IRS Notices

IRS CP22A Notice: What It Means, Your Deadline, and What to Do (2026)

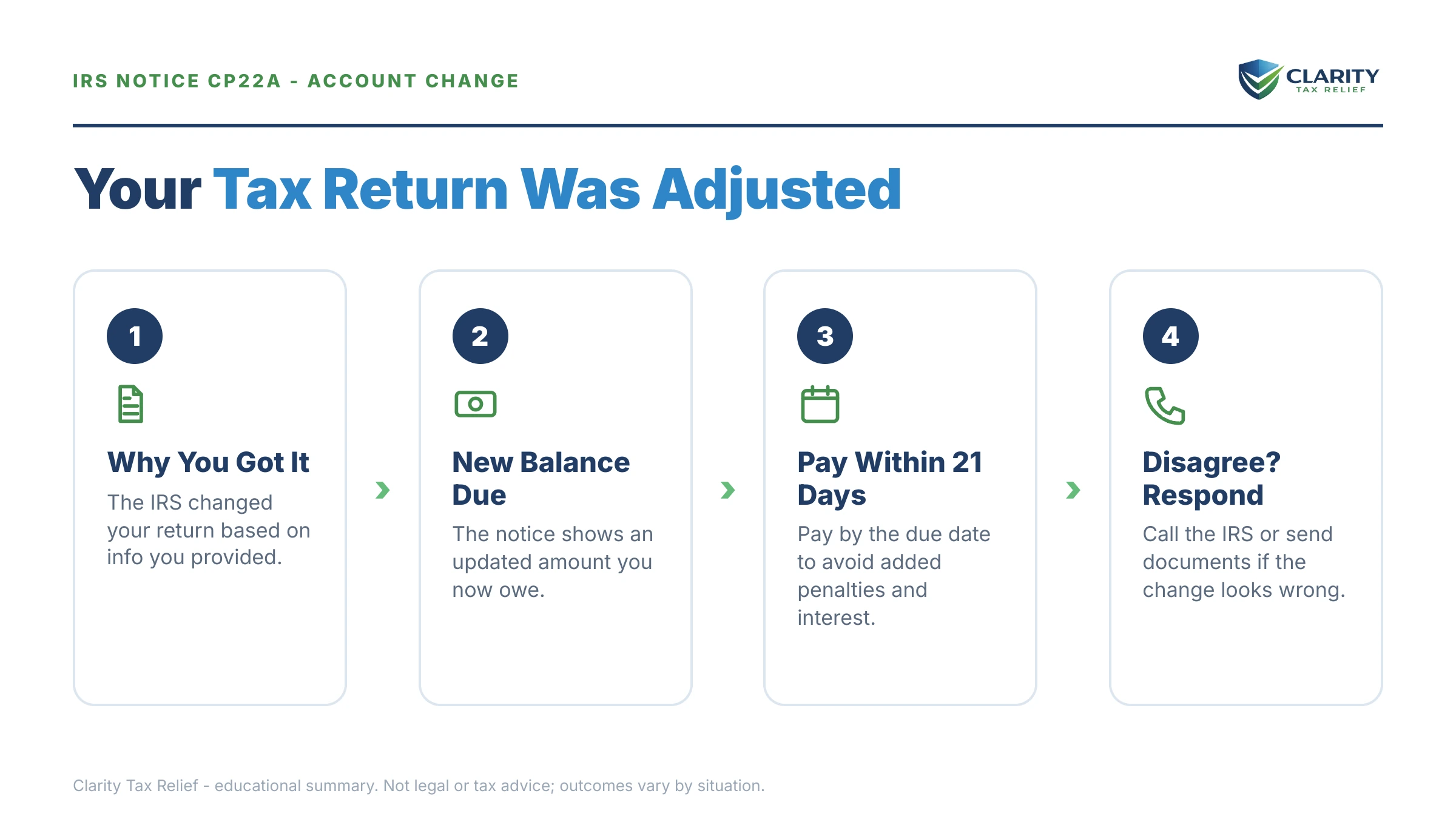

The short answer: a CP22A notice means the IRS made changes you requested to your tax return — usually from an amended return — and the changes left you owing money. Verify the changes match what you asked for, then pay or set up a payment plan by the date printed on the notice, typically about 21 days out.

You sent the IRS a correction — a Form 1040-X, a letter, maybe a phone request — and after months of waiting, the answer that finally arrived is a bill. It stings to do the right thing and owe more for it. But a CP22A is one of the most predictable notices the IRS sends, and every good option for handling the balance is still on the table today.

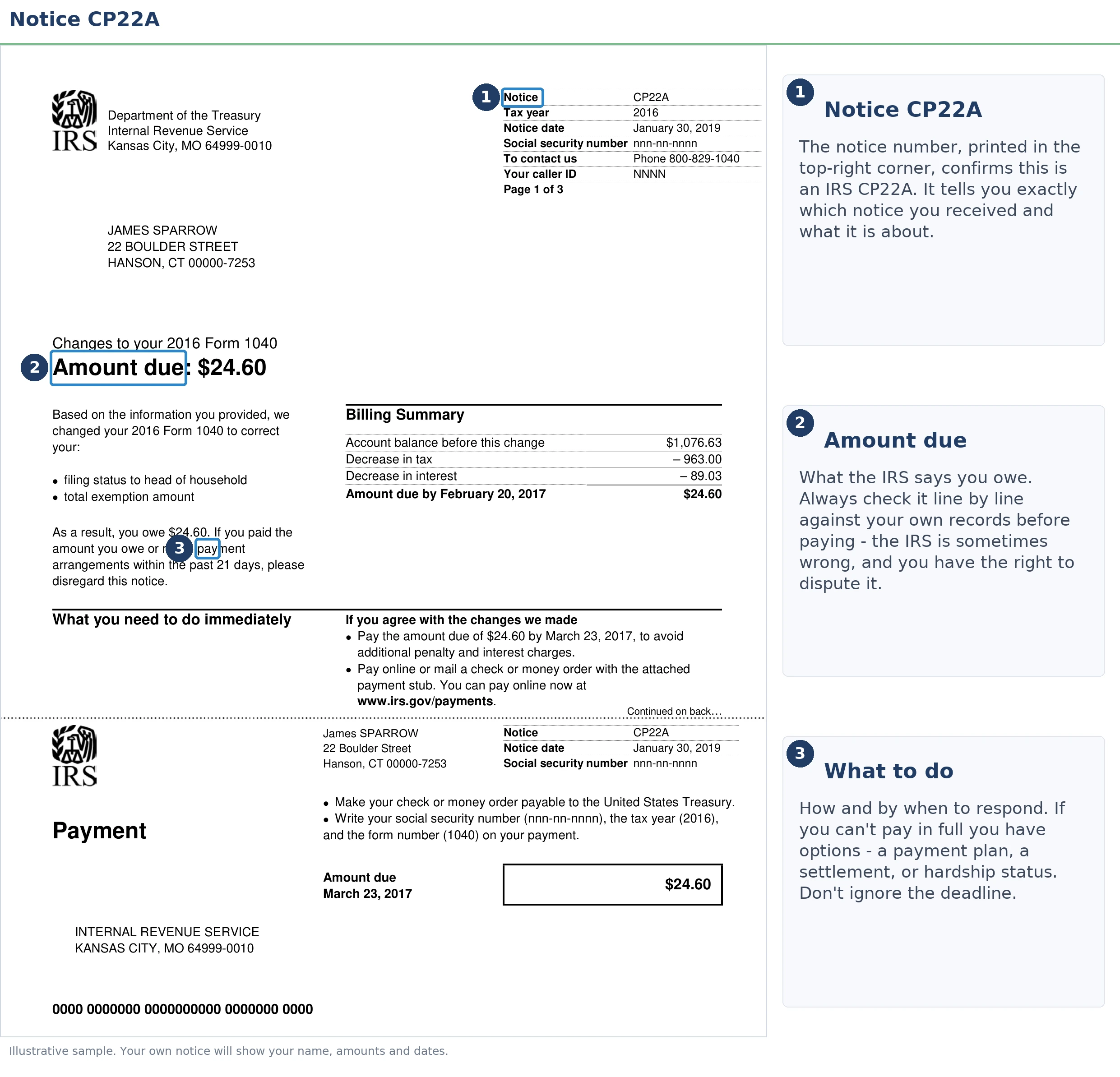

Two things make this notice different from most IRS mail. First, you set it in motion: the changes on it should match a request you made. Second, the amount is often bigger than the figure you calculated on your amendment, because interest on a CP22A balance is generally computed from the original due date of that year's return — not from the day your change was processed. The image below shows exactly what a CP22A looks like and where to find the two items that control everything: the notice date and the amount due.

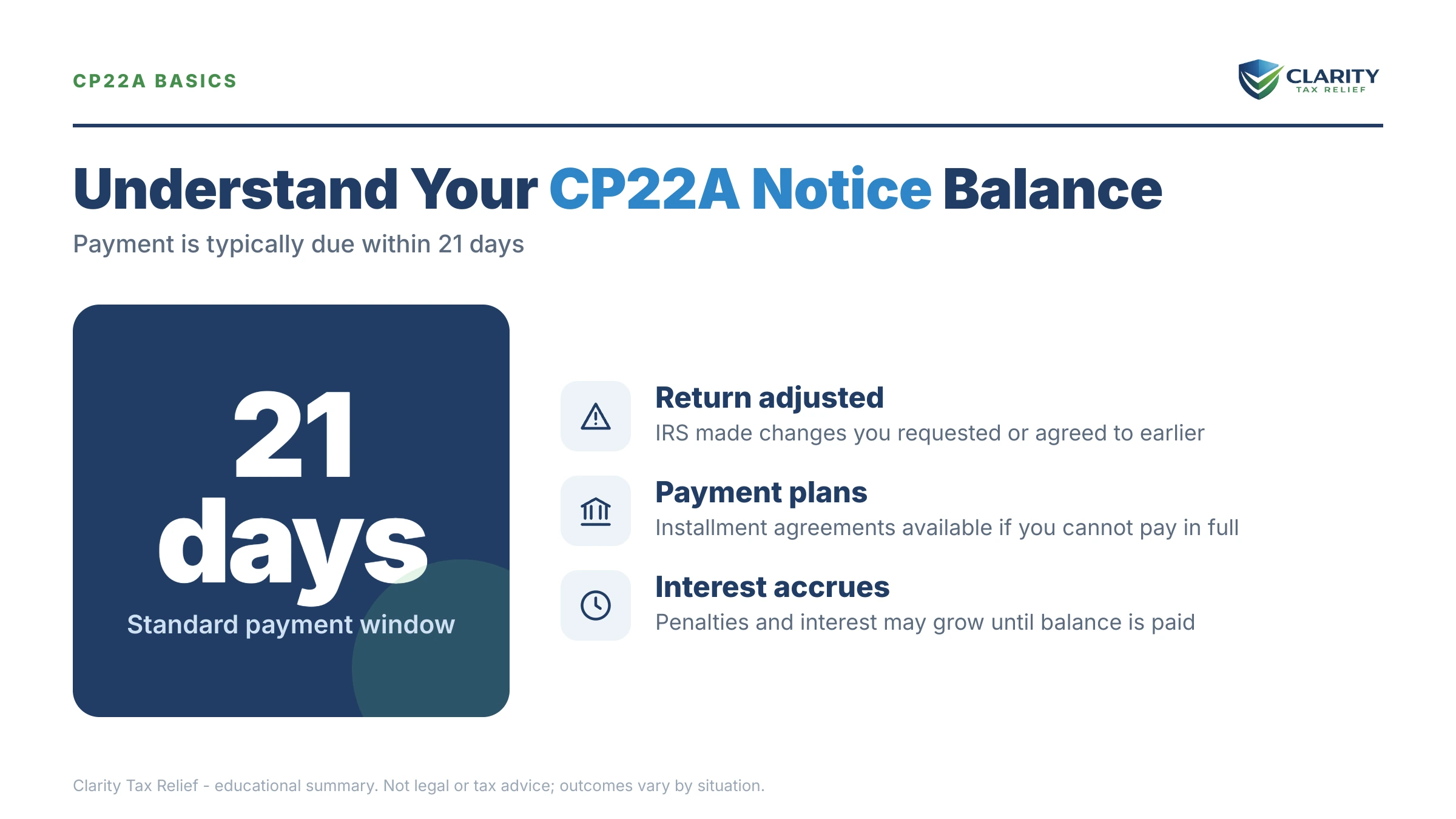

⏱ Your deadline: the "pay by" date printed on your CP22A — typically 21 days from the notice date. After that date, the 0.5% monthly failure-to-pay penalty and daily-compounding interest keep growing the balance, and the IRS's automated system queues the first collection reminder. Use the date printed on your notice, not an estimate.

Why you got a CP22A notice

A CP22A is issued when the IRS processes a change you requested to a filed return and the change produces a balance due. The most common trigger by far is a Form 1040-X amended return — you fixed something the original return got wrong (unreported retirement income, a corrected 1099, a dependent change, a credit you shouldn't have claimed), and the corrected math came out against you. But it isn't only amendments: corrections requested by phone or mail, filing-status changes, and injured spouse allocations can all land as a CP22A.

The notice shows the tax year, a "changes to your return" section describing what was adjusted, and the new balance broken into tax, penalties, and interest. If the general question "why is the IRS writing to me at all" is still nagging you, our decoder on why did I get a letter from the IRS covers the whole notice universe — this page stays focused on the CP22A specifically.

Just as important is what a CP22A is not. It is not an audit and not a proposal you can still argue down through an exam process — the change is already assessed. It is also not a math-error correction the IRS made on its own; those arrive as a CP11 notice when you owe or a CP12 notice when your refund changed. And it is not the near-twin CP21A notice's exam cousin: changes that come out of an audit arrive on a CP22E notice, which carries different appeal rights.

First: confirm the changes match what you requested

A CP22A is only as correct as the request behind it, so ten minutes of comparison protects you from paying a mistake. Before any money moves:

- Set the notice next to your 1040-X or correction letter. The "changes to your return" section should mirror what you submitted, line by line. Amendments occasionally get keyed in with a transposed figure or applied to the wrong tax year.

- Reconcile the dollar difference. If your 1040-X showed $2,400 due and the notice says $2,760, the gap is usually backdated interest plus the failure-to-pay penalty — legitimate, but worth confirming against the notice's breakdown.

- Check your IRS online account. If you sent a payment with your amendment, confirm it posted to the right year. Payments and notices cross in the mail constantly.

- Screen for scams. A real CP22A arrives by postal mail, never email or text, and real payments go only to the United States Treasury or through IRS.gov — never gift cards, wire transfers, or payment apps.

If you never requested any change at all, don't pay — call the number on the notice. Sometimes an adjustment lands on the wrong account; rarely, it means someone submitted paperwork in your name, which is worth reporting on Form 14039.

What happens if you ignore a CP22A

An unpaid CP22A balance enters the same automated collection sequence as any assessed IRS debt — reminders, then a levy warning, then a final notice that unlocks real enforcement. Until it's resolved, the balance grows by a 0.5% monthly failure-to-pay penalty plus interest that compounds daily. Here's the order of what follows:

- CP22A — the bill for the changes you requested. You are here. No lien, no levy — this is the cheapest moment to act.

- CP501 / CP503 — reminder notices for the same balance, each arriving with more accrued penalty and interest attached.

- CP504 notice — Notice of Intent to Levy. The IRS can now seize your state tax refund, and a federal tax lien becomes a realistic next step.

- LT11 notice / Letter 1058 — Final Notice of Intent to Levy. This starts a 30-day clock and your Collection Due Process appeal rights. After the 30 days, bank levies and wage levies are authorized.

- Levy — enforcement. Levied bank funds are held 21 days before they're sent to the IRS; wage levies continue paycheck after paycheck until released. If you're on Social Security, the Federal Payment Levy Program can take up to 15% of your benefit continuously.

In 2026 this sequence runs with almost no human involvement. The IRS workforce shrank roughly 27% in 2025, which makes the agency harder to reach by phone — but the notices, liens, and levies come from automated systems that never stopped. Waiting for a person to intervene is not a strategy.

| Notice | What it means | What the IRS can do at this stage |

|---|---|---|

| CP22A | Bill for the changes you requested | Nothing yet — collection hasn't started; penalties and interest accrue |

| CP501 / CP503 | Automated reminders of the same balance | Still just billing, but future refunds are now offset automatically |

| CP504 | Notice of Intent to Levy | Seize your state tax refund; a federal tax lien becomes likely |

| LT11 / Letter 1058 | Final Notice of Intent to Levy | After a 30-day window, levy bank accounts, wages, and up to 15% of Social Security |

| Levy | Active enforcement | Bank funds held 21 days, then sent to the IRS; wage levies continue until released |

Holding a CP22A right now?

A CP22A has one controlling date — the pay-by date printed on it. Get your notice reviewed free before that date passes: an experienced tax professional will confirm the changes match what you requested and map the cheapest way to handle the balance. Call (888) 825-7779 or use the 2-minute form.

CP22A payment options when you can't pay in full

The IRS offers four real paths for a CP22A balance you can't pay at once: a 180-day short-term plan, a monthly installment agreement, hardship status, and — in narrow cases — an Offer in Compromise. Which one fits depends mostly on the size of the balance and what your monthly budget can genuinely absorb:

- Short-term payment plan — up to 180 days to pay in full, with a $0 setup fee. Interest and the late-payment penalty continue, but the account never enters the collection sequence.

- Installment agreement — a monthly plan requested online, or by mail on Form 9465. Balances up to $50,000 can be spread over as long as 72 months without detailed financial disclosure; our walkthrough on how to set up an IRS payment plan online covers the whole process screen by screen.

- Currently Not Collectible status — if paying anything would leave you unable to cover basic living costs, collection can be paused. The debt remains and the 10-year collection statute keeps running, but levies and garnishments stop. This matters most for readers on fixed incomes — see our guide for people who are retired and owe back taxes.

- Offer in Compromise — settling for less than the full balance. It's real, but strictly means-tested: the IRS accepted roughly 1 in 5 offers in FY2024, and approval depends on math showing the debt exceeds what the IRS could ever collect from your income and assets.

- Penalty relief — if your prior three years are clean, first-time penalty abatement can remove the failure-to-pay penalty. And starting summer 2026, the IRS's new Automatic Exemption from Penalty (AEP) applies qualifying relief automatically, with no request needed. You can estimate what penalties and interest are adding to your balance with our IRS penalty and interest calculator.

| If your CP22A balance is | Realistic options | What it takes |

|---|---|---|

| Under $10,000 | Guaranteed installment agreement or 180-day short-term plan | All required returns filed; set up online in minutes with no financial disclosure |

| $10,000 – $25,000 | Streamlined installment agreement | No Form 433 financials; payments spread over up to 72 months |

| $25,001 – $50,000 | Streamlined agreement with direct debit (a $48,300 balance sits here) | Direct debit from a bank account is typically required; still no financial disclosure |

| Over $50,000 | Negotiated installment agreement, CNC, or Offer in Compromise | Full financial disclosure on Form 433-F before the IRS agrees to terms |

| Any amount, genuine hardship | Currently Not Collectible or Offer in Compromise | Proof that paying would leave you unable to cover allowable living expenses |

A worked example: a $48,300 CP22A on a fixed income

Say you're retired, living on Social Security and a small pension, and the 1040-X you filed to report a large IRA distribution the original return missed comes back as a CP22A for $48,300. This is hypothetical, but the math is real:

- Installment agreement: $48,300 is under the $50,000 online threshold, so a 72-month plan is available without financial disclosure. The base math is $48,300 ÷ 72 ≈ $671 a month — and because interest and the 0.5% monthly late-payment penalty keep accruing inside the plan, the real cost runs higher, so any month you can pay extra shortens the tail meaningfully.

- Hardship route: if your income is, say, $2,150 in Social Security plus $600 of pension ($2,750 total) and your allowable living expenses run $2,900, there's no $671 in that budget. That gap is exactly what Currently Not Collectible status exists for — collection pauses while the 10-year clock keeps running.

- Offer in Compromise reality check: the same retiree with $120,000 of home equity is unlikely to qualify, because the IRS counts that equity as collectable. With little equity and expenses exceeding income, an offer becomes genuinely worth pricing out.

Notice that all three paths start from the same document: an honest monthly budget. Which one is cheapest depends entirely on your numbers, not on which program sounds best.

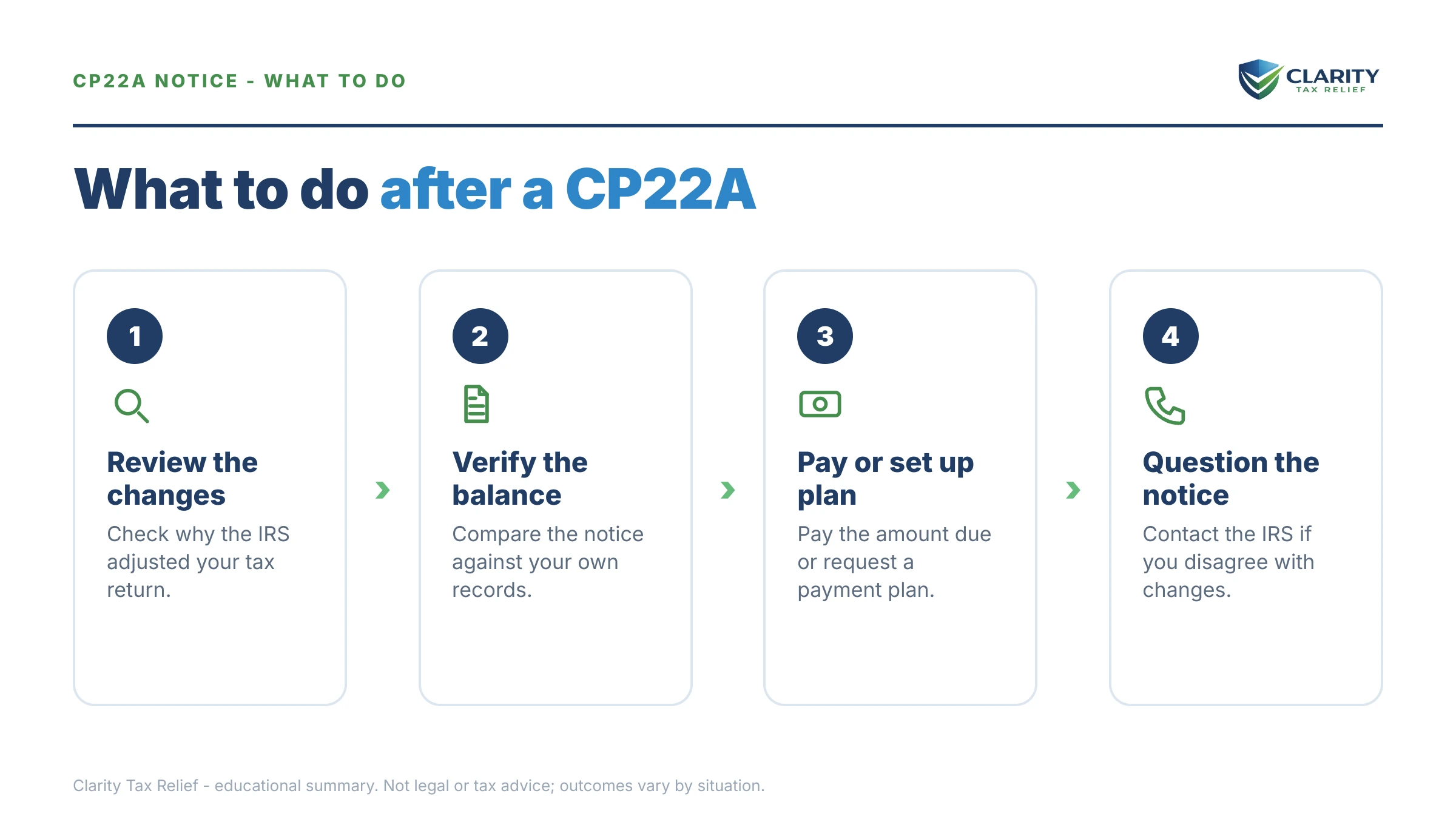

How to respond to a CP22A notice, step by step

- Pull your change request: set your Form 1040-X or correction letter next to the notice's 'changes to your return' section and compare line by line.

- Verify the balance: log into your IRS online account and confirm the assessment, the tax year, and any payments already posted.

- Pay what you can by the printed date: even a partial payment at IRS.gov/payments shrinks the base that penalties and interest compound on.

- Set up a plan if you can't pay in full: balances up to $50,000 qualify for an online installment agreement of up to 72 months.

- Dispute in writing if the changes are wrong: call the number on the notice, send documentation, and keep copies of everything.

- Get a professional review for large or hardship cases: a balance near $50,000 on a fixed income deserves a strategy check before you commit to terms.

The IRS's own explainer lives at Understanding your CP22A notice, payments go through IRS.gov/payments, and plan details are on the IRS payment plans page.

When you can handle a CP22A yourself

Most CP22A recipients don't need professional help — and it would be dishonest to tell you otherwise. If the changes match your request and you can pay in full or within 180 days, handle it yourself online — the whole thing takes an evening. The same goes for a balance under $25,000 you can comfortably cover with a streamlined monthly plan.

Experienced help changes outcomes in a narrower set of situations: the balance sits near or above $50,000, where terms are negotiated rather than automatic; you're on a fixed income where the "obvious" payment plan would quietly starve your budget when hardship status fits better; the notice covers one year but other years are unfiled or unpaid; or you believe the adjustment itself is wrong and the phone-and-letter dispute is going nowhere. In those cases, the order you fix things in — returns first, penalties second, balance last — changes what you ultimately pay.

Terms on your CP22A, decoded

- Assessment — the formal recording of tax on your account; once the CP22A change is assessed, the IRS can collect it like any other tax debt.

- Form 1040-X — the amended-return form that triggers most CP22A notices; keep your copy, because it's your proof of what you actually requested.

- Notice date vs. pay-by date — the notice date starts the clock; the pay-by date printed near the amount due is the deadline that matters.

- Failure-to-pay penalty — 0.5% of the unpaid tax per month, stacked on top of interest, until the balance is resolved or the penalty is abated.

- Federal Payment Levy Program (FPLP) — the automated system that can take up to 15% of Social Security benefits once a debt reaches the final-notice stage.

- CSED — the collection statute expiration date; the IRS generally has 10 years from assessment to collect, though certain actions pause that clock.

CP22A questions, answered

Why did I get a CP22A notice if I never amended my return?

A CP22A can follow any change the IRS recorded as requested by you — a correction made by phone or mail, an injured spouse allocation, or a dependent or filing-status fix — not just a Form 1040-X. If you genuinely requested nothing, call the number on the notice right away; occasionally a change is applied to the wrong account, and in rare cases it signals someone filed paperwork in your name, which is worth reporting on Form 14039.

What is the difference between a CP21A and a CP22A notice?

Both notices confirm that the IRS made changes you requested to your return and that you owe money as a result — the difference comes down to which IRS processing path handled the adjustment, not to anything you did differently. Your response is identical either way: verify the changes against what you actually requested, then pay or arrange payment by the date printed on the notice.

How long do I have to pay a CP22A notice?

Your deadline is the pay-by date printed on the notice, which typically falls about 21 days after the notice date. Interest and the 0.5% monthly failure-to-pay penalty continue to accrue after that date, and the balance moves into the IRS's automated reminder sequence. Setting up a payment plan by the printed date keeps the account out of collections entirely.

Can I set up a payment plan for a CP22A balance?

Yes. A short-term plan gives you up to 180 days to pay in full with no setup fee, and balances up to $50,000 can go on a monthly installment agreement online for up to 72 months. Above $50,000, the IRS requires financial disclosure before agreeing to terms. Interest and penalties continue during any plan, so paying faster always costs less.

What if I disagree with the changes on my CP22A?

Call the number printed on the notice and have your amended return or correction request in front of you — if the IRS applied a change incorrectly, it can reverse or adjust the assessment. Follow up in writing with copies of your documentation and keep proof of everything you send. Don't simply ignore the notice while you dispute it; the balance keeps accruing interest until the account is corrected.

Can the IRS take my Social Security to collect a CP22A balance?

Not at this stage — a CP22A carries no enforcement power by itself. But if the balance escalates unanswered through the full notice sequence to a final notice of intent to levy, the Federal Payment Levy Program can take up to 15% of your Social Security benefit continuously until the debt is resolved. You get 30 days and formal appeal rights before that final step.

Will the IRS keep my tax refunds until the CP22A balance is paid?

Yes. Any federal refund you're owed in a future year is applied automatically to the outstanding balance, even if you're current on a payment plan. State refunds can also be intercepted once the account escalates to the CP504 stage, where the IRS gains the power to levy state tax refunds.

Is a CP22A notice an audit?

No. A CP22A reflects changes you asked for, not an examination of your return — nobody is questioning your deductions or requesting receipts. Changes that come out of an actual audit arrive on a CP22E notice instead, and proposed changes the IRS initiates from mismatched income documents come on a CP2000. Each of those has different response rights and deadlines.

Your next 24 hours

- Find two things on your notice: the pay-by date (near the amount due on the first page) and the "changes to your return" section. Those two items decide your timeline and whether the bill is even right.

- Gather three documents: your copy of the 1040-X or correction request, the return for the tax year on the notice, and a rough monthly income-and-expense picture if you can't pay in full.

- Get the notice reviewed free before your pay-by date passes: send it through the 2-minute form or call (888) 825-7779, and an experienced tax professional will confirm the changes are correct and price out your cheapest path.

This guide is general information, not tax or legal advice for your specific situation. Eligibility for IRS programs depends on individual facts and circumstances; no outcome is guaranteed.