What You Owe

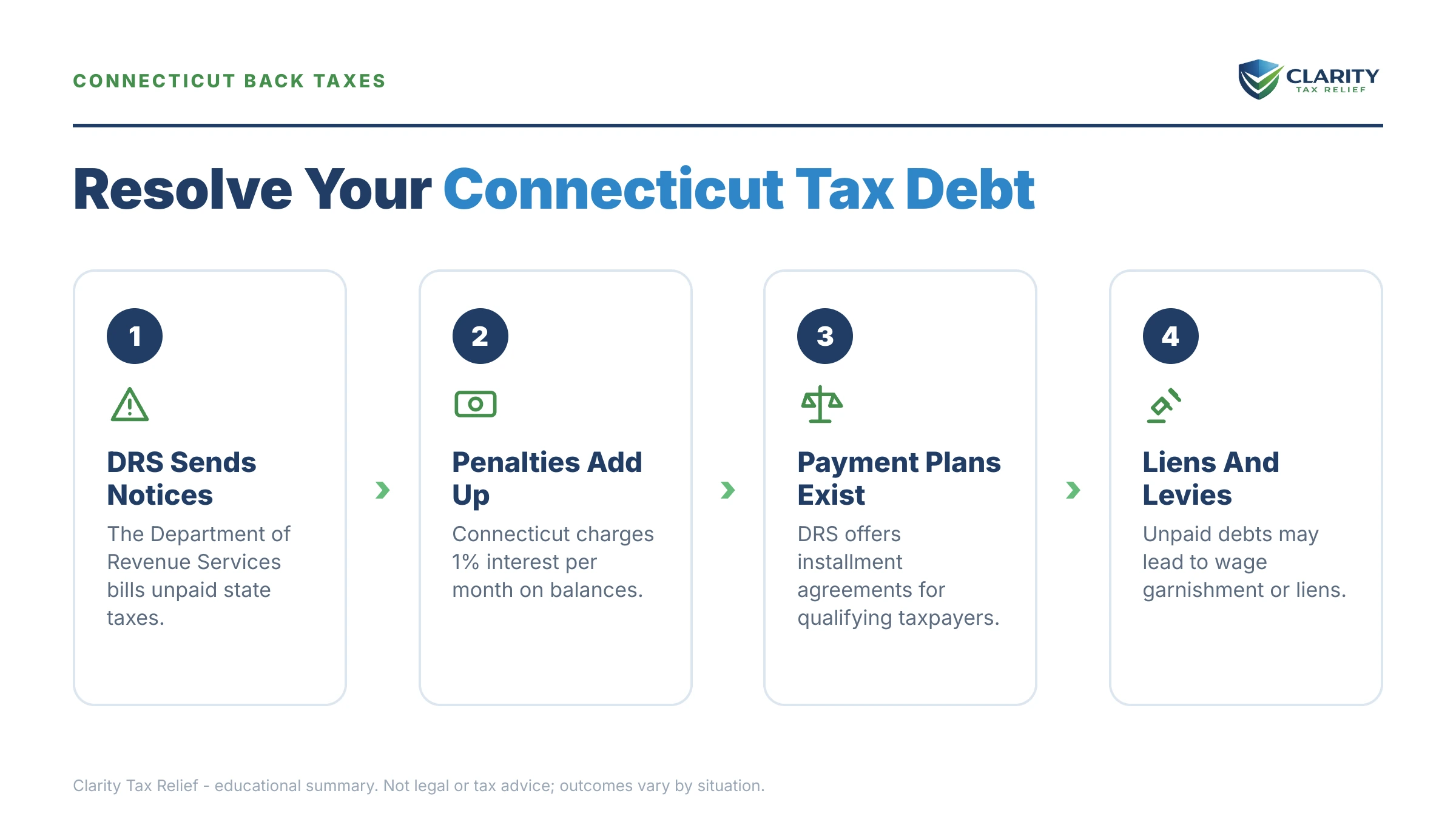

The short answer: Connecticut back taxes are collected by the Department of Revenue Services (DRS), not the IRS. Interest accrues at 1% per month, and DRS can file liens, garnish wages, and seize bank funds with fewer warnings than the IRS gives. Your paths out: pay in full, a myconneCT payment plan, a penalty waiver, or — in limited cases — an Offer of Compromise.

You filed your Connecticut return, the money wasn't there in April, and now a bill from the Department of Revenue Services is sitting on the counter — quietly growing by 1% every month. That feels heavier than a federal bill because you've probably never dealt with DRS before. The fix is real, though: DRS has defined resolution paths, and a W-2 taxpayer can usually start one this week.

Two things make Connecticut back taxes different from an IRS debt: the state's interest rate is a flat 1% per month — 12% a year — and DRS moves from polite billing to liens and warrants through fewer warning stages than the IRS's long notice ladder. If you're not even sure the letter is legitimate, the image below shows exactly what a DRS balance-due notice looks like and where to find the three numbers that matter: the tax year, the total due, and your response date.

⏱ Your deadline: the due date printed on your DRS notice. There is no quiet grace period after it — interest keeps accruing at 1% per month on the unpaid tax, and unresolved accounts move to DRS's Collections & Enforcement unit, where liens, bank warrants, and wage garnishment begin.

Why you owe Connecticut back taxes — and how DRS found you

A Connecticut back-tax balance almost always comes from one of six sources, and which one you have changes your best move.

You filed but couldn't pay. The most common case. Your CT-1040 was on time, the balance wasn't. DRS bills the tax plus a late-payment penalty and monthly interest. This is the easiest version to fix, because your filing record is clean.

Your withholding came up short. Two jobs, a bonus taxed at a flat supplemental rate, a spouse who returned to work — Connecticut's withholding tables miss these the same way federal tables do, and the shortfall lands on your April return.

DRS adjusted your return. A math correction, a disallowed credit, or a change flowing from a federal adjustment. Connecticut requires you to report IRS changes to your federal return — and if you don't, DRS often finds out anyway, because the two agencies share data.

You never filed. DRS can assess tax against non-filers using IRS income data — without your deductions, exemptions, or credits. If you've gone quiet for a while, our guide to what happens when you haven't filed taxes in 3 years covers the federal side; the Connecticut fix is the same first move: file real returns to replace the inflated estimate.

You're self-employed and missed estimates. Connecticut expects quarterly estimated payments just like the IRS does. Skip them and you owe the year's tax in one lump, plus an underpayment charge.

You moved — but Connecticut still claims the income. Part-year residents owe CT tax on income earned while resident; nonresidents owe it on Connecticut-source wages. Leaving the state does not erase the balance, and DRS collects across state lines.

What happens if you ignore Connecticut tax debt

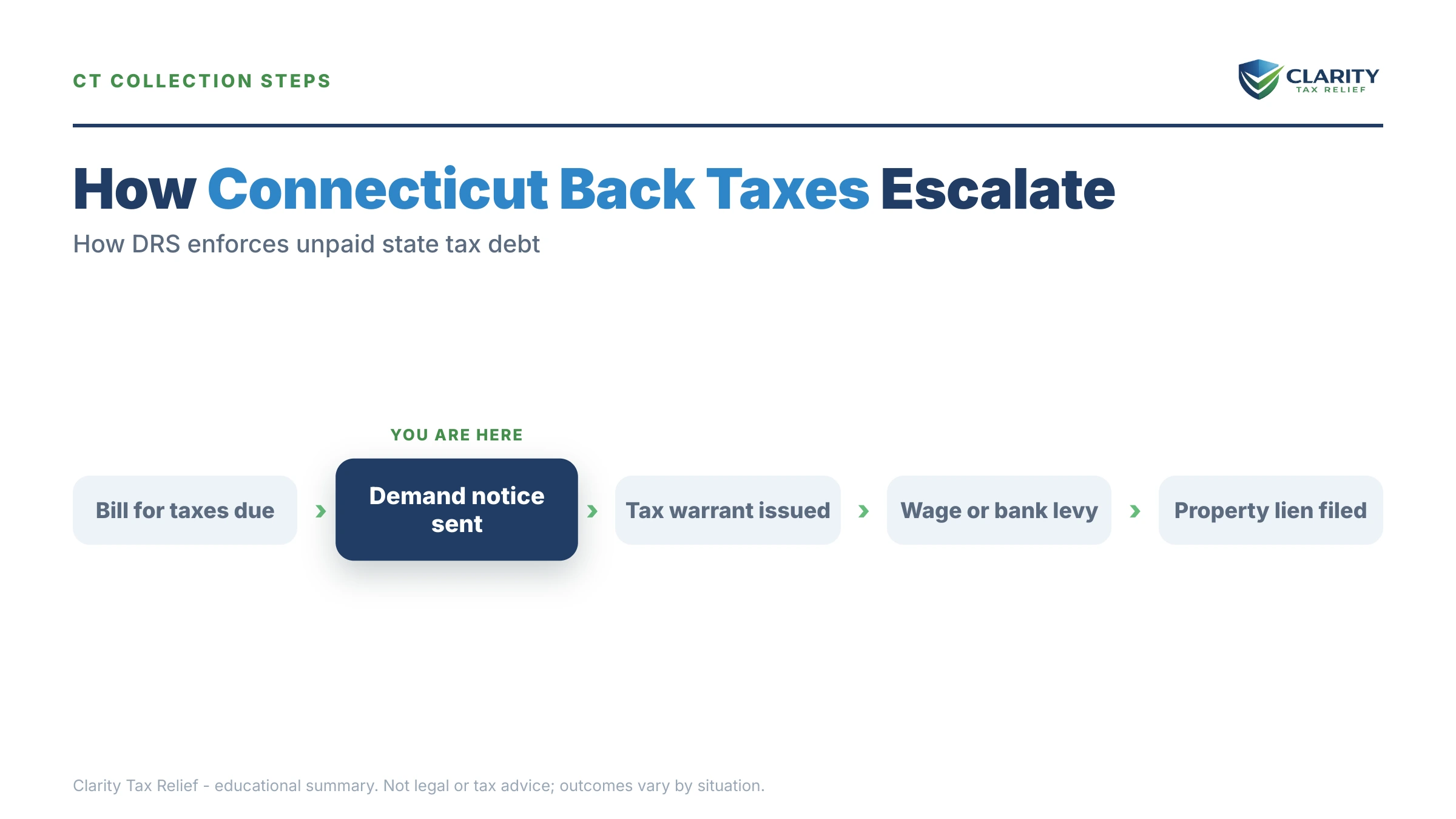

DRS collection is a sequence, and it runs whether or not a human ever reviews your file. Here is the order of escalation — the exact timing between stages varies by account, so treat the due date on your current notice as the only clock you can rely on:

- Balance-due notice. The first bill, showing the tax year, the tax, the penalty, and interest to date. It also appears in your myconneCT account. No enforcement yet — this is the cheapest moment you will ever have.

- Demand for payment. The tone changes: pay or make arrangements, or the account moves to enforcement. This is typically the last routine ask.

- Collections & Enforcement — lien filing. DRS can record a tax lien against your real property with the town clerk. It's a public record that attaches to your home and complicates any sale or refinance until the debt is resolved.

- Warrants against your bank and paycheck. DRS can serve warrants that seize funds from your bank account and take a slice of every paycheck — Connecticut's counterpart to the IRS levy and wage garnishment. Critically, there is no state equivalent of the IRS's 30-day Collection Due Process letter standing between you and enforcement.

- Everything else, indefinitely. Your Connecticut refund is intercepted every year. Unpaid state income tax can be submitted for federal refund offset. DRS may refer accounts to outside collection agencies, publish its largest delinquencies on a public list, and block license or permit renewals for business taxpayers.

One more difference that surprises people: the IRS's 10-year collection statute — the CSED — is a federal rule. It does not apply to Connecticut, and a recorded state lien can keep a debt enforceable against your property for many years. Waiting out a DRS balance is not a strategy.

Owe Connecticut back taxes and not sure how close DRS is to a lien or warrant?

Send us your DRS notice. An experienced tax professional will pinpoint where your account sits in the sequence and which resolution actually fits your numbers — free and confidential. Every month you wait adds another 1% in interest.

Your options for resolving Connecticut back taxes with DRS

DRS offers fewer programs than the IRS, and its terms are tighter — shorter plans, stricter settlement math, and interest that never turns off. The general playbook for choosing between agencies lives in our guide to state tax debt vs. IRS — which to resolve first; here is the Connecticut-specific menu.

| Option | Who it fits | What to know |

|---|---|---|

| Pay in full | Anyone who can raise the money | Stops the 1%-per-month interest immediately. Because DRS interest runs 12% a year, financing at a lower rate can genuinely save money. |

| DRS payment plan | Filers who can retire the balance quickly | Requested through myconneCT. Terms are typically far shorter than the IRS's 72 months — often around a year — so monthly payments run high. Interest continues while you pay. |

| Penalty waiver | Filers with documented reasonable cause | Can remove the 10% late-payment penalty for illness, disaster, or events beyond your control. Interest generally cannot be waived. |

| Offer of Compromise | Filers who genuinely cannot ever pay in full | DRS's settlement program. Granted sparingly, on doubt as to liability or collectibility, with full financial disclosure. Not a discount for asking. |

| Hardship handling | Filers in true financial crisis | DRS has no advertised equivalent of IRS Currently Not Collectible status; hardship is handled case by case. Expect to document everything. |

| Amnesty / voluntary disclosure | Depends on timing and filing history | Connecticut has run amnesty windows periodically. None is announced for 2026 — do not wait on one while interest accrues. |

The payment plan is the workhorse. For most W-2 taxpayers, a myconneCT installment plan is the realistic path: it stops the march toward liens and warrants while you pay. The trade-off is the short term — Connecticut expects the balance retired quickly, so the same debt costs far more per month here than it would on a federal plan. If the payment DRS wants doesn't fit your budget, that's the moment to involve a professional, because negotiating terms or documenting hardship is where experience matters.

The penalty waiver is the cheapest win available. Connecticut's late-payment penalty is a one-time 10% of the tax due. Unlike the IRS — which has first-time penalty abatement and, starting summer 2026, an automatic exemption — DRS relief runs on reasonable cause, meaning a documented event beyond your control. A hospitalization, a death in the family, a disaster: build the paper trail before you ask.

The Offer of Compromise is real but narrow. DRS can accept less than the full balance when there's genuine doubt you owe it or genuine doubt it could ever be collected. A single W-2 employee with steady income and equity in a home will almost always be steered to a plan instead. Where offers succeed is closed businesses, insolvency, and disputed assessments — situations where the state's own math says full collection is impossible.

How much do you owe? Realistic paths by balance

The right move shifts with the size of the debt, because DRS's short plan terms make monthly affordability the binding constraint.

| Balance owed to DRS | Realistic path | What changes at this level |

|---|---|---|

| Under $1,000 | Pay in full through myconneCT | A plan isn't worth the friction; the 1% monthly interest costs more than the convenience is worth. |

| $1,000 – $10,000 | Short payment plan + penalty waiver request | The classic W-2 scenario. A roughly year-long plan is usually approvable; a granted waiver can claw back the 10% penalty. |

| $10,000 – $50,000 | Negotiated plan; lien risk is live | Monthly payments on a short term get steep — a $30,000 balance over 12 months is $2,500/month before interest. Expect financial disclosure and possible lien filing even with a plan. |

| Over $50,000 | Professional representation from day one | Enforcement attention rises sharply, business balances bring personal-liability questions, and Offer of Compromise math may genuinely be in play. |

What an $8,900 Connecticut tax debt actually costs (worked example)

Say you're a single W-2 employee who owes $8,900 on your Connecticut return — filed on time, unpaid because two jobs left your withholding short. This is hypothetical, but the arithmetic is DRS's standard math:

- Late-payment penalty: 10% of the tax due — 0.10 × $8,900 = $890, added to the balance.

- Interest: 1% per month on the unpaid tax — about $89 every month the $8,900 sits there.

- Do nothing for a year: $8,900 + $890 penalty + ($89 × 12 = $1,068 interest) ≈ $10,858 — the debt grows roughly 22% in twelve months, before any enforcement costs.

- Start a 12-month plan today instead: roughly $816/month against the $9,790 balance, plus interest that starts near $89 and shrinks as the principal falls — total interest in the ballpark of $580 instead of $1,068 and climbing. No lien, no warrant, no intercepted refunds.

- Win the penalty waiver too and the $890 comes back off, bringing the payoff close to the original tax plus interest.

One practical note: because DRS interest runs 12% a year on top of an already-assessed penalty, a personal loan or promotional-rate card below that cost can beat the state's terms. Run the comparison before you commit to a plan.

Connecticut DRS vs. the IRS: what's different when you owe the state

DRS is a smaller, faster, less forgiving creditor than the IRS — and the two debts must be resolved separately, because the agencies don't coordinate.

| Feature | Connecticut DRS | IRS |

|---|---|---|

| Interest | 1% per month (12%/year), set by statute | Rate set quarterly by law, compounds daily |

| Late-payment penalty | 10% of the tax due, one-time | 0.5% per month, capped over time |

| Payment plans | Typically short — often around 12 months via myconneCT; longer terms need DRS approval | Up to 72 months online for balances under $50,000 |

| Settlement program | Offer of Compromise — granted sparingly, full disclosure required | Offer in Compromise — $205 fee; roughly 1 in 5 offers accepted in FY2024 |

| Collection time limit | No taxpayer-friendly 10-year rule; liens can extend enforceability for many years | 10 years from assessment (CSED), with tolling exceptions |

| Pre-levy warnings | Fewer stages; no CDP-hearing equivalent before a warrant | Multi-notice ladder ending in a 30-day final notice with appeal rights |

If you owe both, sequence matters. Connecticut's higher carrying cost and faster enforcement usually argue for clearing the state first while parking the federal balance on a longer plan — our walkthrough on how to set up an IRS payment plan online covers that side, and you can estimate what the federal penalties and interest are adding with our IRS Penalty & Interest Calculator. Two cross-agency traps to know: the IRS can seize your Connecticut refund through the State Income Tax Levy Program, and Connecticut can reach your federal refund through the Treasury Offset Program — so a refund from either government is exposed until both balances are handled.

How to respond to Connecticut back taxes, step by step

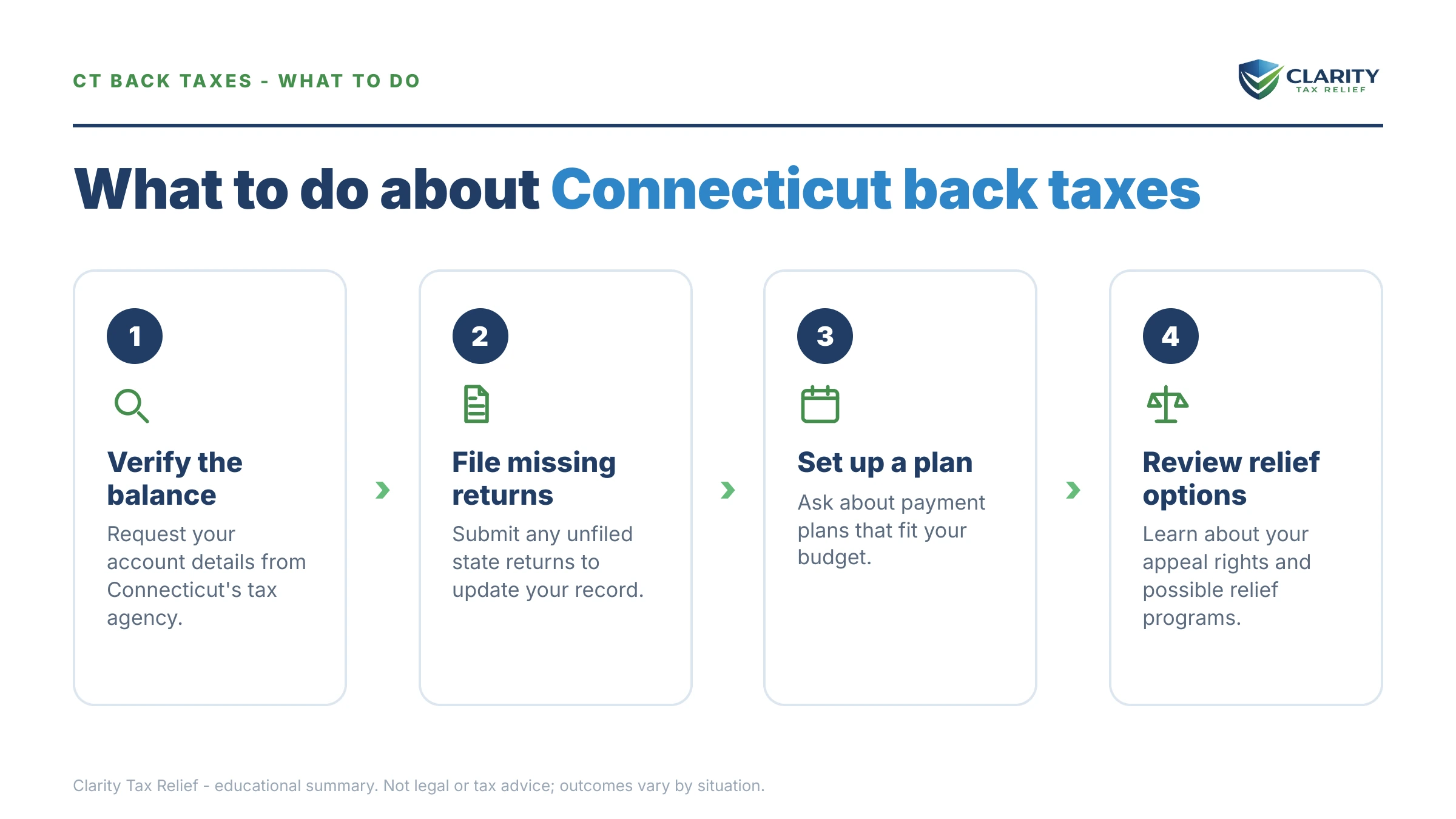

- Verify what DRS says you owe — log into myconneCT, pull up your account, and match the balance, tax year, and due date against the notice in your hand before you pay anything.

- File every missing Connecticut return — DRS will not approve a payment plan, penalty waiver, or Offer of Compromise while returns are outstanding, and your own return almost always beats a DRS estimate.

- Pick your resolution path — pay in full, request a payment plan through myconneCT, ask for a reasonable-cause penalty waiver, or, if your finances genuinely cannot cover the debt, evaluate an Offer of Compromise.

- Set it up before your notice due date — an arrangement in place before the due date keeps your account out of Collections and Enforcement, where liens and warrants start.

- Handle any IRS balance on a parallel track — the two debts are separate, the agencies do not coordinate your payments, and ignoring one to pay the other invites enforcement from the one you ignored.

Payments to Connecticut go through myconneCT on the Connecticut Department of Revenue Services website; federal payments go only through IRS.gov/payments. Anyone directing you anywhere else — gift cards, wire transfers, payment apps — is a scammer, not a tax agency.

Situations that change the Connecticut playbook

Married filing jointly. Both spouses are liable for the full joint balance, and DRS can pursue either of you. If the debt traces to a spouse's income you knew nothing about, Connecticut has its own spousal-relief process — don't assume an IRS innocent-spouse grant automatically fixes the state side.

Self-employed and 1099 workers. Your fix has two halves: resolve the old balance, and start Connecticut quarterly estimates now so next April doesn't rebuild it. DRS looks hard at whether you're staying current before approving anything.

Business owners. Connecticut sales tax and employee withholding are trust taxes — money collected on the state's behalf — and responsible individuals can be held personally liable for them, even after the business closes. Enforcement here is faster and harsher than on income tax, and unresolved balances can jeopardize permit and license renewals. See our guide to sales tax debt help before you talk to DRS.

You dispute the assessment. Every DRS assessment notice prints a protest window. Miss it and the assessment becomes final — collectible even if it's wrong. If the number looks off, appeal first and negotiate payment second; the order is everything.

You've left Connecticut. DRS collects nationwide, and neighboring states run their own aggressive programs — if your history spans state lines, our guides to New York state back taxes and Massachusetts back taxes map those systems.

When you can handle this yourself — and when help changes the outcome

Be honest with yourself about which case you have, because plenty of Connecticut back-tax problems don't need professional help.

Handle it yourself when: the balance is a few thousand dollars or less, you agree with the number, all your returns are filed, and a roughly year-long payment plan fits your budget. Set it up in myconneCT, request the penalty waiver in writing if you have real reasonable cause, and you're done.

Get experienced help when: a lien has been recorded or a warrant is in motion against your bank or wages; you have multiple unfiled years and DRS has assessed estimates against you; the debt includes business sales tax or withholding with personal-liability exposure; you're weighing an Offer of Compromise, where the financial disclosure makes or breaks the result; or you owe the IRS and Connecticut at once and the sequencing genuinely determines what you pay. In those cases, the gap between a decent outcome and an expensive one is usually the paperwork and the order of operations — exactly what experienced tax professionals do daily.

If you're in the Hartford area and want to talk through a DRS notice with someone who handles Connecticut cases, start with our tax relief in Hartford guide — or skip straight to a free case review of your notice.

Terms on your DRS notice, decoded

- Assessment — DRS's official determination that you owe a specific amount for a specific year; once final, it's collectible even if it's wrong.

- Tax lien — a public claim DRS records against your real property with the town clerk; it doesn't take anything, but it blocks clean sales and refinances.

- Warrant — Connecticut's enforcement instrument: served on your bank it seizes funds, served on your employer it garnishes wages. The state counterpart of an IRS levy.

- myconneCT — DRS's online portal, where you can see your balance, file returns, make payments, and request a payment plan.

- Offer of Compromise — DRS's program for settling a debt for less than the full amount when liability or full collection is genuinely in doubt.

- Reasonable cause — the standard for waiving penalties: a documented event beyond your control, not an inability to pay.

Connecticut back taxes: questions people ask

Can the Connecticut DRS garnish my wages?

Yes. DRS can serve a warrant on your employer that takes a portion of every paycheck until the debt is resolved — Connecticut's counterpart to an IRS wage levy, and it is continuous, not one-time. Setting up a payment plan before enforcement starts is almost always cheaper and less disruptive than trying to release a garnishment after your employer has already been served.

Does Connecticut tax debt expire after 10 years?

No — the 10-year rule people cite is the IRS collection statute, and it does not apply to Connecticut. DRS operates under its own state deadlines, and a recorded tax lien can keep a debt enforceable against your property for many years. Do not plan around expiration; confirm what applies to your specific tax years with DRS or an experienced tax professional.

Can I get a payment plan for Connecticut back taxes?

Yes. DRS offers installment plans, and many individual taxpayers can request one online through the myconneCT portal. Connecticut plans are generally much shorter than the IRS's 72-month agreements — often around a year — so expect a higher monthly payment for the same balance. Interest continues at 1% per month while you pay, and staying current on new taxes is a condition of keeping the plan.

Does Connecticut have an offer in compromise program?

Yes — DRS calls it an Offer of Compromise, and it is granted sparingly. You generally must show genuine doubt that you owe the tax or genuine doubt that DRS could ever collect it in full, supported by complete financial documentation. It is not a discount for asking; a W-2 earner with steady income and some equity will usually be steered to a payment plan instead.

Can Connecticut take my federal tax refund for state back taxes?

It can happen. States can submit unpaid state income tax debts to the federal Treasury Offset Program, which intercepts federal refunds to pay them. Connecticut can also keep your state refund every year and apply it to the balance until it is gone. If a refund you were counting on disappears, the offset notice you receive will name the agency that took it.

What penalties does Connecticut charge on back taxes?

For late-paid income tax, DRS's standard penalty is 10% of the tax due, and interest accrues at 1% per month — 12% a year — on the unpaid tax. The penalty can be waived for documented reasonable cause, but interest generally cannot be waived. On an $8,900 balance, the late-payment penalty alone is $890.

Will DRS waive penalties or interest?

DRS will consider waiving penalties when you document reasonable cause — a serious illness, a disaster, circumstances genuinely beyond your control — not simply a tight budget. Requests go through DRS's penalty review process with your evidence attached. Interest is set by statute and is generally not waivable, which is why paying the tax itself down fast usually saves more than the waiver does.

I owe both the IRS and Connecticut — which do I pay first?

Usually the agency closer to enforcement — and state agencies often move faster than the IRS. Compare where each account stands: a DRS warrant in motion outranks an IRS reminder notice. Connecticut's short plans and 1%-per-month interest also argue for clearing the state balance first while using the IRS's longer payment plans to keep the federal side manageable.

What if I never filed my Connecticut returns?

File them — DRS learns about your income through information sharing with the IRS and can assess tax against non-filers based on that data, without the deductions and credits you are entitled to. Filing your own returns almost always produces a smaller balance than a DRS estimate. Once the returns are in, you can set up a plan or request penalty relief on the real number.

Is there a Connecticut tax amnesty in 2026?

No amnesty program is currently announced. Connecticut has run amnesty windows periodically in past years, offering reduced interest to taxpayers who came forward, but waiting for the next one is a gamble — interest accrues at 1% per month while you wait, and DRS enforcement does not pause. Resolve the balance now; if a future amnesty offers better terms, you will have paid less interest in the meantime.

Your next 24 hours

- Find two things on your DRS notice: the due date and the tax year. Those tell you how much time you have and which return the balance comes from — and whether the number even matches your records.

- Gather your file: the notice itself, your most recent Connecticut and federal returns, and your last few pay stubs. That's everything needed to price a payment plan or build a penalty-waiver request.

- Get the notice reviewed free: use the 2-minute form or call (888) 825-7779. An experienced tax professional will tell you where your account sits in the DRS sequence and which option fits your $8,900 — or $89,000 — before another month of 1% interest posts.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed. State program terms are set by the Connecticut Department of Revenue Services and can change — confirm current details with DRS.